BOQ today announced interim cash earnings after tax of $179 million for the six months to 29 February 2016. This was below consensus of $186m thanks to lower revenue grow, despite good cost control, and lower provisioning. However, the announcement today of lifts in home loan pricing will assist going forwards. We will see if other lenders follow, as we think they might.

Statutory profit after tax rose 11 per cent to $171 million on the prior comparative half.

On a cash basis, BOQ’s basic earnings per share were up 5 per cent on the prior half to 47.8 cents. Return on average tangible equity increased 20 basis points to 14 per cent, and return on average equity was up 20 basis points to 10.5 per cent.

Managing Director and CEO Jon Sutton said the result was driven by above system housing lending growth and strong asset quality levels. The Bank also maintained its Net Interest Margin and kept costs under control.

The BOQ Board has determined to pay an interim dividend of 38 cents per share fully franked, an increase of 2 cents on 1H15.

The BOQ Board has determined to pay an interim dividend of 38 cents per share fully franked, an increase of 2 cents on 1H15.

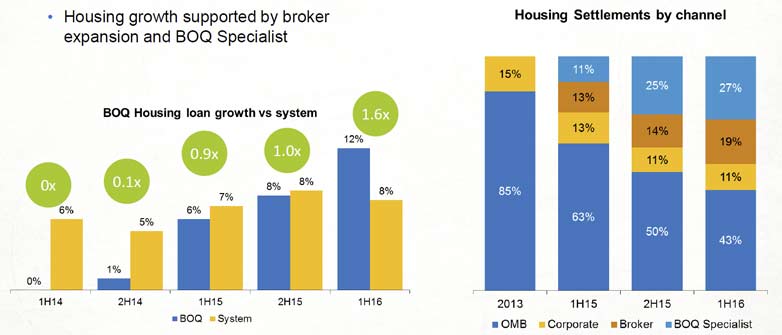

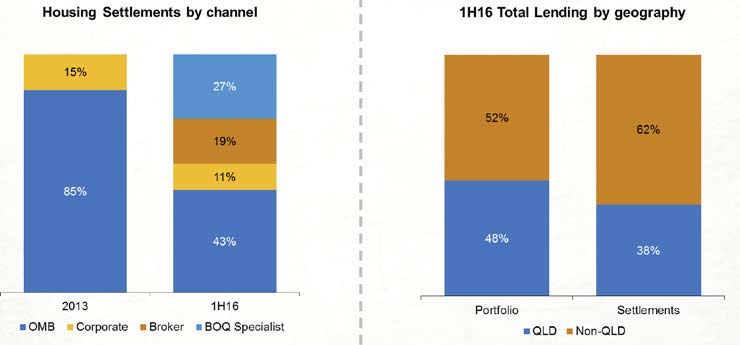

Loan Growth – BOQ achieved above System loan growth of $2 billion (1.2x System) for the half predominantly as a result of its decision to diversify distribution channels. Housing mortgage growth for the half was $1.7 billion (1.6x System), driven by strong growth through BOQ Specialist and the broker network.The third party strategy has allowed for home loan growth beyond QLD.

Growth in these channels also improved the Bank’s mortgage portfolio diversification outside of Queensland and increased its lower LVR lending relative to the portfolio. They did not disclose the mix between investment and owner occupied loans. According to recent APRA data BOQ has one of the highest proportions of investment loans among the banks.

Growth in these channels also improved the Bank’s mortgage portfolio diversification outside of Queensland and increased its lower LVR lending relative to the portfolio. They did not disclose the mix between investment and owner occupied loans. According to recent APRA data BOQ has one of the highest proportions of investment loans among the banks.

Commercial lending growth was 6 per cent (0.5x System) for the half as it maintained a focus on credit quality and appropriate pricing for risk within its targeted niche segments. BOQ Specialist’s commercial loan book grew 14 per cent to $2.4 billion year on year while the BOQ Finance portfolio grew 1 per cent (0.6x System).

Commercial lending growth was 6 per cent (0.5x System) for the half as it maintained a focus on credit quality and appropriate pricing for risk within its targeted niche segments. BOQ Specialist’s commercial loan book grew 14 per cent to $2.4 billion year on year while the BOQ Finance portfolio grew 1 per cent (0.6x System).

