The Commonwealth Bank has provided an update on its business plans and has said it is committed to the exit of its wealth management and mortgage broking businesses; via InvestorDaily.

The update follows last week’s release of the bank’s full response to

implementing the recommendations from the Royal Commission.

While CBA remains committed to exiting the wealth management and

mortgage broking business it has suspended these plans in order to focus

on the priorities of refunding customers and remediating past issues.

Over recent years, the bank has spent $1.46 billion on or provisioned to address refunding customers including $1.21 billion relating to the wealth management business.

The $1.46 billion comprises of over $600 million already paid to customers or provisioned to address issues relating to advice quality, fees for no service and banking fees and interest.

The program costs and processes of this work has cost the bank $650 million and another $200 million has been provisioned for wealth management related remediation issues and program costs, including ongoing service fees charged by aligned advisors.

Editors note: Post updated from millions to billions (source was incorrect).

It promises to be a dog fight Royale. The four big banks can be expected to behave

like uncontrollable Pit Bulls, determined to savage Senator Hanson’s Banking

System Report (Separation of Banks) Bill 2019.

This Bill is about re-establishing confidence in the banking system by

separating ‘core banking’, called retail and commercial banking where deposits

are protected, from the risky wholesale and investment banking.

By Patricia Warren,Byron Echo Vol 33 #40 March 13, 2019 p21

By default the

recent Haynes Royal Commission has brought focus on how banks are currently

structured to do business. It’s their

power base and they will fight to defend it. Fur will fly because bankers do not want a firewall

between deposits and the flow of these into their trading activities. Bloodletting can be expected should this Bill

stand in the way of using your money to cover their gambling in high return

investments, including derivatives.

Learned from the GFC?

People are

reminded that it was the collapse of the derivatives market that brought about

the Global Financial Crisis 2007/08.

Nothing has been learned. In December

2018 “The notional value of the

derivatives cleared worldwide is 4.4 times world GDP, up from 2.8 times in

2008.” While not all derivatives

are evil, it is estimated that Australian banks are currently exposed to more

than $37Tr in derivatives and billions in short term debt. The global derivatives markets are vast,

unregulated, some deliberately untraceable in off-shore entities and commonly

off the books. Currently, there is

potentially US$540Tr of global derivatives set to ignite a global financial

crisis.

Divorce time

The idea of separating core banking activities from the higher

risk investment banking is not new.

Leading financial commentator, Alan Kohl wrote of his random sampling of

10,140 submissions to the Royal Commission, “ Without exception they called for the banks to be broken up and most

of them, surprisingly, used the term ‘Glass Steagall’ suggesting that the

now-repealed American law that used to forcibly separate banking from insurance

and investment banking be introduced into Australia”. Hanson’s Bill has been crafted after the Glass

Steagall and modified to suit the Australian conditions.

There is widespread support for the breaking up of the banks,

including that coming from former CEOs of major banks, academics and former

Prime Minister Paul Keating. In fact,

there are now more people supporting the breakup of the banks since the Royal

Commission than before it.

The banks are powerful and effective lobbyists exercising undue

influence not only in the market place where they work like an oligopoly but

with both major political parties to which they reportedly have donated $2.6m.

Their relationship with Treasury and the regulator, Australian Prudential

Regulatory Authority (APRA) has been described as ‘incestuous’.

Currently there is approximately $2.8Tr held in deposits as

unsecured loans in Australian financial institutions of which over 80% is

concentrated in the four big banks. Banks are currently paying very little interest

on deposits whilst using a significant proportion of funds to trade in high

risk areas.

BAIL IN

Under Australia’s BAIL IN legislation, where there is no explicit

exclusion of deposits in the law, deposits are exposed to cover the gambling

risks of financial institutions in times of financial crisis in the global

system. So, if the derivatives market

collapses, as it did in the GFC, then cash will be used to BAIL IN and stablise

failing global institutions be it from peoples’ term deposits, business

operating and superannuation fund accounts. Politicians have refused to amend the

Financial Sector Legislation Amendment (Crisis Resolution Powers and Other

Measures) Act 2018 (FSLA) to exclude deposits from this and hence are

protecting the bankers and their risk taking behavior.

