NAB says that an additional charge of $525 million after tax ($749 million before tax) relating to its customer remediation programme. As a result 1H19 cash earnings will drop by around $325 million and earning from discontinued operations by $200 million.

They say they have made around 360,000 payments to customers with a total valuer of $145 million, and the remediation team is building from 350 to around 500 across NAB.

Of the 1H19 charges, 90% relate to wealth, the remainder banking. IN combination with provisions raised in 2H18, total provisions for customer related remediation to 31 Match 2019 is $1,102 million.

The items responsible for this include:

Consumer credit insurance

Non-compliant advice to wealth customers

Adviser service fees by NAB advice partnerships (does not include allowance for customer refunds)

Adviser service fees charged by NAB Financial Planning

Banking related matters such as incorrect fee take on fee expect transactions.

These costs are to be held below the line as it were, but clearly investors and potentially customers will have to pay for this litany of poor practice.

It begs the question, can the NAB behaviourial norms be turned around? And at what cost?

The major

banks have seen their reputations significantly downgraded in an annual

perception survey, with AMP placing last out of 60 Australian companies.

The

Reputation Institute’s Australia RepTrak 2019 list examined 60 of the

top revenue making Australian firms, which saw all of the big four banks

and AMP ranked within the bottom ten.

The list was based on a

survey with around 10,000 respondents giving ratings across factors such

as trust and respect to generate overall reputation, in addition to

seven parameters: products/services, innovation, workplace, citizenship,

governance, leadership and performance.

AMP scored the lowest out of any company across all seven dimensions, dropping by 18 rankings from 2018.

NAB was the next lowest bank, falling at 58th place and having fallen 15 rankings from the year before.

Commonwealth Bank of Australia remained at its spot of 57th, while Westpac fell nine places to 55th.

ANZ fared the best of the big four, coming in at 51st, having fallen 16 places.

“In

the past 12 months we’ve seen many issues raised about corporate

behaviour and consumer trust,” Oliver Freedman, vice president and

market leader, Reputation Institute said.

“As a result, the reputations of our major banks and some financial services organisations have taken a major hit.”

Meanwhile,

Bendigo and Adelaide Bank rose seven places to 11th, which Mr Freedman

said was due to a strong performance in the individual measurements of

citizenship and governance.

“This proves that you can be a bank

and still have a strong reputation if you are focused on reputation

drivers that resonate with customers and increase trust,” he added.

Macquarie on the other hand came in at 42nd, down five places, as Allianz fell seven places from the year before to 37th.

New addition to the list Rest Super ranked 21st,while the Reserve Bank of Australia placed 18th, having risen by eight places.

AustralianSuper was down eight places to 15th.

“The

banking sector has a long road to recovery and could learn a lot from

those with consistently strong rankings, like Qantas and Air New

Zealand,” Mr Freedman said.

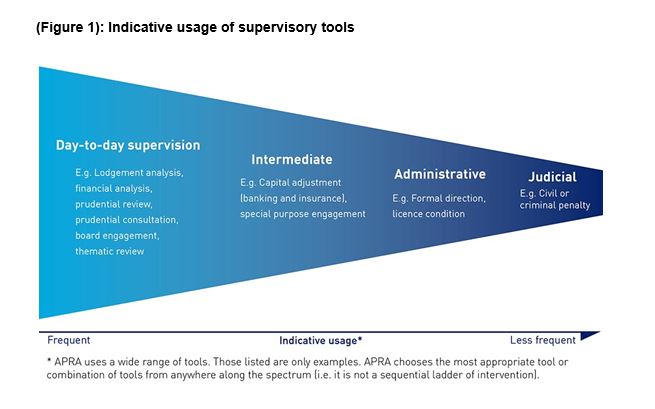

The Australian Prudential Regulation Authority (APRA) has released details on the future role and use of enforcement activities in achieving its prudential objectives.

Guiding principals include “risk-based”, “forward-looking”, “outcomes-based” and deterrence impact. Of course the question is, will it really make any difference? Here is the release.

APRA’s new Enforcement Approach, published today, sets out how APRA will approach the use of its enforcement powers to prevent and address serious prudential risks, and to hold entities and individuals to account.

The new Enforcement Approach is founded on the results of its Enforcement Review, which has also been published today. The Review, conducted by APRA Deputy Chair John Lonsdale, made seven recommendations designed to help APRA better leverage its enforcement powers to achieve sound prudential outcomes.

The APRA Members formally commissioned the Enforcement Review last November in response to a range of developments, including the creation of the Banking Executive Accountability Regime, the Prudential Inquiry into Commonwealth Bank of Australia, evidence presented to the Royal Commission into Misconduct in the Banking, Superannuation and Financial Services Industry, and proposals to give APRA expanded enforcement powers, particularly in superannuation. Mr Lonsdale led the Review, supported by a secretariat within APRA. Mr Lonsdale also utilised an Independent Advisory Panel comprising Dr Robert Austin, ACCC Commissioner Sarah Court and Professor Dimity Kingsford Smith to provide external perspectives and advice.

