After successfully leading Westpac’s consumer bank, BOQ’s new boss George Frazis has landed a big job at a much smaller bank with a shrinking mortgage book, via InvestorDaily.

In

April, Bank of Queensland reported reporting negative mortgage growth

of $248 million, down from positive growth of $11 million in 1H18, with

its portfolio dropping to $24.7 billion.

The fall was driven by a

$717 million contraction in settlements through BOQ’s retail bank,

offset by a $469 million rise in home loan volumes through its

subsidiary, Virgin Money Home Loans.

The regional lender is well

aware of the challenges within its retail bank, which is effectively

franchised with branches being run by ‘owner-managers’. Given the

negative press generated by the royal commission, attracting new owner

managers has been difficult for BOQ.

Prior to the appointment of

George Frazis as CEO on 6 June, interim chief executive Anthony Rose

delivered an 8 per cent drop in cash earnings in the first half of

FY19.

“Across

the industry, as you are well aware, there have been significant

changes in the banking landscape which has created revenue headwinds for

the sector. In addition, the outcome from the royal commission is

lifting expectations of the regulators. Adjusting to the new regulatory

environment will come with a higher cost profile, absent any mitigating

actions which we are of course exploring,” Mr Rose said in April.

“BOQ

also has challenges that are specific to our business, particularly in

the retail bank. Our digital customer offering, lending processes and

the inability to attract new owner-managers with the overlay of

regulatory uncertainty, has hampered customer acquisition and returns.”

Mr

Rose, BOQ’s chief operating officer, will remain as interim CEO until

Mr Frazis takes over in September. Rose took charge following the

resignation of John Sutton in December 2018.

Morningstar analyst

David Ellis praised the appointment of Mr Frazis, an experienced banker

with 17 years in the industry, most recently as CEO of Westpac’s

consumer bank and CEO at St George Bank.

“While Frazis has strong

credentials and deeply understands the dynamics of Australia’s consumer

banking industry, he will be taking control of a regional player with a

small geographic distribution footprint, higher funding and operational

costs, a lower credit rating and tougher regulatory capital burden,” Mr

Ellis said.

The Morningstar analyst believes the challenge for

Mr Frazis is to assume a bigger role in a smaller organisation that

lacks market share, brand awareness, distribution capabilities and

funding advantages that major banks enjoy.

“Bank of Queensland’s

lending growth has been subdued for several years,” Mr Ellis said.

“Based on APRA banking statistics for April 2019, the bank’s 12-month

growth in home loans sit at just 0.3 per cent in April, compared to 1.7

per cent a year ago and 11.8 per cent three years prior.”

Bank system home loan growth is 3.3 per cent for the year to April 2019.

With

the RBA cutting rates this month, BOQ has lowered its fixed rates in an

effort to remain competitive in a mortgage market dominated by the big

four. However, with more cash rate cuts expected, Morningstar is

concerned whether BOQ can sustain its course of passing on the

reductions.

“The bank lacks access to lower-cost funding options

and has a much lower return on equity than the major banks,” Mr Ellis

said.

Under Mr Frazis’ leadership, Westpac’s consumer bank

attracted more than a million new customers in the past four years.

Digital channels now account for a third of sales.

“Frazis will have to do the same at Bank of Queensland,” Mr Ellis said

I discuss the latest attempt to deal with deposit bail-in with Robbie Barwick from the CEC, who have just launched a new petition seeking to exclude bank deposits.

The Reserve Bank of New Zealand has released an important statement on the new approach they are going to adopt in policy setting. The focus will be on improving wellbeing. In addition they are expanding their dna to avoid group think. This follows their recent moves to lift bank capital.

There is so much here the RBA should embrace.

The Reserve Bank has significantly changed the way it makes monetary policy decisions, keeping itself in step with public expectations.

In a panel discussion last week at the Institute for Monetary and Economic Studies (Bank of Japan) in Tokyo, Reserve Bank Assistant Governor and General Manager of Economics, Financial Markets and Banking Christian Hawkesby talked about the importance of good decision making and governance, and of being credible and trusted, in achieving the long-term goal of improving wellbeing.

“We maintain our legitimacy as an institution by serving the public interest and fulfilling our social obligations. Keeping our ‘social licence’ to operate depends on maintaining the public’s trust that we are improving wellbeing,” Mr Hawkesby said.

