Senator Malcolm Roberts joins John Adams and Martin North on IOTP to discuss the draft cash ban legislation and he outlines One Nation’s policy position.

We extend the conversation into important broader issues including civil liberties, structural reform and media policy. A landmark event on IOTP!

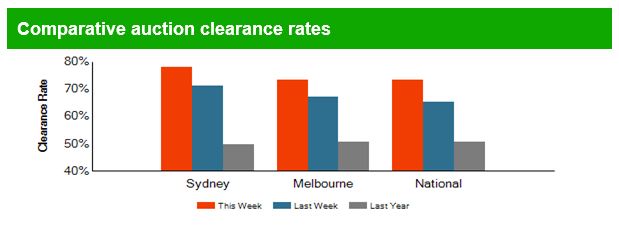

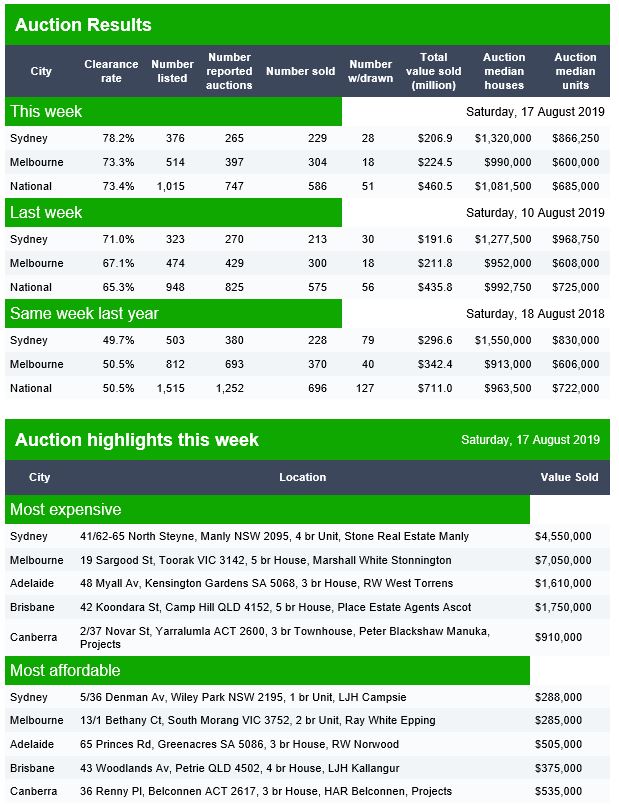

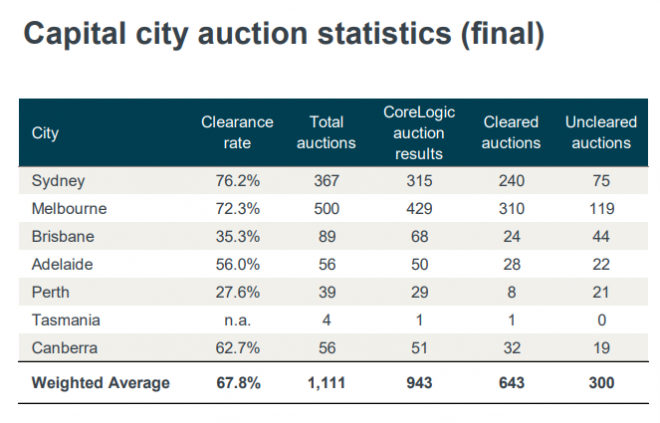

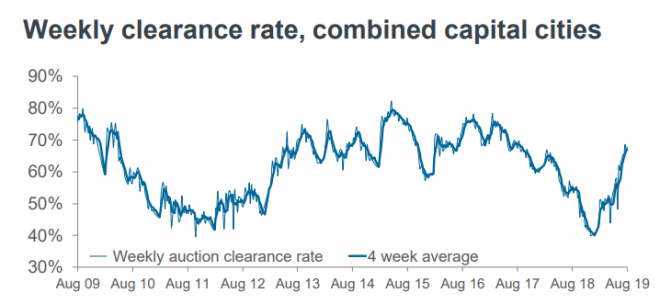

The trends continue, higher clearance rates on lower volumes than last year. 1,015 listed this week, compared with 1,515 a year back. And a smaller number reported sold (dispute the natural bias to report sold events!).

