The RBA just published the results of its annual bank fee survey, based on data from 16 institutions covering 90% of the Australian banking sector. Last year, overall fees rose 2.8% to $12 billion compared with 2.6% the previous year. The rise is a combination of rises in unit prices, and volumes. Households fees rose 1.5% to $4,141 million, and business grew 3.5% to $7,791 million. The data does not include wealth management, broker, loan mortgage insurance, or other fees across financial services and the non-bank sector.

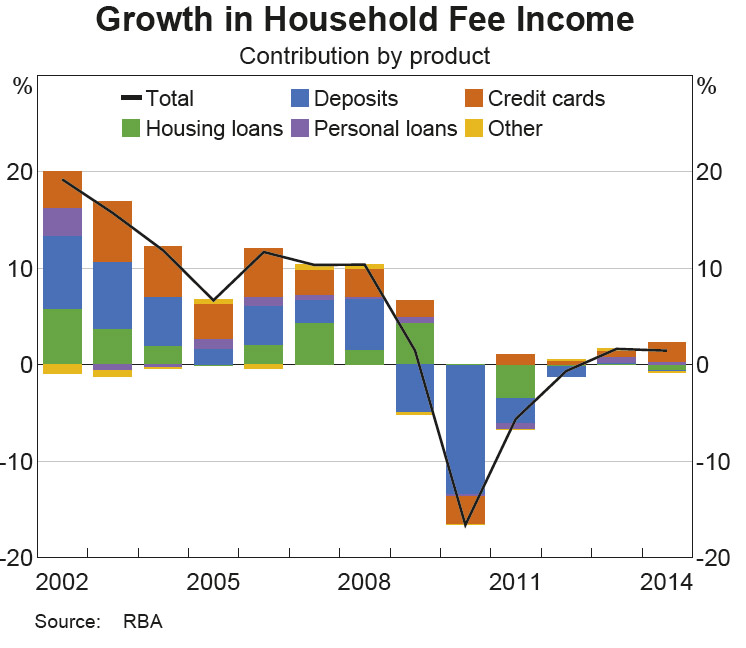

Looking in more detail at households, higher fee income reflected growth in credit card and personal lending fees, whereas fee income from housing lending and deposit accounts declined.

Fee income from credit cards, which represents the largest component of fee income from households, increased by 5.9 per cent. You can read our previous analysis of the credit card business here.

Fee income from credit cards, which represents the largest component of fee income from households, increased by 5.9 per cent. You can read our previous analysis of the credit card business here.

Total deposit fee income decreased slightly in 2014, following a modest increase in 2013. The decrease in fees from household deposits was broad based across most types of fees on deposit accounts. In particular, account-servicing and transaction fee income, as well as some fee income on other non-transaction accounts (e.g. break fees on term deposit accounts) declined notably. This decrease was the result of fewer customers incurring these fees rather than a decrease in the level of fees, as well as customers shifting to lower fee products. However, this was partially offset by an increase in income from more frequent occurrences of exception fees (such as overdrawn fees and dishonour fees) and foreign exchange conversion fees being charged on deposit accounts involving such transactions.

Total fee income from housing loans decreased in 2014, with all components of housing loan fee income decreasing, including exception fees. This was due to a combination of fewer instances of penalty fees being charged, and lower unit fees as a result of strong competition between banks in the home lending market. Similar to 2013, there was a decrease in fee income from housing lending despite strong growth in such lending. Several banks again reported waiving fees on this type of lending for some customers.

