ASIC has commenced proceedings in the Federal Court of Australia against the Bank of Queensland concerning unfair contract terms in small business contracts.

ASIC alleges that certain terms used by Bank of Queensland in

contracts with small businesses are unfair. If the Court agrees with

ASIC, the specific terms will be void and unenforceable by the Bank of

Queensland in these contracts.

ASIC alleges that certain terms used by the Bank of Queensland are unfair, as the terms:

cause a significant imbalance in the parties’ rights and obligations under the contract;

were not reasonably necessary to protect the Bank of Queensland’s legitimate interests; and

would cause detriment to the small businesses if the terms were relied on.

Some of the unfair terms pleaded by ASIC include clauses that give

lenders, but not borrowers, broad discretion to vary the terms and

conditions of the contract without the consent of the small business

owner, along with clauses that allow the bank to call a default, even if

the small business owner has met all of its financial obligations.

ASIC is also seeking a declaration from the Federal Court that the

same terms in any other small business contract are also unfair.

Background

If the Federal Court finds that any of the terms of the standard form

contracts are unfair, the unfair terms are void (it is as if the terms

never existed in the contracts). ASIC is seeking that the terms are

declared void from the outset – not from the time of the court’s

declaration. The remainder of the contract will continue to bind parties

if it can operate without the unfair terms.

Since 1 July 2010, ASIC has administered the law to deal with unfair

terms in standard form consumer contracts for financial products and

services, including loans.

With effect from 12 November 2016, the unfair contract terms

provisions applying to consumers under the Australian Consumer Law and

the ASIC Act were extended to cover standard form ‘small business’

contracts.

Small businesses, like consumers, are often offered contracts for

financial products and services on a ‘take it or leave it’ basis,

commonly entering into contracts where they have limited or no

opportunity to negotiate the terms. These are known as ‘standard form’

contracts. Small businesses commonly enter into these ‘standard form’

contracts for financial products and services, including business loans,

credit cards, and overdraft arrangements.

The unfair contracts law applies to standard form small business

contracts entered into, or renewed, on or after 12 November 2016 where:

the contract is for the supply of financial goods or services (which includes a loan contract);

at least one of the parties is a ‘small business’ (under the ASIC

Act, a business employing fewer than 20 people is a ‘small business’);

and

the upfront price payable under the contract does not exceed $300,000, or $1 million if the contract is for more than 12 months.

ASIC says Suncorp Life and Superannuation Limited (Suncorp) has recently completed a remediation program, which impacted over 4,000 clients of Suncorp-owned GuardianFP Limited (Guardian Advice).

Suncorp paid $1,431,167 in compensation to Guardian Advice clients who had received poor advice.

Suncorp undertook the remediation program after ASIC imposed

additional licence conditions on the Australian financial services (AFS)

license of Guardian Advice because a surveillance uncovered

deficiencies in the life insurance advice provided by Guardian Advice to

retail clients (15-003MR).

ASIC was concerned that Guardian Advice had failed to comply with its

general obligations as an AFS licensee, including monitoring and

supervising its representatives and ensuring they were adequately

trained or competent. A number of clients suffered harm a result of

these failures.

When Suncorp announced that it would exit the financial planning

business carried on by Guardian Advice in November 2015, ASIC obtained a

commitment from Suncorp that it would complete the remediation program

provided for in the additional licence conditions and fund the

compensation of Guardian Advice clients (15-353MR).

Additionally, Suncorp undertook to compensate clients who may have

been at risk of having received poor advice from ‘high-risk’ advisers,

who were identified using a range of risk metrics applied to all

advisers in the Guardian Advice network. Affected clients were also

compensated under this remediation program.

Suncorp’s remediation program was overseen by independent experts.

Australian

consumers are paying too much for foreign currency conversion (FX)

services because of confusing pricing and a lack of robust competition, a

new ACCC report has found.

