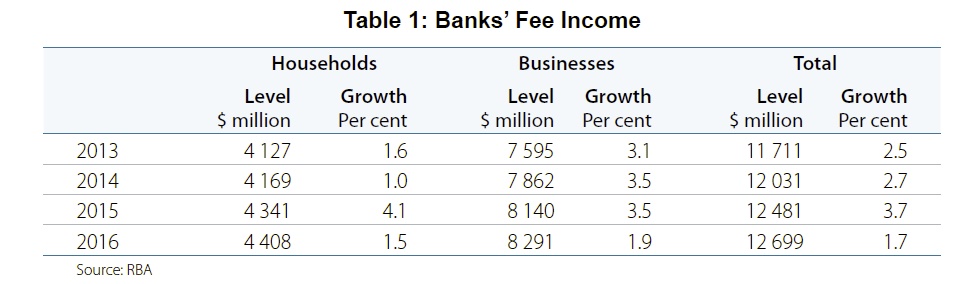

The latest RBA Bulletin includes a section on Bank fees. In 2016, domestic banking fee income from households and businesses grew at a relatively

slow pace of 1.7 per cent, to around $12.7 billion.

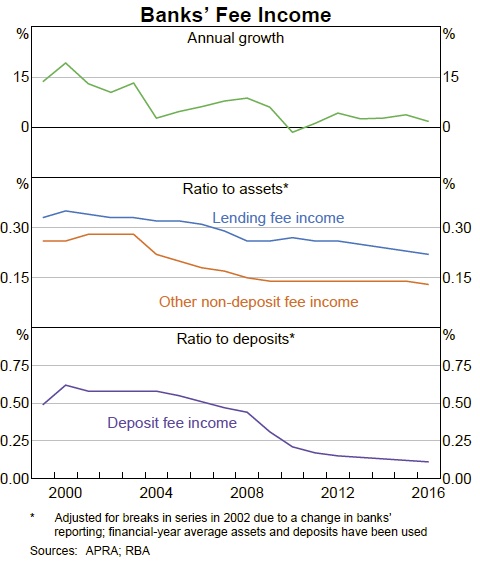

Deposit and loan fee income relative to the outstanding value of products on which these fees are levied was slightly lower than in the previous year.

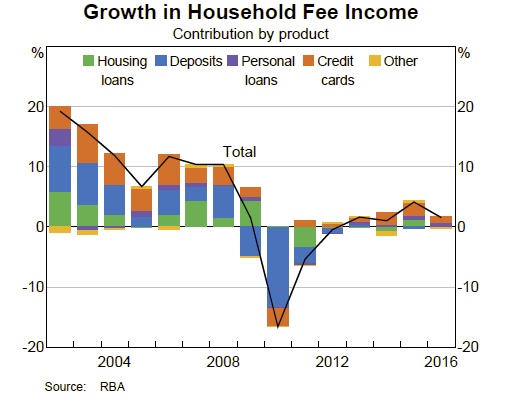

Banks’ fee income from households grew by 1.5 per cent in 2016. This represented a slowing in growth from the previous year, reflecting lower

growth in fee income from housing lending and credit cards.

Growth in fee income from credit cards slowed in 2016 to slightly below the average since 2010, but remains the largest component of fee income from households. The growth in fees was supported by continued take-up of credit cards bundled with home loan packages. There were also more instances of fees being charged, with some banks no longer waiving fees for transferring a credit card balance to a new card provider.

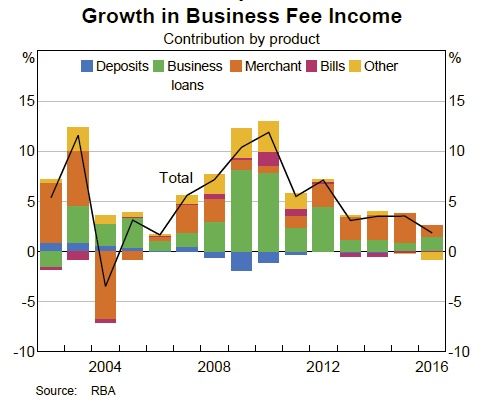

Total fee income from businesses increased by 1.9 per cent in 2016, around the slowest pace for a decade. Slower growth was recorded for fee income from both small and large businesses. By product, growth in fee income

Total fee income from businesses increased by 1.9 per cent in 2016, around the slowest pace for a decade. Slower growth was recorded for fee income from both small and large businesses. By product, growth in fee income

was driven by increases in business loan fees and merchant service fee income from processing card transactions. Fee income from deposit accounts also increased slightly, while fee income from bank bills and other sources declined. The increase in business loan fees mainly

reflected higher reported fee income from small businesses.

Growth in merchant service fee income was mainly attributable to increased transaction volumes, particularly for credit cards due to wider

acceptance of contactless payments. Increased use of platinum and business credit cards, which attract higher interchange fees, also contributed to growth in merchant service fee income from small businesses. Nevertheless, growth in merchant service fee income was evenly spread across small and large businesses.

Total fee take was $12.6 billion, still a substantial sum, but small beer compared with the $31 billion grabbed by the superannuation industry.

Total fee take was $12.6 billion, still a substantial sum, but small beer compared with the $31 billion grabbed by the superannuation industry.