The Henderson Global Dividend Index found that total dividend payouts across all geographies rose a little – by 0.1 per cent – to reach US$1.154 trillion in 2016, reflecting flat profits. They are predicting a headline growth rate of 0.3 per cent in 2017 with global dividends forecast to reach US$1.158 trillion. The index covers the world’s largest 1,200 firms, representing 90% of global dividends paid.

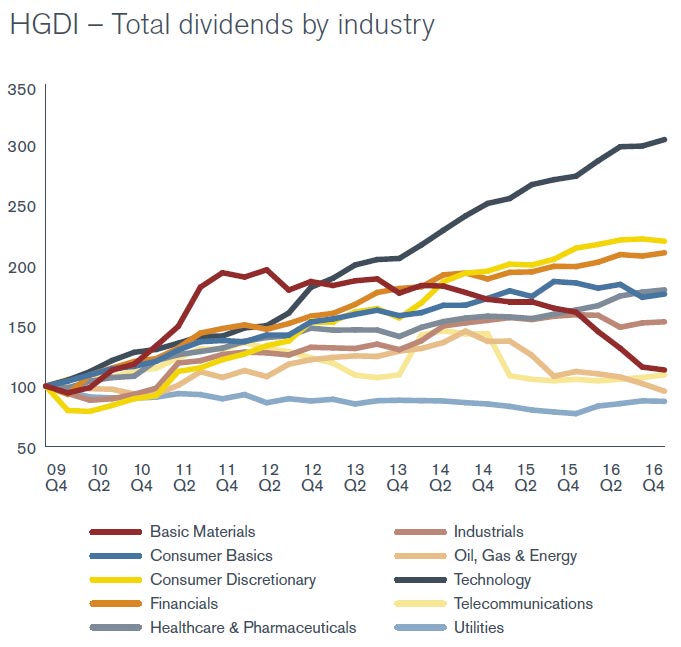

Strongest sectors were utilities, healthcare and technology, weakest were energy and mining sectors. Finance contributed 23 per cent of the total paid.

In Australia total dividends were US$41.8 billion, down 10.1 per cent on 2015. They say Australian dividends are more reliant on the payouts from just a few large stocks than any other developed country and is the largest payer in Asia Pacific excluding Japan, making up almost two-fifths of the total.

In Australia total dividends were US$41.8 billion, down 10.1 per cent on 2015. They say Australian dividends are more reliant on the payouts from just a few large stocks than any other developed country and is the largest payer in Asia Pacific excluding Japan, making up almost two-fifths of the total.

The report says declines in the mining sector inflicted the most damage, with dividend payouts down US$4.5 billion year-on-year. After adjusting for a slightly stronger Australian dollar, the underlying fall from the total market was 12.2 per cent. This included big dividend cuts from Woolworths and Woodside Petroleum.

But their next comment is important:

Together the banks account for half of the country’s total dividends, while CBA alone is responsible for $1 in every $5 distributed.

CBA was the 12th largest dividend payer in the world, with HSBC in 6th place in the rankings. These are the two highest placed finance sector companies.

Think about the implications of this given the talk about corporate tax cuts. Much of the benefit will flow to a small number of larger companies, and many of these have high numbers of overseas investors. So the flow of “stimulation” into the local economy is likely to be very small.

The North American dividend payments of US$443.7 billion grew at 0.5 per cent because of a series of special dividends and index changes, though underlying growth was 3.9 per cent. The USA accounted for two-fifths of global payouts.