While APRA’s appetite for taking enforcement action is closely linked to a number of other components of its supervisory approach, the Review was focused on enforcement activity and not APRA’s wider operations

APRA Chair Wayne Byres

said APRA would implement all the recommendations, including:

adopting a “constructively tough” appetite to enforcement and setting it out in a board-endorsed enforcement strategy document;

ensuring APRA supervisors are supported and empowered to hold institutions and individuals to account, and strengthening governance of enforcement-related decisions;

combining APRA’s enforcement, investigation and legal experts in one strengthened support team, and ensuring resources are available to support the pursuit of enforcement action where appropriate; and

strengthening cooperation on enforcement matters with the Australian Securities and Investments Commission (ASIC).

Mr Lonsdale said the Review found APRA had, on the whole, performed well in its primary role of protecting the soundness and stability of institutions. But he said APRA could achieve better outcomes in the future by taking stronger action earlier where entities were not cooperative or open, and by being more willing to set public examples.

“APRA’s strong focus on financial risk has ensured the ongoing stability of Australia’s financial system, even during periods of financial and market stress, and protected the interests of bank depositors, insurance policyholders and superannuation members. But to remain effective, we must continue to evolve and improve, especially in response to the ways in which non-financial risks, such as culture, can impact on prudential outcomes.

“The recommendations of the Review will still mean that APRA as a safety regulator remains focused on preventing harm with the use of non-formal supervisory tools. However, APRA will be more willing to use the full range of its formal powers – such as direction powers and licence conditions – to achieve prudential outcomes and deter unacceptable practices,” Mr Lonsdale said.

Mr Byres thanked Mr Lonsdale and the APRA Review team for delivering a valuable piece of work that would sharpen APRA’s ability to hold entities and their leaders to account. He said enforcement activity is not intended to be a separate or stand-alone function, but rather a set of tools that APRA supervisors would use more actively, particularly in the case of uncooperative institutions. (See Figure 1)

“Having joined APRA only last October, John brought a fresh set of eyes to the task of examining APRA’s historical approach to enforcement. The Review acknowledges that as a supervision-led prudential regulator, APRA’s primary focus will always be on resolving issues before they cause problems for depositors, insurance policyholders and superannuation members, rather than relying on backward-looking actions after harm has occurred. In most cases, we will continue to achieve this through non-formal tools.

“However, formal enforcement is an important weapon in our armoury when non-formal approaches are not delivering prudential outcomes. Particularly as our powers have recently been strengthened in a number of areas, the new Enforcement Approach will ensure we make use of those powers as the Parliament intended. That means that in future, APRA will be less patient with the time taken by uncooperative entities to remediate issues, more forceful in expressing specific expectations, and prepared to set examples using public enforcement to achieve general deterrence.

“With the release of APRA’s revised Enforcement Approach today, the new enforcement appetite comes into effect immediately,” Mr Byres said.

Mr Byres indicated support for the recommendations on legislative change, and that these would be referred to the Government for its consideration. He also welcomed the recent passage of the Treasury Laws Amendment (Improving Accountability and Member Outcomes in Superannuation Measures No 1) Bill 2019 as a useful complement to APRA’s renewed enforcement appetite.

The Panel, led by Graeme Samuel, currently undertaking a Capability Review of APRA will take into account APRA’s new Enforcement Approach in its work.

Following an ASIC investigation, Citigroup will refund over $3 million to 114 retail customers for losses arising out of structured product investments offered by Citigroup between 2013 and 2017. Citigroup will also write to over 1000 customers remaining in the products to provide them an opportunity to exit early without cost.

ASIC investigated Citigroup’s sale and provision of general advice to

customers for fixed coupon structured products, which are complex,

capital at risk products tied to the performance of reference shares.

ASIC was concerned that while Citigroup considered its financial

advisers to be providing general advice, elements of its practice may

have led some customers to believe that Citigroup was providing personal

advice.

Citigroup’s practices included its advisers asking customers about

their personal circumstances, such as their tolerance for risk, and

providing financial education about benefits and risks to customers who

had no previous experience of investing in structured products.

Financial advisers have higher obligations and disclosure requirements

when providing personal advice.

From 1 January 2018, as a result of ASIC’s investigation, Citigroup

ceased selling structured products to retails clients under a general

advice model.

Citigroup will shortly start contacting affected customers. The

remediation will be completed by 10 September 2019, will be

independently assured and Citigroup will report to ASIC once the process

is complete.

ASIC has warned Australian financial services licensees that offer over-the-counter derivatives to retail investors located overseas could be breaking laws abroad, with Chinese authorities having alerted the watchdog that some online platforms have engaged in illegal activity, via InvestorDaily.

Regulators

in jurisdictions including Europe, Japan, North America and China have

restricted or prohibited the provision of certain OTC derivatives, such

as binary options, margin foreign exchange and other contracts for

difference (CFDs) to mitigate harm to retail investors.

ASIC has

expressed concern that some OTC derivative issuers that hold AFSLs may

be marketing or soliciting overseas clients to open accounts with

Australia-based licensees on the basis of avoiding overseas intervention

measures.

The regulator said is it considering whether breaching

overseas laws is consistent with obligations under Australian law to

provide services ‘efficiently, honestly and fairly’.

ASIC is also

considering whether it will see AFSL holders could be making misleading

or deceptive statements about the scope or effect of their license.

“AFS licensees who break the law in overseas

jurisdictions, or who mislead retail investors about their services

undermine the integrity of the Australian licensing regime,”

commissioner Cathie Armour said.

“ASIC will not tolerate that conduct.”

