The latest minutes from the RBA continues the steady-as-we-go story, once again and so the cash rate remains on hold.

At its meeting today, the Board decided to leave the cash rate unchanged at 1.50 per cent.

The global economic expansion is continuing. A number of advanced economies are growing at an above-trend rate and unemployment rates are low. Growth in China has slowed a little, with the authorities easing policy while continuing to pay close attention to the risks in the financial sector. Globally, inflation remains low, although it has increased due to both higher oil prices and some lift in wages growth. A further pick-up in inflation is expected given the tight labour markets and, in the United States, the sizeable fiscal stimulus. One ongoing uncertainty regarding the global outlook stems from the direction of international trade policy in the United States.

Financial conditions in the advanced economies remain expansionary but have tightened somewhat recently. Equity prices have declined and yields on government bonds in some economies have increased, although they remain low. There has also been a broad-based appreciation of the US dollar this year. In Australia, money-market interest rates have declined recently, after increasing earlier in the year. Standard variable mortgage rates are a little higher than a few months ago and the rates charged to new borrowers for housing are generally lower than for outstanding loans.

The Australian economy is performing well. Over the past year, GDP increased by 3.4 per cent and the unemployment rate declined to 5 per cent, the lowest in six years. The forecasts for economic growth in 2018 and 2019 have been revised up a little. The central scenario is for GDP growth to average around 3½ per cent over these two years, before slowing in 2020 due to slower growth in exports of resources. Business conditions are positive and non-mining business investment is expected to increase. Higher levels of public infrastructure investment are also supporting the economy, as is growth in resource exports. One continuing source of uncertainty is the outlook for household consumption. Growth in household income remains low, debt levels are high and some asset prices have declined. The drought has led to difficult conditions in parts of the farm sector.

Australia’s terms of trade have increased over the past couple of years and have been stronger than earlier expected. This has helped boost national income. While the terms of trade are expected to decline over time, they are likely to stay at a relatively high level. The Australian dollar remains within the range that it has been in over the past two years on a trade-weighted basis, although it is currently in the lower part of that range.

The outlook for the labour market remains positive. With the economy growing above trend, a further reduction in the unemployment rate is expected to around 4¾ per cent in 2020. The vacancy rate is high and there are reports of skills shortages in some areas. Wages growth remains low, although it has picked up a little. The improvement in the economy should see some further lift in wages growth over time, although this is still expected to be a gradual process.

Inflation remains low and stable. Over the past year, CPI inflation was 1.9 per cent and, in underlying terms, inflation was 1¾ per cent. These outcomes were in line with the Bank’s expectations and were influenced by declines in some administered prices due to changes in government policies. Inflation is expected to pick up over the next couple of years, with the pick-up likely to be gradual. The central scenario is for inflation to be 2¼ per cent in 2019 and a bit higher in the following year.

Conditions in the Sydney and Melbourne housing markets have continued to ease and nationwide measures of rent inflation remain low. Growth in credit extended to owner-occupiers has eased but remains robust, while demand by investors has slowed noticeably as the dynamics of the housing market have changed. Credit conditions are tighter than they have been for some time, although mortgage rates remain low and there is strong competition for borrowers of high credit quality.

The low level of interest rates is continuing to support the Australian economy. Further progress in reducing unemployment and having inflation return to target is expected, although this progress is likely to be gradual. Taking account of the available information, the Board judged that holding the stance of monetary policy unchanged at this meeting would be consistent with sustainable growth in the economy and achieving the inflation target over time.

The upcoming round of public hearings for the financial services royal commission will focus on misconduct and conduct falling below community expectations as well as possible regulatory reform, via The Adviser.

The seventh round of hearings for the final round of the Royal Commission into Misconduct in the Banking, Superannuation and Financial Services Industry (RC) will be held at the Lionel Bowen Building in Sydney from 19 to 23 November and at the Commonwealth Law Courts Building in Melbourne from 26 to 30 November.

Following on from the six previous rounds (which focused on consumer lending practices; financial advice; SME loans; issues affecting Australians who live in remote and regional communities; and insurance, respectively), it has now been revealed that the seventh round of hearings will focus on “causes of misconduct and conduct falling below community standards and expectations by financial services entities (including culture, governance, remuneration and risk management practices), and on possible responses, including regulatory reform”.