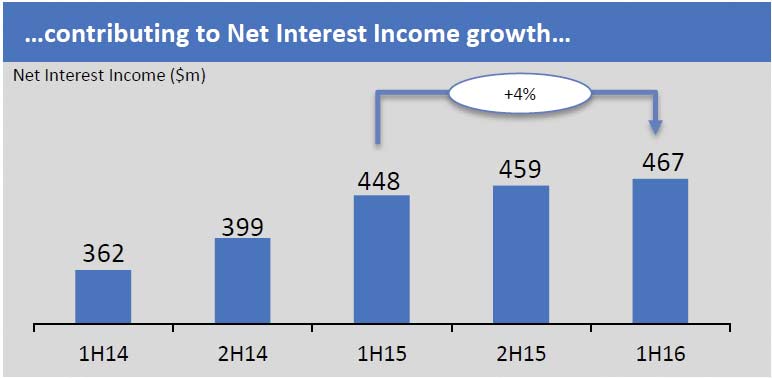

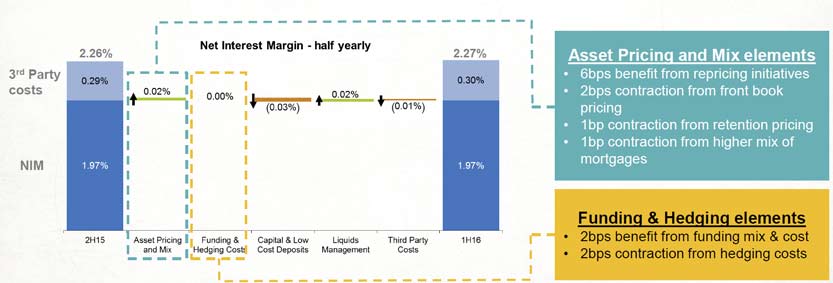

Net interest margin – BOQ maintained its 1H16 net interest margin at 1.97%. Benefits from repricing initiatives during the half were partially offset by front book and retention pricing. The targeted loan growth in new channels has resulted in a better quality loan portfolio that will support longer term balance sheet durability. BOQ has increased its variable home loan interest rates by 12 basis points for owner occupied loans and 25 basis points for investor loans, effective from 15 April 2016.

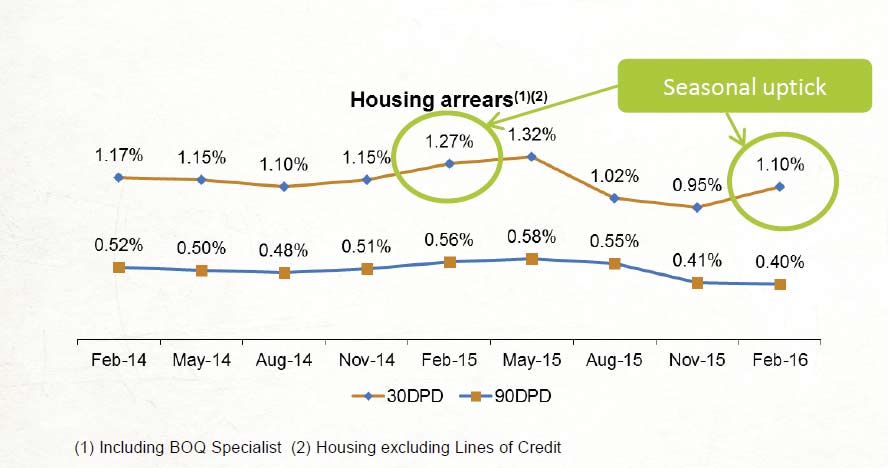

The underlying credit quality of BOQ’s portfolio remained strong in 1H16. This reflects the Bank’s continued focus on prudent lending and risk management practices, as well as the low interest rate environment. Total loan impairment expense was flat on the prior comparative period at $36 million (1H15:$36 million). Total impaired assets across retail, commercial and BOQ Finance fell 7 per cent to $240 million (1H15: $259 million). Home lending arrears rose a little. Whether this is just a seasonal uptick, or something more systemic, we will see.

The underlying credit quality of BOQ’s portfolio remained strong in 1H16. This reflects the Bank’s continued focus on prudent lending and risk management practices, as well as the low interest rate environment. Total loan impairment expense was flat on the prior comparative period at $36 million (1H15:$36 million). Total impaired assets across retail, commercial and BOQ Finance fell 7 per cent to $240 million (1H15: $259 million). Home lending arrears rose a little. Whether this is just a seasonal uptick, or something more systemic, we will see.