The final report of the ACCC’s Foreign Currency Conversion Services Inquiry

highlights important competition and consumer issues affecting

individuals and small businesses who use international money transfers

(IMTs), foreign cash, travel cards, and credit cards or debit cards for

transactions in foreign currencies.

The ACCC found that it can be challenging for consumers to shop

around and make informed decisions about FX services. As a result, many

consumers continue to use the big four banks for FX services despite the

availability of much cheaper alternatives.

It is difficult for consumers to compare prices because some

suppliers do not disclose their total price up front. In addition,

consumers pay unexpected fees for some services. Finally, complex prices

can deter consumers from shopping around because of the time and effort

required to do so.

During 2017-18, individual consumers who used the big four banks to

send IMTs in US dollars and British pounds could have collectively saved

about AUD150 million if they had instead used a lower priced IMT

supplier.

“Shopping around could save Australian consumers hundreds of millions of dollars each year,” ACCC Chair Rod Sims said.

“Consumers and small businesses tend to default to their usual bank

to send money overseas, but this may not be the cheapest option. This is

another example where consumers may end up paying more for their

loyalty.”

Guidance for consumers using FX services

The ACCC has released a guide to

help consumers shop around. For example, the guide gives tips on

sending money overseas and avoiding fees when making overseas purchases

online.

“The guide will help consumers to shop around, carefully select where

and how they pay for their purchases and to identify fees so they can

get the best deal,” Mr Sims said.

“For example, the guide explains how foreign exchange services with low or no fees are not always the best value for money.”

“We have also tried to clear up a few misconceptions, such as the

assumption that paying in Australian dollars when shopping overseas is

always best, when that is not the case.”

The final report warns that travellers can pay a high price for

leaving their purchase of foreign cash to the last minute and buying at

the airport.

Consumers should also consider whether their existing credit or debit

card may be cheaper than using foreign cash or a travel money card for

overseas purchases. Some credit and debit providers offer cards with no

international transaction fees which can be a much cheaper option than

many other products.

Consumers should be aware that some commercial comparison sites may

not be independent and that suppliers may pay for their services to be

promoted by these sites. There are, however, two government-funded

comparison websites for international money transfers (IMTs): www.sendmoneypacific.org and www.saverasia.com, which compare prices of IMT services available to a number of South-East Asian and Pacific Island countries.

Savings to be made

The ACCC inquiry found:

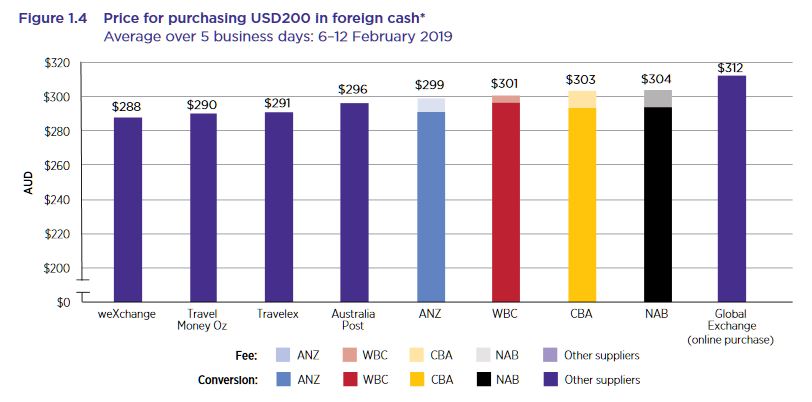

Foreign cash is more expensive at airport locations than at other

locations. When buying USD200 in February 2019, consumers could have

saved AUD40 by purchasing from the cheapest supplier at a non-airport

location, compared with the most expensive supplier at the airport.

Consumers and small businesses who used the most expensive bank to

transfer USD7000 would have paid more than AUD500 more than if they had

used the cheapest supplier.

If customers of the big four banks used a debit or credit card

without international transaction fees instead of a travel money card,

they could save up to AUD13 on a USD200 purchase.

