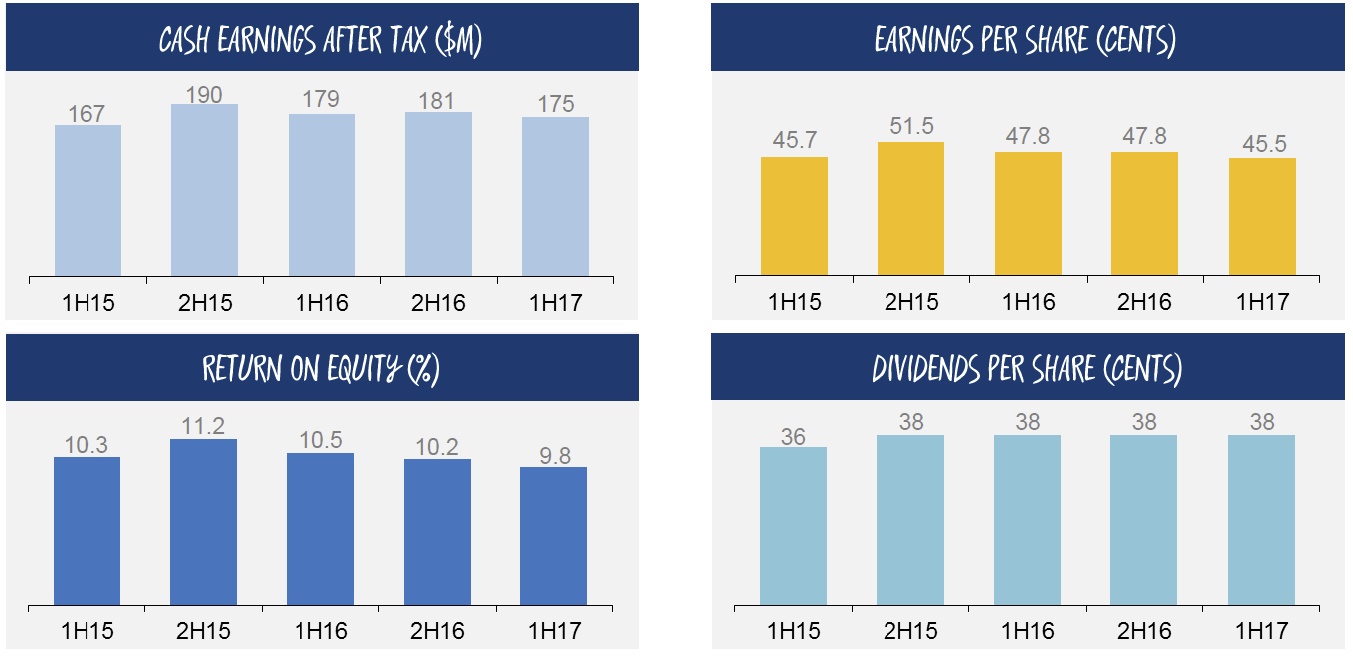

The Bank of Queensland released their 1H17 results today. Interim cash earnings after tax were $175 million for the six months to 28 February 2017, down 2 per cent on the prior corresponding period. Statutory net profit after tax was down 6 per cent to $161 million.

It is not pretty, though there may be some upside in the the second half, depending on potential out of cycle uplifts to support net interest margin. Competition has been tough, and intense pressure on mortgage pricing plus higher deposit costs were not fully offset by out of cycle uplifts. In addition, as a regional player, they have to hold more capital than the majors, which costs. Whether moving towards advance capital metrics will help is a moot point. Nevertheless, the BOQ Board maintained a fully franked interim dividend of 38 cents per share in line with the prior half.

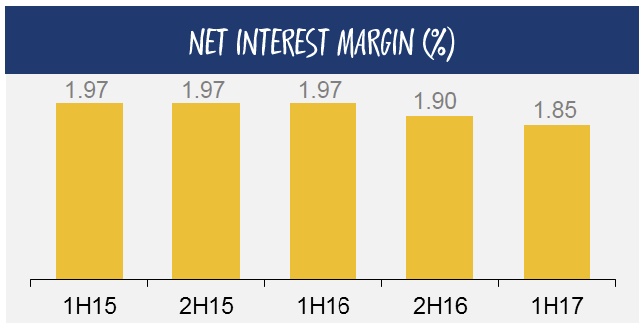

Net Interest Margin was down 5 basis points on the prior half to 1.85%, they are looking to get back to 1.89% in second half.

Net Interest Margin was down 5 basis points on the prior half to 1.85%, they are looking to get back to 1.89% in second half.