Chinese

authorities have already informed ASIC that “some online platforms are

illegally engaged in forex margin trading activities”.

Under Chinese law, no institution or agency has approval to carry out margin foreign exchange trading.

Temporary

product intervention measures have also been extended in Europe by the

European Securities and Markets Authority, with authorities in the UK

and Germany introducing permanent measures including anti-avoidance

provisions.

“AFS licensees offering OTC derivatives to overseas

retail clients should, as a matter of priority, seek advice on the

legality of their offerings to these clients,” commissioner Armour said.

“Any non-compliant activities should cease immediately and be notified to ASIC and the relevant overseas authorities.”

ASIC has released KordaMentha Forensic’s final report on CBA’s advice compensation program under its additional licence conditions.

CBA has offered approximately $9.3 million to customers whose advice has been reviewed as a result of the licence conditions imposed by ASIC in August 2014.

ASIC had imposed additional conditions on the Australian financial

services (AFS) licences of CBA’s Commonwealth Financial Planning Ltd and

Financial Wisdom Ltd with the consent of the licensees in August 2014,

and appointed KordaMentha Forensic as the independent expert to monitor

the licensees’ compliance with the additional licence conditions.

ASIC took this action because the licensees did not apply review and

remediation processes consistently to customers of 15 financial

advisers, disadvantaging some customers. The additional licence

conditions required that CBA offer compensation for inappropriate advice

that caused financial loss (where applicable) and offer affected

customers up to $5,000 to get independent advice from an accountant,

financial adviser or lawyer.

KordaMentha Forensic has produced five reports since the licence conditions took effect. In the first report, the Comparison Report, KordaMentha

Forensic identified inconsistencies in treatment of clients and

required the licensees to correct the inconsistencies for approximately

2,740 customers.

In the second report, the Identification Report,

KordaMentha Forensic found that the licensees had taken reasonable

steps in 2012 to identify which clients of the 15 advisers had to be

included in the compensation program.

KordaMentha Forensic also found that the licensees had taken

reasonable steps to identify other potentially high-risk advisers, but

that the licensees had not adequately reviewed advice given by 17 of

those advisers. To address this, KordaMentha Forensic prescribed the

scope of the additional reviews (of the 17 advisers) that the licensees

had to undertake.

KordaMentha then produced three additional reports describing the

licensees’ compliance with the conditions, the additional steps that the

licensees were required to take, and the compensation outcomes. Compliance Report Parts 1 & 2 assessed

the steps taken by the licensees to communicate with and compensate

(where applicable) customers of 15 former advisers for advice provided

between 2003 and 2012.

Compliance Report Part 3 described

the licensees’ review of the 17 potentially high-risk advisers and

KordaMentha Forensic’s conclusion that the licensees should apply the

compensation program to customers of five of those advisers.

In the final report, Compliance Report Part 4,

published today, KordaMentha Forensic covers the last of CBA’s advice

compensation program under the licence conditions. The report states

that CBA has offered a further $2.3 million to 232 clients of the five

advisers. This is in addition to:

$4.95 million (including interest) offered to customers of different

advisers under the licence conditions (reported in KordaMentha

Forensic’s Compliance Report Parts 1 & 2);

$1.9 million (including interest) offered to additional customers as

a result of CBA’s review outside the licence conditions. The need for

these reviews was identified during the licence conditions process.

This means that CBA has offered approximately $9.3 million to

customers whose advice has been reviewed as a result of the licence

conditions imposed by ASIC in August 2014.

The latest amendments passed into law last week extends the capital raising capabilities of mutuls in Australia, via mutual capital instruments (MCIs), which Moody’s rates as “credit positive”.

However, we are concerned by the extension of “financialisation” into the mutual sector, the potential higher risks it introduces as players compete for returns to investors, and the complexity of the financial markets they have to engage in. This could be a disaster.

Frankly, this just continues the journey away from meat and potato banking and is a further illustration of the myopic views of the regulators, especially APRA.

Rather than extending these additional capital channels, we need banking structural reform to contain the over-risky sector. This is the wrong strategy at the wrong time (especially as the housing sector tanks).

Anyhow, this is what Moody said:

On 4 April, Australia’s parliament passed the Treasury Laws Amendment (Mutual Reforms) Bill 2019, which amends the Corporations Act 2001 to allow mutually owned institutions to issue capital instruments. The development is credit positive for mutuals because it will enhance their ability to support growth, invest in technology innovation and, over time, will also strengthen their competitiveness.

In particular, the amended Act introduces a definition of a “mutual entity;” clarifies that demutualisation rules can only be triggered by an intended demutualisation and not by other acts such as capital raising; and creates mutual capital instruments (MCIs) that are specific to the mutual industry to raise equity capital.