Deny Risk

CEO’s of the major banks and other leading financial institutions

deny that deposits are at risk. They argue they are controlled by APRA’s

prudential standards and that ‘currently’

and ‘as the legislation sits’, only

‘capital instruments’ can be called upon to stablise a failing

institution. But APRA can change this

under the secrecy provisions of the FSLA to capture deposits as part of BAIL

IN. There is a loop hole which allows

APRA to change its standards to include ‘instruments’ ‘that are not currently considered capital under prudential standards.”

Failed

Gatekeeper

No CEO responded to concerns raised directly with them months ago

about that provision. Nor did APRA! APRA has failed as the gatekeeper on our financial system.

APRA takes recommendations directly from the International Bank of

Settlement (IBS). This means our

financial institutions are influenced by the motivation of the central bankers

to protect the global financial system above depositors.

Under the

Banking System Reform (Separation of Banks) Bill 2019 it is intended to break

that direct connection. Instead, APRA must

not only come before an Australian parliamentary committee for “prior express written approval and consent” to

act before implementing any recommendations or decisions of any foreign bank,

or foreign authority but have Parliamentary approval to change its prudential

standards for the purpose of regulating our financial institutions.

Public Inquiry

Parliament’s

Senate Standing Committee on Economics is currently holding a public inquiry on

the Bill and calling for submissions.

It is a numbers game and broad based support of the Bill is needed to

counter what can be expected from the banks, Treasury and APRA.

Submissions

need only read: I support the Banking System Reform

(Separation of Banks) Bill 2019 and I support the separation of retail commercial banking

activities involving the holding of deposits from wholesale and investment

banking as proposed in the Bill. Submissions

need to be sent to economics.sen@aph.gov.au or mailed to the Senate Standing Committee

on Economics PO Box 6100 Canberra ACT 2600 by 12 April 2019. If you want your cash made more secure then

you’re encouraged to make a submission.

Alternatively, there is always under the

mattress.

Yesterday afternoon, the coalition government announced a dramatic change to its position on the future of trail commissions, via Australian Broker.

Rather than barring trail commissions on new loans starting in 2020,

Treasurer Josh Frydenberg announced that they will be left to operate as

is with a review held in three years’ time.

In the statement, mortgage brokers were said to be “critically

important” for securing better consumer outcomes in the mortgage market.

“The Government wants to see more mortgage brokers – not less,” the media release stated.

MFAA CEO Mike Felton

said, “The announcement reflects the fact that the case for the removal

of mortgage broker trail commission has not been made, nor has it been

demonstrated that existing trail arrangements lead to poor customer

outcomes.”

In past weeks, there has been confusion throughout the broking

industry as to what benefit was being sought from eliminating the trail

commission payment structure.

“Trail commission for mortgage brokers is deeply misunderstood, and

is often confused with ongoing commissions earned by other financial

services providers,” Felton said.

He explained, “Trail is contingent income that is only paid to a

broker if the loan is not in arrears, is not refinanced and does not

involve fraud.

“As such, it is an important control mechanism that aligns the

interests of brokers and their customers, and ensures that the broker

focuses on the customer relationship rather than simply pursuing the

next transaction.”

“Today’s announcement is a positive step by the treasurer and

provides a good timeframe for this consultation process to take place,”

he said.

Meanwhile, FBAA managing director Peter White welcomed the move but said that policy changes were needed to back it.

“The Coalition’s announcement to keep trail commissions has been

delivered in a pre-election environment so uncertainty remains about how

exactly this will work after the election. Hayne simply didn’t get it

but it’s now the case that both sides of politics are now very clear on

the importance of mortgage brokers.

“Both the Coalition and Labor recognise that the recommendations of

the royal commission would in fact hand power back to the big four

banks, which is an absurd result,” he added.

Treasurer Josh Frydenberg has said that the government will look at reviewing the impacts of removing trail in three years’ time rather than abolishing it next year as originally announced, following concerns regarding competition, via The Adviser.

In

an announcement on Tuesday (12 March), Treasurer Josh Frydenberg said

that “following consultation with the mortgage broking industry and

smaller lenders, the Coalition government has decided to not prohibit

trail commissions on new loans but rather review their operation in

three years’ time”.

The review, to be undertaken by the Council of

Financial Regulators and the Australian Competition and Consumer

Commission (ACCC) will therefore look at both the impacts of removing

trail as well as the feasibility of continuing upfront commission

payments.

Both the abolition of trail and upfront commissions were recommended by commissioner Hayne in his final report for the Royal Commission into Misconduct in the Banking, Superannuation and Financial Services Industry.

