ANZ has announced that it will implement a swathe of changes to its home and investment lending policy., via The Adviser.

ANZ has informed brokers that it will introduce enhanced home loan verification requirements, effective from 20 November.

Key changes include the following:

PAYG income: Brokers are required to obtain three months’ bank statements showing salary credits in order to verify income (in addition to payslips).

For casual, temporary and contract employees, six months of continuous employment is required, supported by six months of bank statements showing salary credits.

Overtime, bonus and commission income: Brokers are required to make inquiries of customers as to whether any of their income is comprised of overtime, bonus or commission, and record the overtime/bonus/commission amounts in the Statement of Position, adding that brokers should also include an explanation of the income in their submission/diary note.

In line with current ANZ policy, any income from bonus, commission or overtime needs to be removed from the income calculation and shaded in accordance with credit policy (currently 80 per cent), before being added back to the customer income, using the ANZ Toolkit.

However, the bank noted that if the overtime/commission/bonus amount cannot be identified from the customer’s payslips, or the customer has chosen to provide six months’ salary credits rather than salary credits and payslips, further payslips may be required in order to verify the amount of income that is derived from bonus, overtime or commission payments.

Casual, temporary or contract employment: Where a customer is in casual, temporary or contract employment, the customer will need to provide evidence of six months of continuous employment via salary credits through either ANZ transaction history or OFI bank statements.

In order to satisfy the continuous employment requirement, customers cannot have a gap greater than a total of 28 days (either continuous or cumulative), which ANZ said is measured by the pay period start/end dates on payslips or the number of salary credits available on ANZ transaction history/ OFI bank statements.

Additional checks by ANZ for irregular income: An additional check will be performed by ANZ to confirm if a customer’s income is irregular. If the assessor cannot satisfy themselves of the reasons for irregular income via the documents provided, the Statement of Position and any relevant diary notes, then they will contact the broker for further information.

OFI home loan: Three months of statements are required (even if the home loan liability is not being refinanced) to confirm monthly repayment amount and that the account conduct is satisfactory.

Where the loan account is less than three months old, a copy of the Letter of Offer (LOO) or the loan transaction history (showing balance AND at least one repayment) is considered acceptable provided the above conditions are also met.

Rental expenses: Three months of bank statements showing rental payments made by the customer will be required, or a lease agreement to verify the ongoing rental expense.

Brokers are required to make adequate inquiries with customers about their financial situation and provide additional commentary to explain any material differences between verification documents (for example, bank statements) and customer-stated income or expense figures in the Statement of Position, as well as any potential indicators of financial hardship.

ANZ stated that indicators of financial hardship may include adverse account conduct (e.g. overdrawn, excess, late payments, arrears), regular overdrawing of an account due to gambling transactions, and payday lender transactions.

Brokers have also been asked to include any additional commentary/explanation in a diary note, which the bank said will form part of ANZ’s assessment.

Changes to Broker Interview Guide: Also effective on 20 November, ANZ has also announced that it will change questions in its Broker Interview Guide in relation to inquiries into a customer’s future financial circumstances, which will apply to all home and investment loan applications.

Key changes include: More detailed information required from customers who have stipulated a significant change to their future financial circumstances including the requirement for supporting documentation in some instances.

More detailed information required from customers who are approaching retirement including the requirement for supporting documentation in some instances.

The use of HEM may well be back in play, following the latest from the Westpac ASIC case. Given that at some banks HEM is still being used for around half of applications, and the Royal Commission commented specifically in the use of HEM, perhaps the law needs to be changed.

The core of the argument is whether the loans were unsuitable, and that it seems would depend of the ultimate progress of the loan subsequently. In other words, it cannot be proved to be unsuitable until it falls over. ASIC would need to prove the loan was unsuitable!

Actually we think the law says lenders have to verify expenses, and in other cases, for example in pay day lending specific inquiries are required as part of the assessment.

But its a clear as mud at the moment! When is unsuitable lending to be demonstrated. This will have a significant impact on any potential class actions. Expect bank share prices to rise!

A federal court has rejected a $35million fine for Westpac after it admitted breaking responsible lending laws, via MPA.

Last year the Australian Securities and Investments Commission (ASIC) began proceedings against Westpac in relation to its use of the Household Expenditure Measure (HEM) when assessing home loans.

ASIC argued the bank failed to conduct proper assessments to ascertain whether borrowers could afford to repay their loans.

The $35m penalty was a negotiated settlement between the two parties after it admitted to using the HEM to assess borrowers’ living costs.

ASIC alleged the bank approved around 50,000 home loans based on a HEM benchmark, even though expenses were presumably higher.

Among the explanations of the reasons behind the decision to refuse the penalty, Justice Nye Perram said the court had been asked to determine whether Westpac was in contravention of Section 128 of the National Consumer Credit Protection Act 2009.

Justice Perram said this section merely prohibits the making of a credit contract where an assessment has not been carried out. Regardless of the bank using the HEM benchmark, an assessment was in fact carried out.

Justice Perram also said that although both parties had agreed on the sum, “the theoretical maximum penalty is therefore either $1.1 million or $1.7 million per contravention” depending on the dates of contravention.

Justice Perram said because the parties could not agree on what contravened the section, it was difficult to “judge the appropriateness” of the $35m figure.

The corporate regulator has told the Hayne royal commission that it is at a loss over how to successfully prevent misconduct in financial services, via InvestorDaily.

The Australian Securities and Investments Commission has expressed in its submission that work had to be done to stop misconduct in the industry but there was not enough evidence as to how.

“There is unfortunately currently a dearth of knowledge and research as to what effectively deters misconduct across the range of corporate sectors and, in particular, the financial sector itself,” it reads.

ASIC recognised that it had a duty to force significant cultural change in the industry and said it would begin onsite supervision in major financial institutions.

However, ASIC rejected the interim reports idea that it did not go to court or issue civil penalties.

The Hayne Interim Report made claims that ASIC rarely went to court, seldom brought civil penalty proceedings and allowed entity’s to pay infringement notices with no admission.

ASIC said it was willing to change its enforcement practices but said it regularly undertook litigation against the financial sector.

“ASIC has litigated matters (through civil and criminal proceedings) twice as much as it has accepted enforceable undertakings,” ASIC’s report read.

ASIC also rejected the emphasis the interim report placed on its track record in the past decade against the major banks.

The interim report noted how ASIC had only issued commenced 10 civil proceedings against the major banks but 45 infringement notices to the major banks and accepted 13 enforceable undertakings.

ASIC said that the figures expressed in the report do not support the proposition that ASIC presently avoids compulsory enforcement action, nor do they reflect the full variety of enforcement tools made available to ASIC.

ASIC provided no comment on the interim reports findings that the commission had never brought proceedings against a licensee who failed to report a data breach.