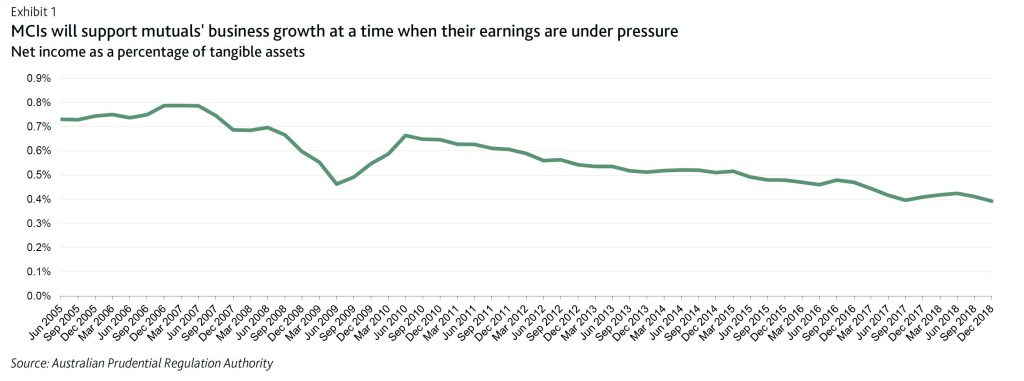

MCIs will provide mutuals with an additional capital channel to respond to growth opportunities, supplementing the retained earnings they have relied on to date. This additional capital channel is particularly important for mutual authorised deposit-taking institutions (mutual ADIs, which include mutual banks, building societies and credit unions) at a time when their profitability is under pressure. Pressure on profitability stems from competition for lower-risk owner-occupier mortgages with principal and interest repayments, the mutuals’ core products. This elevated competition stems from a number of factors including reduced overall loan growth; a reduced demand for investor mortgage loans in the face of potential changes to negative gearing and capital gains taxes; and tightened underwriting criteria at the major commercial banks as a result of public scrutiny during Australia’s Royal Commission into Misconduct in the Banking, Superannuation and Financial Services Industry.

Additional capital options will also help mutual ADIs build the scale and efficiency they need for technology investment, which is particularly important at a time when banking services are rapidly becoming technology-based. Compared with mutual ADIs, the large commercial banks have more resources to develop or acquire innovative products, digitise processes and integrate new technologies into their business models. Technology-driven financial firms (fintechs) are seeking entry to banking, while the Australian Prudential Regulation Authority (APRA) has established a framework that allows new entrants to begin operating at an earlier stage in their licensing process than previously. These new entrants are currently small and subject to regulatory constraints in taking deposits and making loans. In most cases they have not yet built up a retail customer base of meaningful size. However, they could grow to challenge incumbents, particularly small-scale ones like the mutual ADIs, over time.

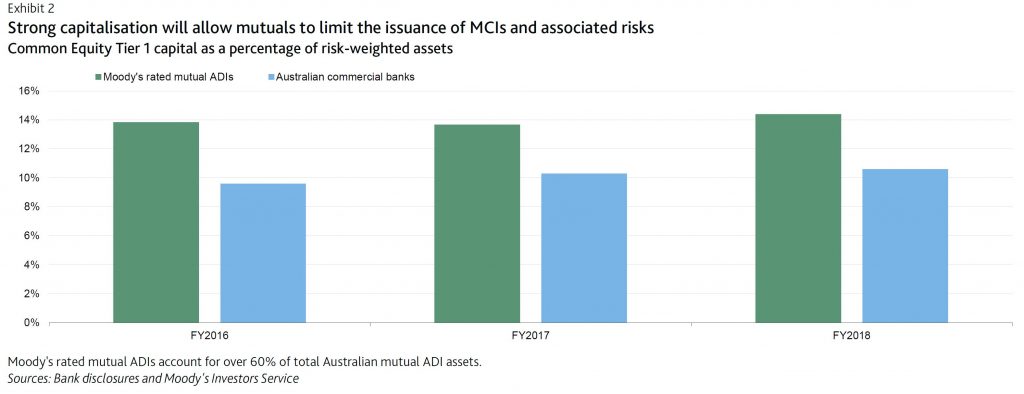

We do not expect mutual ADIs to swiftly ramp up their issuance of MCIs because their already-strong capitalisation and the current low loan growth environment are likely to reduce their need for additional capital. Mutual ADIs’ average Common Equity Tier 1 (CET1) capital ratio is well above that of the major commercial banks, which is itself strong by international standards. Moreover, APRA has set a 25% cap on the inclusion of MCIs in CET1 capital and has also capped the annual distribution of profit to holders of MCIs at 50% of a mutual institution’s net profit after tax for the year in question.

The prospect that the issuance of MCIs will remain limited will reduce the risk that mutual ADIs will significantly increase their risk profiles in an attempt to generate greater dividend returns for MCI holders. Mutuals will need time to amend their constitutions and build market recognition for MCIs. The experience of mutual banking peers in the UK also suggests that the process will be gradual. In the UK, mutuals have been allowed to issue core capital deferred shares, similar to MCIs, under the Building Societies (Core Capital Deferred Shares) Regulations 2013, but few have done so to date. We expect that Australian mutual ADIs that already have a strong investor base in the debt market to be in a better position to issue MCIs.

Industry insiders have revealed why banks are distancing themselves from wealth management and how their actions will reshape the Australian financial services sector; via InvestorDaily.

There

are a number of reasons why the big four have decided, to varying

degrees, to put a ‘for sale’ sign on their wealth management

businesses.

Some major bank chief executives have run a ruler

over their advice businesses and seen poorly performing divisions that

just don’t provide enough margin for the group’s bottom line.

Others,

like Westpac CEO Brian Hartzer, have seen the “writing on the wall” and

the mountain of increasing compliance that must be scaled to make

advice operational, let alone turn a profit.

But it may also have

been a strategic play based on negative sentiment, bad press and the

misguided belief that commissioner Hayne would propose an end to

vertically integrated wealth models.