The royal commission had previously stated that the seventh round would focus on “policy questions arising from the first six rounds”.

In an update, the royal commission revealed that the purpose of round seven is “to provide the commissioner with an opportunity to explore with senior executives from certain financial services entities, and the regulators of those entities, some of the policy issues identified in the interim report, and following rounds five and six of the public hearings”.

The hearings will also consider the role of the Australian Securities and investments Commission (ASIC) and the Australian Prudential Regulation Authority (APRA) in “supervising the actions of financial services entities, deterring misconduct by those entities, and taking action when misconduct may have occurred”.

According to an update from the RC, the hearings will include all four major banks (Australia and New Zealand Banking Group Limited, the Commonwealth Bank of Australia, National Australia Bank Limited and Westpac Banking Corporation) as well as AMP Ltd, Bendigo and Adelaide Bank Ltd, Macquarie Group Ltd, and ASIC and APRA.

However, the commission has said that further entities may be included before the hearings commence.

Due to the “different nature” of this next round of hearings, the RC has said that there will be no process for applications for leave to appear for this round of hearings.

Instead, a person who is summoned to give evidence before the commission may be represented by a legal representative at the hearing without the need for that representative to obtain separate authorisation, the commission revealed.

It is expected that the procedure for the next round of hearings will see the counsel assisting the commission lead and ask questions of all witnesses, after which the legal representative for the witness may ask questions of the witness (limited to matters arising out of the questions asked by counsel assisting, unless given leave to ask questions beyond those matters). The counsel assisting the commission may then re-examine the witness. Cross-examination of witnesses by other persons or entities will not be permitted.

The commission has further revealed that the commission is now “considering” the public submissions received relating to the interim report and rounds five and six, adding that “they will inform the matters that the commissioner seeks to explore during round seven”.

There will be no process for further submissions to be lodged following the conclusion of round seven.

It is expected that the seventh round will be the final round of the financial services royal commission, unless Commissioner Hayne requests, and is granted, an extension.

Commissioner Kenneth Hayne is expected to release his final report, which will include the topics of the fifth, sixth and seventh rounds of hearings (focusing on superannuation, insurance and “policy questions arising from the first six rounds”, respectively) by 1 February 2019.

PEXA, Australia’s online property exchange, which assists members such as lawyer, conveyancers and financial institutions to lodge documents with Land Registries and complete financial settlements electronically, has been acquired by via a joint bid from Link Administration Holdings Limited, Morgan Stanley Infrastructure Partners and Commonwealth Bank (who is already a key stakeholder in the venture).

States across Australia have been moving across to the platform as the country aims for loans to become 100% digital.

CBA chief executive officer Matt Comyn said, “Having been a key stakeholder in PEXA since its inception in 2011, today’s announcement represents our continued commitment to support the property industry as it transitions towards an innovative, fully digital, settlements process that aims to provide improved experiences for customers.”

CBA also said the transaction aligns with its strategy to focus on its core banking businesses and to create a simpler, better bank for our customers. As part of the transaction, which is subject to a number of conditions precedent, CBA will invest a further $50 million, totalling approximately $100 million invested in PEXA to date. This will result in an increase in our ownership stake from 13.1% to approximately 16%.

No one seems to have noticed that one of the largest mortgage lenders is now also has a significant interest in the property settlement and transfer system – what could possibly go wrong?

The government has announced that it will boost APRA’s funding by $58.7m and extend the appointment of its chair Wayne Byres despite the criticism the regulator copped from the royal commission, via MPA.

“The new funding will allow APRA to reinforce the resilience and soundness of our financial system at a time of significant reform,” Treasurer Josh Frydenberg said in a statement.

Besides supervising several industries, APRA’s current agenda includes the implementation of the new Banking Executive Accountability Regime (BEAR) and monitoring and targeting issues in the housing market to retain stability, which it previously dealt with by introducing speedbumps on interest-only and investor lending.

The new funding will be provided over four years to enhance APRA’s supervision across regulated industries and its ability to identify and address new and emerging risk areas, such as cyber, fintech and culture. It will also allow APRA improve its data collection capabilities and provide for a review of its enforcement strategy.

Frydenberg said Byres’ reappointment as chair for another five years was “important for stability during this time of significant reform in Australia’s financial system”.