“As at April 2018, ASIC had never brought, or sought to have the Commonwealth Director of Public Prosecutions (CDPP) bring, proceedings against a licensee for failing to comply with the 10 day time limit for breach reporting under Section 912D of the Corporations Act 2001 (Cth) (the Corporations Act), 21 despite affirming that it believed that entities frequently fail to comply with the section,” the report read.

The commission also provided no comment to the reports findings that it had never commenced proceedings against an entity for fees for no service.

“At 30 May 2018, ASIC had never commenced, or sought to have CDPP commence, proceedings under Section 12DI of the Australian Securities and Investments Commission Act 2001 (Cth) (the ASIC Act). This prohibits accepting payment for financial services when the payee does not intend to, or there are reasonable grounds to believe it cannot, supply the service,” it read.

Welcome to the Property Imperative weekly to 10th November 2018, our digest of the latest finance and property news with a distinctively Australian flavour.

Loads more data this week, all pointing to the impact that tighter credit conditions are having on the economy – that is unless you are the RBA, which seems to see everything as just fine and missing the debt bomb elephant in the room.

Watch the video, listen to the podcast or read the transcript.

And by the way you value the content we produce please do consider joining our Patreon programme, where you can support our ability to continue to make great content.

We start with the latest lending stats from the ABS. Further evidence of the lending slow down came through in spades in their housing finance statistics to September 2018. Looking at the trend flows first, new lending for owner occupation fell 1.7% compared with last month, to $13.78 billion. Investment lending flows fell 0.8%, to $8.96 billion, and owner occupied refinanced loans were flat at $6.24 billion. Refinanced loans as a proportion of all flows rose to 20.8% and we continue to see this sector of the market the main battleground for lenders who are trying to attract lower risk existing borrowers with keen rates. Investment loans, were 39.4% of all new loans, up again from last month as owner occupied lending demand eases.

Looking at all the categories of loans month on month, we see lending for owner occupied construction down 1.2%, lending for the purchase of new dwellings down 2.2%, lending for the purchase of other existing dwellings down 1.7%, while investment lending for the construction of new property fell 2.5%, investment property for individuals fell 0.6% and investment lending for other entities, such as self-managed super funds, dropped 2.2%. As a result, total flows were down 1.1% compared with last month.

First time buyers were also down in number in September, falling by 8.8% to 8,693 new loans. This was 18% of all loans, up from 17.8% last month. As we highlighted in our recent post “Mortgage Lending Enters the Danger Zone”, household debt is still rising, home prices are falling creating a negative wealth effect, and this will drive prices lower still.

Yet according to the RBA’s latest statement on Monetary policy, all is well, as they continue to paint a picture of underlying momentum in the economy based on jobs growth, low unemployment, and a prospect of wages growth, but still down the track. “GDP growth is running above 3 per cent. The unemployment rate has declined noticeably, reaching 5 per cent in the month of September. GDP growth is now expected to be around 3½ per cent on average over 2018 and 2019, but to ease in the latter part of the forecast period as production of some resource commodities stabilises at high levels”. They of course left the cash rate unchanged on Tuesday.

They are now forecasting an unemployment rate down to 4¾ per cent by the end of 2020. That would normally be a catalyst for wage rises, but we are not so sure that logic works any more given the international evidence, and the different employment structures (e.g. gig economy, part-time work, zero hours’ contracts etc.).

GDP was helped by strong terms of trade thanks to higher commodity prices. “Global energy demand has supported oil, liquefied natural gas (LNG) and thermal coal prices, while ongoing strong demand for steel in China and, increasingly, India, has supported the prices of iron ore and coking coal; supply disruptions have also boosted coking coal prices in recent quarters. But later they warn of a potential slow down.

They argue that the housing slowing down, which is apparent in most areas across the country is inconsequential, and the housing debt burden (high by any standards), is manageable. But we note the debt ratio is as high as ever it’s been, the household savings ratio is falling, and household wealth is declining thanks to falling prices now. This could well crimp consumption down the track. And that has supported GDP growth for years.

So overall, they say the positives outweigh the negatives, and the next few quarters are looking fine, but we believe there are a number of clouds on the horizon. These include further interest rate rises in the USA, flowing through to higher funding costs in Australia for many mortgage holders, the risks from China slowing, and possibility that wages growth will remain stuck in neutral. High household debt remains a significant burden. Yet they cannot see the elephant!

So whilst the RBA still suggest the cash rate may rise higher later, we think there is a significant chance they will have to cut further, to levels never seen before. Our read is there are significant risks in their outlook, and they are mostly on the downside. But then the RBA does have a habit of wearing rose-tinted glasses.

In fact, there is panic in the air as tightening credit spills over into falling home prices and potentially impacts the broader economy. Indeed, the AFR reported today that Treasurer Josh Frydenberg has urged banks to ease their lending clampdown for the public good as the government seeks to head off a royal commission-inspired credit crunch just as the housing market hits the skids. He expressed concern that lending across the board – for homebuyers, small business and borrowers – could tighten further after Commissioner Kenneth Hayne releases his final report by February 1.

The early reappointment of Australian Prudential Regulation Authority chairman Wayne Byres sends a message that is both poorly timed and off-key, given the important questions that have been raised by the royal commission. See out post “Shock Announcement Collapses Confidence And Trust In Australia’s Financial System”. Commissioner Ken Hayne’s interim report was so incendiary that it’s easy to forget it only covered the first two-thirds of the commission’s hearings.

The Reserve Bank of Australia and Treasury have also privately cautioned the Morrison government that any regulatory response to the financial services Royal Commission must be careful to avoid putting the brakes on lending to home buyers and business.

This is remarkable given the high debt ratios and mortgage stress, and is one of the “un-natural acts” we have been warning about. Let’s be clear, the Royal Commission has shone a light on poor practice, but APRA had already been applying belated pressure on the banks for loose lending, especially to investors and we have been in a long-term forced upswing thanks to poor Government policy, and weak supervision. This is now being pulled back, finally, but to BLAME the Royal Commission for this outcome is nonsense. It’s the same category as the exaggerated claims that Labor’s negative gearing reforms would hit existing investment property holders. It is just not true.

I discussed the underlying trends in the housing sector and why this is not just a bubble, but a structural crisis, in an interview I did with Alex Saunders from Nugget’s News. We explored the question of whether housing is in a bubble, micro-markets, and the expectations for the future trajectory of home prices given tighter lending conditions. And where might block chain fit in? You can watch the programme on YouTube.

I also discussed the latest results from our Mortgage Stress surveys. Having crossed the 1 million Rubicon last month, across Australia, more than 1,008,000 households are estimated to be now in mortgage stress (last month 1,003,000). This equates to 30.7% of owner occupied borrowing households. In addition, more than 22,000 of these are in severe stress. We estimate that more than 61,000 households risk 30-day default in the next 12 months. We continue to see the impact of flat wages growth, rising living costs and higher real mortgage rates. Bank losses are likely to rise a little ahead. We discussed these results in our post “October Mortgage Stress Update”.

