APRA today published the quarterly ADI performance statistics to September 2014.

Over the year ending 30 September 2014, ADIs recorded net profit after tax of $33.5 billion. This is an increase of $3.6 billion (12.0 per cent) on the year ending 30 September 2013.

As at 30 September 2014, the total assets of ADIs were $4.2 trillion, an increase of $345.0 billion (9.1 per cent) over the year. The total capital base of ADIs was $210.4 billion at 30 September 2014 and risk-weighted assets were $1.7 trillion at that date. The capital adequacy ratio for all ADIs was 12.4 per cent.

Impaired assets and past due items were $29.1 billion, a decrease of $7.4 billion (20.3 per cent) over the year. Total provisions were $16.6 billion, a decrease of $6.1 billion (26.9 per cent) over the year.

We have been looking at the relative capital positions of the banks, highly relevant in the current climate where we expect the FSI inquiry report to be commenting on this, as well as the current regulatory reviews, globally and locally.

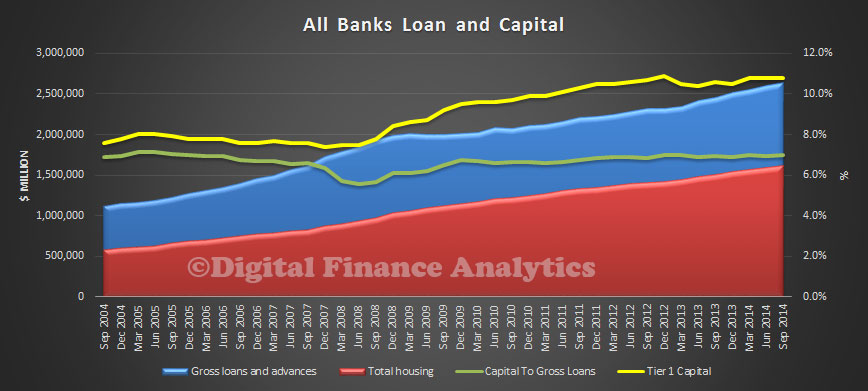

So we have taken the All Bank data and compared the Tier 1 capital ratio (the yellow line) with a plot of the ratio of lending to capital held. Because the mix of loans has changed, with a greater proportion relating to lending for housing, and the fact that these loans have lower capital weighting, the reported Tier 1 capital is significantly better than the true, unweighted position. In fact, banks are holding relatively less capital against their loan books now compared with before the GFC. This is one reason why capital ratios are under review.

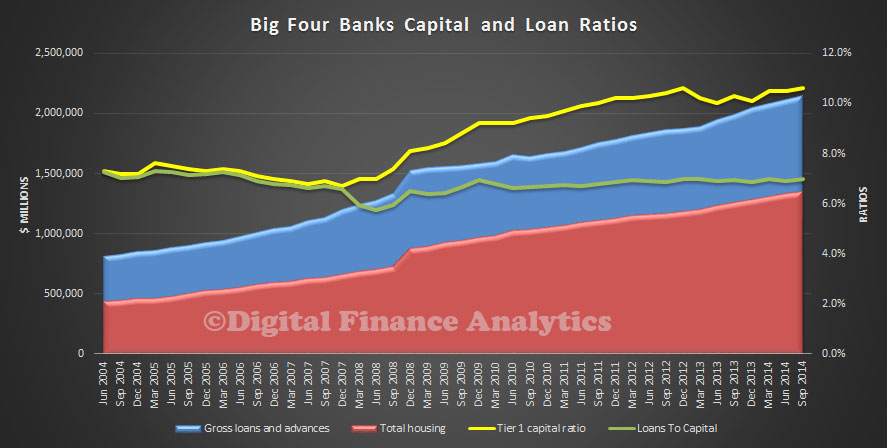

Now, if we look only at the APRA data for the big four banks, we see an even wider divergence, enabled by the advanced capital calculations which enable these banks to hold even less capital against certain housing loan categories. This places the major banks at a competitive pricing advantage.

Now, if we look only at the APRA data for the big four banks, we see an even wider divergence, enabled by the advanced capital calculations which enable these banks to hold even less capital against certain housing loan categories. This places the major banks at a competitive pricing advantage.

Almost certainly, the majors will be required, in due course to hold more capital, and this may tilt the playing field towards some of the smaller players. It may also mean lower returns of deposit accounts, and and reduced loan discounting. Overall profitability for some players will also be tested, though we believe there is plenty of slack in the system currently.

Almost certainly, the majors will be required, in due course to hold more capital, and this may tilt the playing field towards some of the smaller players. It may also mean lower returns of deposit accounts, and and reduced loan discounting. Overall profitability for some players will also be tested, though we believe there is plenty of slack in the system currently.

One thought on “Banks And Their Capital”