In the royal commission’s interim report, however, it asked whether the regulatory architecture needed to be changed, and questioned whether APRA’s regulatory and enforcement practices were satisfactory.

“APRA is obliged to look at issues of governance and risk culture through the lens of financial system stability. Understood in that light, APRA’s lack of action in response to the widespread occurrence of the conduct described in this report may, perhaps, be more readily understood,” the report said.

But, the commission said that didn’t excuse APRA from not taking any steps to identify the major banks’ deficiencies in governance and culture as they became increasingly apparent.

“Regulatory complexity increases pressure on the regulator’s resources and may allow entities to develop cultures and practices that are unfavourable to compliance,” the commission wrote.

Prior to this latest funding injection, APRA’s estimated budget for 2018-19 was $682m, according to the royal commission

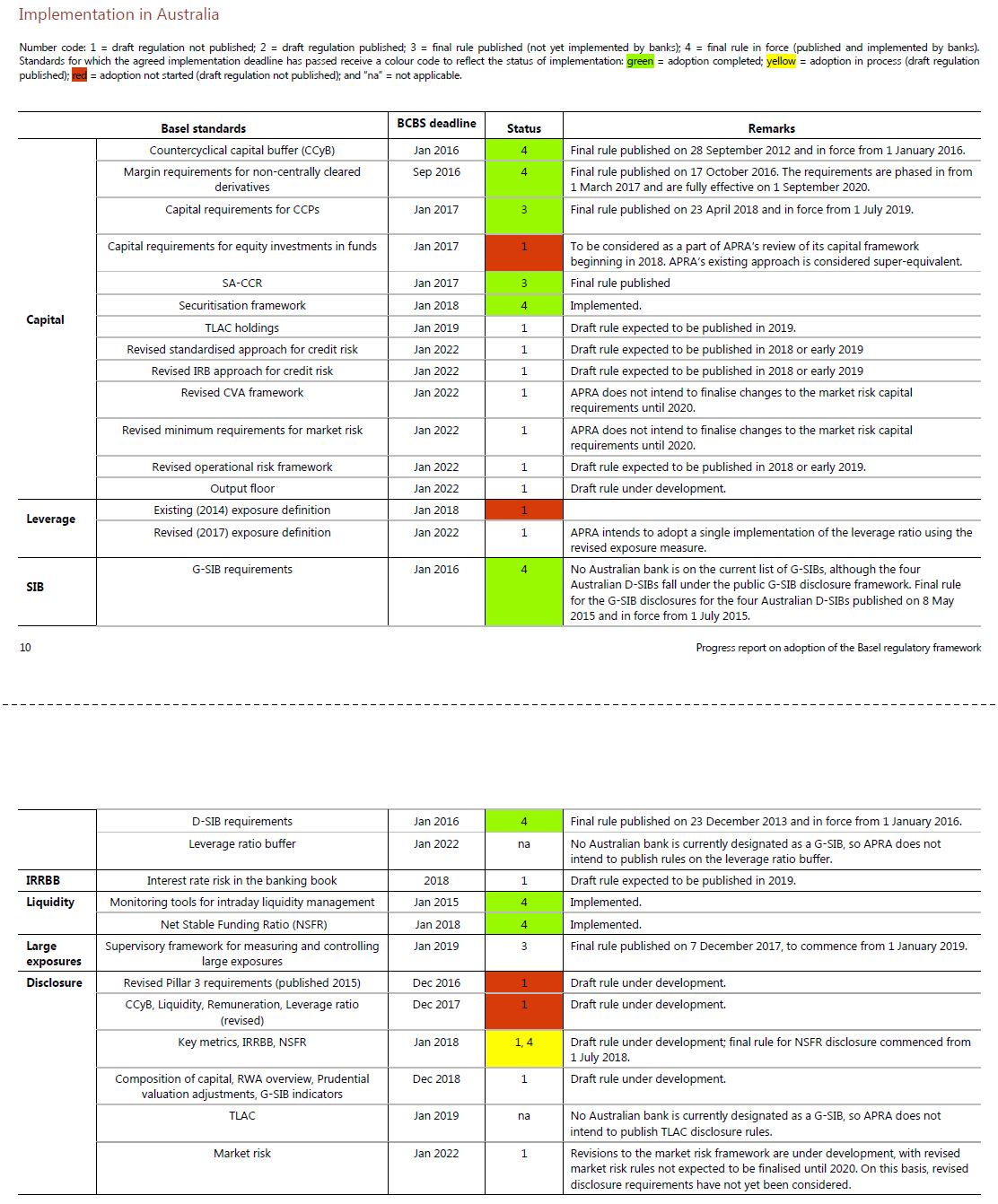

The Basel Committee released their status update of progress in implementation the requirements under Basel III. While some progress is being made, there are still gaps. The Australian implementation still has gaps, especially around aspects of disclosure.