It’s also worth noting that the ABS data this week on costs of living showed that many households seeing their costs rise way faster than the official CPI data. Most households would not be at all surprised.

We now know that the Royal Commission will be interrogating the major banks and the regulators in the final series of hearings, and there are some hard questions to be asked, about poor culture, behaviour standards and practice. Yet we noted that the 300 or so documents released this week from a range of players, are following “party lines”. The major banks are arguing in their submissions that no significant changes to structure or regulation are required, some of the smaller players argue they are at a competitive disadvantage thanks to the current industry structure and regulation and the mortgage broker sector argues that no significant changes are required to remuneration and conflict of interest rules. On the other hand, consumer groups stress the current issues of poor selling, advice and supervision.

And the submissions from the industry also lay bare more of the criminal activity, fraud, and worse, which has beset the sector. We still believe significant change is required, and you can watch our segment on this “Our Royal Commission Submission”. The regulators need a shake-up as well. So the question is, will the Royal Commissioner stand firm, or wilt under the pressure from so many stakeholders. I hope he can see the elephant in the room!

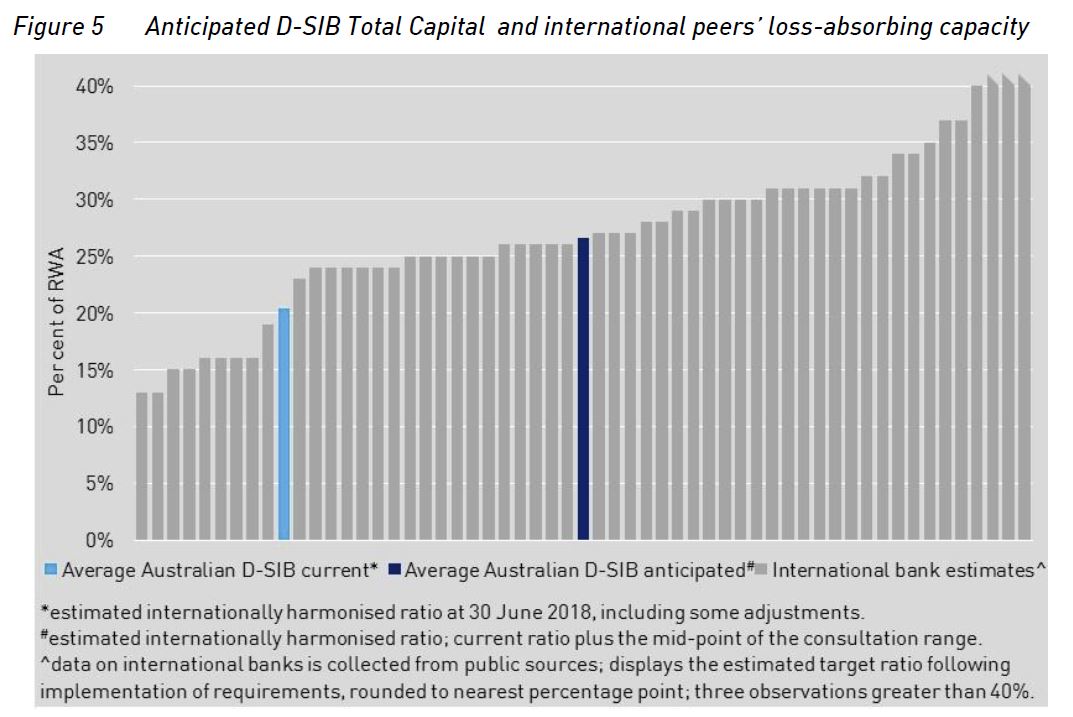

And talking of regulators, APRA released a paper this week on Loss-Absorbing Capacity of ADI’s. It shows that currently major Australian banks are at the lower end of Total Capital compared with international peers. As a result of proposed changes, major banks (Domestic systemically important banks in Australia, D-SIBs) will see their funding costs rise – incrementally over four years – by up to five basis points based on current pricing. This is intended to build in more financial resilience by lifting the capital requirements, centred on tier 2. Other banks may also be impacted to an extent.

If the D-SIBs were to maintain an additional four to five percentage points of Total Capital they would have ratios more in line with their international peers. But not in the top 25%, and the banks overseas are also lifting capital higher… so some tail chasing here! Is this “unquestionably strong”? “The aim of these proposals and resolution planning more broadly is to ensure that the failure of a financial institutions can be resolved in an orderly fashion, which protects the interests of beneficiaries and minimises disruption to the financial system,” APRA Chairman Mr Byres said. Written submissions are open to 8 February 2019.

The Bank reporting season revealed weaker profits, pressure on net interest margins, a rise in 90+ mortgage delinquencies, and more provisions for customer remediation. Yet, the banks managed to tweak their provisions to maintain capital levels. The earnings of Australia’s four major banks are likely to fall further in the near term due to slowing credit growth, especially in the residential mortgage segment, and further remediation and compliance costs associated with inquiries into the financial sector, including the Royal Commission, says Fitch Ratings. They said “Slower growth puts pressure on the banks to increase lending margins to maintain profitability. However, intense regulatory and public scrutiny of the sector, as well as strong competition, may make it difficult for the banks to reprice loans and pass on the recent increase in wholesale funding costs, as evidenced from the latest financial results. Net interest margins are therefore unlikely to improve in the short term”.

Jonathon Mott from UBS, one analyst I rate very highly, said: (1) ‘Underlying’ revenue fell -1.3% (h/h); (2) NIM was down 7bp to 199bp; (3) Average Interest Earning assets grew just 1.4% as the banks further tightened underwriting and continued to run off low yielding institutional assets; (4) Fee income and markets revenue were weaker; (5) ‘Underlying’ costs rose 1.9% (h/h) given ongoing investment, compliance and regulatory spend, which more than offset productivity savings; (6) This left ‘Underlying’ Pre-Provision Profits down 3.6% (h/h); (7) Credit impairment charges fell to just 11bp – the lowest ever recorded.

Oh and NAB this week finally moved to protect their Net Interest Margin, saying it would be changing the special offer on its base variable rate, available for new owner occupier principal and interest customers, from 3.69 per cent to 3.87 per cent. The change, which comes into effect from this Friday, November 9, reduces the discount on the advertised rate from 48 basis points to 30 basis points. It will only affect new customers taking out the product. The announcement comes nearly two months after the fourth-largest lender said it would not join the rest of the Big Four in raising mortgage rates in a bid to “rebuild trust” with customers.

So to property. Home prices are still falling according to the CoreLogic index, with year to date declines on average of 6.12% in Sydney, 4.79% in Melbourne and 3.5% in Perth. Brisbane is up 0.04% and Adelaide up 1.7% making a 5 capital average fall of 5%. In fact, the rate of decline appears to be accelerating.