Customers of the big four banks could save up to AUD5 on a USD200

purchase if they used a ‘regular’ debit or credit card instead of a

travel money card.

Guidance for businesses

The report includes best practice guidance for businesses supplying

FX services. It explains how they should disclose prices to consumers.

The guidance focuses on ensuring that businesses clearly disclose the

full price of an FX service to consumers upfront.

“We consider businesses who ignore this best practice guidance may be

at risk of breaching the Australian Consumer Law,” Mr Sims said.

“The ACCC will take action against businesses who do not make appropriate disclosures to consumers.”

New entrants providing lower prices, more advanced services

The ACCC has found that recent competition from newer entrants is

delivering better outcomes for consumers making use of IMTs, including

through lower prices and more advanced services.

These new entrants often rely on obtaining services from banks, their

vertically integrated competitors, to provide IMTs to their customers.

However, the inquiry found that some non-bank IMT suppliers had been

denied access to bank services, such as bank accounts.

“Banks need to comply with Australia’s anti-money laundering and

counter terrorism financing laws, and this is one reason banks have

given for withdrawing banking services to IMT providers,” Mr Sims said.

“The withdrawal of banking services from non-bank IMT suppliers

represents a significant threat to competition that could ultimately

result in less choice and higher prices for consumers.”

To address this issue, the ACCC recommends development of a scheme to

facilitate continued and efficient access to banking services by

non-bank IMT suppliers. This would include addressing the due diligence

requirements of the banks, including in relation to anti-money

laundering and counterterrorism financing requirements.

This scheme should be operational by the end of 2020.

Background

The inquiry was preceded by:

findings by the World Bank

in June 2018 that the cost of sending money overseas from Australia was

approximately 11 per cent higher than the G20 average, 13 per cent

higher than the UK and almost 40 per cent higher than the US

the Productivity Commission’s Report on Competition in the Australian Financial System

which recommended that the ACCC, in consultation with ASIC, investigate

what additional disclosure methods could be used to improve consumer

understanding and comparison of fees for foreign transactions.

On 2 October 2018,

the Treasurer approved the ACCC holding an inquiry into the supply of

FX services in Australia. On the same day, the ACCC released an issues

paper for the inquiry. In response, the ACCC received 63 written

submissions from a mix of consumers, FX services suppliers, small

businesses and other stakeholders.

The final report focuses its competition analysis primarily on IMTs. IMTs are significant for a number of reasons including:

prices in Australia are high by global standards and IMTs are a

significant outlay for Australians with an estimated AUD21 billion in

personal IMTs sent from Australia each year

IMTs are regularly used by groups of potentially vulnerable and disadvantaged consumers such as migrants and temporary workers

the average transaction size for IMTs is much larger than the other services considered in the inquiry.

The inquiry is the second inquiry undertaken by the ACCC’s Financial

Services Competition Branch (FSCB). The FSCB proactively monitors and

promotes competition in Australia’s financial services sector by

assessing competition issues and undertaking market studies.

But, the Reserve Bank of Australia has pointed to Australia’s high debt levels as a factor in its decision making for the cash rate, fearing that it will make the economy more vulnerable to shocks.

Just remember this in the context of APRA reducing the lending standards recently! And in APRA’s Corporate plan Australia’s banking watchdog will stress test the country’s banks every year, instead of the current three-year cycle, ramping up oversight of a sector that has been marred by misconduct.

In the most recent series of stress tests in 2017, all 13 of the country’s largest banks passed the “severe but plausible” scenarios applied by the regulator, despite projected losses of about A$40 billion in home loans alone.

The RBA published its four-year corporate plan on Friday, pointing to the banks’ exposure to housing loans and cyber security in financial institutions as the largest risks to the country’s financial stability.

In Australia, wages growth is low, reflecting spare capacity in the labour market as well as some structural factors.

The

central bank expects the unemployment rate will remain around 5.25 per

cent for a time, before declining to around 5 per cent in 2021, with

wages growth expected to remain stable and then increase modestly from

2020.