Here is their summary.

In 2012, the Committee started the Regulatory Consistency Assessment Programme (RCAP) to monitor progress in introducing domestic regulations, assessing their consistency and analysing regulatory outcomes.

As part of this programme, the Committee periodically monitors the adoption of Basel standards. The monitoring initially focused on the Basel risk-based capital requirements, and has since expanded to cover all Basel standards. These include the finalised Basel III post-crisis reforms published by the Committee in December 2017, which will take effect from 1 January 2022 and will be phased in over five years. When those reforms were published, the Group of Central Bank Governors and Heads of Supervision, the oversight body of the BCBS, reaffirmed its expectation of full, timely and consistent implementation of all elements of the package.

As of end-September 2018, all 27 member jurisdictions have risk-based capital rules, Liquidity Coverage Ratio (LCR) regulations and capital conservation buffers in force. Twenty-six member jurisdictions also have final rules in force for the countercyclical capital buffer and the domestic systemically important bank (D-SIB) requirement. With regard to the global systemically important bank (G-SIB) requirements published in 2013, all members that are home jurisdictions to G-SIBs have final rules in force.

Since the last report published in April 2018, member jurisdictions have made further progress in implementing standards whose deadline has already passed. These include the leverage ratio based on the existing (2014) exposure definition, which is now partly or fully implemented in 26 member jurisdictions. Moreover, 25 member jurisdictions have issued draft or final rules for the Net Stable Funding Ratio (NSFR), and 20 member jurisdictions have issued draft or final rules for the revised securitisation framework. In case of implementation of the standardised approach for measuring counterparty credit risk exposures (SA-CCR), 24 member jurisdictions have issued draft or final rules. Also, draft or final rules for the capital requirements for bank exposures to central counterparties (CCPs) have been issued by 23 member jurisdictions.

However, in many jurisdictions, rules for these standards are yet to be finalised and come into force. This is notably the case for the NSFR, with only 10 member jurisdictions having final rules in force as of end-September 2018.

There has been also progress in implementation of standards whose deadline is within the next six months. On requirements for total loss-absorbing capacity (TLAC), 15 member jurisdictions have issued draft or final rules. Similarly, 21 member jurisdictions have issued draft or final rules for the large exposure (LEX) framework and for interest rate risk in the banking book (IRRBB).

They publish a country by country assessment, here is the one of Australia. Still more to do clearly, especially in terms of disclosure.

Deloitte has measured how Australians feel about the banks after their dirty laundry was aired by the Hayne royal commission. The results aren’t pretty, via InvestorDaily.

This week Deloitte launched its Australian Trust Index, which measures levels of customer trust and general trust influence factors. In this Inaugural Index – Banking 2018, the professional services firm surveyed banking customers to identify the way forward to rebuild reputation and trust.

Over 2,000 randomly selected demographically representative Australians were surveyed in August of this year. The vast majority of Australians (80 per cent) believe that banks are unethical. The index found that only 20 per cent believe that banks in general are ethical – that they do what is “good, right and fair”.

“The banking sector has undergone a rigorous and exposing investigation through the Royal Commission into Misconduct in Banking, Superannuation and Financial Services,” Deloitte Trust Index author Willem Punt said. “It highlights the depth of the crisis of trust in the sector in Australia.

“We specifically designed the index to measure levels of customer trust and general trust influence factors so that we could deepen our understanding of the factors influencing trust. This enables us to point to actions banks can take to restore reputation and trust,” he said.

The index also gives a weighted national benchmark to use to compare individual organisational performance. It considered what is most important to the average Australian customer when it comes to trusting their bank and ‘banks in general’.