Macquarie has joined the bearish view of home prices, saying they now expect national dwelling prices to fall for at least another 12 months, with a peak-to-trough correction of around 10 per cent. They expect prices in Sydney and Melbourne to fall by 15-20 per cent. They suggest it is a housing correction rather than being the result of a macro correction, in that falls have so far been orderly, with little evidence of distressed selling, even among investors affected by changes in prudential policy and lending standards. A disorderly housing price correction is unlikely, absent a major global economic downturn. They see declines, even a 20 per cent peak-to-trough decline would merely take prices back to April/May 2015 levels. They see no evidence of a severe credit curtailment, which is interesting. We do not agree.

The number of properties coming on the market continues to skyrocket, as more are forced to sell, or are confronted with the fear of not getting out, as the Sydney listings shows from Domain. There are more than 27,000 listed which seems to be some sort of record, our property Insider Edwin Almeida is tracking the results.

CoreLogic says the weighted average clearance rate saw further softening last week, with only 42.7 per cent of homes successful at auction. There were 1,541 auctions held across the combined capital cities, having decreased from the 2,928 auctions held over the week prior when a higher 47 per cent cleared. Both volumes and clearance rates continue to track lower each week when compared to the same period last year (2,046 auctions, 61.5 per cent).

In Melbourne, final results saw the clearance rate fall last week, with 45.7 per cent of the 266 auctions successful, down from the 48.6 per cent across a significantly higher 1,709 auctions over the week prior.

Across Sydney, the final auction clearance rate came in at 42.6 per cent across a slightly higher volume of auctions week-on-week, with 813 held, up from 798 the previous week when 45.3 per cent cleared. Sydney’s final clearance rate last week was not only the lowest seen this year, but the lowest the city has seen since December 2008.

The only capital city to see more than 50 per cent of auctions successful last week was Adelaide (50.8 per cent), however this was lower than the prior week’s 57.6 per cent. Brisbane saw the lowest clearance rate, with only 30 per cent of homes selling.

Geelong recorded the highest clearance rate of all the non-capital city regions, with 57.1 per cent of auctions reporting as successful, while the Sunshine Coast region had the highest volume of auctions (55).

This week, the number of auctions scheduled to take place across the combined capital cities is expected to rise, with 2,276 currently being tracked by CoreLogic, increasing from the 1,541 auctions held last week, although lower than results from one year ago (2,907). Across Melbourne, auction activity is expected to rise considerably after the slowdown seen preceding the Melbourne Cup festivities last week, with the city set to host 1,074 auctions this week, up from the 266 auctions held last week. In Sydney, 817 homes are scheduled to go to auction this week, increasing slightly from the 813 auctions held last week. Across the smaller auction markets, the number of homes scheduled for auction this week is lower than last week across all cities.

So to the markets, where the ASX 100 fell 0.09% on Friday to 4,874, whilst the ASX 200 Financials rose 0.23% to end at 5,911 and the local fear index rose 1.45% to 14.09.

AMP bumped along the bottom at 2.67, up 2.30 on Friday, ANZ moved up to 27.13, or 0.3%, the Bank of Queensland rose 0.61% to end at 9.92, while Bendigo and Adelaide Bank rose 0.57% to 10.55. CBA rose 0.47% on Friday to 70.95 while Mortgage Insurer Genworth was up 2.2% to 2.32. Macquarie recovered to 123.64 up 0.45%. National Australia Bank slid 0.12% to end the week at 24.90, Suncorp was up 0.64% to 14.08, and Westpac was up 0.07% to 27.70.

The Aussie, which reacted positively to the US mid-terms, ended the week at 72.25, but was down 0.44% on Friday. The Aussie Bitcoin rate was 8,566, down 0.54% and the Aussie Spot Gold fell 0.71% to 1,674.

Across to the US markets. U.S. stocks were lower after the close on Friday, as losses in the Technology, Basic Materials and Industrials sectors led shares lower. At the close in NYSE, the Dow Jones Industrial Average fell 0.77%, while the S&P 500 index fell 0.92% to 2,781, and the NASDAQ Composite index fell 1.65% to 7,407. The CBOE Volatility Index, which measures the implied volatility of S&P 500 options, was up 3.83% to 17.36. Gold Futures for December delivery was down 1.30% or 15.90 to $1210.30 a troy ounce. Elsewhere in commodities trading, Crude oil for delivery in December fell 1.37% or 0.83 to hit $59.84 a barrel. The US has just become the largest oil producer. Generally, a 20% drop from high close to low close defines a bear market. We are entering that territory!

Banks were off, with the S&P500 Financials down 0.93% to 449.49. On the whole, consumer discretionary stocks are slightly outpacing the S&P 500 since early October. The outlier might be Apple, which is actually a tech stock but obviously can have a huge impact on shopping season. The stock has made it back a bit after falling below $200 a share last week, but remains a long way from recent highs of around $230 as investors continue to debate what the company’s holiday quarter guidance and decision to stop reporting iPhone unit sales might mean moving forward. It ended at 204.5, though down 1.93 on the day.

A weakening Chinese economy helped affirm the bearish narrative of slower global growth. The FED kept the cash rate on hold, but the narrative confirms the view that further hikes are likely, with the 3-month bond rate flat at 2.36, and the 10-year rate back a little off its highs, down 1.44% to 3.19. The Fed said it expects “further, gradual increases” in rates as the economy continues to thrive. It’s a bit hard to understand any panic about these words, because they didn’t tell investors anything that most didn’t already know.

The European Commission tangled with Italy over the Italian government’s budget forecasts, which the EC said looked too optimistic on deficits. Moving west, debate raged about whether a Brexit deal might be getting close, and the U.K. government is holding meetings on the issue this weekend, media reports said. A Brexit breakthrough, if it comes, might give European markets a boost. But it’s unclear how close it might be. Deutsche Bank was down 1.75% on Friday to 8.97, and we are watching this as a bellwether for more trouble ahead.

Bitcoin was down 1.45% to 6,415.

So to conclude, the big debt question still remains the elephant in the room, and many are choosing to look past it, though as interest rates continue to push higher in the US, this will be harder to do. Locally, we expect more unnatural acts to try and keep the credit balloon in the air, but we believe that tighter standards are set to lurk in the shadows, meaning that the stage is set for more home price falls ahead.

Finally, a quick reminder, our next live Q&A session is now scheduled for November 20th at 8 pm Sydney time. You can schedule a reminder by using the YouTube Link and join in the live discussion, or send in questions beforehand. If previous sessions are any guide, it should be a lively event!

The earnings of Australia’s four major banks are likely to fall further in the near term due to slowing credit growth, especially in the residential mortgage segment, and further remediation and compliance costs associated with inquiries into the financial sector, including the Royal Commission, says Fitch Ratings. The banks reported an aggregate decline in profitability in their latest full-year results.

Slower growth puts pressure on the banks to increase lending margins to maintain profitability. However, intense regulatory and public scrutiny of the sector, as well as strong competition, may make it difficult for the banks to reprice loans and pass on the recent increase in wholesale funding costs, as evidenced from the latest financial results. Net interest margins are therefore unlikely to improve in the short term.

