The Reserve Bank New Zealand has published an Analytics Note entitled “Diving in the deep end of domestic deposits“. They conclude that banks may need to limit credit growth unless they are able to grow retail deposits in line with credit growth.

Deposits are an important part of the New Zealand financial system. Deposits play a large role in funding bank lending – banks try to attract deposits in order to build up funds to lend out to borrowers. Over the past couple of years, lending has been growing faster than deposits, requiring banks to source funding from offshore wholesale funding markets. External funding can increase risks in the financial sector, as deposits are typically a more stable (“core”) source of funding than offshore wholesale funding.

This paper explores deposit growth in New Zealand in order to answer two questions:

1) What factors drive deposit growth in New Zealand, particularly in the past few years?

2) Can banks increase deposits by increasing interest rates?

We use two models to explore the dynamics of household deposits in New Zealand’s banking system in order to answer these questions. The first model uses bank-specific data from New Zealand’s four largest banks, while the second uses aggregate data for the entire banking system.

The paper highlights that the rate of domestic deposit growth has varied significantly since the Global Financial Crisis, and sharply slowed over 2016. We provide evidence that a range of supply and demand factors influence deposit growth, and that the recent slowing was largely driven by a reduction in supply (that is, households wanting to allocate less money to deposit products). We also find that banks increased their demand for deposits in late 2016 in an effort to close the gap between deposit growth and lending.

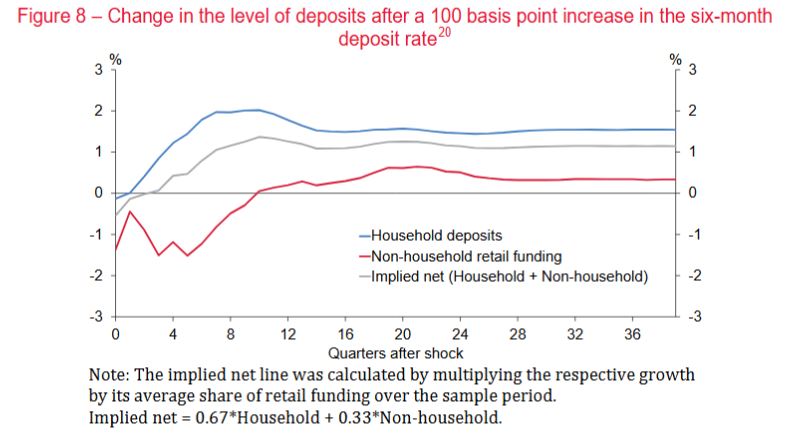

We also consider the degree to which banks are able to increase deposit growth materially by raising interest rates. We find that a 1 percentage point increase in the six-month deposit rate can increase the level of household deposits by about 1 percent after four quarters, and by 1.3 percent in the long-run.

As we find that deposits are not strongly responsive to interest rates, if banks wish to maintain robust funding profiles by not becoming too reliant on offshore wholesale funding, they may need moderate credit growth or use a combination of approaches to bring deposit growth in line with credit growth.

The Analytical Note series encompasses a range of types of background papers prepared by Reserve Bank staff. Unless otherwise stated, views expressed are those of the authors, and do not necessarily represent the views of the Reserve Bank.