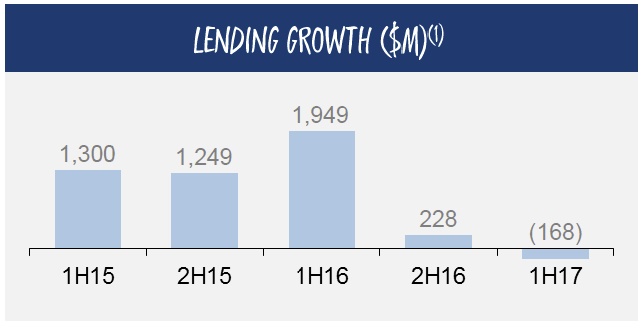

BOQ Managing Director and Chief Executive Officer Jon Sutton said “We have prioritised margin and credit quality over growth in this half, in what has been an intensely competitive period not just in lending but also in retail deposits.”

BOQ Managing Director and Chief Executive Officer Jon Sutton said “We have prioritised margin and credit quality over growth in this half, in what has been an intensely competitive period not just in lending but also in retail deposits.”

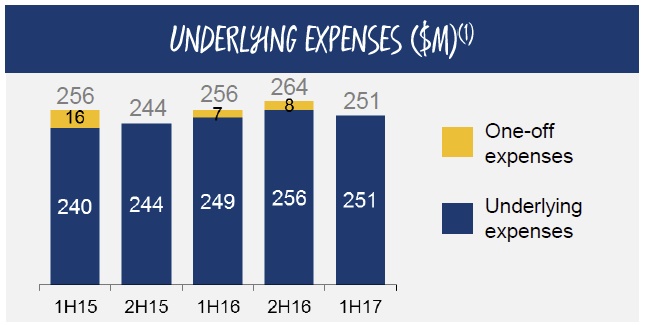

The cost to income ratio was up 100 basis points to 47.4%. Underlying expenses fell, and there will be an ongoing focus on efficiency.

The cost to income ratio was up 100 basis points to 47.4%. Underlying expenses fell, and there will be an ongoing focus on efficiency.

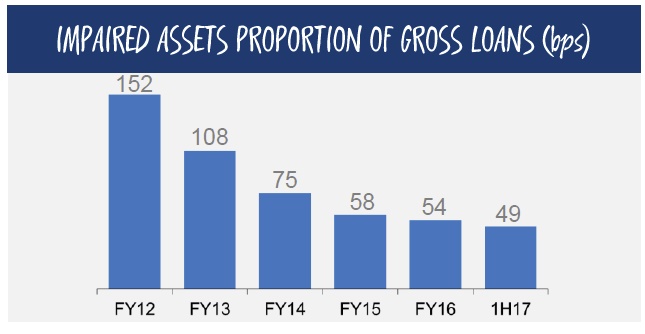

BOQ’s asset quality was again a highlight with Loan Impairment Expense down 25 per cent to $27 million, or 13 basis points of gross loans.

BOQ’s asset quality was again a highlight with Loan Impairment Expense down 25 per cent to $27 million, or 13 basis points of gross loans.

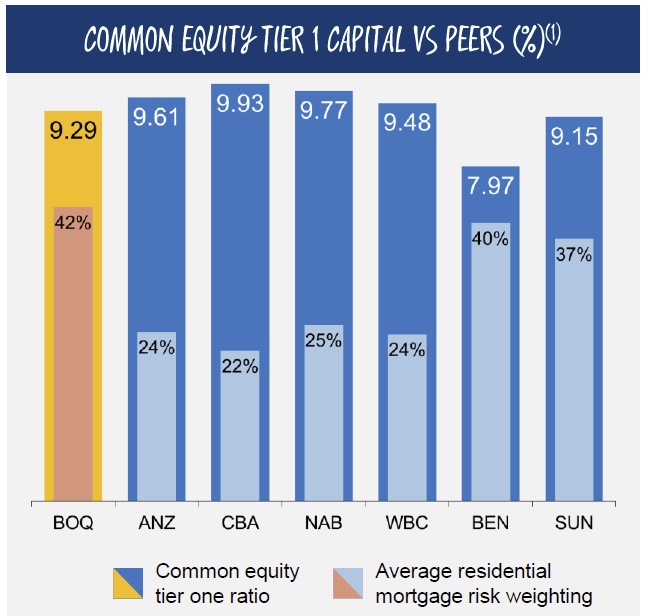

BOQ’s strong capital position improved, with the Common Equity Tier One ratio up 29 basis points over the half to 9.29 per cent. They are pushing towards advanced accreditation.

BOQ’s strong capital position improved, with the Common Equity Tier One ratio up 29 basis points over the half to 9.29 per cent. They are pushing towards advanced accreditation.