The major banks made provisions for client remediation costs during the last financial year in response to the initial findings from the Royal Commission. Fitch expects some remediation costs to flow into the 2019 financial year as the banks continue to investigate previous behaviour. Meanwhile, compliance and regulatory costs to address shortcomings are likely to rise, despite the banks simplifying their business and product offerings. The banks also remain susceptible to fines and class actions as a result of the banking system inquiries.

The four major banks – Australia and New Zealand Banking Group (ANZ, AA-/Stable/aa-), Commonwealth Bank of Australia (CBA, AA-/Negative/aa-), National Australia Bank (NAB, AA-/Stable/aa-) and Westpac Banking Corporation (Westpac, AA-/Stable/aa-) – reported aggregated statutory full-year profit of AUD29.4 billion, a decrease of 0.8% from a year earlier, while cash net profit was down by 6.5%. CBA’s financial year ended June 2018, while ANZ’s, NAB’s and Westpac’s ended September 2018. The drop in aggregate profit was driven by slower lending growth, customer remediation charges and higher funding costs, especially in the second half of the financial year, as expected by Fitch. These pressures were partly offset by a benign operating environment that limited impairment expenses across the board.

All four banks reported lower or steady loan impairment charges during the reporting period. However, 90-day-plus past-due loans increased slightly, reflective of pressure on household finances from sluggish wage growth. Impairments are likely to rise from current historical lows due to the cooling housing market and high household leverage, which make households more susceptible to shocks from higher interest rates and unemployment. The ongoing tightening of banks’ risk appetites and underwriting standards should, however, support asset quality in the long term.

Common equity Tier 1 (CET1) ratios are broadly in line with the 10.5% threshold that regulators define as “unquestionably strong”. Banks have to achieve this level by 1 January 2020. ANZ reported a CET1 ratio of 11.4%, the highest of the major banks. ANZ is undertaking a share buyback and is likely to announce further capital management plans once it has received proceeds from recent divestments and asset sales. Westpac recorded a CET1 ratio of 10.6% and therefore already meets the new minimum requirement ahead of the deadline.

CBA reported a CET1 ratio of 10.1% at June 2018, which incorporates the AUD1 billion additional operational risk charge put in place following an independent prudential inquiry published in May 2018. However, this will translate to a pro forma CET1 ratio of 10.7% after already-announced divestments. NAB’s CET1 ratio is 10.2%, but we expect it to meet the 2020 deadline, with its capital position likely to be supported by an announced discounted dividend reinvestment plan and the potential sale of its MLC wealth-management business.

ASIC says the Federal Court of Australia today ordered Westpac Banking Corporation (Westpac) pay a pecuniary penalty of $3.3 million for contravening s12CC of the Australian Securities and Investments Commission Act 2001 (Cth) (ASIC Act) through its involvement in setting BBSW in 2010.

In reasons for making the pecuniary penalty order, Justice Beach noted the legislative constraint he had in imposing the order,

‘If I had been permitted to do so I would have imposed a penalty of at least one order of magnitude above $3.3 million in order to discharge [the objectives of specific and general deterrence]. But I am not free do so.‘

Justice Beach concluded in his reasons,

‘Westpac’s misconduct was serious and unacceptable…Westpac has not shown the contrition of the other banks. Moreover, imposing the maximum penalty is the only step available to me to achieve specific and general deterrence. The message that should be sent is that if you manipulate or attempt to manipulate key benchmark rates you are likely to have the maximum penalty imposed, whatever that is from time to time.‘

The Court also ordered that an independent expert agreed between ASIC and Westpac be appointed to review whether Westpac’s current systems, policies and procedures are appropriate, and to report back to ASIC within 9 months.

It was also ordered that Westpac pay ASIC’s costs of and incidental to the penalty hearing as agreed and assessed.

Today’s court orders follow Justice Beach’s judgment, delivered on 24 May 2018, which found that Westpac on 4 dates in 2010 traded with a dominant purpose of influencing yields of traded Prime Bank Bills and where BBSW set in a way that was favourable to its rate set exposure. His Honour held that this was unconscionable conduct in contravention of s12CC of the ASIC Act.

His Honour also found in his 24 May 2018 judgment that Westpac had inadequate procedures and training and contravened its financial services licensee obligations under s912A(1)(a), (c), (ca) and (f) of the Corporations Act 2001 (Cth).

ASIC Commissioner Cathie Armour welcomed today’s decision and noted that ‘ASIC brought this litigation to hold the major banks to account for their unacceptable conduct, and to test the scope of the law in combating benchmark manipulation. ASIC actions have led to these successful court outcomes, and also contributed to new benchmark manipulation offences being enacted by Parliament, and the calculation method and administration of the BBSW being radically overhauled.’

On 5 April 2016 ASIC commenced civil penalty proceedings in the Federal Court against Westpac, alleging in the period between 6 April 2010 and 6 June 2012 (inclusive) it traded in a manner that was unconscionable and created an artificial price and a false appearance with respect to the market for certain financial products that were priced or valued off BBSW.

This mirrored proceedings brought in the Federal Court against the Australia and New Zealand Banking Group (ANZ) on 4 March 2016 (refer: 16-060MR), against National Australia Bank (NAB) on 7 June 2016 (refer: 16-183MR) and Commonwealth Bank of Australia (CBA) on 30 January 2018 (refer:18-024MR).

On 10 November 2017, the Federal Court made declarations that each of ANZ and NAB had attempted to engage in unconscionable conduct in attempting to seek to change where the BBSW set on certain dates and that each bank failed to do all things necessary to ensure that they provided financial services honestly and fairly. The Federal Court imposed pecuniary penalties of $10 million on each bank.

On 20 November 2017, ASIC accepted enforceable undertakings from ANZ and NAB which provides for both banks to take certain steps and to pay $20 million to be applied to the benefit of the community, and that each will pay $20 million towards ASIC’s investigation and other costs (refer: 17-393MR).

On 21 June 2018, the Federal Court in Melbourne imposed pecuniary penalties totalling $5 million on CBA for attempting to engage in unconscionable conduct in relation to BBSW. CBA admitted to attempting to seek to change where BBSW set on five occasions in the period 31 January 2012 to 15 June 2012.

On 11 July 2018 ASIC accepted a court enforceable undertaking to address its BBSW conduct which provides for CBA will pay $15 million to be applied to the benefit of the community and $5 million towards ASIC’s investigation and legal costs (refer: 18-210MR).

In July 2015, ASIC published Report 440, which addresses the potential manipulation of financial benchmarks and related conduct issues.

The Government has recently introduced legislation to implement financial benchmark regulatory reform and ASIC has consulted on proposed financial benchmark rules.

