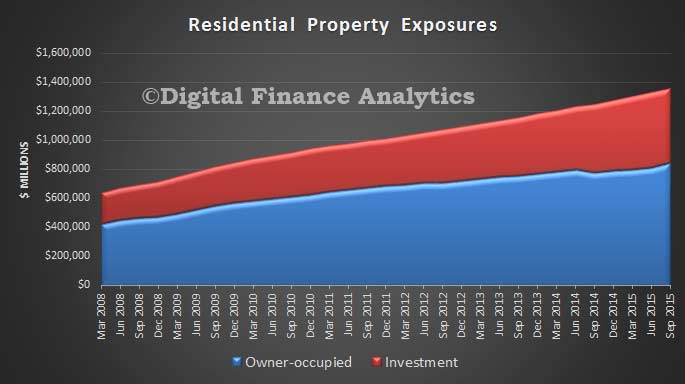

The latest APRA Property Exposure data, to September 2015 provides an additional perspective on the loan books of the ADI’s. Overall property exposures are a record $1.35 trillion, up from $1.33 trillion in June, and up 9% on September 2014. Within the mix, owner occupied loans rose from $810 bn to $841 bn, up 8.9% from 2014; in response to the changed lending environment, whilst investment loans for residential property fell from $517 bn to $514 bn, the first fall in a long long time (APRA data goes back to 2008), but still up 9.1% from September 2014. Within the data we can see the adjustments which the ADI’s have made as they reclassify loans. A process which is not yet complete.

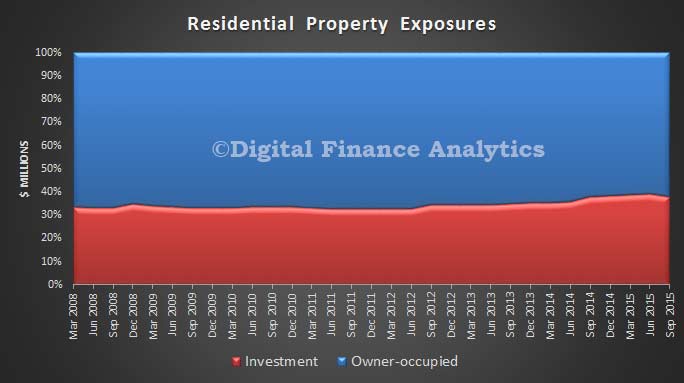

Investment loans comprise 37.9% of all loans, a fall from 38.9% last quarter, but still worryingly high, and higher than the regulators previously had thought.

Investment loans comprise 37.9% of all loans, a fall from 38.9% last quarter, but still worryingly high, and higher than the regulators previously had thought.

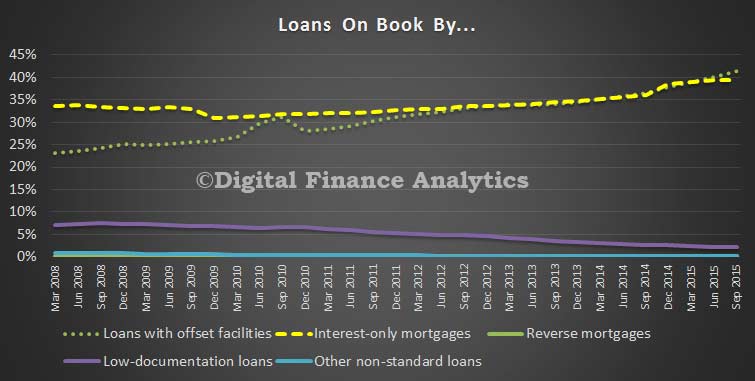

Looking at some of the key characteristics of loans on book, 40% of loans (by value) have offset facilities, and 35% are interest only loans. There appears to be a slight slowing in the growth of interest only loans, reflecting the changed lending environment, and a slowing in investment lending. But see below for data on new loans.

Looking at some of the key characteristics of loans on book, 40% of loans (by value) have offset facilities, and 35% are interest only loans. There appears to be a slight slowing in the growth of interest only loans, reflecting the changed lending environment, and a slowing in investment lending. But see below for data on new loans.

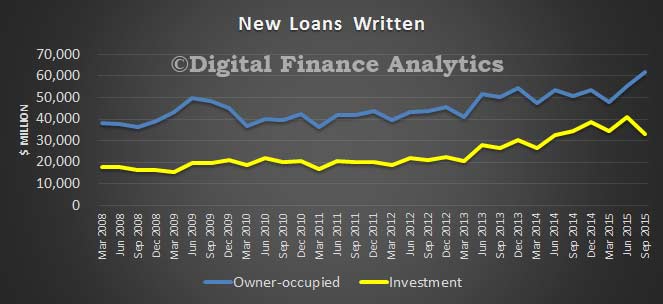

The volumes of new loans being written is still strong, with close to 100,000 being written each month. Owner-occupied loan approvals were $219.0 billion (59.8 per cent), an increase of $13.1 billion (6.4 per cent) from the year ending 30 September 2014;

The volumes of new loans being written is still strong, with close to 100,000 being written each month. Owner-occupied loan approvals were $219.0 billion (59.8 per cent), an increase of $13.1 billion (6.4 per cent) from the year ending 30 September 2014;

investment loan approvals were $147.0 billion (40.2 per cent), an increase of $23.4 billion (19.0 per cent) from the year ending 30 September 2014.