Consumer price inflation is forecast to increase to be a

little under 2 per cent over 2020 and a little above 2 per cent over

2021.

The

RBA noted over the next four years, “movements in asset values and

leverage may be more important for economic developments than in the

past given the already high levels of debt on household balance sheets.

“Especially

in the context of weak growth in household income, high debt levels

could complicate future monetary policy decisions by making the economy

less resilient to shocks,” the RBA said.

The central bank noted

policymakers in the US and other countries employing quantitative easing

as a result of intensifying trade and technology disputes.

Globally,

the RBA reported, labour market conditions remain tight in major

advanced economies, although unemployment rates are at multidecade lows.

“Global

interest rates and measures of financial market volatility both remain

low compared with historical experience,” the RBA said in its corporate

plan.

“The future path of global monetary policy and financial

conditions more generally remain subject to substantial uncertainty.

These global factors significantly influence the environment in which

monetary policy in Australia is conducted,” the RBA said.

Last

week, RBA governor Philip Lowe reflected on the RBA’s decision on the

cash rate during an address to Jackson Hole Symposium in Wyoming.

“So

the question the Reserve Bank Board often asks itself in making its

interest rate decision is how our decision can best contribute to the

welfare of the Australian people,” Mr Lowe said.

“Keeping

inflation close to target is part of the answer, but it is not the full

answer. Given the uncertainties we face, it is appropriate that we have a

degree of flexibility, but when we use this flexibility we need to

explain why we are doing so and how our decisions are consistent with

our mandate.”

He said a challenge the central bank is facing is elevated expectations that monetary policy can deliver economic prosperity.

“The

reality is more complicated than this, not least because weak growth in

output and incomes is largely reflecting structural factors,” Mr Lowe

commented.

“Another element of the reality we face is that

monetary policy is just one of the levers that are potentially available

for managing the economy. And, arguably, given the challenges we face

at the moment, it is not the best lever.”

The RBA is due to deliver its cash rate decision tomorrow.

ASIC says that Allianz Australia Insurance Limited (Allianz) will refund over $8 million in consumer credit insurance (CCI) premiums and fees including interest to more than 15,000 consumers.

This follows ASIC’s review of the sale of CCI by lenders in Report 622 Consumer credit insurance: Poor value products and harmful sales practices (REP 622), and forms part of ASIC’s broader priority to address harms and unfair practices impacting consumers in insurance.

Allianz’s refund relates to the sale of cover to

consumers who were ineligible to make a claim for unemployment or

disability, the sale of death cover to customers under 21 years of age

who were unlikely to need that cover, and the charging of fees to

customers who paid premiums by the month without adequate disclosure.

The remediation program covers certain CCI products

issued by Allianz including mortgage and loan protection policies sold

through financial institutions. These CCI products provided cover

against the risk of consumers being unable to meet loan commitments

because of death, injury, illness or involuntary unemployment.

To address these issues, Allianz will,

for ineligible sales of unemployment and disability cover,

refund premiums charged plus interest for active, cancelled or lapsed policies sold between 1 January 2011 to 31 December 2018;

reassess all withdrawn and declined claims where the consumer was ineligible for the policy at the time of sale;

invite consumers to submit a claim if they have not already done so and pay valid claims plus interest; and

continue to honour active policies and not rely on employment eligibility criteria as a basis to decline an unemployment or disability claim;

for sales of death cover to customers under 21 years of age,

refund all premiums charged plus interest for active, cancelled or lapsed policies sold between 1 January 2011 to 31 December 2018; and

preserve existing death cover for active policyholders on current terms without charging for it;

for monthly policy payment customers,

refund all administration fees and loading charged plus interest; and

correct any future direct debit amounts.

ASIC Commissioner Sean Hughes said, ‘Disappointingly,

our work on the sale of CCI has highlighted widespread mis-selling and

poor product design. This remediation outcome is only one of many

examples where CCI has failed consumers. We expect insurers to cease to

sell insurance products that provide little or no value.’