While the government had initially said in its official response to the final report

that it would ban trail commission payments for new mortgages from 1

July 2020, the Treasurer has now said that the removal on trail will

instead be reviewed in three years’ time.

“Mortgage

brokers are critically important for competition and delivering better

consumer outcomes in the mortgage market. Almost 60 per cent of all

residential mortgages are settled by mortgage brokers,” Mr Frydenberg

said on Tuesday.

“There are 16,000 mortgage brokers across

Australia – many of which are small businesses – employing more than

27,000 people. The government wants to see more mortgage brokers, not

less,” he said.

The Treasurer added that ASIC’s 2017 review of

broker remuneration “did not identify trail commissions as directly

leading to poor consumer outcomes and did not recommend the removal of

trail commissions”.

“Only the government can be trusted to protect

the mortgage broking sector and ensure that competition is strengthened

so consumers get a better deal,” he said.

Mr Frydenberg added that the government was “taking action on all 76 recommendations contained in the final report” of the banking royal commission and had already announced a number of new measures that will be brought in, including:

a best interests duty that will legally obligate mortgage brokers to act in the best interests of consumers;

a new requirement that the value of upfront commissions be linked to the amount drawn down by consumers;

a ban on campaign and volume-based commissions; and

a two-year limit on commission clawbacks.

“These

changes will address conflicts of interest in the industry by better

aligning the interests of consumers and mortgage brokers,” Treasurer Frydenberg said.

The Australian Bankers Association (ABA), says the banking industry welcomes a new independent report by former Public Service Commissioner Mr Stephen Sedgwick AO, which has found that banks are on track to meet their 2020 deadline to overhaul staff pay, a critical issue highlighted by the Royal Commission, while also noting there is more work to be done to ensure full implementation.

In April 2017, the industry announced an overhaul to the way banks pay and reward their retail staff to deliver better outcomes for customers. The deadline to fully implement these changes is the 2020 performance year. These key changes include:

No longer paying retail bank staff bonuses based directly or solely on sales

Where incentives are paid, they will be based on a range of measures such as excellent service and good outcomes for customers (with financial targets not the main component)

Incentives paid will not be based on the type of product (eg one type of credit card over another) but rather rely on the time taken by staff to process an application for a customer

Refocussing workplace culture and leadership structure to ensure a focus on the customer is paramount.

Following the release of the Royal Commission Interim Report, the Australian Banking Association commissioned a progress report by Mr Sedgwick on the changes to ensure the reforms were on track to meet their 2020 deadline.

The key findings of this progress report are:

Banks are on track to implement the report well in advance of the 2020 deadline

Banks have significantly reduced the use of bonuses based on financial incentives for front line staff

Bonuses for bank tellers, typically 10% of fixed salary, are now generally based on broader customer service measures, with ‘sales based’ measures greatly reduced

Salaries for other bank staff such as ‘in house’ mortgage brokers, are now greatly weighted towards fixed pay, rather than variable bonuses

Banks are retraining front line staff to encourage a ‘customer first’ approach, rather than a ‘sales first’ mindset

There is still more work to be done on ‘leaderboards’ (which track individual performance), with the practice still found to be occurring in a limited number of branches.

Regarding third party mortgage brokers, Mr Sedgwick noted his recommendations made in 2017 were not yet fully met (although there is a 2020 deadline). He acknowledged the uncertainty caused by the Royal Commission which itself has recommended different changes to the area and acknowledged the difficulty in navigating reform in a diverse industry such as mortgage broking.

CEO of the Australian Banking Association Anna Bligh said the Royal Commission highlighted the need to continue to implement the 2017 report by Mr Sedgwick as soon as possible.

Commissioner Hayne in his final report stated:

“In my view, full implementation of the Sedgwick recommendations is an important first step towards improving front line remuneration practices. But implementation will only improve these practices if banks implement the Sedgwick recommendations both in letter and in spirit” (pg 370-371 Final Report, Royal Commission into Banking, Superannuation and Financial Services).

“The way banks pay their staff was revealed as a critical issue of concern throughout the Royal Commission,” Ms Bligh said.

“When investigating the issue of bank staff pay Commissioner Hayne acknowledged these reforms were an important first step towards improving front line remuneration practices.

“In the Final Report, Recommendation 5.5 made it explicitly clear that Sedgwick needed to be fully implemented, which the industry has heard loud and clear.