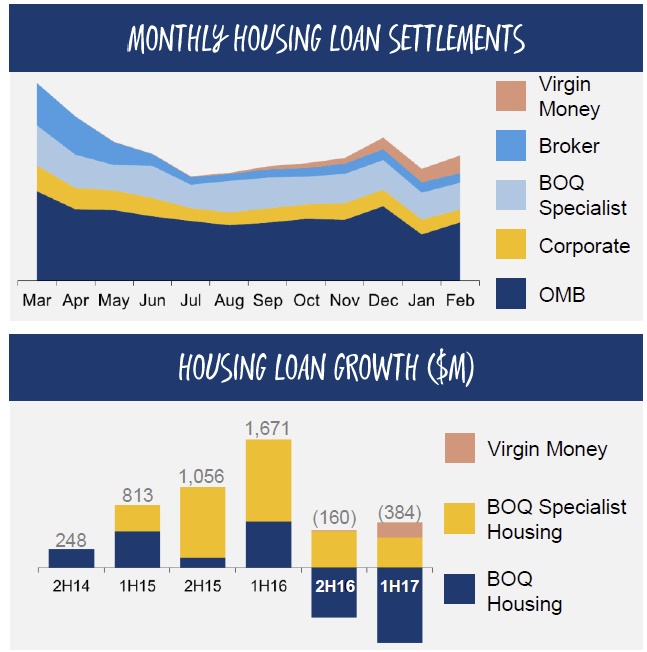

A quick look at their home lending shows settlements were down, but they said recent application volume were up, not investment lending, and they have the latest APRA guidance on expense and and income criteria in place. As competitors gear up to follow the revised guidelines, the bank expects stronger volume flows.

A quick look at their home lending shows settlements were down, but they said recent application volume were up, not investment lending, and they have the latest APRA guidance on expense and and income criteria in place. As competitors gear up to follow the revised guidelines, the bank expects stronger volume flows.

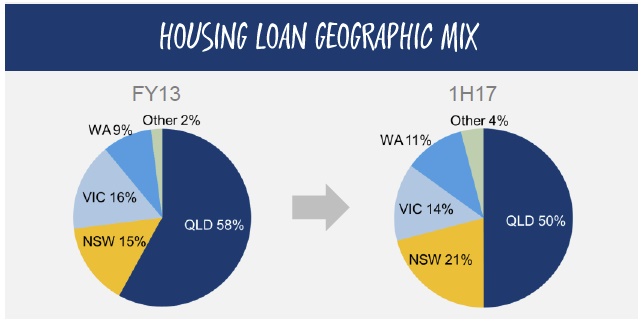

The geographic mix changed somewhat, with a focus on NSW, and growth in the “wobbly” WA market.

The geographic mix changed somewhat, with a focus on NSW, and growth in the “wobbly” WA market.

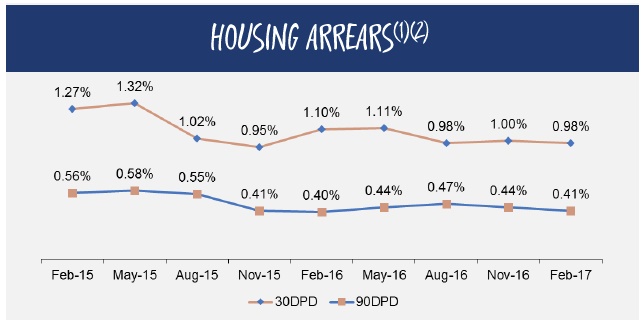

30 Day Past Due are 0.98%.

30 Day Past Due are 0.98%.

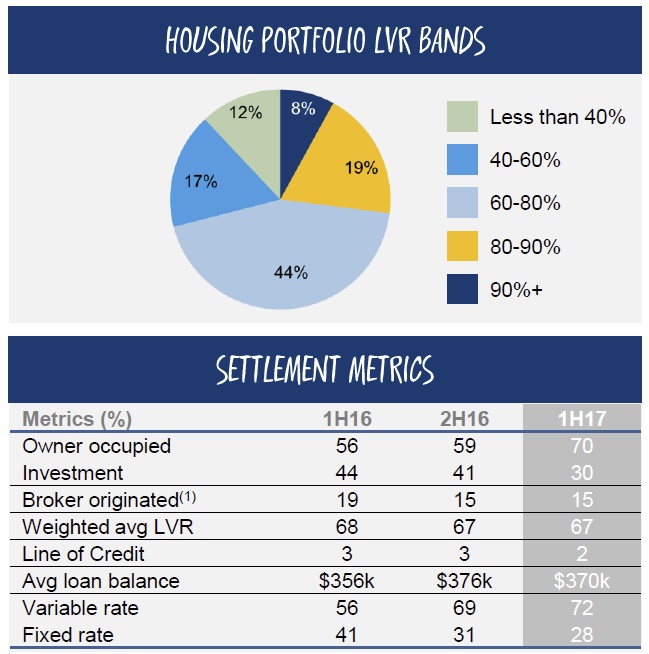

The LVR splits reflect industry trends, but the share of loans via brokers is still lower than it might be.

The LVR splits reflect industry trends, but the share of loans via brokers is still lower than it might be.

They appear to have low exposures to apartment construction, and regional housing.

They appear to have low exposures to apartment construction, and regional housing.