“Thirty years ago New Zealand was prepared to accept a single expert – the Governor – making decisions about how to fight inflation. People now expect to see how and why decisions are made, expect that decision makers reflect wider society, and that current issues and concerns are factored into the decision making. By meeting these expectations, we can improve public trust in the legitimacy of the Reserve Bank’s work,” he said.

Mr Hawkesby outlined the new committee process that the Reserve Bank uses for deciding the official cash rate, noting that diversity among decision makers improves the pool of knowledge, insures against extreme views, and reduces groupthink.

“This diversity is needed to confront issues such as climate, technological, and other structural and social changes,” he said.

He also said that collaboration with government can be undertaken in a way that maintains the Reserve Bank’s political independence while working on the broader objective of improving wellbeing.

Here is the supporting speech.

Introduction

Tena koutou katoa

Thank you for the opportunity to talk about the Reserve Bank of New

Zealand and the changes we are making to maintain our credibility in

times of change.

I would like to focus on two building blocks of credibility:

renewing a social licence to operate by aligning our objectives with the needs of the public; and

achieving those objectives through good decision making enabled by a framework of good governance.

A common theme is the importance of transparency.

The imperative for change: Central banks in the 21st century

The first building block of credibility is the renewal of a social

licence to operate—by this I mean the legitimacy an institution earns by

serving the public interest. It is granted by the public when an

institution is seen to fulfil its social obligations.1

New Zealand was the first country to officially adopt inflation

targeting in 1989, with a number of central banks around the world

following the example.2

Under a single-decision-maker model, we brought inflation down from

around twenty percent to two percent in five years. In doing so, we

helped build our credibility during the high-inflation environment of

the times.3

Fast-forward to 2019, and monetary policy in New Zealand has

undergone major change. Firstly, we have adopted a dual mandate, focused

on achieving price stability and supporting maximum sustainable

employment. Secondly, we have adopted a committee structure for decision

making, and are delivering greater transparency in our decision making.

Why the change?

The reform of our framework was not merely a simple choice based on

technical performance. As you can see in figure 1, when it comes to

inflation and growth, over the past 30 years inflation-targeting central

banks (e.g. New Zealand and the United Kingdom) have a pretty similar

track record to central banks with a dual mandate (e.g. Australia and

the United States). 4

The imperative for change comes from more than examining our history;

it comes from our expectations of the future, and the present we find

ourselves in. Our policy framework changed because times are changing.

For the Reserve Bank to maintain its credibility and relevance, we must

change too.

Figure 1: Inflation, and GDP growth across monetary policy frameworks5

Wellbeing of our people

Inflation has been low and stable in New Zealand for nearly 30 years.

There is a greater appreciation that low inflation is a means to an

end, and not the end itself. In the fight to lower inflation that was

perhaps easy to forget. The end goal is, of course, improving the

wellbeing of our people.6

For many in the general public, employment is one tangible measure of wellbeing. Employment can provide an opportunity to earn your own wage, contribute to society, and live a fulfilling life.

It is in this light that the Reserve Bank Act (1989) has been amended to include a dual mandate with an employment

objective alongside our price stability goal. Incorporating the

objective of supporting maximum sustainable employment, and equally

weighting it alongside inflation, emphasises our long-term goal of

improving New Zealanders’ wellbeing. This aligns us with the needs of

the public. And it helps us renew our social licence to operate – the

first building block for maintaining our credibility.

But it is not enough for the public to believe in and understand our

objectives. We must also prove to them that they can be achieved. This

brings us to the second building block necessary for maintaining

credibility: establishing modern governance principles for dealing with

modern problems, and translating good governance into good decisions.

Good governance

In preparing for our dual mandate, and a formal Monetary Policy

Committee (MPC), we have updated the principles and processes that form

our governance framework for monetary policy.

In pursuit of greater transparency, we have also published these

principles and processes in a comprehensive Monetary Policy Handbook

(the Handbook). 7 This is an essential document, for everyone from school students to MPC members.

Importantly, it is also a living document that will evolve as our understanding evolves.

