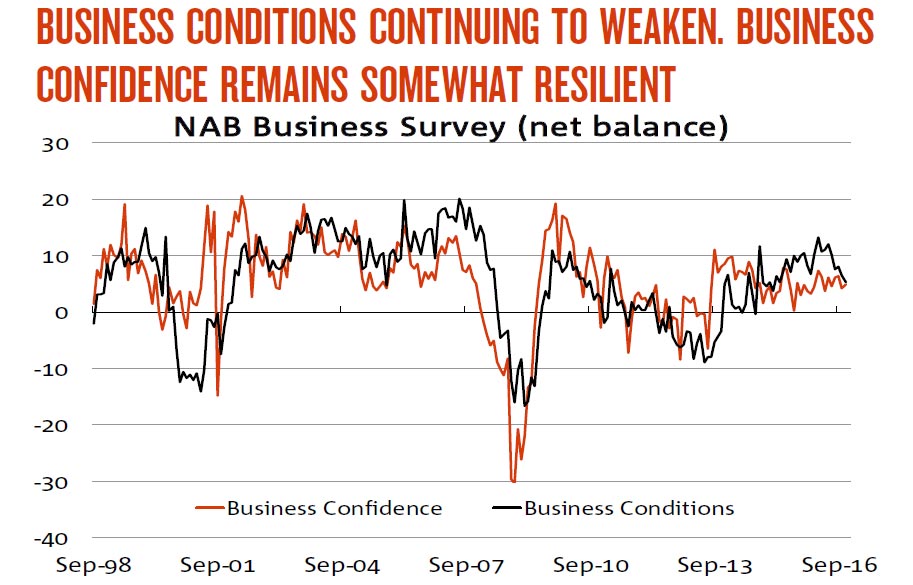

The November NAB Monthly Business Survey gave more hints of a moderation in the non-mining economic recovery.

Business conditions slid further in the month, dropping back to long-run average levels for the first time since April 2015 – largely driven by profitability and trading conditions (sales), as employment conditions were steady at already subdued levels.

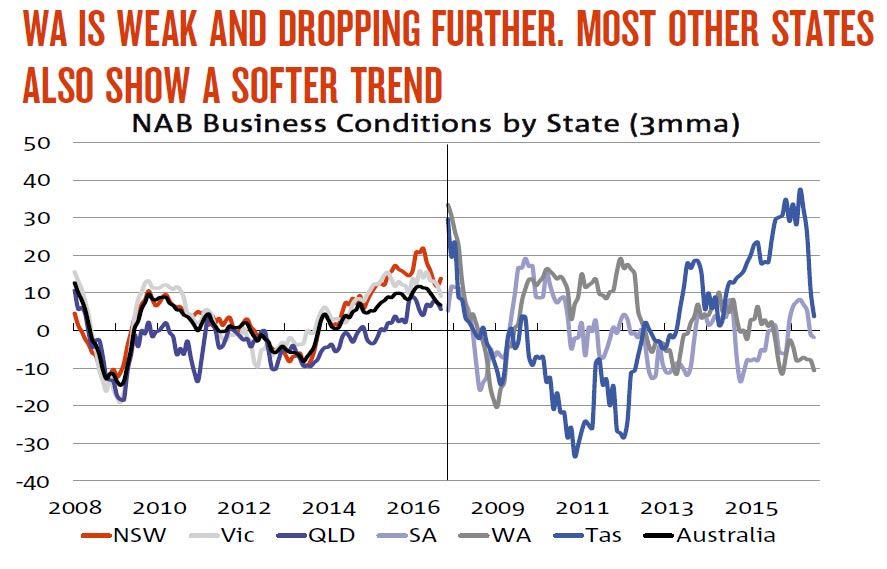

However, in spite of the declining trend in business conditions, business confidence has remained relatively resilient, tracking broadly sideways in recent times and showing a modest improvement in November. For the month of November, the business conditions index dropped 2 points, to +5 index points, which is in line with the series long-run average. The retail industry continues to be a major drag on conditions, despite signs of improved retail sales recently, and now has the equal worst business conditions (along with mining). Inflation measures in the Survey remained subdued, with retail price growth remaining flat – despite notable increases in upstream retail costs.

In the context of numerous global uncertainties and weakening business conditions, the resilience of business confidence has been encouraging. With that said, it is not clear what effect (if any) the recent US election result has had on confidence. The business confidence index rose 1 point, to +5 index points in November – although this is slightly below the series long-run average (+6). But while confidence has been relatively resilient, it is not at levels conducive of higher levels of investment activity – confirmed by disappointingly soft investment intentions in the recent ABS Capex Survey. Nonetheless, the capex measure in the NAB Business Survey remained positive this month, consistent with an increase in capacity utilisation rates, although forward orders remained soft.