“The index indicates the greatest driver of perceptions of trustworthiness among bank customers is a mindset of consistently keeping promises,” Mr Punt. “Trust improves when it comes to my own bank as opposed to banks in general.”

Only 36 per cent of the 2,000+ Australian banking customers surveyed believe their bank has their best interests at heart, whereas only 21 per cent believe banks in general have their customers’ best interests at heart. Also, 49 per cent trust their own bank to keep its promises compared with 26 per cent in general.

“These results and those of the full index are particularly valuable given that culture and conduct will both get a very hard edge in the strengthened regulatory environment mooted by Commissioner Hayne, who has signalled a greater role for the judiciary in ensuring accountability for significant and systemic poor conduct,” Mr Punt said.

The way forward to rebuild reputation and trust in today’s business world is far more about communities and relationships and far less about transactions, said Andy Bateman, Monitor Deloitte Strategy Partner and a key author of the Deloitte Trust Management Model.

“The companies that get this, at the deepest level, are exhibiting the kinds of behaviours that genuinely build trust,” he said.

The opposition has called on the coalition government to extend the Hayne royal commission after listening to victims of the banks, via InvestorDaily.

Labor leader Bill Shorten made the comments after a town hall meeting with Victorians in the federal seat of Deakin.

“We’ve heard today from victims of the banks, we’ve heard from small businesses, we’ve heard from women trapped in domestic violent relationships. We’ve heard from people who were the victims of crime and then became victims of crime again reinjured through the processes of careless greedy negligent banks,” he said.

The opposition leader said it was clear from the royal commission that the banks were guilty of ripping off ordinary Australians.

“The banks should be ashamed of themselves. In Australia if you steal from the banks you go to jail but if the banks steal from you they get a bonus and a promotion and a bigger profit,” he said.

Mr Shorten said he thought the Hayne Royal Commission was doing a great job and that what they had exposed would wake up the industry.

“This is the biggest wake-up call that we’ve seen in Australian corporate history,” he said.

Mr Shorten said that Labor called on the government to extend the royal commission and demanded an apology from the guilty parties.

“I think the people in power and regulators owe a big apology to the tens of thousands of victims of banking in Australia. We want to see Mr Morrison extend the royal commission,” he said.

Mr Shorten said that Scott Morrison’s track record on the royal commission called into question his ability to implement any changes.

“On 26 occasions the current Prime Minister, when he was Treasurer, voted against the royal commission. The action of him rejecting the banking royal commission 26 times speaks far louder than the words in our mouths.

“I’ve got my doubts that this government and this prime minister can be trusted to implement what comes out of the RC,” he said.

Mr Shorten acknowledged that Labor potentially should have called for a royal commission years ago but reiterated the parties support for the victims.

“Labor just wants to say to all the victims of the banks, we hear you and sure maybe things should have been done a lot longer ago but for the last 2 years we’ve stood up for the victims and today we are putting a submission into the royal commission just drawing attention to our knowledge and the voices we hear,” he said.

There would be challenges ahead in regulating banks as it was hard to legislate against being a bully said Mr Shorten.

“Some of the conduct we have heard is illegal and you shouldn’t have to pass a law to say don’t charge dead people for services that they are not getting. Some things are allowed within the law and they just exploit,” he said.

Blame was also to be put on the regulators who gave out the equivalent of corporate speeding tickets to banks, said the opposition leader.

“The regulators have found this royal commission to be highly embarrassing as they should. Having said that it does go back to the banks. The system is broken when it comes ethical protections of consumer and customers,” he said.

It is not enough to come to parliament to apologise said Mr Shorten and he said executives at banks should think about how they show they mean it.

“If the boards of banks and CEOs were to hand back some of the bonuses they’ve received whilst they were in charge of banks whilst they were exploiting ordinary Aussies. It doesn’t change where the victims are but it would be a good down payment,” he said.

This town hall meeting was the first of many as the Shadow Minister for Financial Services Clare O’Neil is currently undertaking a series of roundtables with victims in towns that have not been visited by the Royal Commission.

The move by labor was announced following the release of the interim report with Mr Shorten outlining that despite over 9000 submissions, the hearing had only heard from 27 customers.

“All of the hearings of the commission have been in just three capital cities; regional and rural customers have not had a sufficient chance to have their say in this process.

“Misconduct in the financial services sector is a national issue, and Australians across the country deserve their chance to be heard.”

