ASIC says that following an ASIC investigation of Get Approved Finance, a West Australian car finance provider, Esanda has agreed to compensate more than 70 borrowers for car loans organised by Get Approved Finance.

ASIC’s investigation found that between 2011 and 2014, over 15 brokers employed by Get Approved Finance engaged in unfair conduct by having Esanda approve loans for consumers with poor credit histories, who otherwise did not meet Esanda’s lending criteria. The brokers arranged for a friend or relative of the consumer to become the nominated borrower, instead of the consumer who was not eligible for credit. They did this by misleading the friend or relative about the effect of the documents they were signing, for example, by stating they were a guarantor rather than the borrower.

The Get Approved Finance brokers also sold add-on products (such as insurance or warranties), on behalf of various insurers, to some borrowers without their knowledge or consent. The additional premiums increased the amount borrowed and therefore the risk of borrowers defaulting. In one case, the consumer was sold add-on products costing more than $15,000, increasing the amount borrowed from around $24,000 to over $39,000.

The total value of the loans financed was more than $1.38 million, with some loans approved of over $50,000.

Get Approved Finance was able to earn commissions from both Esanda and the providers of the add-on products that would have been lost if Esanda had rejected the applications for credit. ASIC was concerned that Esanda did not have systems in place to manage the risks created by these commission payments or to effectively identify the serious misconduct by the Get Approved Finance brokers, given that it continued for over two years.

Esanda is a division of Australia and New Zealand Banking Group Ltd.

West Australian-based finance broker, Jeremy (WA) Pty Ltd, trades as Get Approved Finance.

According to ASIC, National Australia Bank (NAB) has made changes to its debt collection practices following ASIC concerns that some of NAB’s collection letters may have been misleading, deceptive or unconscionable.

ASIC was concerned that NAB was sending debt collection letters to customers using letterheads for “Fairhalsen Collections” and “Brunswick Collections Services”, which may have given the incorrect impression that NAB had sold, outsourced or otherwise escalated a debt when this was not the case. These letters only disclosed that the entity was a division of NAB in fine print at the bottom of the page.

ASIC was also concerned that letters sent to some customers during the collection process stated that if the debt was not paid, or contact made:

legal proceedings for recovery of the entire debt might commence without further notice and that such proceedings could result in a judgment being entered and/ or bankruptcy;

a debt collector might visit the customer’s home to collect the debt; or

NAB might use any other legal action necessary to collect the debt.

In fact, for the majority of recipients, such action was either unlikely or would only be considered at a later stage in the collection process.

In response to ASIC’s concerns NAB has removed from its collection letters:

references to Fairhalsen Collections and Brunswick Collection Services

representations in relation to face-to-face contact, legal action and bankruptcy (unless such action is likely to occur).

ASIC Deputy Chairman Peter Kell said, ‘Creditors and collectors are entitled to accurately explain the consequences of non-payment of a debt, but the consequences must not be misrepresented or overstated. The threat of legal proceedings and bankruptcy can be very stressful. Collectors must not threaten legal action if such action is not possible, not intended, or not under consideration.’

Regulators here and overseas are forcing banks to hold more capital in order to make the banking system “more secure”. In Australia, because of the lack of true competition, this will in practice mean the banks passing additional costs through to borrowers, thus maintaining the high (on an international basis) shareholder returns. Higher capital means higher priced bank products.

However, continuing to lift capital ratios will not alone make banks more secure. There are other strategies which we need to consider if we are truly to have undoubtedly strong banks. We need, in effect, to broaden the debate.

First, one of the main drivers of higher capital is to ensure that banks, should they get into trouble, would not be bailed out by tax payers via government intervention. In 2007, the UK the government became the major shareholder in a number of banks, which were on the brink. This led in turn to significant public debt, which has yet to be repaid. The FSI estimated that the economic cost of a severe financial sector crisis is around 158 per cent of annual GDP. For Australia, this is around $2.4 trillion. And this is just the annual cost. The question becomes how to handle banks that are too big to fail and get into difficulty. It should be essential for banks to think the unthinkable, and have in the bottom draw a secure exit plan should they get into difficulty, and this resolution plan has to be approved by the banking regulator. It should not simply be “raise more capital”, because as the APRA stress tests highlighted recently, individual banks assumed they could top up their reserves in a crisis, but did not consider the fact that everyone might be trying to do this at the same time (because of a broader crisis) as so might not be successful.