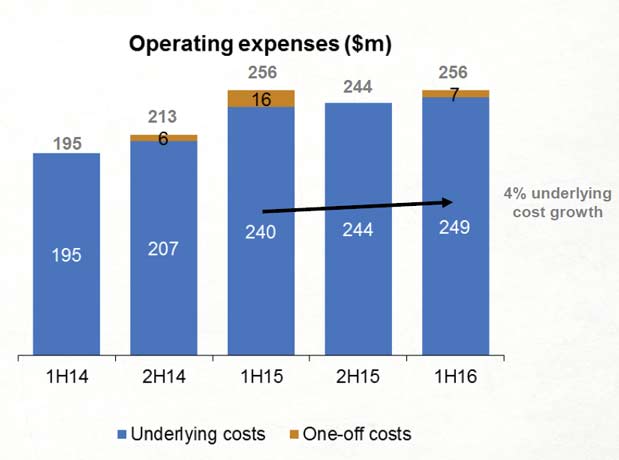

Costs – BOQ’s cost to income ratio for the half was 46.4 per cent including one-off restructuring costs of $7 million pre-tax. Excluding one-off costs, the cost to income ratio was 45.1 per cent with underlying cost growth of 3.8 per cent from the prior comparative half, in line with market guidance provided at the end of the 2015 financial year. The Bank continues to focus on its goal to reduce its cost to income ratio to the low 40s in the years ahead.

Costs – BOQ’s cost to income ratio for the half was 46.4 per cent including one-off restructuring costs of $7 million pre-tax. Excluding one-off costs, the cost to income ratio was 45.1 per cent with underlying cost growth of 3.8 per cent from the prior comparative half, in line with market guidance provided at the end of the 2015 financial year. The Bank continues to focus on its goal to reduce its cost to income ratio to the low 40s in the years ahead.

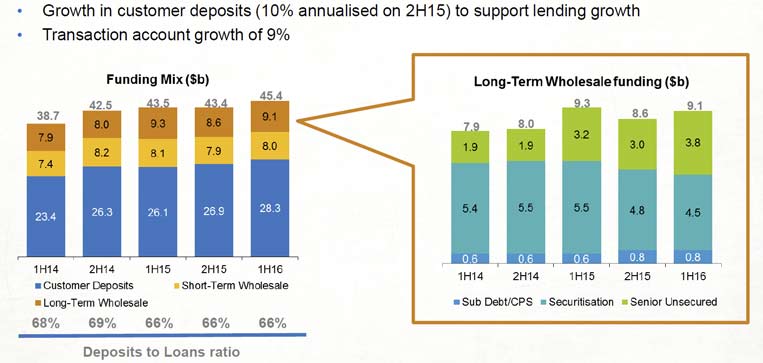

Capital and Funding – Customer deposit growth of $1.3 billion helped BOQ maintain a stable deposit to loan ratio of 66%, with a slight fall in the proportion of long-term funding via securitisation. The ratio of long-term to short-term funding improved a little.

Capital and Funding – Customer deposit growth of $1.3 billion helped BOQ maintain a stable deposit to loan ratio of 66%, with a slight fall in the proportion of long-term funding via securitisation. The ratio of long-term to short-term funding improved a little.

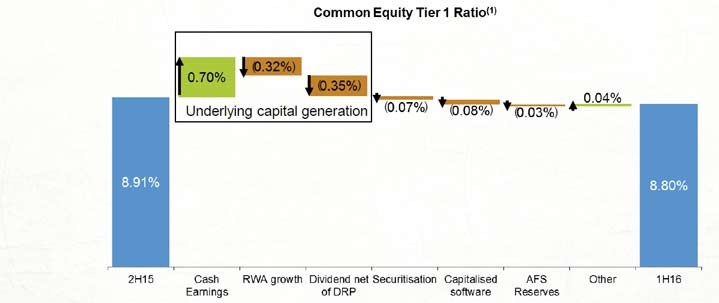

BOQ’s Common Equity Tier 1 ratio decreased 11 basis points to 8.80 per cent during the half, driven by strong loan growth in the second quarter without a full period earnings benefit.

BOQ said this ratio remains solid compared to peers and positions BOQ well for any regulatory changes to capital or risk weighting requirements. BOQ does not use IRB capital methods, so is not necessarily under the same pressure to lift capital ratios.

BOQ said this ratio remains solid compared to peers and positions BOQ well for any regulatory changes to capital or risk weighting requirements. BOQ does not use IRB capital methods, so is not necessarily under the same pressure to lift capital ratios.

BOQ positioned well for the future – Mr Sutton said BOQ’s progress against its strategic objectives positioned it well to deliver its goal of EPS outperformance over the longer term. Australia’s transition away from a resources led economy is ongoing. This presents good opportunities for expansion in the niche segments BOQ is targeting. Mr Sutton said he was also optimistic that the future regulatory environment would provide additional opportunities for standardised banks like BOQ.