‘We need a financial system that is fair. Insurers and

other financial institutions need to rise to the challenge and embed the

principle of fairness into their businesses to ensure we do not see any

further instances of this kind of poor value product being pushed on to

consumers’ added Mr Hughes.

Allianz will stop issuing new CCI policies from 30

September 2019. It will continue to fulfil its obligations to existing

CCI policyholders.

Allianz is expected to write to all affected consumers

about their refund offer from October 2019. Consumers with questions

about their cover should contact Allianz by email at here_to_help@allianz.com.au.

Background

ASIC’s recent review of the sale of CCI has resulted in

refunds of over $100 million due to more than 300,000 affected

consumers. On 11 July 2019, we released Report 622 Consumer credit insurance: Poor value products and harmful sales practices (REP 622) detailing our findings and setting minimum standards for lenders and insurers who issue or sell CCI (19-180MR).

ASIC is currently consulting on a proposal to ban the

sale of CCI and direct life insurance through unsolicited telephone

calls (19-188MR).

The proposed ban aims to address unfair sales conduct and protect

consumers from being sold products that they do not need, want or

understand.

ASIC has also commenced investigations into a number of entities that have been involved in mis-selling CCI to consumers.

Separately, in 2018, Allianz refunded $45.6 million to

68,000 consumers for add-on insurance sold through car dealerships that

were of little or no value (18-008MR).

Interesting speech from Wayne Byers “Reflections on a changing landscape“. He discussed the ” extraordinary intervention” to save our banks a decade ago (in a footnote), significant in my view, for what it said, and for what it missed out. There is no mention that both NAB and Westpac required bailing out by the FED’s TAF after the GFC. An important little fact?

APRA’s activities have expanded significantly over the past five years. This has not been a smooth transition: the regulatory pendulum has swung between periods of significant regulatory change, and times when there have been demands to pare back. But overall there is no doubt that expectations of APRA have grown, and they have pushed us into new fields of endeavour. There is no sign that tide is going to turn soon.

I’m not sure what the issues de jour will be in five years’ time but there’s a very good chance they will not be the issues we think are most important today. The past five years has shown that what might seem unusual or out of scope today, can quickly become a core task tomorrow. Some of the topics that I have talked about tonight were not seen, five years ago, to be at the heart of APRA’s role.

In contrast, later this week we will publish our 4 year Corporate Plan and a number of them will be called out as our core outcomes, ranking alongside maintaining financial safety and resilience.

If there is one lesson from the past five years, it is that – be it regulators or risk managers – being ready and able to respond to the demands of a rapidly changing landscape is probably the most important attribute we all need to possess.

But the footnote was the most interesting in my view. For what it said, and for what it missed out.

It is sometimes said the Australian banking system ‘sailed through’ the financial crisis. While the system did prove relatively resilient, there was extraordinary intervention necessary to keep the system stable and the wheels of the economy turning.

That included (i) an unprecedented fiscal response – one of the largest stimulus packages in the world;

(ii) an unprecedented monetary response – the official cash rate was cut by 425 basis points in a little over six months;

(iii) the RBA substantially expanded its market operations and balance sheet;

(iv) ASIC imposed an 8-month ban on the short selling of financial stocks; and

(v) the Federal Government initiated a guarantee of retail deposits of up to $1 million, and a facility for authorised deposit-taking institutions (ADIs) to purchase guarantees for larger deposits and wholesale funding out to 5 years (indeed, at one point more than one-third of the banking system’s entire liabilities were subject to a Commonwealth Government guarantee).

As I have said previously, if all of the above was needed to keep the system stable and operational, then it is difficult to argue that the system sailed through or that some further strengthening of regulation was not justified.

He failed to mention the massive bail-out of our banking system from the FED and the fact that it was China’s response which supported our economy. The evidence suggests we were much closer to the abyss than was acknowledged at the time. Westpac and NAB both required support from the FED, as revealed in papers from the FED.

