Among the major banks, Commonwealth Bank is least favoured due to its exposure to the mortgage market and the weakest capital position among its peers.

Big Australian banks could still face increased risk weightings on their mortgage loan books, regardless of this month’s international banking review.

That’s the view of Morgan Stanley analysts, who argue that Australia’s bank regulator, APRA, has the scope to enforce higher risk weightings to meet its own definition of an “unquestionably strong” capital position for the banks.

Higher risk weightings for mortgages would require the majors to increase their levels of Tier 1 capital in order to meet minimum capital ratio requirements.

The analysts highlighted comments by Brad Carr, director of banking prudential policy at the Institute of International Finance. Carr said that the Basel IV requirements wouldn’t be particularly onerous on Australian banks, given their already strong capital positions in comparison to international peers.

However, Morgan Stanley is of the view that APRA could use its authority domestically to enforce stricter capital requirements in addition to the Basel IV guidelines.

Referring to Basel IV as more of a minimum international standard, the analysts highlighted recent comments from APRA about higher lending risks and the high concentration of home loans in the asset portfolios of Australian banks.

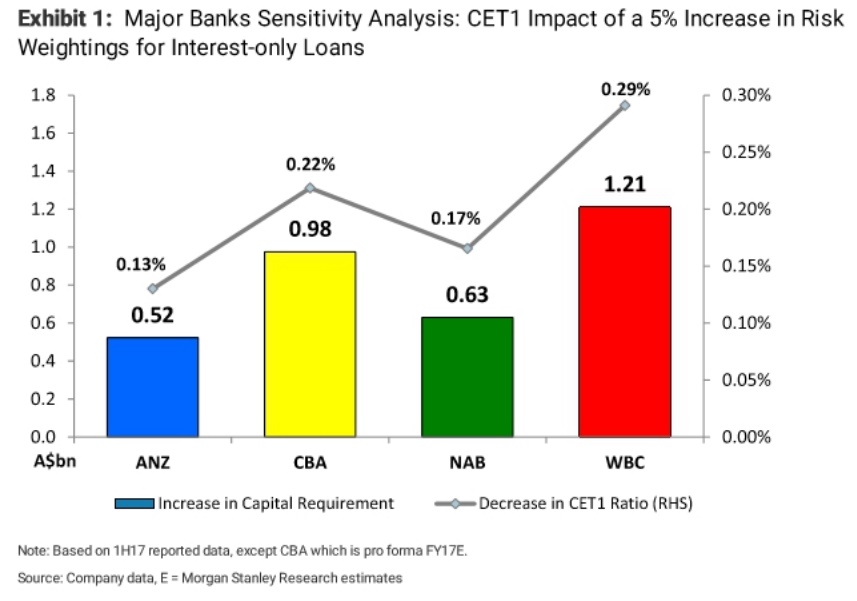

Morgan Stanley says that for every 5% increase (from the current level of 25%) will require the big 4 Australian banks to raise another $3.3 billion worth of capital:

Of the Big 4, Morgan Stanley says Westpac is the most exposed to more stringent capital requirements, given the size of its home loan portfolio.

For a 5% risk weighting increase, Westpac would be required to raise another $1.2 billion, while on the other end of the spectrum ANZ would have to raise around $500 million.

ANZ remains the favoured pick of Morgan Stanley analysts, with superior earnings per share (EPS) to its peers and a strong capital position.