In Canberra, 21 were listed, 19 reported and 17 sold, with 2 passed giving a Domain result of 89%.

In Brisbane, 68 were listed, 43 reported with 20 sold, 23 passed in and 2 withdrawn giving a Domain result of 44%.

In Adelaide, 36 were listed, 23 reported with 16 sold, 7 passed in and 3 withdrawn giving a Domain result of 62%.

Recently, on 13 August, the Federal

Court rejected the case of Australian

Securities and Investments Commission (ASIC) against Westpac for irresponsible mortgage lending and ordered the regulator

to pay the bank’s costs. Such failures

at enforcing regulation have occurred numerous times in the past and have cost

taxpayers many millions, for little benefit.

The paper “The farce of fake regulation: royal commission exposed Australia”

explains how enforcement failures have led to fake regulation in Australia. In

relation to ASIC, the paper noted:

The

new commissioner Sean Hughes declared that the mantra at ASIC going forward

will be “Why not litigate?” He appears to have a short memory because he should

know well from his past experience working at ASIC how costly, unsuccessful and

unpopular litigation has been for the regulator. What is the point of more

litigation recommended by HRC, if it only ends in failures?

The Hayne Royal Commission (HRC) discovered the lack of enforcement of

regulation for past decades, but did not go far enough to discover why. The reason is: due to the underlying neoliberalist

assumption of market efficiency, Australian financial regulation was not designed

to protect consumers. Indeed, it is caveat emptor as noted by Wayne Byres, the

chair of the Australian Prudential Regulation Authority (APRA).

In the ASIC vs Westpac case, the judge probably did not understand why a

lender such as Westpac would knowingly make bad housing loans risking losses to

the bank itself. So the litigation

hinged around the interpretation of responsible lending as to whether there is legal

flexibility on the part of the lender to assess mortgage serviceability by using

the benchmark Household Expenditure

Measure (HEM) rather actual expenditures of individual borrowers.

Clearly, complex rules by

regulators on how a business should be run can usually be refuted by actual

evidence and experience. That is, ASIC does

not have enough business knowledge or access to hard data to prove conclusively

that the HEM criterion is the main cause of irresponsible lending. Therefore, unproven causality was inadequate to

compel a conviction.

There are so many other aspects of

mortgage serviceability to which one could attribute irresponsible lending that

it is difficult to see how picking one single aspect will lead to successful

prosecution by the regulator. Probably,

by taking on Westpac, ASIC was merely showing that it was following the HRC

recommendation for more enforcement.

Without understanding the real problem, HRC has been ineffective in

reforming the financial system, as nothing much will change.

The real reason for why the banks

lend irresponsibly is not incompetence, but conflict of interest, because the

bad loans they create can be packaged and on-sold to unwary investors as

mortgage-backed securities. Those

mortgage-backed securities can be used for speculation with credit default

swaps (CDS) and they can be sliced and diced to create other derivative

securities such as collateralized debt obligations (CDO).

Hence irresponsible lenders can avoid adverse consequences to themselves by securitizing their loans. One proven way of removing the perverse incentive to lend irresponsibly is to remove banks’ ability to securitize their mortgages by separating commercial lending from securitization under the prohibition which was the US Glass-Steagall Act. When banks are broken up so that they are no longer “too big to fail”, they can be allowed to suffer the natural consequences of bad loans without being rescued with “bail-out” or “bail-in” and without protection from bank-runs by banning cash.

In 2017 then Treasurer Scott Morrison announced a bill that would require the big four banks to participate fully in the mandatory comprehensive credit reporting regime. Via The Adviser.

The legislation passed the

House of Representatives but had not passed the Senate prior to the

dissolution of parliament due to the election.

The

revised bill has introduced a new category of information within credit

reporting, enabling hardship information to be reporting alongside

repayment history information.

Attorney-General Christian Porter

also introduced new hardship arrangements to allow consumers to reveal

hardship arrangements to other credit providers.

“Proposed

changes to the Privacy Act will make sensible changes to allow for

transparent and responsible lending practices where people are subject

to hardship arrangements,” Mr Porter said.