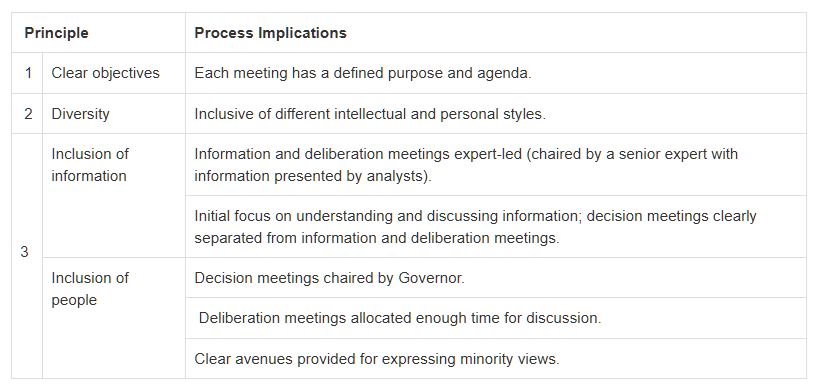

Principles

The first part of the Handbook I would like to cover is the section on MPC deliberation principles. 8

Figure 2: MPC deliberation principles

There are three principles which guide the deliberations within the MPC.

I’ve talked already about providing clarity around our objectives –

the equal weighting of our employment and inflation goals. This is the

first of our three principles.

The second, is diversity – diversity in the skills, experiences, thoughts, and personal characteristics of the MPC members.

The third, is inclusion – inclusion of information and people, ensuring decisions are made on the basis of all the available insights, and reflecting the views of all of the committee members.

Why are diversity and inclusion so important?

The governance literature shows that diversity and inclusion improves

the pool of committee knowledge, insures against extreme views, and

reduces groupthink.9 These principles drive the committee towards an unbiased policy decision – the best that is possible given existing information.

Think about this from a practical perspective. Modern monetary policy

is confronted by diverse issues such as climate, technological, and

other structural and social changes. A sole decision maker or uniform

committee cannot possibly hope to possess the broad range of insights

necessary to consider these issues.

A diverse committee operating in an inclusive environment can. It is

these additional insights that improve collective understanding, and

lead to better monetary policy decisions.

So you see these principles are not simply rhetorical devices. They

are carefully chosen pillars to support our credibility though good

decision making in achieving our dual mandate.

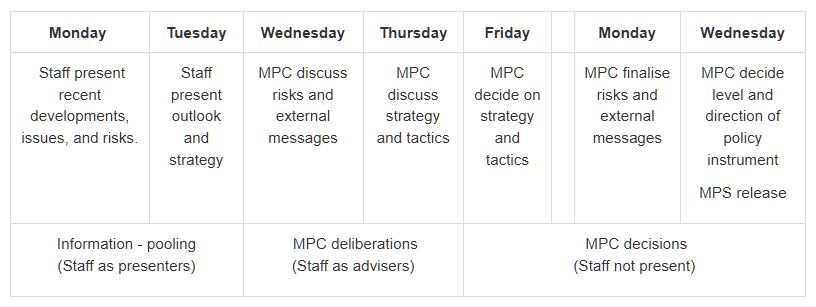

Good decision making

Processes

Our principles of good governance have directly influenced the policy-setting process of the MPC. 10

This is a process that has been designed with consensus-based decision

making front and centre, consistent with the agreement with the Minister

of Finance. 11

Figure 3: The structure of the forecast week for quarterly Monetary Policy Statements

We begin with information pooling, which flows through to MPC

deliberations, and culminates in the final decision making meeting.

As you can see, the policy-setting framework is highly collaborative

and deliberate. Deliberate in the sense that the process inspires lively

debate, giving MPC members every possible chance to challenge

assumptions, critique policy judgements and assess a range of policy

strategies to achieve our dual mandate objectives.

A crucial part of this is that the MPC members hold back their views

on the decision until the final stages, rather than starting with them.

This supports evidence-based decision making and guards against

confirmation bias.

The process begins with open information pooling on recent

developments and the outlook for the economy. Here, the MPC have the

opportunity to investigate and challenge the assumptions made in the

staff’s initial forecasts. This is where the MPC member’s judgement

enters the picture, and where creative tensions improve collective

understanding.

While the MPC members may enter the room with different insights and

questions about the economy, at the end of the information pooling stage

the committee shares a common reference point for the economic outlook.

There are numerous opportunities to discuss and reflect on key

issues, judgements, risks, strategy, and communication throughout the

week. There are also a number of anonymous internal surveys we perform

to gauge collective opinion among staff and MPC members.12

By the end of the week-and-a-half, the final monetary policy decision reflects the greater momentum of the MPC’s discussion.