Second, and connected to the work-out plans, we think there is a case to ring-fence the retail bank operations of these large financial conglomerates, from their other operations. Risks in the treasury, wealth management, insurance, and international trade areas are potentially higher than in core retail banking. At the moment, it is all scrambled. The UK for example, to working towards adequate risk separation of core banking operations and the other elements within financial conglomerates. Whilst implementation needs to take account of the structure of individual entities, we think this is important.

Third, the obligations of the top managers in the banks with regards to complying with regulation should be clearly stated and enforced. We have seen some banks essentially flex lending standards to maintain market share. APRA and ASIC have both highlighted these shortcomings and the RBA have admitted risks were higher than initially thought because of loose lending criteria. The obligations on top managers should have legal force, and in severe cases of non-compliance, regulators should be more overtly holding them to account personally. More broadly, this speaks to the cultural norms within the banks, and the incentives in place. It also balances the obligations of regulators and those managing the banks – at the moment, it appears the onus is too much on the regulators to try and “catch” bad behaviour, rather than having the right behaviours championed by the banks themselves. This balance needs to be recast.

Fourth, we need stronger, real competition in the banking sector, not the faux competition where everyone marches to the same tune, and follows each other with rate rises and falls. We have some of the most profitable banks in the world, thanks to weak competition, not brilliant management, or super efficiency. Regulators are more concerned with financial stability than competition, though moving the dial on IRB banks from 15-17 to 25 is a starting point, tweaking capital is not sufficient. With so many regulatory authorities involved, from ACCC, APRA, ASIC and RBA, the onus of driving real competition falls through the cracks, at the expense of Australia Inc. The FSI recommended ASIC be given a specific competition mandate.

We should not become myopic about more capital being the total solution to fixing the banking system. Structure, culture, competition and governance must all be on the table.

ASIC has announced that from today, National Australia Bank (NAB) will be contacting customers who may have received non-compliant advice since 2009. Affected clients will have their files reviewed to determine if compensation should be paid. NAB will also provide affected customers with financial assistance to seek professional independent advice where appropriate.

ASIC has worked with NAB to develop their Financial Advice Customer Response Initiative (CRI), a large review and remediation program for customers affected by non-compliant advice. ASIC will ensure that the CRI will provide a fair and effective mechanism for customers to be properly compensated (REF: MR15-101). The CRI will also be subject to independent scrutiny by an external consultant, which will report its findings to ASIC. ASIC acknowledged NAB’s co-operation in this matter. This action is associated with ASIC’s broader Wealth Management Project (refer MR15-081).

Background

The Wealth Management Project was established in October 2014 with the objective of lifting standards by major financial advice providers The Wealth Management Project focuses on the conduct of the largest financial advice firms (NAB, Westpac, CBA, ANZ and AMP). ASIC’s work in the Wealth Management Project covers a number of areas including; (i) ASIC’s work with other the Wealth Management participants to address the identification and remediation of non- compliant advice. This is in addition to the work ASIC is doing to ensure appropriate customer remediation where fees have been charged and no advice service has been provided; ii) Seeking regulatory outcomes where appropriate against Licensee’s and advisers. For example, since ASIC’s Wealth Management Project commenced ASIC has banned the following advisers from the financial services industry:

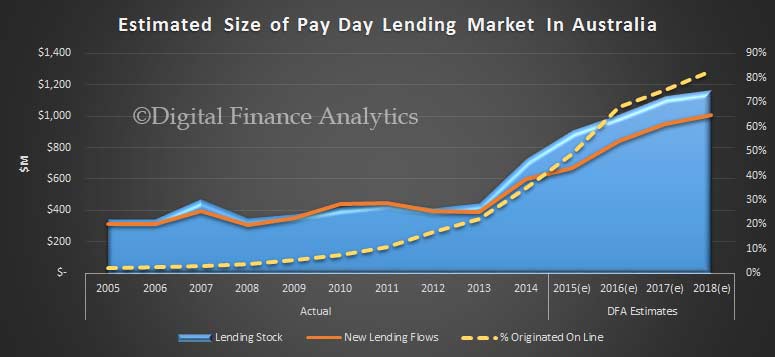

We review detailed data from the 2005, 2010 and 2015 surveys as a means to dissect and analyse the longitudinal trends. The data results are averaged across Australia to provide a comprehensive national picture. We segment Australian households in order to provide layered evidence on the financial behaviour of Australians, with a particular focus on the role and impact of payday lending.

We think the overall size of the market is growing, thanks to the rise on online access, and we recently posted our modelling, which we summarise below:

The transference to online channels is linked with a rise in the number of households who, whilst not financially distressed (distressed households are first not meeting their financial commitments as they fall due, and are also exhibiting chronic repeat behaviour, and have limited financial resources available) are financially stressed (struggling to manage their financial affairs, behind with loan repayments, in mortgage stress, etc).

Digital disruption opens the door to new lenders (local and overseas), and makes potential access to this source of credit immediate. The volume of loans is set to increase and more than ever will be originated online. In addition, some digital players offer special member designated areas secured by a password, where special offers and repeat loans could be made away from public sight. Online services are now mainstream, and this presents significant new challenges for customers, policy makers and regulators.

Some of the key points (as summarised by Good Shepherd Microfinance) from the report:

• The total number of households using a payday lending service in the past three years has increased by more than 80 per cent over the past decade (356,097 to 643,087 households).

• All payday borrowers were either ‘financially stressed’ (41 per cent) in that they couldn’t meet their financial commitments or ‘financially distressed’ (59 per cent) because in addition to not meeting their financial commitments, they exhibited chronic repeat behaviour and had limited financial resources.

• 2.69 million households are in ‘financial stress’ which represents 31.8 per cent of all households and is a 42 per cent increase on 2005. Of the households in financial stress, 1.8 million are ‘financially distressed’ (just over 20 per cent of all households) – a 65 per cent increase on 2005.

• The number of people who nominated overspending and poor budget management as causes of financial stress had decreased over the past 10 years (from 57.2 per cent to 44.7 per cent). Unemployment has become a more significant factor with over 15 per cent of households indicating this caused their financial problems.

• In 2005, telephone and local shops were the most common interface to payday lenders. By 2015, more than 68 per cent of households used the internet to access payday lending. Mobile phones and public personal computers (eg libraries) were the most common device used.

• The number of borrowers taking out more than one payday loan in 12 months has grown from 17.2 per cent in 2005 to 38 per cent in 2015 and borrowers with concurrent loans have increased from 9.8 per cent to 29.4 per cent in the same period.

• The top three purposes for a payday loan were: emergency cash for household expenses (35.6 per cent). Emergency cash for household expenses included children’s needs (22.7%), clothing (21.6%), medical bills (15.1%) and food (11.4%). More payday loans are being used to cover the costs of internet services, phone bill and TV subscriptions (7.8 per cent) than in 2005 and 2010.

• Many distressed households (38.7 per cent) were refinancing another debt and 36.8 per cent already had another payday loan when taking out their payday loan. Around half of the households that had used payday lending services indicated they would be willing to take out another payday loan.

• Single men were more likely to use a payday loan (53 per cent) and the average age of the borrower was 41 years old. In the last five years, households in their thirties almost doubled their use of payday loans (16.3 per cent in 2005 to 30.35 per cent in 2015). Only 5.26 per cent of borrowers had a university education. The average annual income of payday borrowers in 2015 was $35,702.

• ‘Financially distressed’ households generally use payday loans either because it is seen as the only option (78 per cent), while ‘financially stressed’ households are attracted by the convenience (60.5 per cent).

St George Bank ruined a lot of bank holiday plans this weekend when their online banking systems stopped working.