However, federal Treasurer Josh Frydenberg has censured Mr Shorten for “threatening the independence, the authority of our royal commission”, stating earlier this month: “Bill Shorten first thought that he knew better than the royal commissioner saying there must be an extension of time, when the royal commissioner has yet to ask for it. Now he thinks he is the royal commissioner by conducting his own hearings and running a parallel process around the country.”

However, when asked whether the government would extend the commission further, should Commissioner Hayne ask for one, the Treasurer has previously said: “If he asks for more time, he has got it”.

AMP Bank has revealed that, effective for loans settled from January 2019, it will be calculate broker commissions for its home loans on the net balance, instead of the total approved facility amount, via The Adviser.

The bank becomes the third large lender to change the upfront commission structure to the new model in the past few weeks, after NAB and Westpac announced similar changes.

The bank outlined that it had made the changes “in line with Sedgwick recommendations” from his Retail Banking Remuneration Review (which helped form the basis of the Combined Industry Forum’s reform package).

Mr Stephen Sedgwick AO recommended in his report last year that remuneration should not “directly link payments to loan size”, suggesting that alternative payment arrangements could include: commission based payments that take the loan to value ratio (LVR) or the loan type, or “the quality of the advice given to the customer into account; and, preferably arrangements between lenders, mortgage brokers and aggregators that are not product based such as lender-funded fees for service”.

Speaking of the changes, an AMP Bank spokesperson said that the change “centres on ensuring customers obtain loans that are appropriate for their needs and objectives”.

The spokesperson continued: “Brokers and advisers play a vital role in our community, providing more than 50 per cent of all home loan applications and the portion of the market they service continue to grow, reflecting the important service they provide.

“Like brokers and advisers, AMP Bank is committed to ensuring we continue to deliver good customer outcomes so we’re making some changes to the way commissions are calculated for home loans.

“These are changes that have been committed to by the industry and we have announced the detail early as we think it’s important to give brokers and advisers early visibility of the changes.”

Lenders expected to make changes by the end of the year

NAB became the first major lender to implement the recommendations from the ASIC and Sedgwick reviews, which were backed by the Combined Industry Forum package of reforms.

Its white label brand, Advantedge (and Advantedge-funded brands, such as Homeloans) announced the same changes in tandem, and Westpac announced earlier this week that the bank and its subsidiaries (St. George, Bank of Melbourne and BankSA) will link upfront commission payments for standard home loans to net debt utilisation and inclusive of loan offset arrangements, rather than the approved loan limit, effective 1 January 2019.

The CIF recently hosted an event which further outlined its work on mortgage broking reforms and reiterated that lenders are expected to make the remuneration changes by December 2018

AMP Limited has announced the successful completion of its portfolio review including an agreement to divest its Australian and New Zealand wealth protection and mature businesses (AMP Life) and reinsure New Zealand retail wealth protection for total proceeds of A$3.45 billion.

The stock dropped (in a down day) to a new low.

AMP will exit its Australian and New Zealand wealth protection and mature businesses via a sale to Resolution Life1 for total cash and non-cash consideration of A$3.3 billion; transaction expected to complete in 2H 2019; subject to regulatory approvals.

Binding agreement with Swiss Re2 to reinsure New Zealand retail wealth protection, releasing additional capital of up to A$150 million to AMP prior to completion of sale; subject to regulatory approvals.

Intention to seek divestment of New Zealand wealth management and advice businesses via initial public offering (IPO) in 2019 subject to market conditions and regulatory approvals, unlocking further value.

Significant capital release will strengthen AMP’s balance sheet and provide strategic flexibility; all options for use of proceeds to be evaluated and update to be provided following transaction completion.

Wealth protection and mature – Resolution Life transaction summary

Under the terms of today’s agreement, AMP will sell its Australian and New Zealand wealth protection and mature businesses (AMP Life) to Resolution Life for a total consideration of A$3.3 billion, which comprises:

A$1.9 billion in cash.

A$300 million in AT1 preference shares in AMP Life (issued on transaction completion).

A$1.1 billion in non-cash consideration:

o Economic interest in future earnings from the mature business, equivalent to A$600 million; expected to provide steady ongoing earnings to AMP of approximately A$50 million after tax per annum, assuming an annual run-off at 5 per cent.

o A$515 million interest in Resolution Life, focused on the acquisition and management of in-force life insurance books globally.