“The amendments will

benefit consumers by making sure credit products are suitable, and

ensuring consumers are encouraged to seek hardship arrangements if they

are struggling to meet repayments under their credit contract.”

The draft legislation has just been released for public consultation which will introduce these changes.

“These

changes balance the needs of both credit providers and consumers. They

are intended to give credit providers relevant information about

consumers who are in financial hardship, or have recently experienced

hardship, in order to facilitate better and informed lending decisions,”

said Mr Porter.

The consultation period is open until September with interested parties welcome to comment on the draft legislation.

The big four bank has told ASIC to consider the utility of the broker channel before proposing bespoke responsible lending obligations, adding that it has not identified a notable difference in the quality of loans originated by the channel. Via The Adviser.

In

February, the Australian Securities and Investments Commission (ASIC)

launched a review to update its responsible lending guidance (RG 209),

which has been in place since 2010.

ASIC opened consultation by

inviting submissions from stakeholders within the financial services

sector and has since commenced a second round of consultation in the

form of public hearings, in which stakeholders that provided submissions

have been called to provide further guidance.

Appearing before

ASIC during its first round of public hearings, Westpac’s general

manager of home ownership, Will Ranken, was asked to provide an

assessment of the quality of mortgages originated through the broker

channel.

Mr Ranken noted that the bank’s verification requirements

for loans originated via the proprietary channel are the same for those

originated by brokers but acknowledged that broker-originated loans

require an “extra layer of oversight and governance”.

“When a

customer chooses to go to a broker, we’re one step removed, so there’s

another layer of oversight and governance on the broker channel,” he

said.

However, the Westpac representative stated that the bank has

not observed substantive differences in the quality and characteristics

of home loans originated by the third-party channel.

“If

you look at performance, particularly the metric around 90-day

delinquencies, they’re largely the same with our proprietary channel –

there’s no meaningful difference between those channels,” Mr Ranken

said.

“In terms of the tenure of loans, I think on average it’s

measured in months rather than quarters. In terms of the difference [in

the average tenure of the loans], it’s one or two [months].

“In terms of the size of a loan, if you look at averages, and averages can be a bit misleading, the average size of a loan through the broker channel is a little bit larger. That’s probably more for smaller loan sizes, customers are happier to deal with a branch, but for larger complex lending requirements, there’s a greater propensity for customers to go to a broker.”

Mr

Ranken was then asked if Westpac would support a move by ASIC to

prescribe different responsible lending obligations depending on how a

loan is originated.

In response, Mr Ranken warned that ASIC should

consider the effect of such changes on the value proposition of the

broker channel.

“I would say on providing additional guidance on

one particular channel over another, it would be important to take into

account the very valuable contribution that brokers do make to the

overall market,” he said.

“Specifically, I talk to the level of

competition that they facilitate in the market, either through providing

independence and access to a multitude of lenders, as well as the

service they give to customers in terms of assisting them with complex

needs.

“To the extent that guidance may require additional steps

either on the lender or the broker themselves, we just want to balance

that with ensuring that it maintains a viable and dynamic broker

channel.”

When pressed on the question, Mr Ranken added: “We’re comfortable with the policies and procedures that we’ve got in place around the broker channel, so it’s hard to comment on guidance… The devil’s in the detail. It really depends on what the detail of the guidance would be.”

Other stakeholders, however, including consumer group CHOICE, have called on ASIC to enshrine specific broker obligations in its RG 209 guidance.

CHOICE

pointed to research from ASIC’s review of interest-only home loans in

2016, which reported that mortgage broking record-keeping from

verification enquiries was “inconsistent” and, in some

cases, “fragmented and incomplete”.

Despite recent reforms from the Combined Industry Forum, which restricted the payment of commission to the loan amount drawn down by a borrower, the consumer group alleged that the supposed lack of record-keeping was “particularly harmful for consumers” because “brokers are currently incentivised to sell loans that will provide them with the largest commission”.

ASIC’s first

round of public hearings concluded, with the second round of hearings to

commence in Melbourne on Monday, 19 August.

The regulator is expected to publish its new guidance before the end of the calendar year.