“What

it looks like the banks have done in most cases, or in some cases, is

they’ve picked up their vertically integrated business, which consist of

advice and other products, and have looked to distance themselves from

that by either demerging or selling the wealth business,” Lifespan

Financial Planning CEO Eugene Ardino said.

Speaking exclusively

on the Investor Daily Live webcast on Wednesday (3 April), the dealer

group boss said the banks aren’t actually dismantling their conflicted

businesses – they’re selling them as bundled, vertically integrated

models where product and distribution sit under the same roof.

“That’s

not dismantling vertical integration. That’s really them trying to

distance themselves from wealth management. Whether that now goes ahead

in some cases remains to be seen,” he said.

“Perhaps what could have happened is some sort of recommendation around how to limit vertical integration or how to control it.

“The

issue you have is when you take a business that’s focused on sales and

that business takes over as the dominant force in a company that also

provides advice, then sales wins. I think that’s natural. Perhaps if

they had started there, that could have led to some moderation of

vertical integration.”

The royal commission hearings, more than

anything, were a targeted attack on the sales culture of large financial

institutions, many of which repeatedly defended their models as

profit-making businesses, often beholden to shareholders.

“In

product businesses, their job is to sell. That’s fine. There’s nothing

wrong with that. But if you’re putting an adviser hat on, there needs to

be some separation. That’s an issue of culture,” Mr Ardino said.

I

haven’t seen some of the employment contracts of the advisers from some

of the groups that got into trouble, but I would venture a guess that a

lot of their KPIs talk about new business rather than retaining

business and servicing clients.”

Fellow panellist and Thomson

Reuters APAC bureau chief Nathan Lynch said that despite Hayne’s failure

to propose banning vertical integration in wealth management, the model

will ultimately be dismantled by market forces.

“Hayne points

out that a lot of the dismantling of the vertically integrated model

comes down to the fact that it’s just not profitable. You have an

environment where vertical integration will be dismantled to some extent

by competitive forces and by technology,” he said.

“Servicing

the vast majority of client is going to become very difficult. Most

businesses are starting to pivot to the high end. I think we need to

view technology in advice as a positive, as an enabler.”

Deposit Bail-In is something which we have been discussing in recent times, not least because of the overt example now active in New Zealand under the Open Banking Resolution, the mandate from the G20 and the Financial Stability board and the implementation in several other countries in response to this.

In Australia, the situation has been unclear, since the 2018 bill was passed on the voice.

Treasury and politicians keep denying there is any intent to bail-in deposits to rescue a failing bank, but then divert to a discussion of the $250k deposit insurance scheme which first would need to be activated by the Government, and second only once a bank has failed. It is irrelevant to bail-in.

Bail-in is where certain instruments could be converted to shares in a bank to buttress its capital in times of pressure to attempt to stop a bank failing, and so would reduce the risk of a Government bail-out using tax payer funds. They will use private funds (potentially including deposits, which are unsecured loans to a bank), instead.

So, today we release an opinion from Robert H. Butler, Solicitor. This was addressed to the Citizens Electoral Council of Australia, and is published with their permission. The key finding is simply that:

Whilst not beyond doubt, it is my opinion that the provisions of the Act do provide for a power of bail-in of bank deposits which did not exist prior to the passing of the Act.

This means that unless the law is changed to specifically exclude deposits (any side of politics going to volunteer to drive this?), bank deposits are not unquestionably free from the risk of bail-in. And we have the view that the vagueness is quite deliberate, and shameful.

Time to pressure our members of Parliament, and raise this issue during the expected election ahead.

Here is the full opinion:

I have been asked to provide an opinion as to whether the Financial

Sector Legislation Amendment (Crisis Resolution Powers and Other Measures) Act

2018 (“the Act”) creates a power of bail-in by Australia’s banks of

customers’ deposits.

At a minimum, the Act empowers APRA to bail in so-called

Hybrid Securities – special high-interest bonds evidenced by instruments which

by their terms can be written off or converted into potentially worthless

shares in a crisis.

However, the Act also includes write-off and conversion

powers in respect of “any other

instrument”. The Government has contended that these words do not extend to

deposits, on the basis that the power only applies to instruments that have

conversion or write-off provisions in their terms, which deposit accounts do

not. However, the reference to “any other

instrument” would be unnecessary if the power only applied to instruments

with conversion or write-off provisions; moreover, banks are able to change the

terms and conditions of deposit accounts at any time and for any reason,

including on directions from APRA to insert conversion or write-off provisions,

which would thereby bring them within the specific terms of the write-off or

conversion provisions of the Act.

The issue could now be simply resolved by Government

passing a simple amendment to the Act to explicitly exclude deposits from being

bailed in.

Bail-in is one of the 3 alternative actions which can be

taken in respect of a distressed bank.

The alternatives are:-

Bankruptcy and liquidation of the bank;

Bail-out, which is the injection into the bank

of the necessary capital to meet the bank’s liabilities. This is the action

which was undertaken after the 2008 GFC by governments through their Treasuries

and Central Banks bailing out the banks with taxpayers’ funds;

Bail-in, which is the injection into the bank of

the necessary capital to meet the bank’s liabilities either by the bank writing

off its liabilities to creditors or depositors or converting creditors’ loans

or deposits into shares whereby creditors and depositors take a loss on their

holdings. A bail-in is the opposite of a bail-out which involves the rescue of

a financial institution by external parties, typically governments that use

taxpayers’ money.