We publish the final Official Cash Rate (OCR) decision, a Monetary Policy Statement (MPS), and a Summary Record of Meeting at the same time.

The Summary Record of Meeting captures the key judgements

and risks underpinning the central forecasts and decision, as well as

indicating where members of the MPC had different views. We identify any

differing views, and communicate where the most significant

uncertainties lie in our baseline forecasts.13

If consensus cannot be reached, a vote by simple majority would be

carried out, and the reasoning behind different stances disclosed in the

Summary Record of Meeting.

Our desire is that the transparency provided in the Handbook can help

the public understand how the Bank’s collective ‘mind’ works. If the

public can see the analytical rigour in our decision making, they should

have greater confidence in the MPC’s conclusions, and thus more faith

in the Reserve Bank.

Our credibility will be supported in the long run if the decisions

made by the MPC are unbiased and effective ones. Our results will speak

louder than our words.

Monetary policy strategy and our May decision

So far I’ve talked about the principles and processes we follow in

setting policy. Now I’m going to cover how we ‘walk the talk’ in

formulating our monetary policy decisions.14

Sound and effective monetary policy strategy requires more than just

deciding whether the OCR should go up or down on any given day; instead

central banks need to be transparent about their views of the economy

over the medium-term and how monetary policy might respond to a changing

economic landscape.

In this regard, around twenty years ago, the Reserve Bank became a

pioneer in another way. When publishing our interest rate decisions, we

also began to publish a forward (and endogenous) projection of interest

rates in the future. We use this to capture the overall stance of

monetary policy.

This tool remains integral to how the MPC sets monetary policy and understands the potential trade-offs with a dual mandate.

The first monetary policy decision of the new MPC occurred last

month, in May. Our starting point was a New Zealand economy where the

labour market was operating near maximum sustainable employment, and

annual core inflation pressures were within our 1 to 3 percent target

range but below the 2 percent mid-point.

We discussed the slowdown in global growth, and how this might affect

New Zealand. We also addressed the recent loss of domestic economy

momentum since mid-2018, through both tempered household spending and

restrained business investment.

In order to continue achieving our policy objectives, we agreed that

additional monetary stimulus was needed to help bring inflation back to

the 2 percent mid-point and support maximum sustainable employment. We

then turned to the question of the magnitude of stimulus we wanted to

adopt (the stance) and the timing and means by which we would try to

deliver this (the tactics).

Figures 4–6 show how different OCR paths could have been used to

achieve our objectives. While each path was consistent with meeting our

objectives, they each offered different trade-offs.15

Figure 4: Official Cash Rate (OCR) paths to achieve alternative monetary policy stances

Figures 5-6: Inflation, and employment gap under alternative OCR paths

If we kept rates unchanged (the higher OCR path), our projections

suggested that it would have taken a number of years for inflation to

return to target, and employment would have fallen below the maximum

sustainable level.

If we lowered the OCR by around 75 basis points over the next 12 months

(the lower OCR path), our projections suggested it would result is a

situation where both inflation and employment would be overshooting

their targets.

By contrast, the baseline (our final published projection), with the

OCR around 40 basis points lower over the next 12 months, brought

inflation back to target in a reasonable time period, with employment

remaining near the maximum sustainable level. We decided this path

captured our preferred strategy, and was robust to the key risks we had

discussed.

After agreeing on the appropriate stance of monetary policy, MPC

turned to the tactical decision of where to set the OCR at the May

meeting, and decided to cut the OCR by 25 basis points to provide a more

balanced outlook for interest rates.

This brings us to discuss the future.

Maintaining credibility in the future

Our central view is that New Zealand’s interest rates will remain

broadly around current levels for the foreseeable future. However, we

need to be ready to adapt to changing conditions, to meet our objectives

even when confronted with unforeseen developments.

An issue that policymakers and academics are grappling with around

the world is the role of both monetary and fiscal stimulus in a world of

low interest rates.

There is emerging consensus that coordination is necessary for an optimal response of broader macroeconomic policy.16 For central banks, operational independence does not have to mean operational isolation.

Rather, collaboration with government can be done in a way that builds

and reinforces the social licence to operate, by showing a willingness

to work with other partners to do whatever is necessary to achieve the

broader objective—improving public wellbeing.