On 21 May 2018, the new BBSW methodology commenced (refer: 18-144MR). The new BBSW methodology calculates the benchmark directly from market transactions during a longer rate-set window and involves a larger number of participants. This means that the benchmark is anchored to real transactions at traded prices.

The latest batches of documents released by the Royal Commission into Financial Services Misconduct included a litany of poor or illegal behaviour across the broker groups. This included detailed incidents of falsifying documents and fraud, plus sexual harassment, offensive behaviour and homophobia based on 215 newly released documents from 94 groups. We can conclude this is way more than “just a few bad apples”.

While most, if not all, broker groups detailed incidents of falsifying documents and fraud, it has been revealed some of the behaviour at Aussie Home Loans included sexual harassment, offensive behaviour and homophobia.

The group has said it will continue to support reporting of such unacceptable behaviour as it to enforces a zero-tolerance policy.

When the Royal Commission into banking misconduct was first established, Commissioner Kenneth Hayne asked financial entities to provide information on misconduct or conduct falling below community standards over the last ten years.

While the incidents listed in the reports were to be the basis for many of the hearings during the Royal Commission, these 215 newly released documents from 94 groups paint a much broader picture.

Looking exclusively at submissions from broker groups, misconduct was listed alongside any action taken and subsequent outcome.

AFG submitted 12 items detailing incidents, which included brokers providing false documents, making administrative errors, breaching the privacy of clients, failing to comply with NCCP obligations and creating false approval letters.

Loan Market also made a submission which detailed 33 incidents of misconduct. Incidents included creating false documents, tampering with documentation, inappropriate use of social media, overstated consumer income and copying and pasting signatures.

Mortgage Choice has listed ten incidents including more than one case of falsifying signatures, providing false loan approval letters, misstating customer financial positions and falsifying documents. The broker group also listed three cases of failing to produce a Statement of Advice to customers.

Smartline listed incidents of altered valuation reports, failure to make reasonable enquiries about a customer’s financial circumstances and inaccurate information on loan applications.

The mortgage group also included an incident where a borrower’s credit card was allegedly fraudulently obtained and used, which at the time of submission was subject to a NSW police investigation.

It also detailed an “isolated incident” relating to theft from a customer and ended with the broker’s licence being revoked and the sale of their franchise.

Yellow Brick Road’s submission also included details of fraud and false documents. In one case a Vow Financial broker was accused of fraudulently gaining access to customer bank accounts and transferring funds.

Commonwealth Bank’s submission included details of behaviour at Aussie Home Loans. It includes details of “offensive or otherwise unprofessional behaviour” directed at employees and/or brokers.

Out of 182 total incidents, there were 29 listed as misconduct relating to false documents and/or declarations and/or misleading information.

There were 19 incidents listed in relation to NCCP breaches, including lack of reasonable care, failing to make the right enquiries and encouraging customers not to disclose the purpose of the loan.

The remaining incidents included, but were not limited, to:

Sexual harassment at a work event, and sexual harassment outside of work

Using Aussie’s IT system to send “emails containing objection material which could cause offense to a reasonable adult”

Accessing customer’s personal details

Numerous counts of unprofessional language and tone

Pretending to be the customer

Mutiple examples of ex-brokers using confidential information to contact former customers

Disclosing customer details to other parties

“Unprofessional conduct by making veiled threats to customer’s solicitor and allegedly impersonated someone else”

Customers experiencing homophobia

Derogatory and discriminatory comments

Alleged abuse of female in car park by a retail store broker and issue disclosed on Facebook

Attending a licenced venue “on a regular basis” and returning to work visibly drunk

Gaining access to an Aussie office after a work event, theft and assault

Inappropriate sexual language with fellow employee

Bullying by senior executives

A spokesperson from Aussie Home Loans said, “Media reports of submissions to the Royal Commission cited isolated incidents of unacceptable conduct involving staff and contractors over a ten year period.

“Aussie provided the Royal Commission a detailed and exhaustive table of incidents as a result of building a culture of actively encouraging and facilitating staff, contractors and customers to speak up and report unacceptable conduct.

“In each and every case of unacceptable conduct, Aussie took appropriate and swift disciplinary action, which included termination of employment and contractor agreements.

“Aussie will continue to actively encourage reporting of unacceptable conduct, to enforce its zero-tolerance policy for such conduct and to enhance its systems and process to prevent, detect and deter such conduct.”

This week the Royal Commission into Misconduct in the Banking, Superannuation and Financial Services Industry published all of the initial submissions from organisations from across the sector, via InvestorDaily.

Prior to the commencement of the public hearings, a number of entities were asked to provide the commission with information concerning instances of misconduct or conduct falling below community standards and expectations that the entity had identified in the past 10 years.

Commonwealth Bank of Australia (CBA)

CBA named 15 former employees who have been banned by ASIC since 2011. All of them were either Commonwealth Financial Planning (CFP) employees or operated under Financial Wisdom Limited (FWL).

The most recent case involved the banning of adviser Kimberley Holgate earlier this year.

CBA explained that the former CFP employee was banned for five years for engaging in conduct that was Holgate likely to mislead by cutting clients’ signatures from documents held on file and pasting them onto new documents.

The bank also noted that the adviser was “not acting in the best interests of her clients when advising they rollover their existing super to a new product issued by CFSIL; not acting in the best interests of her clients by advising them to cancel existing insurance policies and apply for personal insurance issued by Comm Insure; and failing to prioritise the interests of her clients when advising them to acquire financial products which entitled her, her employer and its related entities to a financial benefit.”

In the period since 1 January 2008, CBA identified 15 adverse findings against the group.

Australia and New Zealand Bank (ANZ)

Meanwhile, ANZ admitted to the royal commission that 18 financial advisers falsified customer or compliance documents over the period and had deliberately overcharged fees.

“A number of different factors caused or contributed to the improper or non-compliant conduct of advisers, including the failure of ANZ’s processes, controls and supervision to protect against that conduct,” the bank said.

National Australia Bank (NAB)

NAB’s submission detailed extensive misconduct across its lending and advice divisions over the last decade, including a number of incidents relating to the misuse of customer funds.

“Some of the conduct was or is being investigated by the Victorian Police and ASIC,” NAB said.

“One financial adviser was convicted and sentenced to imprisonment. The financial adviser has appealed the sentence.”

Despite a plethora of examples of misconduct since 2008, NAB does not consider much of the conduct to be attributable to any particular “group culture”.

Westpac Banking Corporation

Westpac identified significant misconduct across its mortgages business, including bankers forging supporting documentation and customer incomes.

In November 2015, Westpac identified incidents of staff engaging in conduct to simulate the creation and activation of new accounts to artificially inflate metrics used to calculate their variable rewards.

“In particular, the conduct involved simulating the deposits and withdrawals of $50 to suggest that accounts were ‘active’. An internal investigation identified a number of instances of simulated account funding between January 2013 and December 2016, which resulted in the termination of a number of staff together with other disciplinary measures,” the bank admitted.

