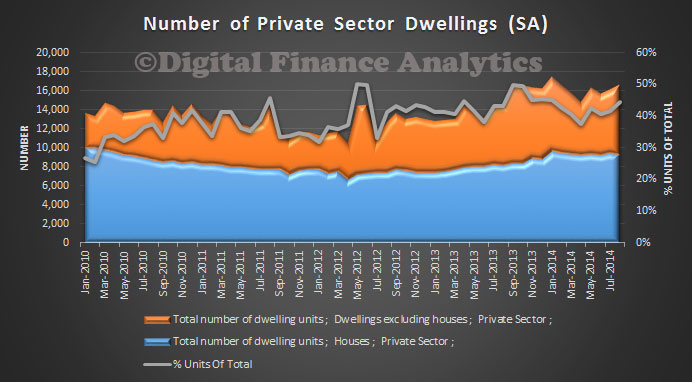

Today the ABS confirmed what we already knew, there was something weird about the employment data. When the last set came out, showing major and surprising movements, we highlighted the figures were probably not reliable. See the chart below.

Now the ABS has said

Now the ABS has said

The ABS has concluded that the seasonal pattern previously evident for the July, August and September labour force estimates is not apparent in 2014. This assessment was made while preparing labour force estimates for September 2014 and relates to all seasonally adjusted labour force estimates other than the aggregate monthly hours worked series.

As there is little evidence of seasonality in the July, August and September months for 2014, the ABS has decided that for these months the seasonal factors will be set to one (reflecting no seasonality). This means the seasonally adjusted estimates (other than for the aggregate monthly hours worked series) for these months will be the same as the original series and this will result in revisions to the previously published July and August seasonally adjusted estimates.

“It is critical that the ABS produces the best set of estimates that it can,” said acting Australian Statistician Jonathan Palmer “so that discussion is on what the estimates mean, and not the estimates themselves.

“To assist in this, the ABS will commission a review with independent external input to develop an appropriate method for seasonally adjusting October 2014 and following months’ estimates.

“The report on the results of this review will be presented in due course.”

The ABS has not made this decision lightly and believes this approach will result in a more meaningful set of seasonally adjusted estimates.

The ABS will continue to produce trend estimates and, as always, encourages users to use the trend estimates to help understand underlying movements in the labour force series.

This admission will increase the level of uncertainty about the accuracy of the data, at a time when unemployment and underemployment are set to remain high (as the IMF stated today). This is exacerbated by the recent cuts to the ABS budgets, making the sample smaller, and less reliable. We are flying somewhat blind at a time when good reliable data is essential if we are to chart a path through current uncertainties. Or maybe the inconvenient truth about rising unemployment will be muted as a result, and this was not entirely without intent.