In part 3 of this series, Damian Klassen from Walk The World Fund and Nucleus Wealth explains how views on inflation impact investment portfolio decisions, and what signs to look out for ahead to determine when to switch.

You can read his full blog post here. https://nucleuswealth.com/articles/beware-the-inflation-snap-back-how-to-invest-part-4-of-4/

Sign up to get alerted to the next release and more: https://walktheworld.nucleuswealth.com/register

Go to the Walk The World Universe at https://walktheworld.com.au/

We have found another example of power pushing out those who are trying to control the banks, and the playbook is PRECISELY the same as the Aussie Post Affair.

I discuss this with Robbie Barwick from the Citizens Party, in the context of the planned removal of Responsible Lending protections and a response to try to remove this risk. You will not believe this…

We look at the latest jobs and population statistics from the ABS, Governor Lowe’s latest outing, and Liberal party moves to try and address the housing crisis, and why they are not strategic enough.

Go to the Walk The World Universe at https://walktheworld.com.au/

This is an edited version of our live Q&A in which I discussed the latest issues in the Property Market with our insider Edwin Almeida from Ribbon Property https://www.ribbonproperty.com.au/.

CONTENTS

0:00 Start 0:19 Introduction 1:30 Edwin Joins 2:15 About Ribbon 8:10 Impact of rate rises on property prices 11:10 Chasing prices 19:20 Buy old or buy new? 29:14 RBA Failed Institution – economic threat – taming the elephant 32:29 Apartment pipeline 38:00 Tenants and rental tax 39:20 Flood-prone land and recourse 48:15 Learning to read an auction 1:00:30 Under-quoting 1:09:00 Subdivision 1:13:00 Potential growth suburbs 1:16:00 Policy failure 1:34:00 Conclusion and close

The original stream and chat replay is at: https://youtu.be/HHsehh29mIU

Go to the Walk The World Universe at https://walktheworld.com.au/

The latest edition of our finance and property news digest with a distinctively Australian flavour.

In today’s show we look at the latest property stats, discuss whether Australia’s economy is in a “triple crisis”, New Zealand’s mortgage crisis and look at more rubbish being spruiked by those who should know better.

Go to the Walk The World Universe at https://walktheworld.com.au/

Join us for a live Q&A as I discuss the latest issues in the Property Market with our insider Edwin Almeida from Ribbon Property You can ask a question live.