HSBC Australia

HSBC Australia detailed more than 20 examples of misconduct over the last 10 years, including a number of instances where branch staff stole money from customer accounts.

Over a number of weeks in late 2009 and early 2010, a staff member at an HSBC Australia branch allegedly made unauthorised use of a customer’s replacement bank card, withdrawing a total of $22,880. An internal investigation revealed a number of recurring breaches of HSBC Australia’s security procedures at the branch concerned, involving two further staff members.

“The employment of all three staff members was terminated for security breaches and the customer reimbursed. Other staff at the branch received supplementary training in security procedures,” HSBC confirmed.

In October 2009, a staff member spent $6,000 using a customer’s credit card. Following an internal HSBC Australia inquiry, HSBC Australia reimbursed the customer’s credit card and the staff member left HSBC Australia.

Between June 2011 and June 2017, a staff member at an HSBC Australia branch in Sydney misappropriated $913,115 from the accounts of eight customers. The bank discovered the conduct in July 2017 after an affected customer disputed a transaction and, following an internal investigation, HSBC Australia reported it to the NSW Police and ASIC.

“HSBC Australia continues to support the police investigation. All customers other than three have been reimbursed,” the bank said, adding that it is working to contact two of those customers, both of whom are foreign nationals and one of whom is presumed dead.

“The third has been contacted numerous times but is yet to provide details to allow return of funds. In the meantime, the money has been placed in holding accounts. The staff member’s employment was terminated consistent with the Consequence Management Framework.”

Finance Brokers Association of Australia (FBAA) has lodged its response to the royal commission’s interim report, arguing that brokers should not be “forced into even more documentary disclosure” regarding commissions and reiterating its support of the current remuneration structure, via The Adviser.

The interim report from the Royal Commission into Misconduct in the Banking, Superannuation and Financial Services Industry was released at the end of September, raising a swathe of questions regarding the mortgage broking industry.

In the report, the commission questioned some aspects of broker remuneration (including the perceived conflicts of upfront and trail commissions based on loan value and the now largely defunct volume-based commissions), outlined that there was “no simple legal answer” for explaining whom an intermediary (such as a broker) acts for, and questioned the need for a new duty on brokers.

“[I]t will be important to consider whether value and volume-based remuneration of intermediaries should be forbidden,” the commissioner wrote in his report, outlining findings from ASIC’s remuneration review that found that broker loans are marginally larger and have slightly higher loan-to-value ratios (LVRs).

While the full responses to the financial services royal commission have not yet been officially released, the Finance Brokers Association of Australia (FBAA) has revealed that it has tabled a “substantive submission” focusing on disclosure obligations, remuneration structures, compliance with existing laws, and the commission’s call for greater regulation.

Speaking of the association’s submission, FBAA managing director Peter White warned of any wholesale changes to the current broker remuneration model, arguing that major change may be detrimental to the industry.

“We are concerned that a change to the existing structure without fully understanding the impact of any proposed model may simply disrupt a stable and important profession with no corresponding improvement,” Mr White said.

“The majority of misconduct has been due to market participants failing to follow existing laws. This shows that further reforms should not be contemplated until there is compliance with current laws.”

The FBAA also said that its submission disputes claims that lenders paying value-based upfront and trail commissions could be a possible breach of the National Consumer Credit Protection Act (NCCP).

“The relevant section does not prohibit conflicts of interest, only those causing disadvantage, yet the term disadvantage is imperfect and can’t be relied on. It’s our submission that the laws already in place strike an appropriate balance,” Mr White said.

Touching on remuneration disclosure to brokers, the FBAA emphasised that brokers already provide “lengthy disclosure documents”, while the NCCP Act ensures that clients are well informed about the costs and commissions.

“We don’t want brokers to be forced into even more documentary disclosure and that view accords with ASIC’s findings that consumers can disengage because of information overload,” Mr White said.

The managing director of the FBAA concluded that that while the association agrees with the commission’s interim report that improvements could be made, he “agreed” that new laws or regulations are not necessarily the answer.

“Some of the responses to the royal commission have verged on emotional or value proposition statements, and while most have merit, we have deliberately taken a strong legal approach to our language to ensure our messages are clearly understood by the commissioner, a High Court Judge,” Mr White said.

The seventh round of hearings for the final round of the financial services royal commission will be held at the Lionel Bowen Building in Sydney from 19 to 23 November and at the Commonwealth Law Courts Building in Melbourne from 26 to 30 November.

The hearings will focus on “causes of misconduct and conduct falling below community standards and expectations by financial services entities (including culture, governance, remuneration and risk management practices), and on possible responses, including regulatory reform”.

It is expected that the seventh round will be the final round of the financial services royal commission, unless Commissioner Hayne requests, and is granted, an extension.

Commissioner Kenneth Hayne is expected to release his final report, which will include the topics of the fifth, sixth and seventh rounds of hearings (focusing on superannuation, insurance and “policy questions arising from the first six rounds”, respectively) by 1 February 2019.

It shows that currently major Australian banks are at the lower end of Total Capital compared with international peers. As a result of proposed changes, major banks (Domestic systemically important banks in Australia, D-SIBs) will see their funding costs rise – incrementally over four years – by up to five basis points based on current pricing. This is intended to build in more financial resilience by lifting the capital requirements, centred on tier 2. Other banks may also be impacted to an extent.

If the D-SIBs were to maintain an additional four to five percentage points of Total Capital they would have ratios more in line with their international peers. But not in the top 25%, and the banks overseas are also lifting capital higher… so some tail chasing here! Is this “unquestionably strong”?