Even with coordination between monetary and fiscal policy, if further

macroeconomic stimulus is needed quickly, the first line of defence

will still inevitably fall upon central banks.17

In New Zealand, we are in the strong position of having further room to provide conventional monetary stimulus if required (using the OCR).

Having effective unconventional policy options expands the

toolbox of a central bank, which is naturally more relevant in a low

interest rate environment. In this spirit, we published a Bulletin article last year on the practicalities of unconventional monetary tools in a New Zealand context, and we continue to learn from the lessons of our central banking cousins.18

It’s better to have a tool and not need it, than need one and not have it.

Conclusion

In the Handbook, we explore the history of central banking objectives, and see how dramatically they have evolved over time. 19

We haven’t always had a mandate to support maximum sustainable

employment, or to achieve price stability, or even control over interest

rates or the money supply.

Nothing lasts forever, and it is possible that the role of central

banks may change again in the future. Our Handbook will inevitably

change. We need to be ready to adapt when changes beckon.

And it is not enough to grudgingly adapt. In order to

maintain credibility, central banks must embrace change and prove to the

public that they are capable of delivering on their objectives. To

remain credible is to remain relevant. Central banks should keep their

eyes open, and be ready to change tack. Our destination—a world with

improved wellbeing for our citizens—may not change, but the best route

for getting there may.

We must adapt. We must continue to improve the wellbeing of our citizens. We must remain credible.

Macquarie Securities (Australia) Limited (‘Macquarie’) has paid a penalty totalling $300,000 to comply with an infringement notice given by the Markets Disciplinary Panel (‘the MDP’).

The MDP had reasonable grounds to believe that Macquarie contravened

the market integrity rules that deal with the provision of regulatory

data to ASX and Chi-X.

Over a four-year period from July 2014 to July 2018, Macquarie

transmitted approximately 42 million orders to ASX and Chi-X that

included incorrect regulatory data or omitted required regulatory data.

Over the same period, Macquarie also submitted approximately

377,000 trade reports to ASX and Chi-X with the same deficiencies.

The kinds of regulatory data that was incorrect or missing was information about:

‘capacity’: a notation to identify whether Macquarie was acting as principal or agent;

‘origin’: a notation to identify the person on whose instructions Macquarie was acting; and

‘intermediary’: the AFSL number of an intermediary using Macquarie’s automated order processing system.

The MDP emphasised that the provision of accurate regulatory data

enhances market transparency and ensures an orderly market. The

provision of incorrect or missing regulatory data to market operators

impedes informed regulatory decision-making by market operators and by

ASIC.

The MDP found that while Macquarie intended to comply with the market integrity rules, there were weaknesses in the configuration and integration of Macquarie’s systems, its processes for on-boarding new clients and its control framework.

The MDP considers Macquarie’s conduct to be negligent, having regard

to Macquarie’s poor design and implementation of updates to key systems,

the high number of orders and trade reports containing incorrect or

missing data, the multiple categories of incorrect or missing data and

the length of time the problems persisted without detection by

Macquarie.

Given Macquarie’s scale, market share and high market flows, the MDP

considers that market participants such as Macquarie have greater

potential and capacity to undermine market integrity. A market

participant such as this should carry a greater responsibility to

properly manage the risks that flow from their conduct. If that risk is

poorly managed, the financial consequences to the market participant

should be commensurately greater.

The MDP noted that, once Macquarie became aware of the scale of the

issues, which it reported to ASIC, it undertook a comprehensive review

to identify the causes, and promptly implemented remedial measures.

Maurice Blackburn Lawyers has filed the first class action against AMP, alleging that the bank eroded more than an estimated two million superannuation accounts with ‘unreasonable fees’, via InvestorDaily.

The action is seeking compensation for the bank’s super fund members. Maurice Blackburn has opened an online portal where members can sign up to claim fees dating back to 30 May 2013.

Material

tendered during the royal commission conveyed that AMP’s super funds

were charging uncompetitive administration fees, with high costs

exceeding returns and causing investment losses in some cases.

Maurice

Blackburn’s action has claimed that AMP trustees failed to monitor,

compare, negotiate or seek reductions of hefty fees being pocketed by

the group’s companies, despite their duty to act in the best interest of

members.

“It’s

important that inquiries and regulators uncover mass wrongdoing of this

nature, but that doesn’t give people back their hard-earned

superannuation funds, which they need for their retirement,” Brooke

Dellavedova, principal lawyer, Maurice Blackburn said.

