Australia’s retirement income policy is on a collision course with trends in home ownership and the result will be more older Australians struggling to support themselves in retirement. It will also make the superannuation system more inequitable.

The housing price boom is causing a major social change in Australia and the results of it are not being factored into policy making.

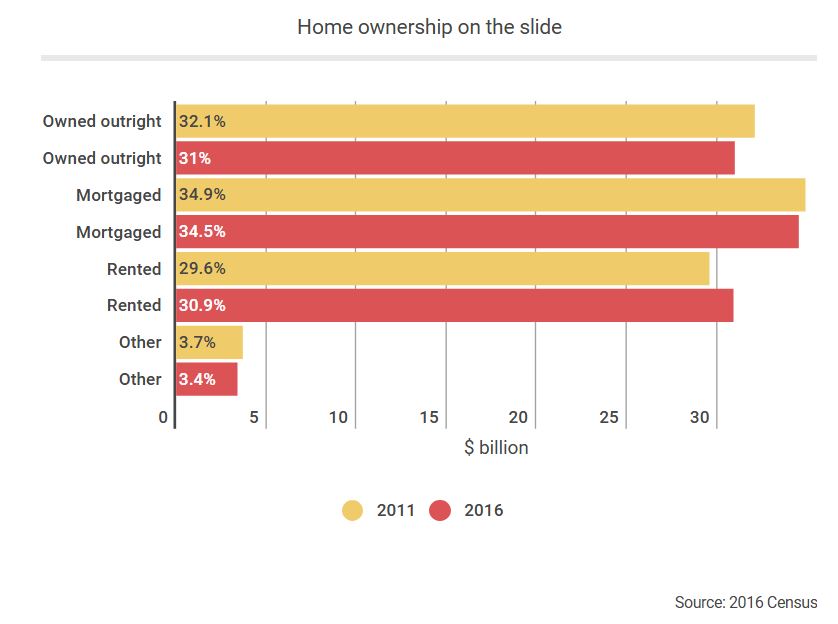

The latest figures from the 2016 census show that home ownership dropped markedly. Households renting rose to 30.9 per cent of the total, compared to 29.6 per cent in mid-2011. In the late 1980s, only 26.9 per cent of households rented.

Households owning outright dropped most markedly, from 32.1 per cent to 31 per cent while those owning with a mortgage dropped from 34.9 per cent to 34.5 per cent of households.

That is bad news for retirees because it means that more people will find themselves renting as they give up work.

“It’s a big thing because the family home is exempt from the pension assets test,” Grattan Institute research fellow Brendan Coates said.

“If you don’t own a home you will have to put aside more money to support yourself in retirement because of rental costs.”

The Association of Superannuation Funds of Australia recently found that to afford a comfortable retirement in a capital city a couple would need more than $1 million saved. That’s almost double needed by a couple who owned their home.

The trouble with saving large amounts like that is that it puts you outside the limits of the age pension assets test.

“Now most people in retirement get the pension,” Mr Coates said.

Holding a lot of assets outside the home means your pension will be discounted once you trigger the assets tests limits. And recent changes have made the situation worse.

In January this year, assets test limits for part pensions were cut by around $200,000. For single non-home owners the new limit is $747,000 and for couples $1 million, compared with $943,250 and $1.32 million previously.

So retiring without a home means many people will get less from the pension while they run down their retirement assets and will face rising rents as time goes by.

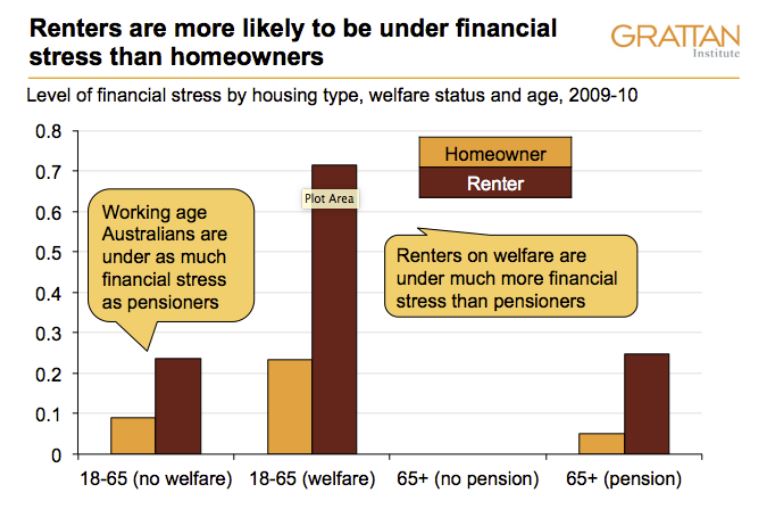

As this table from the Grattan Institute shows, renting leaves people far more vulnerable to financial stress.

While many renters on a pension may be be eligible for Commonwealth rent assistance, it maxes out at $132.20 per fortnight for a single and $124.60 for couples. Rents for a two-bedroom apartment average between $593 a week in Sydney and $329 in Adelaide (less in the regions), and have grown at around 1.6 times the rate of inflation over the past 30 years.

So being a renter will increasingly squeeze your income as your savings diminish and welfare won’t bridge the gap.

The toughening of the assets test and the rise of renting retirees “brings into stark contrast the treatment of home owners and non-home owners”, Mr Coates said.

Currently about half of age pension payments go to people with more than $500,000 in assets and 20 per cent to those with more than $1 million, most of whom are home owners.

It will also widen the gap between home owning and non-home owning superannuants as those without homes will struggle to build balances and have to spend what they have quicker to pay their housing costs.