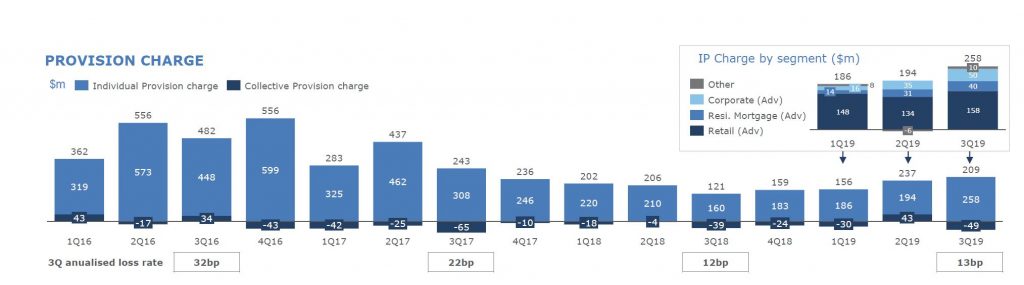

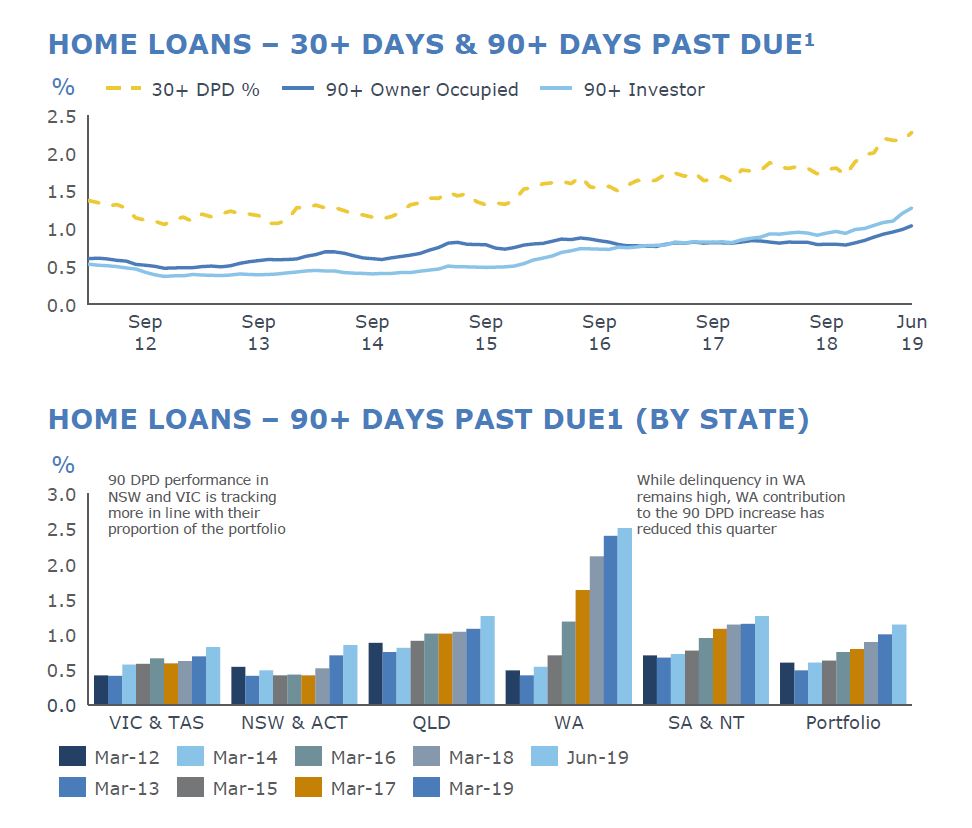

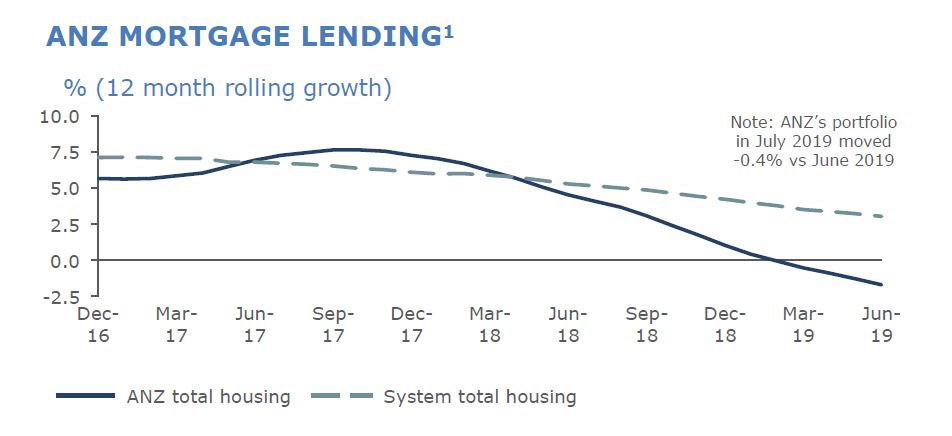

ANZ today provided an update on credit quality, capital and Australian housing mortgage flows as part of the scheduled release of its Pillar 3 disclosure statement for quarter ending 30 June 2019 and associated chart pack. Given the strategy was to shed a portfolio of businesses and focus on the Australian retail market, we need to give attention to their shrinking mortgage book and rising delinquencies.

Total provision charge of $209m for the June quarter remained broadly flat compared with the 1H19 quarterly average, while the individual provision increased $68m to $258m. Total loss rate was 13bp (consistent with the 1H19 loss rate of 13bp).

