Following on from yesterdays discussion about current consumer payment trends, today we will look at the current status of the New Payments Platform. “The proposed centralised infrastructure and real-time nature of the system, combined with the flexibility of payment messaging, ability to carry additional remittance information and the easy addressing capability, will mean that payments can be better integrated with many other aspects of our lives. Businesses should be able to achieve substantial efficiency gains and there will be significant improvements to the timeliness, accessibility and usability of the payments system for consumers” according to Tony Richards, the Head of Payments Policy Department at the Reserve Bank. in his recent speech The Way We Pay: Now and in the Future.

A bit of history first. The current payment infrastructure in Australia is complex, quite old and will not provide the flexibility demanded by new devices and systems. It is supported by a complex web of networks and bilateral charging arrangements, which makes it difficult for new players to enter the payments market, and so protects the current incumbents. In May 2010 the RBA announced a review of the Australian payments systems and how innovation may be improved. It took a medium-term perspective, looking at trends and developments overseas in payment systems and at possible gaps in the Australian payments system that might need to be filled over a time horizon of five to ten years. In June 2012, the conclusions from the review were published. The headline findings reflected the potential gaps in the payments system identified during the course of the Strategic Review.

In the Review, the Payments System Board (PSB) identified a number of gaps in the services currently provided by the payments system. Among these were:

- the ability for individuals to make electronic payments with real-time funds availability to the recipient

- the ability to make and receive such payments outside of normal banking hours

- the ability to address payments in a relatively simple way, such as to an individual’s mobile phone number or email address rather than to their BSB and account number

- and, most relevant for businesses, the ability to send anything more than a minimal amount of information with an electronic payment.

A key objective was the establishment of a system that would provide real-time retail payments, with real-time funds availability, by the end of 2016. The review recognised that this type of system has been a focus of innovation in a number of other countries. Finally, the bank stated that they believed that a real-time retail payment system would best be delivered by the establishment of a real-time payments hub, rather than a web of bilateral links. It is also prepared to consider helping to facilitate these payments by providing a system for real-time interbank settlement via the Reserve Bank’s RITS system, which currently provides real-time settlement for high-value transactions.

So the New Payment Platform (NPP) was born. An industry steering committee is overseeing development of the NPP. The New Payments Platform Steering Committee first met on 20 June 2013. It comprises senior representatives from the Australian banking and mutual sector, an alternative payments provider and the APCA CEO. An independent Chair, Paul Lahiff, was appointed in September 2013. The Steering Committee appointed KPMG as program manager to the project to ensure a well-resourced, highly collaborative industry program.

The programme participants are:

- Australia and New Zealand Banking Group Limited

- Australian Settlements Limited

- Bank of America Merrill Lynch

- Bank of Queensland Limited

- Bendigo and Adelaide Bank Limited

- Citigroup Pty Ltd

- Commonwealth Bank of Australia

- Cuscal Limited

- HSBC Bank Australia Limited

- Indue Ltd

- ING Bank (Australia) Limited

- Macquarie Bank Limited

- National Australia Bank Limited

- PayPal Pte Ltd

- Reserve Bank of Australia

- Suncorp Bank

- Westpac Banking Corporation

According to The Australian Payments Clearing Association CEO, Chris Hamilton, these 17 of its 87 members have agreed so far to fund the network, although the costs are not currently known. Lahiff is quoted as saying that NPP will provide “the basic “rail-tracks” on which “overlays” or payments services would be built. “It is minimalist in what it needs to do. It will be constructed as a utility that will be industry owned,” he said. “That allows networking, switching, addressing and settlement. As long as you have an interface to the basic infrastructure, it allows everybody to compete on how they use it most effectively.”