“Following the Royal Commission Interim Report the industry saw the need to do a ‘check-up’ on the reforms to bank staff pay to ensure they were on track to meet their commitments by 2020.

“Mr Sedgwick engaged a number of stakeholders including the Financial Sector Union, ASIC and APRA to ensure the report was thoroughly independent and gave the most accurate reflection of the current state of the reforms.

“This report has found banks have been on the front foot in implementing the ‘Sedgwick reforms’ to bank staff pay, with many on or ahead of schedule in overhauling their salary structures.

“Bonuses for bank staff are better balanced, focussing on what’s best for the customer and excellent service rather than simply sales targets.

“Mr Sedgwick also highlighted the lack of action on mortgage broking remuneration, however he acknowledged the complexity of the area given the number of parties involved and potential for regulatory intervention following the Royal Commission,” she said.

ASIC today released an update on the fees for no service (FFNS) further review programs undertaken by six of Australia’s major banking and financial services institutions.

ASIC’s ongoing supervision of the review programs undertaken by AMP,

ANZ, CBA, Macquarie, NAB and Westpac (the institutions) has shown that

most of the institutions are yet to complete further reviews – i.e. reviews to identify systemic FFNS failures beyond those already identified and reported to ASIC since 2013.

ASIC Commissioner Danielle Press said the institutions had taken too

long to conduct these reviews, and welcomed the Government’s commitment

to give ASIC new directions powers that could speed up remediation

programs in the future.

‘These reviews have been unreasonably delayed. ASIC acknowledges that they are large scale reviews – they relate to systemic failures over long periods with reviews going back six to 10 years and cover 36 licensees from the six institutions that currently authorise more than 7,000 advisers]. However, we believe the institutions have failed to sufficiently prioritise and resource their reviews, particularly as ASIC advised them to commence the reviews in mid-2015 or early 2016.

‘We are pleased the Government has agreed to adopt recommendations from the 2017 ASIC Enforcement Review Taskforce Report,

which includes a directions power. This would allow ASIC to direct AFS

licensees to establish suitable customer review and compensation

programs,’ she said.

The main reasons for delays by the institutions are:

poor record-keeping and systems within the institutions, which mean

that in many cases they have been unable to access customer files for

review;

failure by some institutions to propose reasonable customer-centric

methodologies to identify and compensate customers despite ASIC’s clear

articulation of expectations. (For example, ASIC rejected a few of the

methodologies such as a requirement for customers to ‘opt-in’ to the

review and remediation program, and a proposal to assess if there had

been a ‘fair exchange of value’ with customers instead of assessing

whether customers received the specific services they paid for); and

some institutions have taken a legalistic approach to determination

of the services they were required to provide. (For example, ASIC’s view

is that if the agreement requires an annual review, the mere offer of

an annual review is not sufficient.)

Overview of ASIC’s FFNS work

ASIC’s large-scale FFNS supervisory work includes overseeing:

the institutions’ programs to compensate customers impacted by the

reported failures to provide advice services paid for by customers (compensation programs); and

the institutions’ reviews to determine whether there were further

systemic FFNS failures beyond those already identified and reported to

ASIC (further reviews).

Under the compensation programs, AMP, ANZ, CBA, NAB and Westpac have

collectively paid or offered approximately $350 million in compensation

to customers who were charged financial advice fees for no service at

the end of January 2019. Additionally, the institutions have provisioned

more than $800 million towards potential compensation for further

systemic FFNS failures. However, these reviews are incomplete.

Along with supervision of the compensation programs and further reviews undertaken by the institutions, ASIC

is also conducting a number of FFNS investigations and plans to take

enforcement action against licensees that have engaged in misconduct.

Westpac chief executive Brian Hartzer has denied claims that Australian employers are offered special deals from the bank if BT becomes the default superannuation provider for employees, via InvestorDaily.

Appearing at the House of Representatives Standing Committee on

Friday, Mr Hartzer was questioned about the major bank’s superannuation

offering through BT Financial.

Labor MP Matt Thistlethwaite asked the Westpac CEO about reports that

employers could be prosecuted for the underperforming retail super

funds that manage staff retirement savings.

Mr Thistlewaite referred specifically to a 21 January news article in The Australian that noted Westpac’s BT super fund was one of the worst performing super funds in the last seven years.

“The article points to ‘bundled services’ for the business behaving

employees in your BT retail fund. What are those bundled services?” the

MP asked.