The US Dodd-Frank Act requires the US Federal Reserve to reveal which institutions it loaned money to under the various bail out programmes.

“Under the program, the Federal Reserve auctioned 28-day loans, and, beginning in August 2008, 84-day loans, to depository institutions in generally sound financial condition… Of those institutions, primary credit, and thus also the TAF, is available only to institutions that are financially sound.

Now of course the question is what does “financially sound” institutions mean. Well, look at the entire list – its long, but some of the names will be familiar. The FED data shows more than 4,200 separate transactions across more than 400 institutions globally between 2008 and 2010.

UK based Lloyds TSB plc received USD$10.5 billion – and was later partially nationalised by the UK government.

And another UK Bank, the Royal Bank of Scotland (RBS) got US$53.5 billion plus and additionally US$1.5 billion for its exposures via ABN Amro after RBS bought it. That was nationalised too.

In Ireland, Allied Irish Bank needed US$34.7 billion of loans from the Fed between February 2009 and February 2010 . This is the bank bailed out via the Irish taxpayer.

And Deutsche Bank needed a massive US$76.8 billion in loans in total (and that bank continues to struggle today).

The list goes on. Bayerische Landesbank required a US$13.4 billion bailout from the state of Bavaria, but also borrowed US$108.19 billion between December 2007 and October 2009.

Where these banks sound?

And our own “financially sound” institutions National Australia Bank and Westpac needed help from the Fed. NAB needed around $7 billion in total (allowing for the exchange rate).

In fact NAB raised $3 billion from shareholders in 2008 to add capital to its business in parallel.

And in January 2008 Westpac said everything was fine with its US exposures, just one month after they got their first bail-out from the FED, worth US$90 million.

In fact, there was a long queue then, as the Fed spreadsheet shows that alongside Westpac, was Citibank, Lloyds TSB Bank, Bayerische Landesbank and Societe Generale, all of whom where bailed out by Governments in their respective countries.

Now, the RBA wrote at the time:

“The Australian financial system has coped better with the recent turmoil than many other financial systems. The banking system is soundly capitalised, it has only limited exposure to sub-prime related assets, and it continues to record strong profitability and has low levels or problem loans. The large Australian banks all have high credit ratings and they have been able to continue to tap both domestic and offshore capital markets on a regular basis.”

So the question is did APRA and the RBA know what was going on?

And my question more generally is how prepared are we for a similar crisis now – given the changed economic and geopolitical forces in play?

The Australian Financial Complaints

Authority will begin naming financial firms in its published determinations to

increase transparency in the financial sector and enhance consumer confidence.

The change comes following the

Royal Commission into Misconduct in the Banking, Superannuation and Financial

Services Industry.

AFCA undertook a public

consultation and submitted an application to the Australian Securities and

Investments Commission (ASIC) to change the AFCA Rules.

AFCA Chief Ombudsman and CEO David

Locke said AFCA is committed to being open, transparent and accountable to the

public.

“AFCA plays an important public

role and we recognise that transparency in our data and decisions is essential

to rebuilding trust in the financial sector,” Mr Locke said.

“We already publish decisions on

our website, but we have been unable to name the financial firms

involved.

“We welcome ASIC’s approval to

change our Rules, which will allow us to now name financial firms in decisions

we publish on our website.

“This is an important change, and

the public will now be able to access increased information about the actions

of financial firms.”

AFCA is working with ASIC to determine the start date for the naming of financial firms. Further updates will be provided when available.

ASIC has approved changes to the Australian Financial Complaints

Authority (AFCA) Rules to allow the scheme to name financial firms in

published determinations.

In its first six months, AFCA received 35,263 complaints. About 4,500

to 5,000 complaints are currently expected to be finalised each year by

way of determination. While the publication of determinations has been a

longstanding feature of the external dispute resolution schemes in

Australia, the names of firms involved in financial services,

superannuation and credit complaints have not been published to date.