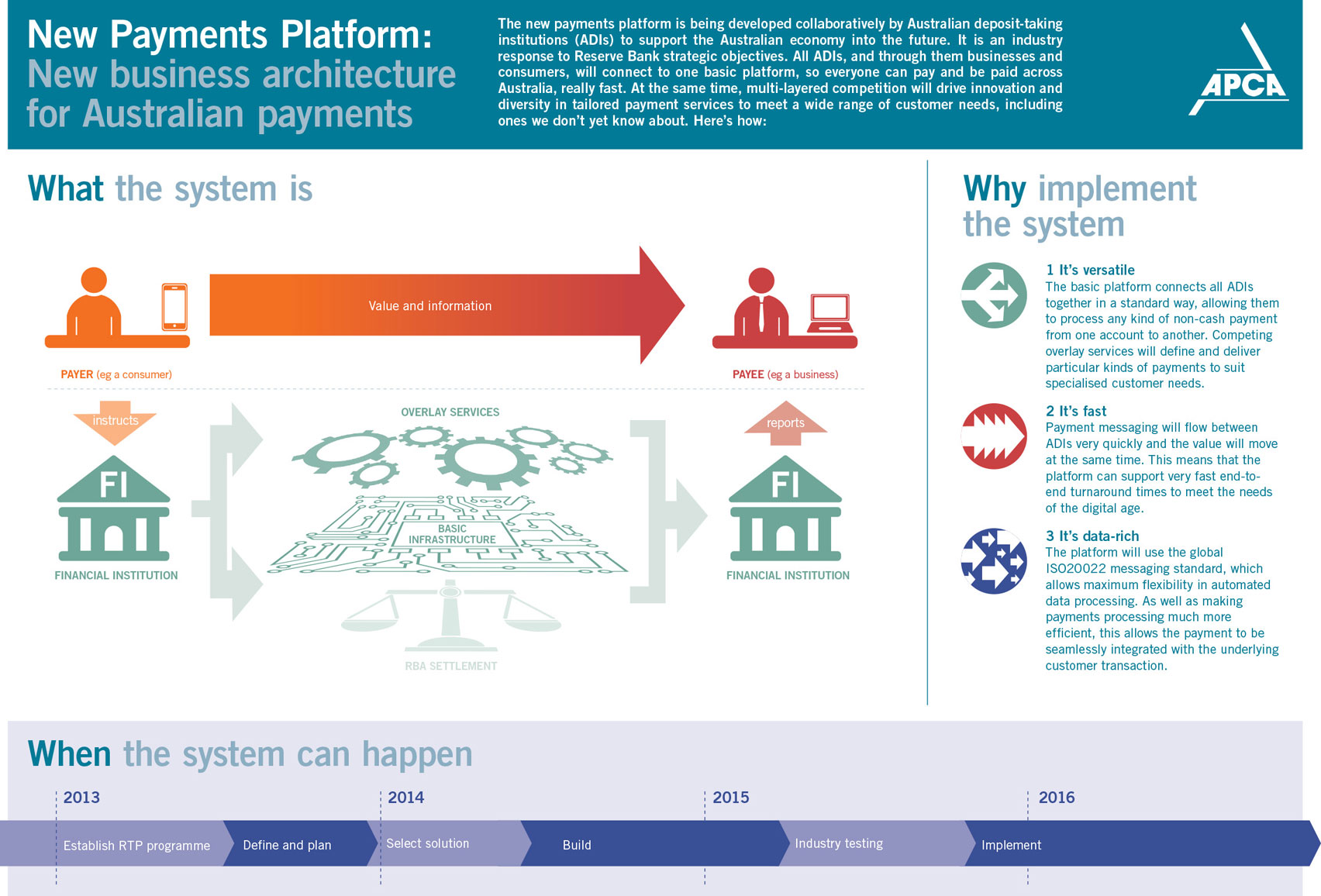

A new utility entity, owned by the payments industry will be created. Tenders were issued earlier in 2014, and responses are being considered at the moment. About 80 people are working on the project. Once the enabling infrastructure in launched, there is the prospect of additional value-added services “overlay services” being offered. Here is the schematic which APCA draws:

There are a number of issues worth reflecting on.

- The banks have considerable investments in the current bilateral systems and processes. Will they need to write off these investments if they migrate to a new platform?

- Whilst the establishment of a centralised payment switch is relatively simple (its been done elsewhere), the real challenge is to retrofit the current bank’s systems and processes into the new world. It is well known that some banks have problematic infrastructure, and as a result any migration will be complex and expensive. Banks with batch processing will have issues fitting into a real-time 24/7 world, and may need to create “shadow” real-time proxies such are used for internet banking.

- What will the revenue model which will underpin the new infrastructure be?

- Will the current 17 members put barriers in the way which means that the new payments infrastructure will be inaccessible by new players and innovators? Will new competitors be locked out?

- The intention will be to migrate from sort code and account numbers to a single number used for receiving payments. So should this infrastructure also be considered an a mechanism to establish account number portability. A number of recent submissions to the Federal Government’s financial system inquiry have proposed this.

The NPP has the potential to liberate payments and offer innovation to consumers and businesses. It is essential to evolve payments into a more innovative and open environment, we will see if NPP fits the bill.

2 thoughts on “Australia’s New Payment Platform (NPP)”