Mr Hartzer said he was not familiar with the news article.

“I’m assuming that bundled services means you provide concessions to

the employer on other banking products for bringing them into BT’s

fund?” Mr Thistlethwaite said.

Mr Hartzer replied: “We checked quite closely and that is not our

practice. The corporate super that is offered up is meant to be on a

competitive basis for the services provided. We don’t provide

inducements in terms of banking.”

Concerns over the relationship between retail super funds and

employers were raised by the Productivity Commission in its report into

the superannuation sector. Released in January, the report recommended

the creation of a ‘best in show’ list of funds for employees to choose

from.

In December last year, The Australian reported that ASIC

commissioner Danielle Press said the regulator would crack down on

employers who placed employees in poor-performing funds in exchange for

“bundled services” that were provided to them by the banks and finance

companies that owned the funds.

“We’ve got to look at the role of employers in the default system and

how they are making their decisions on what funds are their default

funds,” Ms Press told The Australian.

“At the end of the day, consumers are disengaged. There’s no

obligation on employers to make that default choice in the best interest

of their employees.”

More evidence of the peeling back of US bank disclosure, which may reduce the incentive for bank managements to continually improve their capital and risk management processes.

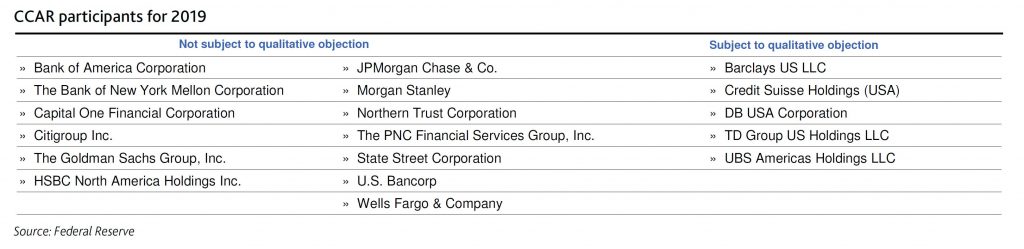

On 6 March, Moody’s says the US Federal Reserve Board (Fed) announced the elimination of the qualitative objection in its 2019 Comprehensive Capital Analysis and Review (CCAR) for most stress test participants. Only five banks, all US subsidiaries of foreign banks, will remain subject to qualitative objection in the current stress tests cycle. In the past, the Fed has used the qualitative objection to address deficiencies in banks’ capital-planning process. Its elimination is credit negative because it reduces public transparency around the quality of banks’ internal capital and risk management processes.

Under the revised rules, a bank must participate in four CCAR cycles before it qualifies for exemption from a potential qualitative objection in future years. If a firm receives a qualitative objection in its fourth year, it will remain subject to a possible qualitative objection until it passes. For most of the five firms still subject to the qualitative objection, their fourth year will be the 2020 CCAR cycle. In total, 18 firms are subject to this year’s CCAR exercise, with five of them subject to a possible qualitative objection.

All five firms subject to the qualitative assessment in 2019 are foreign-owned intermediate holding companies (IHCs), most of which were first subject to the Fed stress tests on a confidential basis in 2017. If the IHC has a bank holding company subsidiary that was subject to CCAR before the formation of the IHC, then the IHC is not considered the same firm for the purpose of the four-year test.

The Fed noted that since CCAR was implemented in 2011, most firms have significantly improved their risk management and capital planning process. Going forward, its capital-planning assessments will be through the regular supervisory process. The Fed highlighted as an example the new rating system for large financial institutions, which will assign component ratings of a firm’s capital planning and positions. However, these ratings will be confidential supervisory information and unavailable to the public unless the deficiencies are so severe that they warrant formal enforcement action. The new process replaces an independent comparative assessment.

The lack of public disclosure may also reduce the incentive for bank managements to continually improve their capital and risk management processes, which the CCAR qualitative review encouraged.

As previously announced, 17 large and non-complex bank holding companies, generally with $100-$250 billion of consolidated assets, will not be subject to CCAR in 2019 because of the Economic Growth, Regulatory Relief, and Consumer Protection Act (the EGRRCPA), which became law in May 2018. They will next participate in 2020. Most of these banks were removed from the qualitative objection in 2017 and the Fed will only object to their capital plans if they fail to meet one of the minimum capital ratios under the stress scenarios on quantitative grounds.