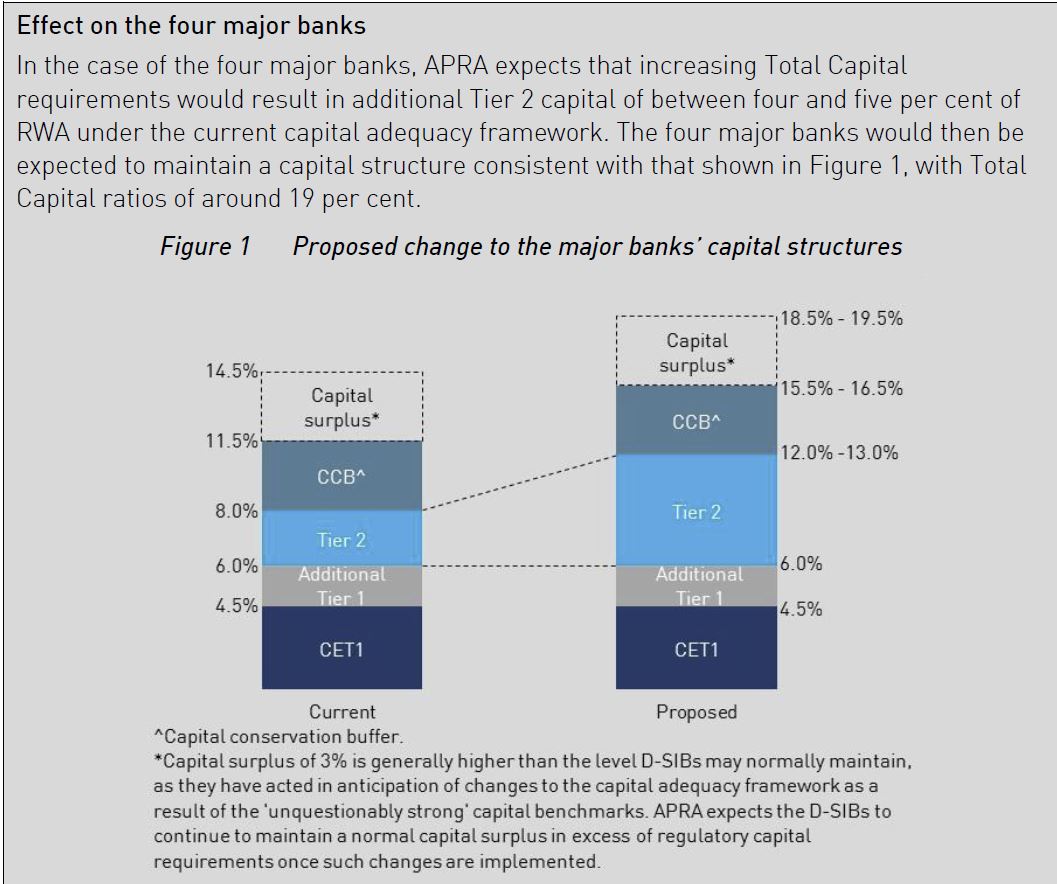

Under the proposals, each D-SIB would be required to maintain additional loss absorbency of between four and five percentage points of RWA. It is anticipated that each D-SIB’s Total Capital requirement would be adjusted by the same amount.

By way of background, the Australian Government’s 2014 Financial System Inquiry (FSI) recommended APRA implement a framework for loss absorbing and recapitalisation capacity in line with emerging international practice, sufficient to facilitate the orderly resolution of Australian ADIs and minimise taxpayer support (FSI Rec 3). The Government supported this recommendation in its response to the FSI.

APRA’s role is not to eliminate failure altogether, but to reduce its probability and impact. This role is set out in APRA’s statutory objectives under the Australian Prudential Regulation Authority Act 1998 and the Banking Act 1959, which require APRA to protect depositors and pursue financial system stability. In performing its functions, APRA will balance those objectives with the need for efficiency, competition, contestability and competitive neutrality in the financial system.

Disorderly failures are inconsistent with APRA’s objectives, as they are highly disruptive to depositors and have an adverse impact on financial system stability. Australia has not experienced a disorderly ADI failure in recent history, though the failure of HIH Insurance Limited (HIH) in 2001 provides an example of the adverse consequences of a disorderly failure of an APRA-regulated institution. In that instance, policyholders were severely affected and essential insurance services to the broader community became unavailable for a period of time.

Conversely, orderly resolution of an ADI would occur when a problem is identified and escalated early enough to allow APRA and other financial regulators to manage and respond in a manner that protects the interests of depositors, stabilises the ADI’s critical functions and promotes financial stability. Achieving an orderly resolution does not necessarily mean a crisis is averted, rather the manner in which an ADI’s failure is managed would result in better outcomes given the circumstances.

APRA’s statutory powers were recently strengthened by the passage of the Financial Sector Legislation Amendment (Crisis Resolution Powers and Other Measures) Act 2018.

The effectiveness of resolution planning will be a focus for APRA over the coming years. APRA is in the process of developing a formalised framework for resolution planning and will consult further on this in 2019.

The proposals in this discussion paper focus on the availability of financial resources to support orderly resolution.

These proposals would ensure ADIs have adequate financial resources available to support orderly resolution in the highly unlikely event of failure. This will be achieved by adjusting, where appropriate, an ADI’s Total Capital requirement.

These proposals are distinct from APRA’s work on ensuring ADI capital levels are ‘unquestionably strong’, which relates to the ongoing resilience of institutions and is in response to a separate FSI recommendation (FSI Rec 1).

APRA is proposing an approach on loss-absorbing capacity that is simple, flexible and designed with the distinctive features of the Australian financial system in mind, and has been developed in collaboration with the other members of the Council of Financial Regulators. The key features of the proposals include:

for the four major banks – increasing Total Capital requirements by four to five percentage points of risk-weighted assets

for other ADIs – likely no adjustment, although a small number may be required to maintain additional Total Capital depending on the outcome of resolution planning, which would inform the appropriate amount of additional loss absorbency required to achieve orderly resolution. This assessment would occur on an institution-by-institution basis.

Tier 2 capital instruments are designed to convert to ordinary shares or be written off at the point of non-viability, which means they will be available to absorb losses and can be used to facilitate resolution actions. Tier 2 capital instruments have been a feature of ADI capital structures in various forms since being introduced as part of the 1988 Basel Accord. These instruments have been used as part of resolution actions in other jurisdictions, supporting orderly outcomes.

It is also important that holders of instruments which are intended to be converted or written off in resolution understand the distinctive risks of these investments. In the context of AT1 instruments, APRA has noted that it is inadvisable for investors to view such instruments as higher-yielding fixed-interest investments, without understanding the loss-absorbing role they play in a resolution.15 In the case of the Australian ADIs’ Tier 2 capital instruments, these are mostly issued to institutional investors, who are likely to understand the risks involved.

As ADIs will be able to use any form of capital to meet increased Total Capital requirements, APRA anticipates the bulk of additional capital raised will be in the form of Tier 2 capital. The proposed changes are expected to marginally increase each major bank’s cost of funding – incrementally over four years – by up to five basis points based on current pricing. This is not expected to have an immediate or material effect on lending rates.

APRA proposes that the increased requirements will take full effect from 2023, following relevant ADIs being notified of adjustments to Total Capital requirements from 2019.

In addition to the proposals outlined in this discussion paper, APRA intends to consult on a framework for recovery and resolution in 2019, which will include further details on resolution planning.

APRA Chairman Wayne Byres said one of APRA’s core functions as Australia’s prudential regulator is to plan for, and if required, execute the orderly resolution of the financial institutions it regulates.

“The resilience of the Australian banking system continues to improve, underpinned by the build-up of capital over the last decade.

“However, no matter how resilient financial institutions are, the possibility of failure cannot be entirely removed. Therefore, in addition to strengthening the resilience of the financial system, it is prudent to plan for the unlikely event of failure.

“The events of the global financial crisis demonstrated the impact that failures can have on the broader financial system and the subsequent social and economic consequences.

“The aim of these proposals and resolution planning more broadly is to ensure that the failure of a financial institutions can be resolved in an orderly fashion, which protects the interests of beneficiaries and minimises disruption to the financial system,” Mr Byres said.