The bank’s Internet systems appear to have stopped working on Sunday evening and were still unavailable almost 24 hours later on Monday afternoon. ATMs were working but, as it was a bank holiday, branches were closed meaning that people who rely on the Internet for account transfers and overseas credit card transactions were out of luck.

Apart from a short message acknowledging the outage on their website, St George has not yet given details of the causes of the problem.

But this was not the only recent Internet banking outage at a major bank.

On the 11th and 12th September, the Commonwealth Bank (CBA) suffered a prolonged disruption to its IT services in particular its ‘industry leading’ banking platform – NetBank. And this was not the only prolonged outage at CBA this year. There were IT service disruptions earlier this year, with failures to transfer money into and out of accounts, thus racking up late and overdraft fees for customers. And also last year, and before that …….

For those who would like to see the impact of such outages on CBA customers, the excellent website Aussieoutages has a whole section devoted to CBA and a blog on which customers can register their frustration, with many of the comments NSFW – as social media terms bad language.

So what has the Commonwealth Bank to say for itself about the latest outages? Nothing!

Where are the banking regulators when banking customers are inconvenienced by the banks that they are paying records fees to?

Unfortunately, APRA and ASIC continue to play pass the parcel on banking regulation.

OK, but which regulator should be wielding the big stick?

In 2011, DBS Bank, the largest bank in Singapore, suffered a computer outage that deprived its customers of access to banking services for about seven hours (half of that experienced by St George customers).

After an investigation, the local banking regulator, the Monetary Authority of Singapore (MAS) hit DBS with a stern rebuke and a set of new regulatory requirements. The bank was also ordered to “redesign its online and branch banking systems platform to reduce concentration risk and allow greater flexibility and resiliency in operation and recovery capability”. In other words – fix your IT systems, or else.

Importantly, the regulator ordered DBS to increase the capital held in reserve for ‘operational risks’ by 20 per cent, or around $180 million. Under the Basel II banking regulations, banks are required to maintain a capital buffer against operational losses, in particular ‘systems risks’.

Because the failure of Internet systems is clearly an operational risk problem, APRA should be considering at least a 20% addition to the operational risk capital charge on Commbank and Westpac (which owns St George and the other banks like BankSA which went offline at the same time). According to Commbank’s latest Risk (so-called Pillar 3) report, which incidentally has pictures of happy Internet users on the front page, a 20% increase would have CBA having to raise just over an additional $500 million of capital. On the same basis, Westpac would require just under $500 million extra capital. Good luck with that, when banks are scrambling to raise capital to cover upcoming regulatory changes.

But has APRA moved to get the IT systems of the country’s biggest banks under control? No sign so far.

So what of ASIC?

ASIC has recently released its regulatory stance on so-called Conduct Risk, or “the risk of inappropriate, unethical or unlawful behaviour on the part of an organisation’s management or employees”. Conduct Risk is the very latest in regulatory fashion and is an attempt to get banks to treat their customers more fairly.

One would have thought that, in return for account fees, providing access to customers’ own money might be a start for banks?

But a quick look at the ASIC web-site shows the usual list of fines and suspensions on financial institutions so tiny that small fry seem huge. But not a whale or even a barramundi in their nets. ASIC does not go after the big fish.

So which regulator should be going into bat for the costumers of the big banks?

Both!

APRA to ensure that IT systems in banks are robust, by using capital tools. And ASIC to ensure that banks treat customers fairly. Demanding return of fees for non-performance might be start?

Author: Pat McConnell, Honorary Fellow, Macquarie University Applied Finance Centre, Macquarie University

Lending money is a risky business. Since 2010, Bank of England figures reveal that lenders have written off an average of £13.2 billion a year in bad loans. You can never be 100% sure that you will ever get your money back.

One way of mitigating that risk is to know as much as possible about the person you are lending to. Indeed, some financial managers reportedly are now considering the use of personality tests to assess the suitability of borrowers seeking loans or credit agreements.

A new model developed by the University of Edinburgh’s Business School, for example, asks borrowers questions designed to reveal their trustworthiness. But could such tests, already used in various forms by some businesses to assess the suitability of potential employees, really work for lenders?

