According to the latest NAB Business Survey for January 2017, both business conditions and confidence jumping to much higher levels.

The strength witnessed in last month’s NAB Monthly Business Survey continued into January, with both business conditions and confidence jumping to much higher levels. While these outcomes are certainly pointing to an improvement in the domestic economy after a soft patch through much of H2 2016, a degree of caution should still be exercised given the diverse and rapidly changing seasonal influences at this time of year (which potentially includes the shift in Chinese New Year to January this year).

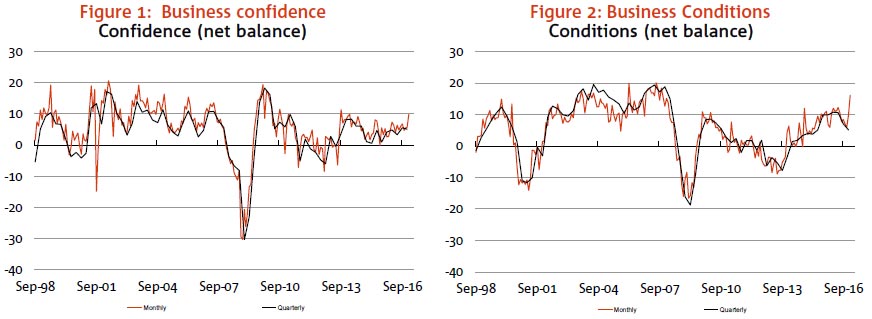

In terms of the headline numbers, the business conditions index jumped by a solid 6 points in January, to +16 index points, which is around pre-GFC boom levels. This month, another rise in trading conditions contributed to the outcome, but there was also a noticeable jump in employment conditions, which bodes well for the generally underperforming labour market – the employment index hit its highest level since 2011.

Meanwhile, profits were unchanged at solid levels. By industry, last month’s surprise spike in wholesale conditions was unwound (as anticipated), but that seems to have been more than offset at the aggregate level by improvements in personal services, while retail and mining are no longer negative. NSW enjoyed the bulk of the improvement in conditions, while the rest of the mainland states were relatively steady. Cost price measures in the Survey also lifted notably, suggesting a build in wage pressures, although retail price inflation remained very subdued.

Business confidence also jumped in the month, aligning itself with the general enthusiasm seen in financial markets and more positive sentiment towards the global economic outlook. The business confidence index jumped 4 points to +10 index points in January, which was well above the series long-run average. Responses on capital expenditure were also much more encouraging in January, consistent with a rise in capacity utilisation – although forward orders do not point to a continuation of that strength in the near-term.

Recent strength in the NAB Business Survey is consistent with an anticipated rebound in economic activity, following the very weak Q3 2016 National Accounts. With that said, a confluence of seasonal factors suggests it is unwise to get too carried away with the result just yet, especially as key industries like retail remain extremely weak (despite improving in the month), which suggests the outlook for consumption remains cloudy. NAB Economics also have concerns for the longer-term growth picture, as the contribution from LNG exports, temporarily higher commodity prices and the residential construction boom fade, keeping pressure on the labour market.

Nevertheless, in light of the recent flow of data, NAB’s economic forecasts (which include expectations for the RBA’s cash rate) are currently under review – to be published tomorrow.