Liability

limited by a scheme, approved under Professional Standards Legislation

The provisions of the Act as they affect bail-in require a consideration

of the issue in 3 different sets of circumstances, and the provisions of the

Act need to be considered separately in relation to each such set of

circumstances.

Those 3 sets of circumstances are:-

Hybrid Securities issued by banks;

Customer deposit accounts with banks;

Bank documentation implementing deposit

accounts.

(i) Hybrid securities

The ASX describes Hybrid Securities as “a generic term used to describe a security

that combines elements of debt securities and equity securities.” Whilst there

are a variety of such securities, in short they are securities issued by banks

which permit the amounts secured by the security to be converted into shares or

written off at the option of the bank in certain circumstances.

The Act provides specifically for Hybrid Securities.

Section 31 adds “Subdivision

B-Conversion and write off provisions” to the Banking Act 1959 and inserts

a definition Section 11CAA which provides that “conversion and write off

provisions means the provisions

of the prudential standards that relate to the conversion or writing off of:

Additional

Tier 1 and Tier 2 capital; or

any

other instrument.”

The Act also inserts Section 11CAB which provides:

“(1)

This section applies in relation to an instrument that contains terms that are

for the purposes of the conversion and write off provisions and that is issued

by, or to which any of the following is a party:

(a) an ADI;

……

The

instrument may be converted in accordance with the terms of the instrument despite:

any

Australian law or any law of a foreign country or a part of a foreign country,

other than a specified law; and

…..

The

instrument may be written off in accordance with the terms of the instrument

despite:

any

Australian law or any law of a foreign country or a part of a foreign country;

…..

Under the Basel Accord, a bank’s capital consists of Tier 1

capital and Tier 2 capital which includes Hybrid Securities.

The Section 11CAB provisions mean that any law which would

otherwise prevent the conversion or write-off of Hybrid Securities does not apply

unless a particular legislative provision specifically provides that it does

apply. One of the principle types of legislation that this provision would be

directed towards is consumer legislation, particularly those provisions which

allow a Court to set aside or vary agreements if a party has been guilty of

false or misleading conduct – this is precisely the sort of argument which

could be raised in the circumstances referred to by outgoing Australian

Securities and Investments Commission (ASIC) Chairman Greg Medcraft in an

exchange with Senator Peter Whish-Wilson in the hearings of the Senate

Economics Legislation Committee on 26 October 2017: Mr Medcraft said: “There are two reasons we believe a lot of

the retail investors buy these securities. One is they don’t understand the

risks that are in over 100-page prospectuses and, secondly – and this is

probably for a lot of investors – they do not believe that the government would

allow APRA to exercise the option to wipe them out in the event that APRA did

choose to wipe them out.“

When Senator Whish-Wilson raised the spectre of

“bail-in”, Mr Medcraft confirmed: “Yes, they’ll be bailed in. The big issue with these securities is the

idiosyncratic risk. Basically, they can be wiped out – there’s no default; just

through the stroke of a pen they can be written off. For retail investors in

the tier 1 securities – they’re principally retail investors, some investing as

little as $50,000 – these are very worrying. They are banned in the United

Kingdom for sale to retail. I am very concerned that people don’t understand,

when you get paid 400 basis points over the benchmark [4 per cent more than

normal rates], that is extremely high

risk. And I think that, because they are issued by banks, people feel that they

are as safe as banks. Well, you are not paid 400 basis points for not taking

risks…” He emphasised: “I

do think this is, frankly, a ticking time bomb.“

The over-riding intention behind Sections 11CAB(2) and

11CAB(3) is to deal with issues arising from the examples in the comments of

Graeme Thompson of APRA in an address on 10 May 1999 when he said: “… APRA will have powers under proposed

Commonwealth legislation to mandate a transfer of assets and liabilities from a

weak institution to a healthier one. This is a prudential supervision tool that

the State supervisory authorities have had in the past, and it has proved very

useful for resolving difficult situations quickly. We expect the law will

require APRA to take into account relevant provisions of the Trade Practices

Act before exercising this power, and to consult with the ACCC whenever it

might have an interest in the implications of a transfer of business.”

The new Sections 11CAB(2) & (3) mean that APRA does not need to consider

those issues (or any other) in relation to conversion and write-off of Hybrid

Securities.

(ii) Deposits

Whether or not bail-in of other than Hybrid Securities is

implemented by the Act has been the subject of debate and concern since the

Bill which led to the Act became public. The principal area of concern is

whether or not the bail-in regime was extended by the Act to deposits made by

customers with banks.

The central issue is the wording of the definition in

Section 11CAA quoted above and what “any

other instrument” means. “Instrument”

is not defined in the Act but a “financial

instrument” is defined by Australian Accounting Standard AASB132 as “any contract that gives rise to a

financial asset of one entity and a financial liability or equity instrument of

another entity.” As confirmed by the Reserve Bank, a deposit with an

ADI bank comes under such a definition – it is a contract with terms and

conditions as to the deposit being set by a bank, accepted by a depositor on

making a deposit and creating a financial asset (a right of repayment) and a

financial liability in the bank (the obligation to repay).

Deposits are created by “instruments” and are governed by the terms and conditions of

those instruments.