AFCA applied for approval to change their Rules to enable

identification of firms following public consultation. Consumers who are

party to a complaint will continue to be anonymised in all

determinations.

In approving this change ASIC took into account stakeholder feedback

to AFCA’s public consultation and the statutory approval criteria.

ASIC’s view is that naming firms in determinations can help identify

conduct or market problems within firms or affecting specific products

or services, as well as highlighting where firms have done the right

thing. It will also enhance transparency and accountability of firms’

performance in complaints handling and of AFCA’s own decision-making.

To support the new Rules, AFCA will shortly be issuing updated

operational guidelines which set out examples of the circumstances in

which a determination naming a financial firm would not be published.

This includes where naming may expose confidential information about a

firm’s systems or policies.

Naming firms in AFCA determinations is part of a broader set of

reforms aimed at increasing transparency in financial services. This

includes Parliament giving ASIC power to collect and to publish internal

dispute resolution (IDR) data at firm level. The UK Financial

Ombudsman Service has been naming firms in published determinations

since 2013

Mark Carney, Bank of England Governor has given a given a significant speech at the Jackson Hole symposium in which he outlines some potential steps to a new global currency. He argues that just as Sterling transitioned to the US Dollar in the 1930s’s, something similar could occur again. But rather than having a battle of competing reserve currencies, perhaps an alternative path is possible via a Synthetic Hegemonic Currency (SHC). This might be based on a network of central bank digital currencies, rather than something like Libra.

This folks is a big deal – when aligned with the reduction in cash, the migration to digital currencies, and globalisation. The potential implications are immense!

Technology has the potential to disrupt the network externalities that prevent the incumbent global reserve currency from being displaced.

Retail transactions are taking place increasingly online rather than on the high street, and through electronic payments over cash. And the relatively high costs of domestic and cross border electronic payments are encouraging innovation, with new entrants applying new technologies to offer lower cost, more convenient retail payment services.

The most high profile of these has been Libra – a new payments infrastructure based on an international stablecoin fully backed by reserve assets in a basket of currencies including the US dollar, the euro, and sterling. It could be exchanged between users on messaging platforms and with participating retailers.

There are a host of fundamental issues that Libra must address, ranging from privacy to AML/CFT and operational resilience. In addition, depending on its design, it could have substantial implications for both monetary and financial stability.

The Bank of England and other regulators have been clear that unlike in social media, for which standards and regulations are only now being developed after the technologies have been adopted by billions of users, the terms of engagement for any new systemic private payments system must be in force well in advance of any launch.

As a consequence, it is an open question whether such a new Synthetic Hegemonic Currency (SHC) would be best provided by the public sector, perhaps through a network of central bank digital currencies.

Even if the initial variants of the idea prove wanting, the concept is intriguing. It is worth considering how an SHC in the IMFS could support better global outcomes, given the scale of the challenges of the current IMFS and the risks in transition to a new hegemonic reserve currency like the Renminbi.

An SHC could dampen the domineering influence of the US dollar on global trade. If the share of trade invoiced in SHC were to rise, shocks in the US would have less potent spillovers through exchange rates, and trade would become less synchronised across countries.

By the same token, global trade would become more sensitive to changes in conditions in the countries of the other currencies in the basket backing the SHC.

The dollar’s influence on global financial conditions could similarly decline if a financial architecture developed around the new SHC and it displaced the dollar’s dominance in credit markets. By reducing the influence of the US on the global financial cycle, this would help reduce the volatility of capital flows to EMEs.

Widespread use of the SHC in international trade and finance would imply that the currencies that compose its basket could gradually be seen as reliable reserve assets, encouraging EMEs to diversify their holdings of safe assets away from the dollar. This would lessen the downward pressure on equilibrium interest rates and help alleviate the global liquidity trap.

Commonwealth Bank of Australia (CBA) has announced that it has entered into further agreements to progress the planned divestment of its Australian life insurance business (CommInsure Life) to AIA Group Limited (AIA).