Predicting the future

The conventional way to assess the likelihood that someone might default is to look at their income and expenditure, their assets and their commitments, and make predictions on the basis of their financial circumstances. We also know that a person’s “credit history” is important – it is useful to know if a person has defaulted on loans before, or has other credit problems in their past.

This is all psychologically valid. It’s a well-known principle that the best predictor of future behaviour is past behaviour. But how do you make predictions where someone has little or no credit history?

This is where psychological tests could come in, and there is some superficial attractiveness here. If – and the word “if” is important – a person’s likelihood to default on a loan was related to their “personality”, and if (again) that was a measurable trait, and if (yet again) that trait could be measured in a way that was impervious to fraud or manipulation, and if – finally – such a questionnaire was asking questions that were something other than the obvious (or the spurious), then they could indeed be a useful tool.

Gaming the system

But there are problems. We learned recently that psychological science is good, but it’s a long way from infallible. In an attempt to replicate key psychological experiments, scientists found that they could substantiate the findings in only about half the studies examined. That may not mean we should lose faith in all psychologists, but it does mean that we should be a little sceptical when we’re told that a particular set of questions can predict loan defaulters.

Indeed, looking at the reported questionnaires, there seem to be a curious mix of questions, including: “I believe others try to do the right thing”, “I believe in human goodness” and “I pay attention to small details”. There may well be links between people’s typical responses to these questions and financial soundness, but the evidence would have to be convincing.

It’s much more likely that, if people want a loan, they will try and game the system. There is a strong chance they would give the answers that they think reflect a better credit trustworthiness: “I definitely pay attention to financial details. I am perhaps, if anything, too cautious.” As opposed to: “Oh, I don’t care, just give me the cash.” Any psychological assessment scheme would have to be robust to such game-playing, perhaps by asking more opaque questions.

Real data

But there’s a more insidious problem. According to the proponents of this approach, the idea is to protect a lender’s assets by assessing “how trustworthy, reliable, emotionally stable and conscientious a customer might be”. First, there is the very real difficulty of assessing these things, as pointed out by, among others, James Daley, of the consumer group Fairer Finance: “If banks think they can psychologically screen bad debt risks, they are deluding themselves.” But, more than this, very many trustworthy, reliable, emotionally stable and conscientious customers find themselves in financial difficulties, often as a result of economic forces entirely outside their control.

Past behaviour is the best predictor of future behaviour. Where there is very little data to go on, it’s then usually the case that people’s behaviour is best explained by looking at the circumstances of their lives. Doing this through personality tests, however, is clearly very tricky.

I am a professional psychologist, and proud to be one. I believe that my profession has much to offer, in the world of mental health and even in the world of politics.

But I also believe that very little of the potential of psychological science is revealed by “personality tests” that purport to address problems that, in truth, are better addressed through other means.

Author: Peter Kinderman, Professor of Clinical Psychology at University of Liverpool

In a speech given by Greg Medcraft, Chairman, Australian Securities and Investments Commission at the 32nd annual conference of the Banking and Financial Services Law Association (Brisbane), he looked at the Financial System Inquiry from a regulator’s perspective.

Specifically, he sees three FSI recommendations as complementary. Product intervention powers would complement and reinforce the good practices and controls required by product design and distribution obligations. Where product design and distribution obligations were in place, and were effectively being complied with, there would be less need for ASIC to intervene. Adequate penalties provide a deterrent for gatekeepers against engaging in misconduct, and this in turn influences their behaviour. Gatekeepers who already have a solid culture have nothing to fear from these recommendations. For those who fall short, ASIC will continue to use the right nudge to change their behaviour. The introduction of a product intervention power, design and distribution obligation and appropriate penalties will assist ASIC in providing the right nudge.

Today I would like to talk about three particular recommendations of significance to ASIC.

1. for ASIC to have a new ‘product intervention’ power

2. to introduce a new product design and distribution obligation on product issuers, and

3. that penalties should be increased to act as a credible deterrent, and that ASIC should be able to seek disgorgement of profits gained by wrongdoing.

I would like to spend a little time now speaking about each of these recommendations in turn.