AMP expects to monetise all non-cash consideration over time.

Together with the New Zealand reinsurance agreement, the total value equates to approximately 0.82x pro forma embedded value of the sold businesses at 30 June 2018, excluding franking credits.

Resolution Life assumes risk and profits of the wealth protection and mature businesses from 1 July 20183, subject to Australian wealth protection risk-sharing arrangements.

A new relationship Agreement has been established with Resolution Life and AMP Capital will continue to manage wealth protection and mature assets under management. AMP Capital will also join Resolution Life’s global panel of preferred asset managers.

The transaction is subject to regulatory approvals and other conditions precedent and is expected to complete in 2H 2019.

Partnering to ensure smooth transition for customers

Resolution Life is an international insurance and reinsurance group whose management has a 15-year track record in providing quality service to in-force insurance customers.

The transaction has been designed to ensure all existing terms and conditions will be retained. The teams supporting existing AMP customers will largely transfer on completion to maintain continuity of service.

AMP and Resolution Life will work closely together to ensure a smooth transition for customers.

New Zealand wealth protection reinsurance

AMP has entered into a binding reinsurance agreement with Swiss Re for the New Zealand retail wealth protection portfolio which is expected to release up to A$150 million of capital to AMP, subject to regulatory approval. The agreement is expected to be effective from 31 December 2018, and will cover approximately 65 per cent of the New Zealand retail wealth protection portfolio for new claims incurred from that date.

The reinsurance agreement is expected to reduce New Zealand profit margins by A$20 million on a full-year basis. The reinsurance outcomes are factored into the Resolution Life transaction.

New Zealand wealth management and advice businesses

AMP is today also announcing its intention to seek divestment of its New Zealand wealth management and advice businesses via an IPO in 2019. The decision to proceed with an IPO and its timing remain subject to market conditions and regulatory approvals.

These businesses have FY18 pro forma operating earnings of approximately A$40 million on a standalone basis. The IPO would release capital to AMP and create a standalone New Zealand wealth management and advice business.4

Portfolio review outcomes will release capital, simplify portfolio and create strategic flexibility

The completion of the portfolio review will strengthen AMP’s balance sheet and provide strategic flexibility. All options for use of proceeds will be considered including growth investments and/or capital management activity.

The exit from Australian and New Zealand wealth protection and mature will also significantly simplify AMP and its earnings profile, enabling it to focus on its higher growth businesses of Australian wealth management, AMP Capital and AMP Bank.

The simplification and separation costs related to the Resolution Life sale transaction are expected to be in the order of A$320 million post-tax.

Additional capital from the transaction with Resolution Life will facilitate a reduction in AMP’s corporate debt of up to A$800 million.

The financial impacts of the transaction on AMP post-separation are outlined in the investor presentation.

AMP will exclude the 2H 18 earnings from the discontinued businesses in determining the FY 18 dividend. AMP continues to target a total FY 18 dividend payout within, but towards the lower end of its dividend guidance range of between 70 – 90 per cent of underlying profit.

Further guidance on use of proceeds will be provided following the completion of the transaction in 2H 2019.

On Friday submission to the Royal Commission into Financial Service Misconduct relating the the draft report closes. You can still make a Public Submission – a quick and painless process, and it is a once in a generation chance to shape the future of finance in Australia.

This is what DFA did today, and here is a copy of what I said.

Summary

We welcome the findings from the draft report and recommend the following policy options.

The culture in the finance sector needs to change, to put the customer first. Mortgage brokers for example should have a best interest duty and commissions should be banned.

The current focus on “financial stability” is myopic, favouring large players, over small, and building structural risks into the system; the regulators have failed.

The large players are too big to fail and too complex to manage, and need to be broken apart. A modern Glass Steagall separation would achieve this, and is proven to reduce risk, and drive better customer outcomes and right size our finance sector.

The existing regulatory structure, operating in the Council of Financial Regulators needs to be changed, as its narrow focus on financial stability, and a massive “bet” on inflating the housing sector now at risk. None of the regulatory actors are without blame.

Introduction.

Digital Finance Analytics (DFA) is an Australian boutique research, consulting and advisory firm which combines primary consumer and small business research, analysis of both private and public datasets and economic modelling to analyse the dynamics of the finance and property sector. We have been operating since 2005.

