Bendigo and Adelaide Bank (BEN), Australia’s fifth largest bank, today announced an after-tax statutory profit of $227.3 million for the six months ending 31 December 2014. The results were in line with the consensus expectations. Underlying cash earnings were $217.9 million, a 10.9 per cent increase on the prior half year result. Bad and doubtful debts expense was $30.1 million, down 29.5% on the prior corresponding period. NIM was maintained at 2.24%. Cash earnings per share were 48.1 cents, an increase of 3.4 per cent.

The interim fully franked dividend of 33 cents per share is up 2 cents on the 2014 interim dividend.

Basel III CET1 ratio increased by 12bps half on half to8.14% and an $292m additional Tier 1 capital issued in October. $600m RMBS was issued in December 2014. Total capital increased 80bps half on half to 12.19%.

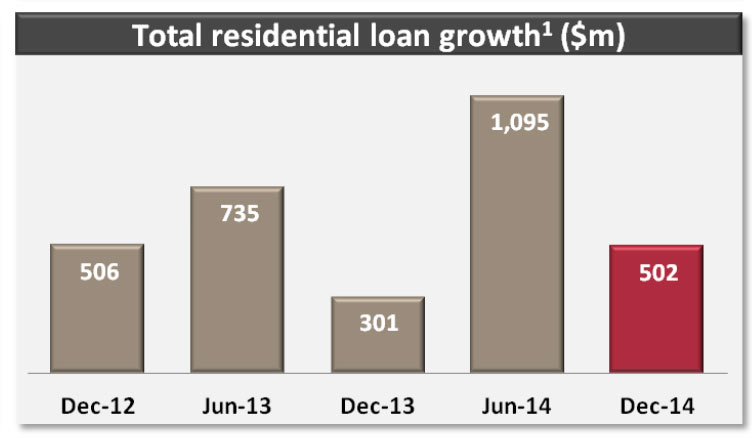

Looking at the segmentals, Retail banking was up 14.2% from Jun 2014 ($128m to $146m), Third party banking was down 4.6% from Jun 2014 ($95.8m) to $91.4m, Wealth fell 37.5% from $19.5m to $12.0m and Rural rose 73.3% from $24.3m to $42.1m including the Rural Finance acquisition – in In July 2014, Bendigo finalised its $1.78 billion acquisition of Rural Finance Corp. from Victoria’s state government which has grown its agricultural lending. Overall, home lending grew at just 3.2% compared with system growth of 7.1%, whilst arrears were around 0.5%. There was strong competition through the broker originated channel.

They grew business lending by 19.7% compared with system of 7.4%. Business loan arrears were around 1.4%. Deposit growth was 1.5%, compared with system of 9.1%. Bendigo had an 8 basis point squeeze on lending margins thanks to competitive pressures and as a result they reduced term deposit pricing to help partly offset this so the net interest margin remained unchanged. Customer satisfaction remains higher than the majors, highlighting their unique position in the market.

They grew business lending by 19.7% compared with system of 7.4%. Business loan arrears were around 1.4%. Deposit growth was 1.5%, compared with system of 9.1%. Bendigo had an 8 basis point squeeze on lending margins thanks to competitive pressures and as a result they reduced term deposit pricing to help partly offset this so the net interest margin remained unchanged. Customer satisfaction remains higher than the majors, highlighting their unique position in the market.

The market reacted negatively to the results, because the growing business lending sector may imply higher loss rates, pressure on home lending margin and share, and reduced provisioning.