Product intervention power

Globally, regulators are looking for a broader toolkit to address market problems, including moving away from purely disclosure-based regulation. For example, the International Organization of Securities Commissions (IOSCO) has recommended that regulators look across the financial product value chain, rather than simply disclosure at the point of sale. In the United Kingdom, the Financial Conduct Authority has a product intervention power in place. A product intervention power would give ASIC a greater capacity to apply regulatory interventions in a timely and responsive way. It would allow ASIC to intervene in a range of ways where there is a risk of significant consumer detriment. ASIC would be able to undertake a range of actions, including simple ‘nudges’, right through to product bans. I know that some commentators have been worried that ASIC would use its powers to ban products – and that this would affect innovation and competition.

We think that such a power would not stifle innovation that has a positive impact on consumers. In fact, banning products would be very rare and would only occur in the most extreme circumstances. Both industry and regulators have a common interest in seeing innovation that fosters investor and financial consumer trust and confidence – innovation that helps investors, but does not harm them. Most interventions would likely fall well short of product banning. For example, we might be able to require amendments to marketing materials, or additional warnings. In more extreme cases, we might be able to require a change in the way a product is distributed or, in rare cases, ban a particular product feature. We agree that the use of intervention powers by ASIC would naturally need to have transparency, clear parameters and accountability mechanisms.

However, let me say that a ‘product intervention’ approach – that is, regulation that is not purely based on disclosure – is not new in the regulation of retail financial markets in Australia. This kind of regulation has improved investor outcomes in a wide range of markets over many years, for example: the Future of Financial Advice (FOFA) reforms, including the restriction on conflicted remuneration, and more broadly, the prohibition on unfair contract terms for financial products.

The FSI’s recommendation would mean that ASIC itself would have greater capacity to apply such non-disclosure based approaches in a timely and responsive way. This would be an alternative to waiting – sometimes many years – for legislation to address the problem.

Product design and distribution obligation

I will now turn to the recommendation to introduce a product design and distribution obligation for product issuers. For this recommendation, I want to set the context from ASIC’s perspective. There are three cornerstones of the free market-based financial system. These are: investor responsibility, gatekeeper responsibility, and the rule of law.

The ability of the free market-based system to function effectively and efficiently, and to meet investor and financial consumer needs, is greatly influenced by the real behaviour of its participants. Investor responsibility is key in our free market-based financial system. It is important that losses remain an inevitable part of this market system. ASIC will not, and cannot, be expected to prevent all consumer losses. In addition, it is important that gatekeepers take responsibility for their actions. Recently I have talked a lot about the culture of our gatekeepers. The culture of a firm can positively or negatively influence behaviour. Poor culture – such as one that is focused only on short-term gains and profit – often drives poor conduct. Conversely, good culture will drive good conduct. I see a good culture as one that puts the customer’s long term interests first.

So the FSI recommendation – that a broad, principles-based obligation be placed on financial institutions to have regard to the needs of their customers in designing and targeting their products – is a recommendation that puts the interests of the customer at its centre. In my view, the FSI’s recommendation aligns very closely with the theme of culture. Product manufacturers should design and distribute products with the best interests of the investor or financial consumer in mind. This is part of having a customer-focused culture.

In fact, the FSI has noted that the kinds of practices required by a design and distribution obligation would already be in place in many institutions that already invest in customer-focused business practices. Firms that already have a customer-focused culture would not need to significantly change their practices.

Penalties

Finally I would like to turn to the recommendation on penalties. The FSI recommended that penalties for contravening ASIC legislation should be substantially increased, and that ASIC should be able to see disgorgement of profits obtained as a result of misconduct. Comparatively, the maximum civil penalties available to us in Australia are lower than those available to other regulators internationally. And they are fixed amounts, not multiples of the financial benefit obtained from misconduct.

In order to regulate for the real behaviour of gatekeepers in the system, penalties need to be set at an appropriate level. And we need a range of penalties available, to act as a deterrent to misconduct. Penalties set at an appropriate level are critical in the ‘fear versus greed’ calculation of the potential wrongdoer. Penalties need to give market participants the right incentive to comply with the law. They should aim to deter contraventions and promote greater compliance, resulting in a more resilient financial system.