The Fed’s announcement was incorporated with its release of instructions for the 2019 CCAR cycle. The Fed also provided information on allowable capital distributions for those firms whose CCAR cycle was extended to 2020. For those banks, the Fed published letters that address each bank’s individual 2019 capital plans. The Fed pre-authorized the firms to distribute, net of any issuance of capital, up to the sum of:

The additional capital the firm could have distributed in CCAR 2018 and remained above the minimum requirements; plus

Capital accretion (change in capital ratios since CCAR 2018); plus

its already approved capital distributions for first-quarter 2019 and second-quarter 2019; minus

its actual distributions for first-quarter 2019 and planned distribution for second-quarter 2019

This plan is also credit negative because it permits capital distributions based on last year’s results, which incorporated a modestly less stringent severely adverse scenario than the 2019 stress test, and it also fails to incorporate any interim changes in the banks’ risk profiles. If any of the 17 banks wants to distribute more than its maximum pre-authorized amount, it may submit a capital plan to the Fed by 5 April 2019 and will be subject to the 2019 CCAR supervisory stress test.

Australia’s major banks will continue to face heightened regulatory scrutiny following recent public inquiries, including the Royal Commission, that identified shortcomings in conduct, governance and compliance, and will all be engaged in remediation that could distract management from day-to-day business, says Fitch Ratings. These challenges come amid other near-term pressures on earnings from a generally tougher operating environment.

The four major banks –

ANZ, CBA, NAB, Westpac – have large market shares across most products

in Australia and New Zealand, which support strong earnings and balance

sheets and help moderate risk appetite compared with many international

peers. However, it may be difficult for the banks to exercise these

advantages fully in an environment of increased public and regulatory

scrutiny, and pressure to increase their focus on customers rather than

shareholders.

In the longer term, there is a risk that the

findings of the inquiries may erode the market position of the four

major banks, either by reducing management focus on revenue growth or

through reputational damage – of which there is so far little evidence.

CBA

and NAB were found to have the most significant weaknesses in their

operational and compliance risk frameworks, and therefore face larger

risks from the remediation process. This is reflected in the Negative

Outlooks Fitch has assigned to these banks’ Long-Term Issuer Default

Ratings. Shortcomings that allowed misconduct issues to arise were

particularly evident at CBA, which is the only bank that will go through

to a formal remediation process and face increased capital

requirements.

Addressing conduct, culture and governance

problems should improve the soundness of the system in the longer term,

but will exacerbate banks’ short-term challenges. Fitch maintains a

negative outlook on the sector as earnings are likely to remain under

pressure in 2019 due to slower loan growth, especially in the

residential-mortgage segment, falling net interest margins, rising

wholesale funding costs, and increasing impairment charges, albeit from a

low level.

The main downside risks to bank performance continue

to stem from the housing market, where prices continue to decline after

large increases up to mid-2017. A sharp drop may result in negative

wealth effects for consumers and could undermine banks’ asset quality.

However, our central scenario is that house prices will fall by only

around 5% in 2019, which would represent a gradual easing of housing

market risks. Moreover, regulatory intervention in the mortgage sector,

including more stringent underwriting measures, has helped to reduce

risks in newer vintages of loans, and should make the major banks more

resilient to any downturn.

YBR told the market on Friday it will incur a statutory after-tax loss for the six months to 31 December 2018, via Financial Standard.

The

results include a material non-cash impairment charge on the carrying

value of the wealth management and lending business and various other

assets across the group, it said.

However, the impairment will not

affect the net present value of the group’s net trail commission

receivable from its underlying mortgage book or book of insurance

premiums under management, but will be applied against goodwill and

intangible and other assets.

The

charge results from assessing goodwill and other intangibles in light

of recent events, including the Royal Commission, YBR said.”It is a

non-cash balance sheet adjustment and has no impact on the underlying

operations of the business.”

One of the Royal Commission’s final

recommendations is to ban lenders paying trail commission to mortgage

brokers and other commissions for new loans.

This

should be enacted within two or three years, Commissioner Kenneth Hayne

said. “The borrower, not the lender, should pay the mortgage broker a

fee for acting in connection with home lending.”

YBR expects the audited half-year report to be lodged before the Corporations Act deadline of 15 March 2019.

It last traded at 5.4 cents per share, plunging from about 14 cents compared to a year ago, down more than 61%.