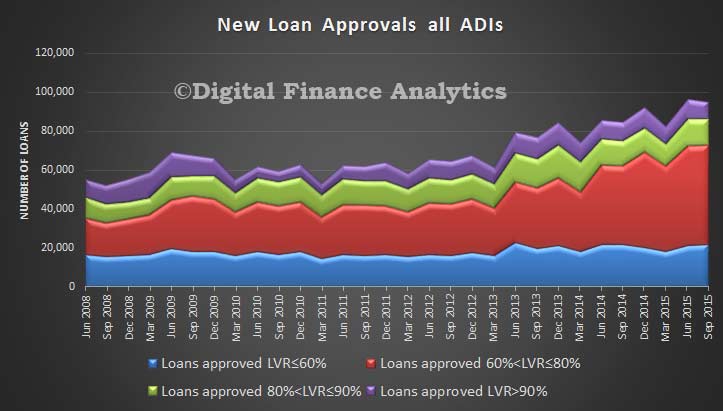

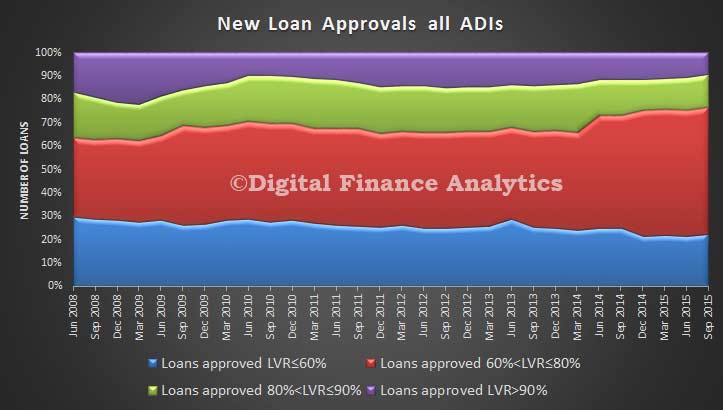

The LVR splits show the bulk of loans are in the 60-80% band, and there is a fall in the LVR above 90% being written.

The LVR splits show the bulk of loans are in the 60-80% band, and there is a fall in the LVR above 90% being written.

The distribution chart below shows this well, and also shows that around 24% of loans are still be written above 80% LVR – at a point in the cycle where house prices in Sydney and Melbourne are probably close to their peaks, and values are falling in some other states.

The distribution chart below shows this well, and also shows that around 24% of loans are still be written above 80% LVR – at a point in the cycle where house prices in Sydney and Melbourne are probably close to their peaks, and values are falling in some other states.

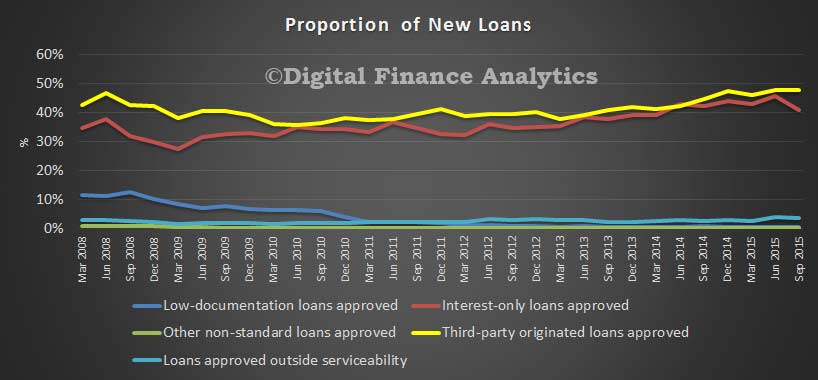

Data on the characteristics of the new loans shows a fall in new interest only loans being approved (but still more than 40% of new loans are interest only, and as we know these contain more potential risks later). The proportion via brokers sits at 47.7%, just a tad lower than last quarter, but it shows how important the broker sector is, in terms of originating new loans. There are a small number of new loans still being approved outside standard serviceability, at 3.6% in the past quarter, slightly lower than then 3.8% in June, but still higher than in previous times. Given the tighter lending standards, this is a concern. Only 0.4% of new loans are low documentation loans via the ADI’s though more are being written via the non-bank lenders, and so are not caught in these figures.

Data on the characteristics of the new loans shows a fall in new interest only loans being approved (but still more than 40% of new loans are interest only, and as we know these contain more potential risks later). The proportion via brokers sits at 47.7%, just a tad lower than last quarter, but it shows how important the broker sector is, in terms of originating new loans. There are a small number of new loans still being approved outside standard serviceability, at 3.6% in the past quarter, slightly lower than then 3.8% in June, but still higher than in previous times. Given the tighter lending standards, this is a concern. Only 0.4% of new loans are low documentation loans via the ADI’s though more are being written via the non-bank lenders, and so are not caught in these figures.