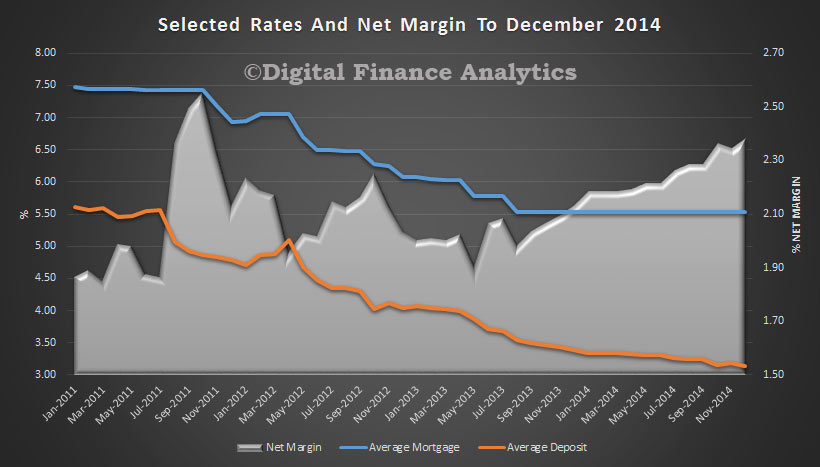

Continuing our analysis of bank margins, we have updated our industry model, with the latest funding and product data. At an aggregate industry level, we see that the average home lending rate has remained static (because whilst there are substantial discounts for new loans, the bulk of the back book has not seen any rate reduction) since 2013. The RBA last reduced their cash rate in August 2013, and the benchmark rate has remained static since then.

However, savers have see their returns falling thanks to deposit repricing initiatives. Between September 2013 and now, the average deposit return has dropped by 35 basis points. As we explained, banks are less reliant on deposits, and can get cheaper funding from other sources (and the recently announced QE in Europe will make funding even cheaper).

However, savers have see their returns falling thanks to deposit repricing initiatives. Between September 2013 and now, the average deposit return has dropped by 35 basis points. As we explained, banks are less reliant on deposits, and can get cheaper funding from other sources (and the recently announced QE in Europe will make funding even cheaper).

So, despite the fact that the banks are unlikely to be able to reduce their provisions much further (as they did last year) to bolster profits, and their increased capital requirements, the highlighted net increase in margins bodes well for bank performance, though at the expense of borrowers, who are not enjoying rate reductions, and depositors who are seeing their interest rates continuing to fall.

One thought on “Bank Spreads Have Increased By 35 Basis Points”