The planned

divestment has been subject to ongoing regulatory approval processes,

which has led to an extended period of uncertainty for CommInsure Life.

The revised transaction path comprises a joint co-operation

agreement, reinsurance arrangements, partnership milestone payments and a

statutory asset transfer. The aggregate proceeds for CBA from the

transaction are expected to be $2,375m,[1] a reduction of $150m from the

original sale price. These arrangements are expected to be implemented

in a staged manner throughout FY20, with CBA to receive approximately

$750 million of proceeds and distributions by the end of 1H FY20 and the

remaining $1,625 million by the end of FY20.

CBA and ASB have also agreed to grant AIA an option to extend the

respective Australian and New Zealand distribution agreements from 20

years to 25 years.

CBA Chief Executive Officer Matt Comyn said: “Today’s announcement

provides CommInsure Life’s policyholders and staff with more clarity

about the future of the business and progresses the simplification of

CBA’s portfolio of businesses.

“We are excited by the opportunity to bring together the strengths of

AIA and CommInsure Life and are working hard with our partner to

develop a new generation of products for CBA’s customers, which will

deliver excellent customer outcomes”.

The revised transaction path is subject to a number of Australian

regulatory approvals, the entry into reinsurance arrangements and life

insurance entity board approvals.

Details of the revised transaction path

The revised transaction path comprises the following key components:

Joint co-operation agreement

CBA and AIA will enter into a joint co-operation agreement, which

once implemented, will result in the full economic interests associated

with CommInsure Life (excluding in relation to the Group’s 37.5% equity

interest in BoCommLife Insurance Company Limited (BoCommLife))

being transferred to AIA and AIA obtaining an appropriate level of

direct management and oversight of the business. AIA Australia & New

Zealand CEO Damien Mu will lead CommInsure Life under these

arrangements.

Implementation of the joint co-operation agreement is expected before the end of 1H FY20 (Implementation Date), at which time CBA will receive an upfront payment of $500 million.

Reinsurance

Colonial Mutual Life Assurance Society Limited (CMLA), the

key life insurance entity of CommInsure Life, intends to enter into a

reinsurance arrangement with a leading global reinsurer.

The reinsurance arrangement would come into effect on the

Implementation Date and is expected to result in CBA receiving a

distribution from CMLA of approximately $200 million shortly following

the Implementation Date.

Partnership milestones

CBA will receive four partnership milestone payments of $50 million

each ($200 million in aggregate), to reflect the progress in the

partnership, with the first payment expected to be received in late 1H

FY20.

Completion

In parallel with the planned share sale of CommInsure Life (which

remains subject to a foreign regulatory approval process), CBA and AIA

are progressing a potential statutory asset transfer as an alternative

approach to completing the divestment of the business. If implemented,

the statutory asset transfer would be expected to take approximately 9

months to implement.

Upon completion, whether achieved through a share sale or statutory

asset transfer, CBA will receive a final payment from AIA of

approximately $1,475 million (subject to completion adjustments).

Financial impacts

Upon completion, which is expected to occur by the end of FY20, the

revised transaction path is expected to have released approximately $1.6

billion – $1.8 billion of Common Equity Tier 1 (CET1) capital,

resulting in a pro forma increase to the Group’s CET1 ratio of

approximately 35 – 40 basis points on an APRA basis as at 30 June 2019.

Sale of equity interest in BoCommLife

CBA remains committed to completing the sale of the Group’s 37.5%

equity interest in BoCommLife to MS&AD Insurance Group Holdings.

Completion of the sale of the BoCommLife equity interest remains subject

to regulatory approval from the China Banking and Insurance Regulatory

Commission (CBIRC) and CBA is working constructively with CBIRC

in relation to the process. For the avoidance of doubt, the revised

transaction path in relation to CommInsure Life does not impact this

sale process and CBA will continue to exercise full control over the

BoCommLife equity interest until its sale has been completed.