An official review of lending standards in the red-hot investor property market is set to reveal serious flaws in how lenders have been assessing customers for credit.

The chairman of the Australian Securities and Investments Commission, Greg Medcraft, on Thursday said the watchdog would in August publish a report finding shortcomings among how some lenders were testing borrowers’ ability to cope with higher interest rates.

The report, based on surveillance of 11 banks and non-banks, had also found some lenders’ credit checks used inadequate estimates of customers’ living expenses, he said.

Even though banks are offering new borrowers interest rates of about 4.5 per cent, Mr Medcraft lenders and customers needed to assess whether borrowers could cope with interest rates of 7 per cent.

“That’s what you should be thinking about if you’re looking at your ability to repay the loan,” he said.

But adding to similar concerns raised by the prudential regulator in recent months, Mr Medcraft said the report had made “mixed” findings on whether banks were using a high enough “stress rate.”

He added that some of the underwriting standards had been improved in recent months. “Many of them have since corrected their ways or are correcting them.”

Mr Medcraft also highlighted some borrowers failing to rigorously assess a borrowers’ cost of living, including national indexes that did not reflect local variations.

Following an independent review, NAB has refunded customers who were impacted by errors dating back to 2001 and are centered on processes and controls relating to Navigator – a platform NAB inherited from the Aviva acquisition in 2009.

ASIC said National Australia Bank’s wealth management business (NAB Wealth) has announced the resolution of its compensation program due to issues with its Navigator Wrap platform, with $25 million in compensation to be paid to approximately 62,000 customers. The issues relate to tax estimation and income estimation errors on its Navigator Wrap platform.

Following ASIC’s request, NAB Wealth appointed PriceWaterhouse Coopers to independently review the payout process, systems integrity and breach reporting and governance.

Commissioner Greg Tanzer said, ‘ASIC expects banks to vigilantly monitor their platforms for issues such as this. Any issues identified should be swiftly and pro-actively reported to ASIC, with a view to promptly compensating customers.’

ASIC acknowledged NAB Wealth’s cooperation in this matter.

In NABs statement, they said as part of this review, NAB has identified errors and processes dating back to 2001, which was prior to NAB’s 2009 acquisition of Aviva, which included the Navigator platform, and when Aviva was eventually integrated into the NAB business in 2011.

These errors and processes relate to how income and tax was being allocated to customers’ accounts on closure. This resulted in surplus monies being held within the Navigator Platform Funds for the benefit of fund customers, rather than being attributed at the individual customer account level. At no stage have these monies been held by, or accounted for, as part of the assets of any NAB Group company.

The review undertaken by NAB over the past 12 months has now resolved this, with all affected customers to be paid their due allocations. In total, approximately 62,000 customers will receive funds to the value of approximately $25 million.

One-third (34%) of customers will receive a payment of $50 or less, 50% of customers will receive less than $100, and 75% of customers will receive less than $350. The average payment per customer is $400, which includes interest.

Group Executive, NAB Wealth and CEO of MLC, Andrew Hagger said that NAB will write to customers and advisers over the coming weeks to explain this legacy issue and what NAB has done to fix the problem.

“NAB Wealth has applied significant focus to our breach identification and reporting processes, which is what led to NAB originally reporting this legacy issue to ASIC,” Mr Hagger said.

“These errors date back to 2001 and are centred on processes and controls relating to Navigator – a platform NAB inherited when we acquired Aviva in 2009. Our teams have worked extensively, with oversight by PwC and ASIC, to ensure the right processes, systems and controls are now in place.

“While this is a legacy issue, we took deliberate steps to make absolutely sure we could get the fairest outcome for our customers.

“These errors are in no way related to the quality of NAB Wealth’s advice to its customers.”

The only customers impacted are customers who closed their accounts on the Navigator platform between 30 September 2001 and 30 April 2015. The majority of money now being distributed to customers is being distributed from within the Navigator Platform Funds to the entitled customers. Given that the majority of the $25 million is being reallocated from the Navigator Platform Funds, this payment is immaterial to NAB.