“We estimate that over two million accounts have been impacted by AMP’s alleged misconduct.

“This

class action asserts that AMP trustees breached statutory and general

law obligations, essentially paying itself handsome fees from members’

funds. The case we are running will hold AMP to account for that.”

AMP said the proceeding will be “vigorously defended” in a statement, noting that it had cut product fees in the last year.

“In

2018, we cut fees on our flagship MySuper products, benefiting

approximately 600,000 existing customers as well as new customers,

improving member outcomes. In 2019, we also cut fees to MyNorth,” AMP

said.

“AMP and the trustees of its superannuation funds are firmly

committed to acting in the best interests of their superannuation

members and acting in accordance with legal and regulatory obligations.

We encourage any customers who have concerns to contact AMP directly or

their financial adviser.”

Litigation funder Harbour is funding the class action, which has been filed in the Federal Court in Melbourne.

“Importantly,

the matter will proceed in a way that means no one has to dip into

their own pockets to fund the litigation,” Ms Dellavedova said.

“AMP

account holders can band together to recover compensation, in

circumstances where most people would not bring a case on their own.

“If

you have had a superannuation account with AMP at any time since 30 May

2013, then you can sign up for this action to recover some of your lost

funds, including compound growth amounts you missed out on.”

Five global investment banks are facing a cartel class action lawsuit after a suit was filed at the Federal Court yesterday, via InvestorDaily.

Maurice

Blackburn Lawyers, who is also taking on AMP in a class action, have

launched the suit against UBS, Barclays, Citibank, Royal Bank of

Scotland and JP Morgan, claiming the banks colluded to rig foreign

exchange rates.

The suit alleges that between January 2008 and 15

October 2013, traders in chat rooms bearing names such as ‘The Cartel’

and ‘The Mafia’ communicated directly with each other to coordinate the

manipulation of FX benchmark rates.

“The chat rooms included

those named ‘The Cartel’, ‘The Mafia’, ‘One Team’, ‘One Dream’, ‘The

Players’, ‘The Three Musketeers’, ‘A Co-Operative’, ‘The A-Team’, ‘The

Sterling Lads’, ‘The Essex Express’ and ‘The Three Way Banana Split’,”

according to Maurice Blackburn’s statement of claim.

It is

alleged that the actions resulted in the pricing of ‘spreads’ and the

triggering of client stop loss orders and limit orders.

“Sharing

with each, alternatively one or more, of the other respondents, and/or

one or more of the other cartel participants, information in relation to

trade in FX Instruments with respect to one or more of the affected

currencies, including in relation to trade volumes and/or trade

strategy,” said the statement of claim.

The alleged conduct has

been the subject of extensive regulatory and private enforcement action

worldwide including settlements in the US and Canada resulting in the

payment of US$2.3 billion and CA$107 million respectively.

Some

of the allegedly affected currencies include the Australia, Canadian,

New Zealand and US dollar as well as the Russian ruble, Indian rupee,

the Euro and the British pound.

Maurice Blackburns principal

lawyer Kimi Nishimura said that the cartel behaviour could have affected

a number of Australian business and investors.

“Australian

businesses and investors – particularly medium to large importers,

exporters, institutional investors and businesses with operations

overseas – have been affected by the distortion of the FX market by

these banks.

“Such cartel behaviour cheats Australian businesses

in circumstances where they may already have been vulnerable to currency

fluctuations,” she said.

The class action will be represented by

lead plaintiff J.Wisbey and Associates, a medical equipment importer,

but is open to any customers that brought or sold currency during the

period where total value of transactions exceeded over $500,000.

Spokespeople for the banks involved did not issue a statement at time of writing.

The Bank Bill Swap Rate continues to track down, which means that Banks are sitting on considerable funding advantage, which is being used to discount attractor mortgage rates.

However, there is a strong case now for banks to reverse their out of cycle rate hikes imposed on borrowers over recent months, irrespective of whether the RBA moves the cash rate down next month.

This would help household with their budgets, and help support the weakening economy. They could also stop the rot in terms of falling bank deposit rates.

The NSW Supreme Court has selected law firm Maurice Blackburn to be the one to take a shareholder class action against AMP following last year’s royal commission; via InvestorDaily.