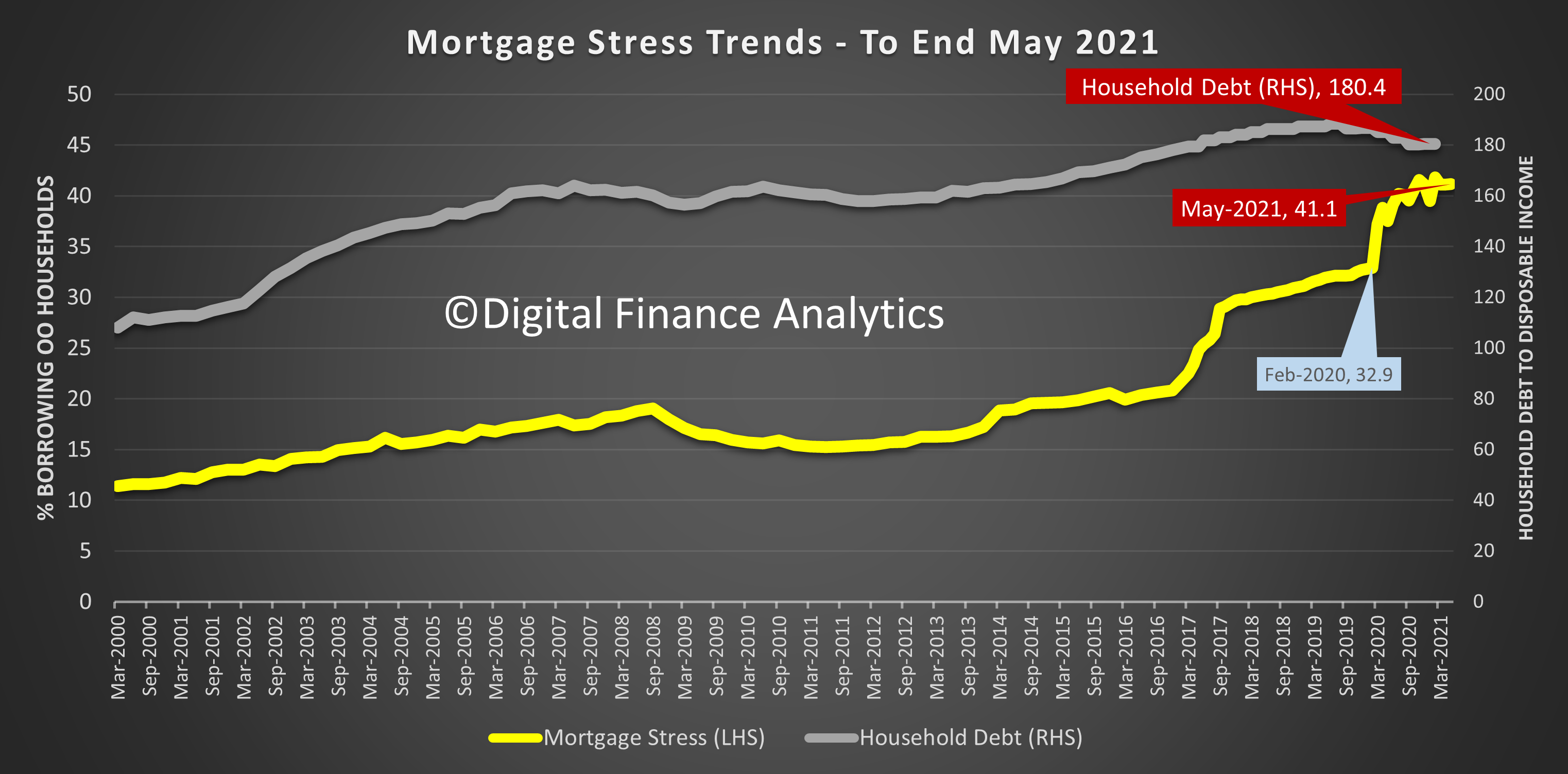

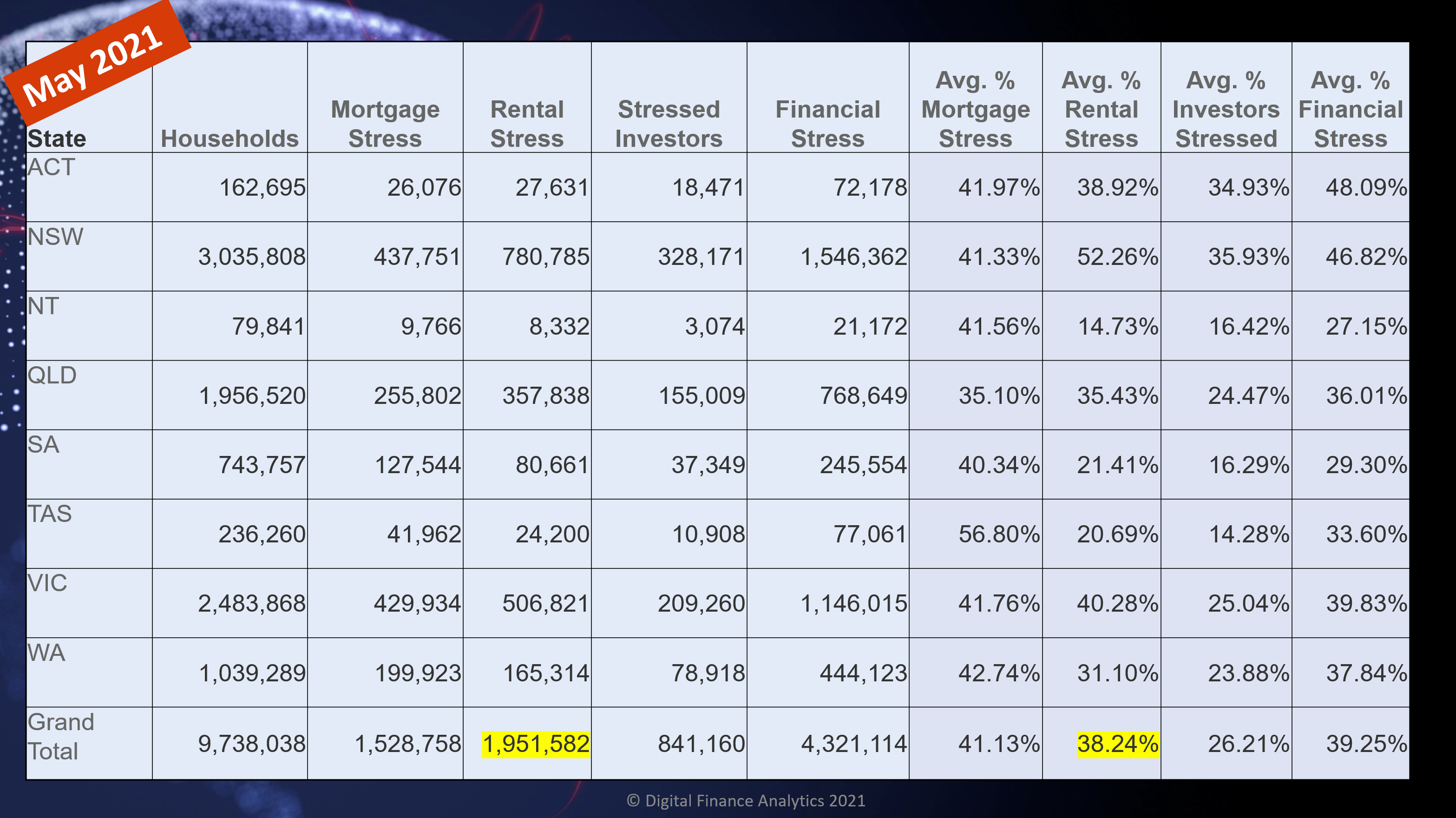

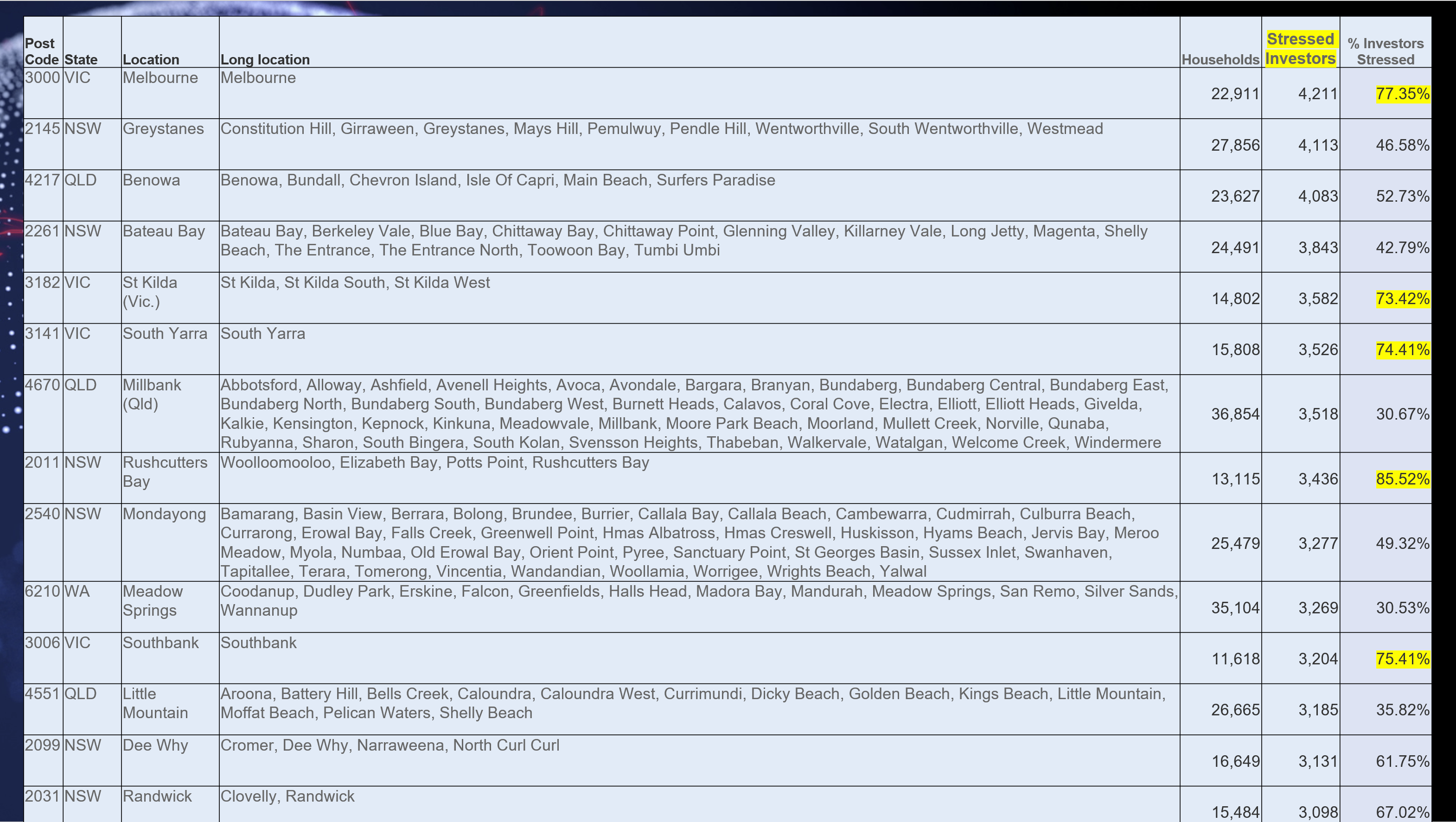

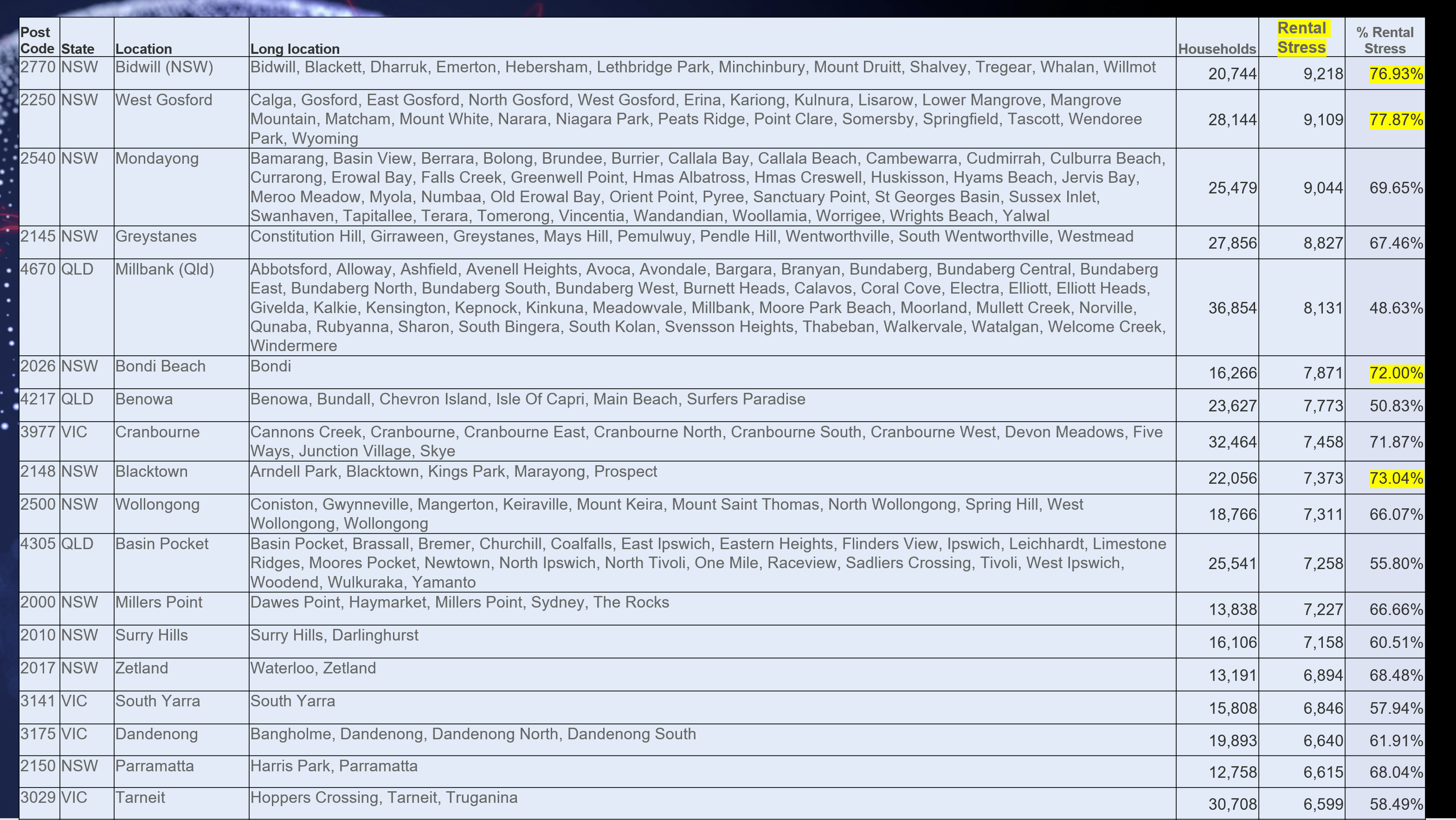

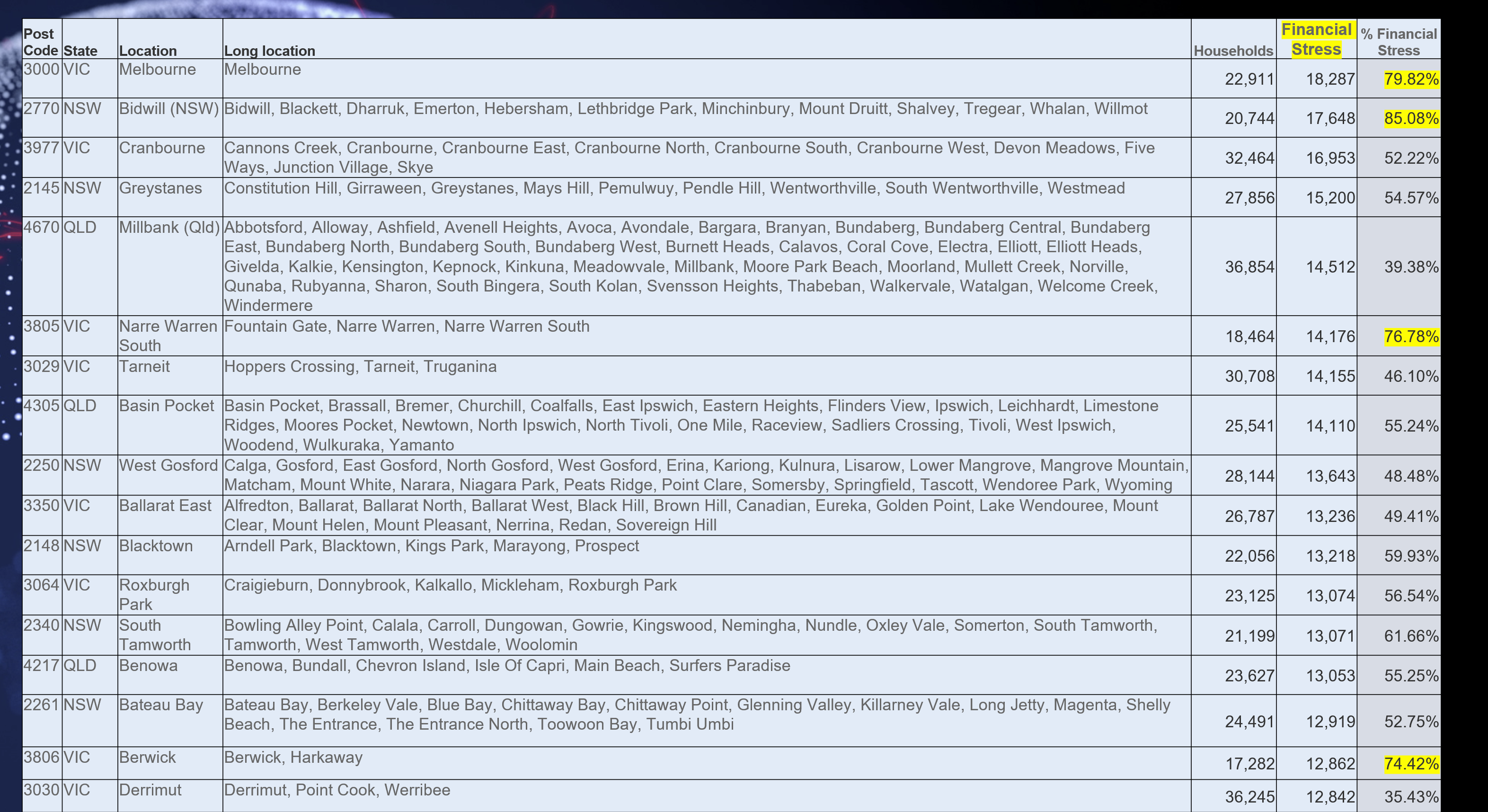

The latest data from our household surveys for May revealed little change in mortgage stress among households – still at around 41%, but there was a shocking rise in rental stress as the JobSeeker and JobKeeper supports were withdrawn, and the random lock-downs continue.

Even Property “experts” accept that affordability has deteriorated recently, as house prices rocket higher in many suburbs, although of course real interest rates are very low, for now, if rising ahead.

Our approach to measuring stress is unique in that we examine household cash flow – money in and money out. Given that many households saved hard last year though the heights of COVID, it is not surprising to see many now draining down those savings, by spending more. This means that their cash flow will in net terms be negative for now, and so will register as stressed. That said, if spending continues unabated financial difficulties will eventuate.

In addition we continue to see more households reaching for credit (from Buy Now Pay Later, to Pay Day loans) as well as equity release from property. In fact the latest hikes in perceived values has led to a run of refinancing, to try and pay down debt, or to provide funds to offspring for property purchase via the Bank of Mum and Dad. Again these one-off moves can adversely impact household stress measures in our methodology.

And we also note that many prefer not to accept the truth that some households are not home and clear in terms of their finances, given the uncertain part-time work, multiple jobs and zero hours contracts which many are on. But we continue to analyze households in net cash flow terms. If more funds drain away, compared with income, they are classified as stressed.