The intent of the reference to “any other instrument” in Section 11CAAAA is assisted by the

Explanatory memorandum which accompanied the Exposure Draft and which states:

“5.14

Presently, the provisions in the prudential standards that set these

requirements are referred to as the ‘loss absorption requirements’ and

requirements for ‘loss absorption at the point of non-viability’. The concept

of ‘conversion and write-off provisions’ is intended to refer to these, while

also leaving room for future changes to APRA’s prudential standards, including

changes that might refer to instruments that are not currently considered

capital under the prudential standards.”

Section 11AF of the Banking Act provides that APRA can

determine Prudential Standards which are binding on all ADIs. These standards

are in effect regulations which have the force of legislation by virtue of the

authorisation in the Banking Act. That Section provides, inter alia:

“(1)

APRA may, in writing, determine standards in relation to prudential matters to

be complied with by: (a) all ADIs; …..”

Banks are ADIs.

The various Prudential Standards issued by APRA are

accordingly headed with the phrase: “This

Prudential Standard is made under section 11AF of the Banking Act 1959 (the

Banking Act).”

That power then leads into the issue of APRA using this

authority to expand the meaning of “capital”

the subject of conversion or write-off, to encompass deposits if deposits are

not already covered by the reference to “any

other instrument”.

That these provisions as to conversion and write-off are

not limited to Hybrid Securities is confirmed in Section 11CAA itself as quoted

above. The provisions extend to “any

other instrument” by sub-section (b) of that Section and must relate

to instruments other than those referred to in sub-section (a), i.e. other than

“Additional Tier 1 and Tier 2 capital”

(being instruments which themselves contain an explicit provision for

conversion or write-off). All instruments that the Act refers to as to being

able to be converted or written off “in

accordance with the terms of the instruments” come under the

definition of “Additional Tier 1 and Tier

2 capital” – “any other

instruments” is not only an entirely unnecessary addition if the Act

is intended to apply only to instruments with conversion or write-off terms,

its very broad language must be intended to encompass some other instruments (“which are not currently considered capital”

as stated in the Explanatory memorandum) and that could extend to instruments

relating to deposits.

If Section 11CAA thus extends to instruments relating to deposits then APRA

can as the Prudential Regulator issue a Prudential Requirement Regulation or a

Prudential Standard for the writing-off

or conversion of deposits.

APRA already has a power to prohibit the repayment of

deposits by ADIs, a power which already verges on the writing off of those

deposits. The Banking Act Section 11CA provides:

“(1)

… APRA may give a body corporate that is an ADI … a direction of a kind

specified in subsection (2) if APRA has reason to believe that:

…..

the body

corporate has contravened a prudential requirement regulation or a prudential

standard; or

the

body corporate is likely to contravene this Act, a prudential requirement

regulation, a prudential standard or the Financial Sector (Collection of Data)

Act 2001, and such a contravention is likely to give rise to a prudential risk;

or

the

body corporate has contravened a condition or direction under this Act or the

Financial Sector (Collection of Data) Act 2001 ; or

….

(h)

there has been, or there might be, a material deterioration in the body

corporate’s financial condition; or

….

(k)

the body corporate is conducting its affairs in a way that may cause or promote

instability in the Australian financial system.

…..

(2)

The kinds of direction that the body corporate may be given are directions to

do, or to cause a body corporate that is its subsidiary to do, any one or more

of the following:

….

not to repay any money on deposit or

advance;

not to

pay or transfer any amount or asset to any person, or create an obligation

(contingent or otherwise) to do so;

…..”

This provision was inserted into the Banking Act in 2003 by

the Financial Sector Legislation Amendment Act (No 1).

It is not known whether this power has been exercised by

APRA. Relevantly Graeme Thompson in the address referred to above said: ”

… Particularly in the case of banks and

other deposit-takers that are vulnerable to a loss of public confidence, APRA

may prefer to work behind the scenes with the institution to resolve its

difficulties. (Such action can include arranging a merger with a stronger

party, otherwise securing an injection of capital or limiting its activities

for a time.)“

It is a relatively small step to then convert or write-off

what the ADI has been prohibited from repaying or paying out.

It might be argued that APRA’s powers in existing Sections

of the Act are not absolute and are subject to various qualifications and

limitations arising out of their context within the Act or the balance of the

Section or Sections of the Act in which they appear. To avoid such an

interpretation, Section 38 of the Act inserts 2 new sub-sections to Section

11CA in the Banking Act:

“(2AAA)

The kinds of direction that may be given as mentioned in subsection (2) are not

limited by any other provision in this Part (apart from subsection (2AA)).

(2AAB)

The kinds of direction that may be given as mentioned in a particular paragraph

of subsection (2) are not limited by any other paragraph of that subsection.”

APRA has already adopted the need for certain capital to be

capable of conversion or write-off, regardless of laws, constitutions or

contracts which may affect such decisions, the Explanatory Statement for

Banking (Prudential Standard) Determination No. 1 of 2014 stating:

“The Basel Committee on

Banking Supervision (BCBS) has developed a series of frameworks for measuring

the capital adequacy of internationally active banks. Following the financial

crisis of 2007-2009, the BCBS amended its capital framework so that banks hold

more and higher quality capital (Basel III). For this purpose, the BCBS

established in Basel III more detailed criteria for the forms of eligible

capital, Common Equity Tier 1 (CET1), Additional Tier 1(AT1) and Tier 2 (T2),

which banks would need to hold in order to meet required minimum capital

holdings.