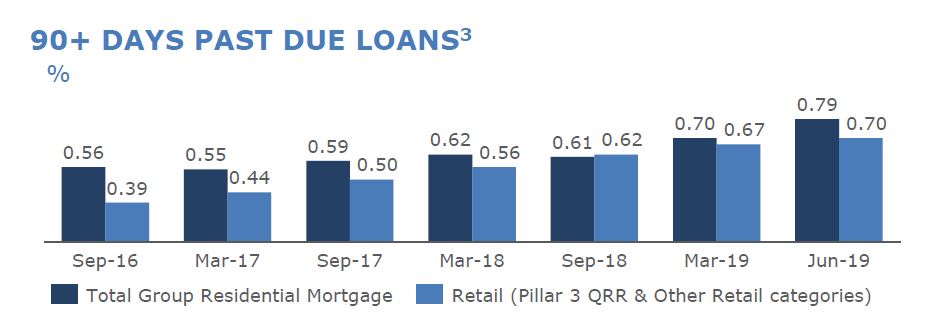

90+ Days Past Due Loans rose in the quarter.

Mortgage delinquency rose in 3Q19, with 90 day increasing 14bp to 114bp. On a geographic basis, ~9bp of the movement came from NSW and VIC in aggregate. On a product basis, ~1/3 of the movement came from Interest Only home loan conversion to Principal & Interest.

WA still leads the way, but delinquencies are also rising in other states. FY17 & FY18 vintages continue to perform better than FY15 & FY16 (when of course lending standards were at their most loose, plus as we know from our mortgage stress work, it can take 2-3 years for households in financial stress to go delinquent). ANZ’s performance is likely to be biased higher given its shrinking mortgage portfolio, as we discuss below.