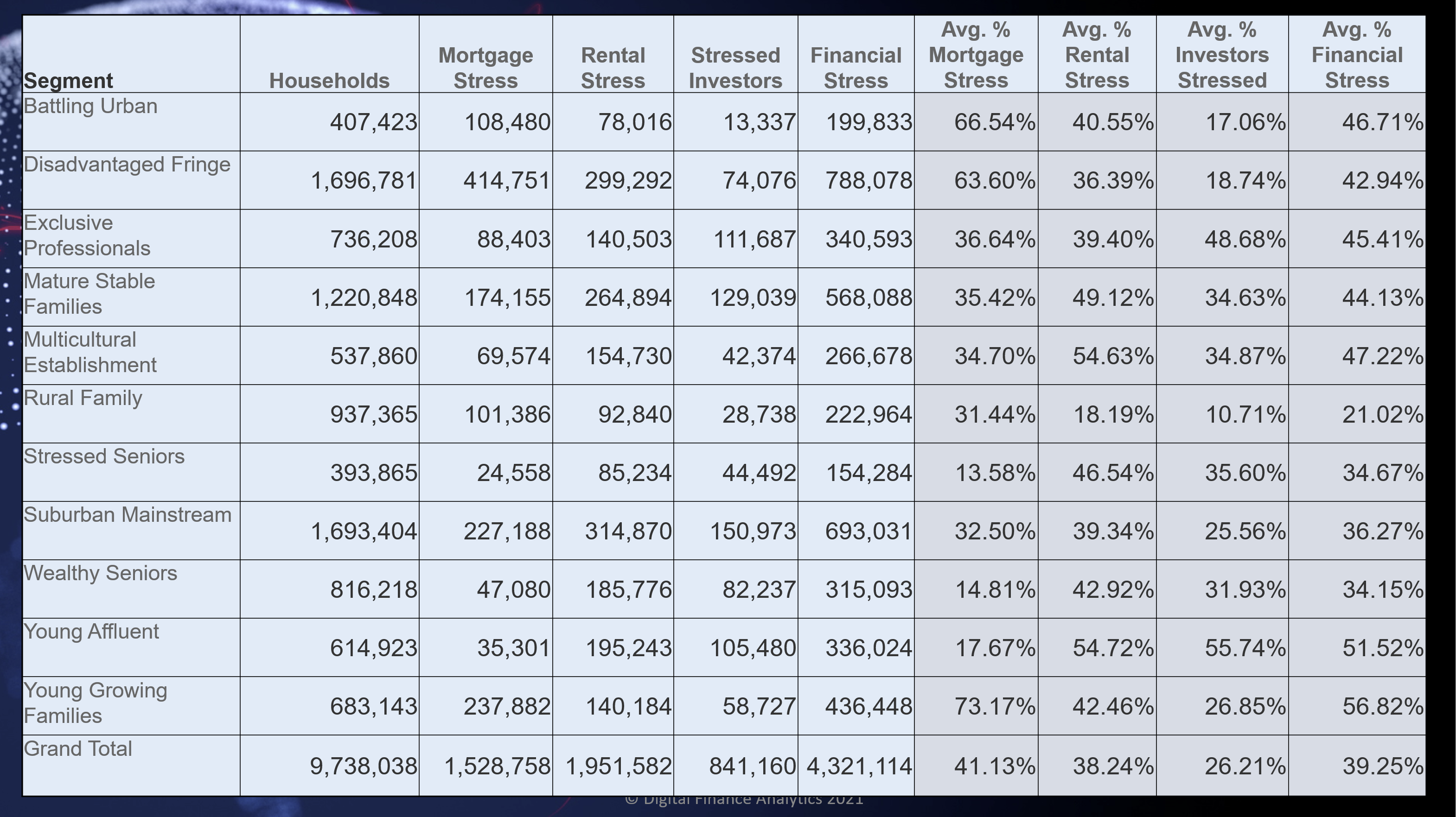

Across our segments we continue to see quite different dynamics emerging, with many younger households (often first time buyers) impacted, alongside the high growth corridors containing many first generation Australians, as well as some more affluent groups. Financial Stress takes no prisoners.