Basel III provides that

AT1 and T2 capital instruments must be written-off or converted to ordinary

shares if relevant loss absorption or non-viability provisions are triggered.

Banking (prudential

standard) determination No. 4 of 2012 incorporated the Basel III developments

into APS 111 with effect from 1 January 2013. …”

(iii) Bank documentation implementing deposit accounts

Even if the words “any

other instrument” in Section 11CAA do not encompass deposits, there is a

further issue in relation to the implementation of bail-in of deposits

revolving around the issue of the documents/instruments issued by banks in opening

accounts and accepting deposits from customers.

The documentation issued by each Australian bank when

opening such an account, has a provision which enables the Bank to change the

terms and conditions from time to time without the consent of the customer. The

specifics of the power vary from bank to bank but each fundamentally contain

such a power. Some examples of various clauses are set out in Appendix 1.

If APRA as the Prudential Regulator issued a Prudential

Requirement Regulation or a Prudential Standard requiring a bank to insert a

provision into its documentation/instruments relating to deposit-taking

accounts providing for the bail-in of those deposits – their write-off or

conversion – then those provisions would then clearly come within the specific

provisions of conversion or write-off within the Act and the deposit the

subject of the account could be bailed-in immediately.

Such a directive could be issued by APRA in accordance with

the secrecy provisions in the Australian Prudential Regulation Authority

Act1998 and be implemented with little or no notice to the account holder.

Whilst not directly relevant to an interpretation of the provisions of the Act, there are a number of unusual and concerning aspects to its introduction, passing and intentions.

As noted above, the issue could now be simply resolved by

Government passing a simple amendment to the Act to explicitly exclude deposits

from being bailed in i.e. written off or converted into shares.

Whilst not beyond doubt, it is my opinion that the provisions of the Act do provide for a power of bail-in of bank deposits which did not exist prior to the passing of the Act.

As both the interim and final report from your Royal Commission into Misconduct in the Banking, Superannuation and Financial Services Industry

has confirmed, the good, decent, hardworking people of Australia are

under attack from their own banking system in a manner reminiscent of an

attack from a foreign invader that wants to destroy the will and

financial resources of the citizens in order to gain absolute control of

the country.

Americans, more than any other people in the world, can understand

and relate to the precarious predicament in which you now find

yourselves. The devious vices and devices of your banksters to transfer

the meager savings of the common man and woman to their own greedy

pockets have been laid bare by your Royal Commission. But just as

happened here in the United States following the report of the Financial Crisis Inquiry Commission, no concrete measures to end the domination of the banks has occurred.

Australians, like Americans, remain on the road to financial ruin at

the hands of predatory banking behemoths that are using their

concentrated money and political power to attack each and every

democratic principle that we cherish as citizens – from repealing

consumer-protection legislation to installing their own shills in

government to regulatory capture of their watchdogs to corrupting the

overall financial system that underpins the stability of our two

countries. Sadly, citizens at large do not understand that their own deposits at these mega banks are being used to accomplish these anti-democratic goals.

What has now occurred in Australia is precisely what has occurred in

America. Last year Bob Katter, MP in your House of Representatives,

introduced the Banking System Reform (Separation of Banks) Bill 2018 in

the Australian Parliament. This year, Senator Pauline Hanson introduced a

bill of the same name in the Australian Senate. The legislation is

tailored after the 1933 legislation that was passed in the United

States, the Glass-Steagall Act, to defang the banking monster that

brought on the 1929 stock market crash and ensuing depression by

separating commercial banks, which take in the deposits of risk-adverse

savers, from the globe-trotting, risk-taking, derivative-exploding

investment banks. (An unsavory group of bank shills succeeded in

repealing the Glass-Steagall legislation in the U.S. in 1999 and then

enriched themselves from the repeal. One year later the U.S. experienced

the dot.com bust and eight years after that the country experienced the

greatest financial crash since the Great Depression – what you call the

GFC or Global Financial Crisis but U.S. bank lobbyists prefer to dub

The Great Recession.)

U.S. Senator Elizabeth Warren, a Democrat, and the late Senator John McCain, a Republican, had been introducing the 21st Century Glass-Steagall Act

for the past five years in the U.S. Congress. Just like the legislation

proposed in Australia, it would have restored integrity to

deposit-taking commercial banks by separating them from the predatory

investment banks that financially incentivize their employees to fleece

unsuspecting customers while using the deposits to engage in high-risk gambles

that regularly implode. The powerful mega banks in the U.S. and their

legions of lobbyists have worked hard to prevent this legislation from

gaining momentum.

Despite the critical need for this legislation in both countries,

mainstream media has not done its share to inform and educate the public

about the pending legislation. We know this to be true in Australia

because the Royal Commission received more than 10,000 submissions from

the Australian public while the Senate’s request for public comment on

the Glass-Steagall legislation has thus far received just 350 responses.

The Senate Committee has elected to publish just a sliver of those responses.

You can submit your comments on the Australian legislation using an online form; or you can email your submission to economics.sen@aph.gov.au;

or you can mail your submission to Senate Standing Committee on

Economics, PO Box 6100, Parliament House, Canberra ACT 2600, Australia. The deadline for submissions is a week from this Friday, April 12, 2019.