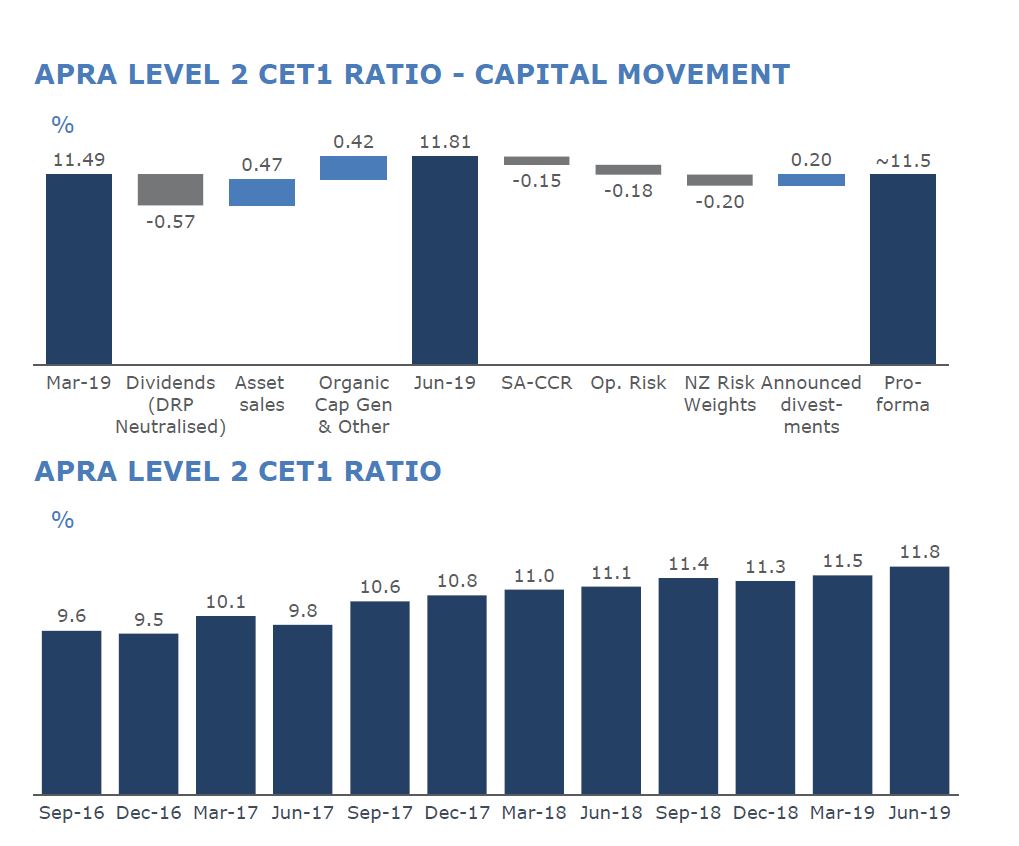

Group Common Equity Tier 1 ratio (APRA Level 2) was 11.8% at the end of June 2019, a ~30bp increase for the June quarter. On a pro-forma basis, inclusive of announced divestments and the recently announced capital changes, ANZ’s Level 2 CET1 ratio is 11.5%.

As indicated at ANZ’s first half result presentation, expectation was for home loan volumes in Australia to decline during the June quarter, with Owner Occupied down 0.2% and Investor down 1.8% (June 2019 compared with March 2019).

They say that home loan applications improved in July 2019 with actions taken in recent months to clarify credit policy and reduce approval turnaround times having a positive impact.

Following its Tuesday victory against ASIC, with the court dismissing the regulator’s allegations of irresponsible lending, Westpac has announced a spectrum of changes to its home lending policies. From Australian Broker.

The updated guidelines are set to go into effect on 20 August, at not

only the major, but its associated brands: St. George, Bank of

Melbourne, and Bank SA.

Perhaps most notably, Westpac is to update and add new expense

categories to its household expenditure measure “to reflect industry

guidelines on the HEM values we use as our customer expense benchmarks” –

bringing the total number of categories from 13 to 18.

Further, the bank will apply income-based HEM bands based on total gross unshaded income, including gross rental income.

Particularly relevant in light of the recently dismissed court case, in instances when total liability is seven times or more higher than total gross income, the loan applications will be reviewed by a credit assessment officer rather than run through the automated system.

ASIC’s case against the bank had hinged on the allegation Westpac

breached the National Consumer Credit Protection Act 2009 through

assessing loans via its automated system which solely considers the

benchmark HEM rather than customers’ declared living expenses.

Westpac additionally addressed the changes being made to tax debt through changing its approach to margin loans. They will now be assessed on the higher of 1% of the balance or the customer’s monthly declared commitment.

Further, Westpac will require a more comprehensive understanding of

payment plans businesses have made with the ATO and decline to lend to

customers with an overdue amount payable to the ATO for the previous

year’s tax without a formal payment plan in place.

The policy changes will impact all new and re-submitted applications

made from Tuesday, requiring brokers to utilise the expanded 18

categories for expenses, as well as heed the new seven times

debt-to-income ratio.

Westpac also announced that changes to the commercial, SME and private wealth broking channels will be made later this year.

I did not receive the Domain results last Saturday so could not make my normal weekly post. I have had many people ask about the data.

So, here is first the data they did publish last week. No comparative data to last year. Volumes are lower, even if Domain clearance rates are higher.

And we also got the CoreLogic final results today. There were 1,402 auctions last year compared with 1,107 this past week. That puts the higher clearances in a better context.