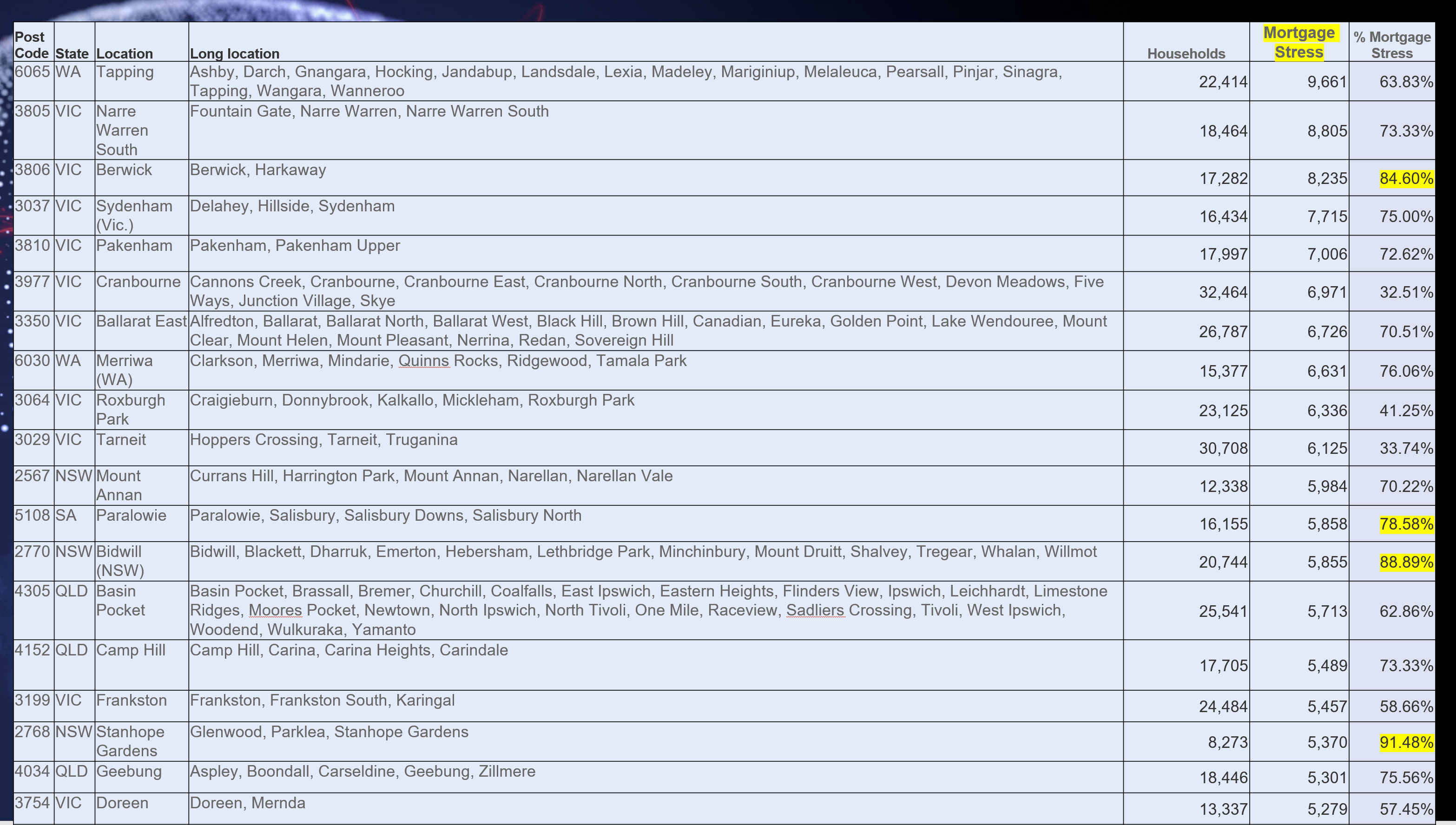

The mortgage stress counts are highest in high growth corridors in WA and VIC – where in some cases more than 80% of households in the area have cash flow issues.

Rental stress is more strongly registered in NSW and QLD, with Western Sydney and the Central Coast and Bundaberg in the top 10.

Property investors are having difficulty in Melbourne 3000, thanks to the lack of students and ongoing lock-downs. A number of VIC suburbs are impacted thanks to high vacancy rates, negative net yields and falling apartment values.

Overall financial stress, our aggregate measure reveals that Melbourne 3000 has the highest stress levels. That is followed by a number of the high growth corridors.

The continued pressure on households from low income growth, and rising living costs will persist, while the risks of interest rate rises grow with the competition of the Term Funding Facility at the end of June.

Households continue to wait for a magic bullet to solve their financial flow issues, and while some can draw on savings and equity, or reach for more credit, unless spending patterns are understood (half have no budgets), we think these trends will continue to bubble away.

Of course, financial stress is not the same a mortgage default, but those with cash flow issues are more likely later to end up having to sell their home, unless remedial action is taken.

Households in financial stress should certainly speak to their lender, prioritise spending, and be cautious about further loan commitments. There is no income growth “get out of jail card” for now.

The latest edition of our finance and property news digest with a distinctively Australian flavour.

Caveat Emptor! Note: this is NOT financial or property advice!!

Today’s post is brought to you by Ribbon Property Consultants.

Shoot Ribbon an email on info@ribbonproperty.com.au & use promo code: DFA-WTW/MARTIN to receive your 10% DISCOUNT OFFER.

If you are buying your home in Sydney’s contentious market, you do not need to stand alone. This is the time you need to have Edwin from Ribbon Property Consultants standing along side you.

Buying property, is both challenging and adversarial. The vendor has a professional on their side.

Emotions run high – price discovery and price transparency are hard to find – then there is the wasted time and financial investment you make.

Edwin understands your needs. So why not engage a licensed professional to stand alongside you. With RPC you know you have: experience, knowledge, and master negotiators, looking after your best interest.

Go to the Walk The World Universe at https://walktheworld.com.au/