Five

law firms, Maurice Blackburn, Slater & Gordon, Phi Finney McDonald

and Shine Lawyers, all filed class action lawsuits against the financial

services company seeking compensation on behalf of shareholders.

The

actions followed a drop in AMP’s share price after testimony at the

royal commission last year, which was followed by the resignation of

AMP’s then chief executive and chairwoman and the dismissal of its

general counsel after criticism of his handling of a report by Clayton

Utz.

NSW Supreme Court Judge Julie Ward chose Maurice Blackburn,

whose funding model under their “no win, no pay” promise she considered

the best.

“In the present case the combination of: absence of a

separate funding commission; the incentive created by an uplift in fees

only once a specified resolution sum is achieved; the comparable return

based on standardised assumptions and the fact that no common fund order

is being sought, seems to me to point in favour of the [Maurice

Blackburn] funding model,” Judge Ward said.

The case against AMP alleges AMP engaged in misleading and deceptive conduct and breached its Corporations Act obligations when it failed to disclose its practice of charging fees for no service and in its interactions with ASIC.

An

AMP spokesperson welcomed the decision to permit only one class action

to proceed and said they would defend against the proceedings.

“AMP

will continue to vigorously defend the class action proceeding. AMP

denies the allegation that it had information that was required to be

disclosed to the market regarding ‘fees for no service’ and AMP’s

interactions with ASIC (including in respect of the Clayton Utz

report).”

AMP also noted that Maurice Blackburn had been ordered to pay millions in security for AMP’s legal costs.

“The selected class action has been ordered to pay $5 million in security for AMP’s costs,” said AMP

A

class action by Slater & Gordon will be consolidated into the

Maurice Blackburn case but with the latter running the litigation

alone.

Maurice Blackburn’s national head of class actions Andrew

Watson was pleased with the result and said he looked forward to getting

on with the job.

“We are pleased that the Court accepted that

Maurice Blackburn’s funding model could help deliver the best returns to

group members. We look forward to getting on with the important job of

obtaining a recovery for affected AMP shareholders.”

Class

actions typically take a long time to reach a conclusion with the next

date set for next week for a directions hearing, which is a largely

procedural issue.

While APRA’s proposed changes to serviceability assessments for ADIs have been broadly celebrated, others have expressed doubt that the regulatory revisions will stimulate the housing market in as meaningful a way as is hoped. Via Australian Broker.

“While these changes are welcome and will help some borrowers that

can’t quite access a mortgage currently to get one, it is unlikely to

result in a rebound in the housing market,” said CoreLogic research analyst Cameron Kusher.

Kusher referred to ANZ’s recent investor update to the market to elaborate on his stance.

The update from ANZ attributed reduced borrowing capacity to three

factors: changes to HEM accounting for 60%, the servicing rate floor

responsible for 30%, and income haircuts causing the remaining 10%.

Kusher pointed out that, according to this data, 70% of the reduction

in borrowing capacity is unrelated to the current serviceability

assessment model. Even if APRA were to change its current guidelines, it

will likely continue to be much more challenging to get a mortgage than

in the past.

Roger Ward, director of Champion Mortgage Brokers, agrees that the

current 7.25% assessment rate is just one of six lending standards that

have contributed to the credit squeeze.

Drawing from his 25 years in the banking and finance industry, Ward outlined the remaining five challenges to lending as:

Banks considering borrowers’ capacity to repay for the full 25 to

30 years of a mortgage term, despite most loans now only lasting seven

to eight years

A one-dimensional and inaccurate approach to identifying spending habits and current costs of living

Changes in credit reporting providing data on the last 24 months’

payment history on credit cards, with one late payment sometimes enough

to be declined by a bank

LVR changes and limitations, especially those impacting investors

Tiered interest rates dependant on the size of the original deposit

While allowing lenders to review and set their own minimum interest

rate floor will undoubtedly help some borrowers access previously

unreachable mortgages, the housing market will require stimulation from

elsewhere in order for dwelling values to begin their rise.

According to Kusher, “[APRA’s] proposed changes, in conjunction with

the uncertainty of the election now behind, will potentially provide

additional positives for the housing market. [They] would potentially

slow the declines further and may result in an earlier bottoming of the

housing market.

“Despite that prospect, it will remain more difficult to obtain a

mortgage than it has done in the past and we would expect that if or

when the market bottoms, a rapid re-inflation of dwelling values is

unlikely,” he concluded.