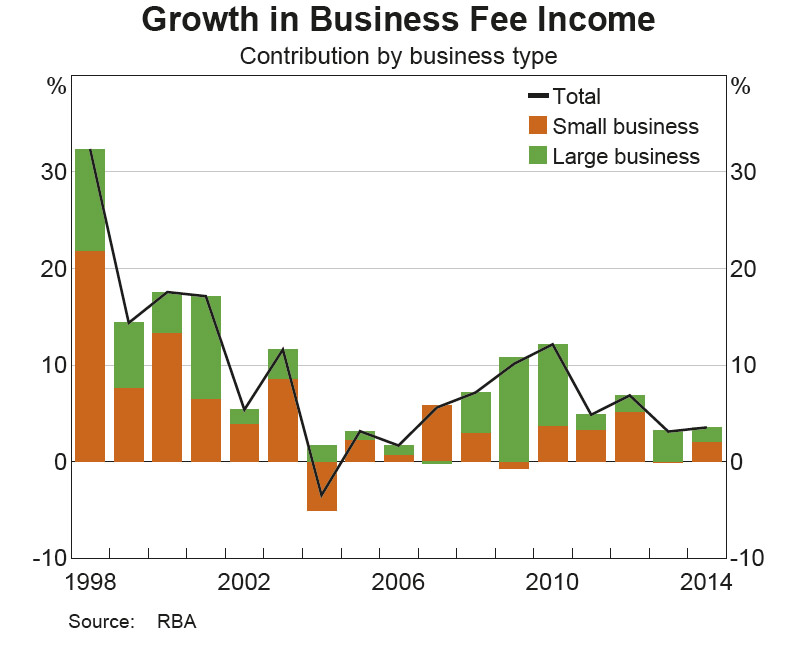

Fees to business rose, across both small and large businesses.

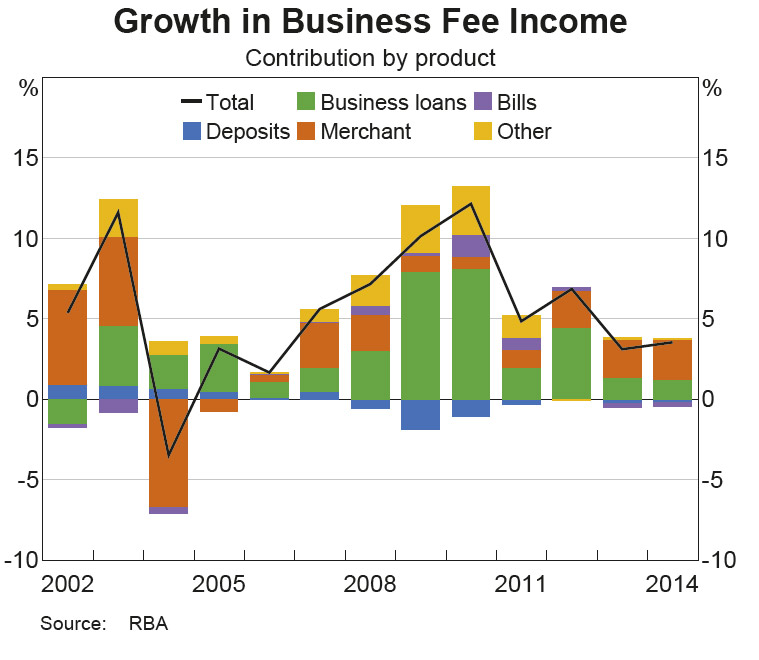

Growth was driven by increases in merchant service fee income and, to a lesser extent, fee income from loans. Business fee income from deposit accounts and bank bills declined over 2014.

Growth was driven by increases in merchant service fee income and, to a lesser extent, fee income from loans. Business fee income from deposit accounts and bank bills declined over 2014.

The increase in merchant service fees was mainly attributable to an increase in utilisation of business credit cards and a slight increase in some merchant unit fees. Merchant fee growth was approximately evenly spread across both small and large businesses. The increase in loan fee income was mainly from an increase in account-servicing and exception fees from small businesses, which was a result of higher lending volumes (including through the introduction of some new lending products). Fee income from loans to large businesses increased slightly due to a higher volume of prepayment fees (though this was mostly offset by declines in other fee income from large businesses).

The increase in exception fee income from business loans was also mainly from small businesses, mostly in the form of honour fees (fees charged in association with banks honouring a payment despite insufficient funds in the holder’s account).

Fee income from business deposits continued to decline in 2014, with most of the decrease resulting from lower account-servicing and transaction fees, particularly for small businesses (small businesses account for the majority of business deposit fee income). The decrease was the result of a combination of lower volume growth and customers shifting to lower fee products.

We observe that the “fee wars” appears to be over now (triggered by NAB a few years ago), and we expect to see subtle rises in fees as bank margins come under increasing pressure. Also, small business bears the brunt of the charges across a number of categories, and we expect this to continue, because the sector is under less pressure from a bank competitive standpoint, and many SME’s have no where else to go.

We observe that the “fee wars” appears to be over now (triggered by NAB a few years ago), and we expect to see subtle rises in fees as bank margins come under increasing pressure. Also, small business bears the brunt of the charges across a number of categories, and we expect this to continue, because the sector is under less pressure from a bank competitive standpoint, and many SME’s have no where else to go.