Our analysis is based on a rolling 52,000 household survey, with more than 4,000 new data points added each month. From this we are able to assess the state of household finances, their future property transaction intentions, and their level of debt; and ability to service it.

Households Are Overextended

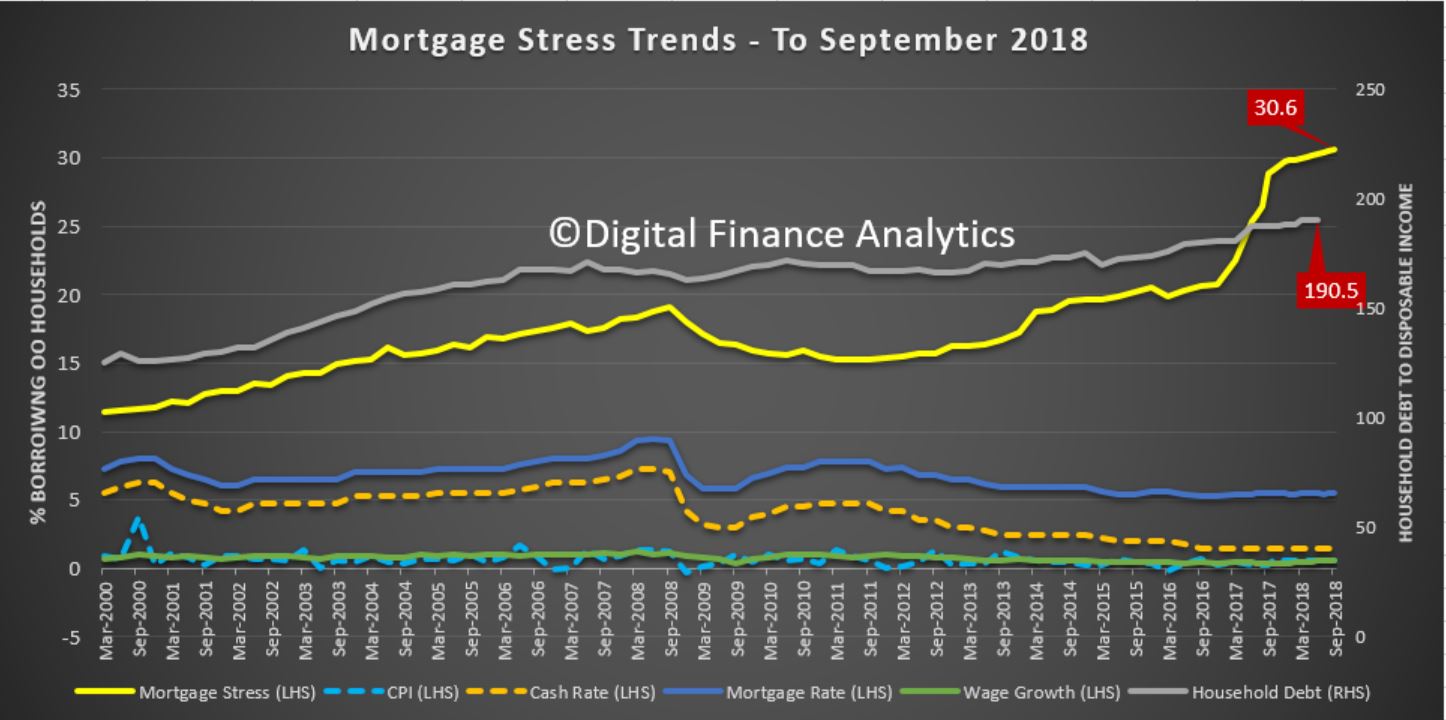

We have observed a considerable expansion of household debt in recent years, driven by low interest rates, more generous lending standards, and some degree of “not suitable” lending and fraud. The RBA reports that the household debt to income ratio is now around 190 and the debt to GDP ratio is one of the highest in the world.

As a result, more households are in financial stress, as tracked in our mortgage stress trends (defined in cash flow terms, not a set percentage), and last month more than one million households with owner occupied mortgages were in difficulty, despite the ultra-low interest rates. This equates to 30.6% of all borrowing households.

This has been exacerbated by flat incomes, and rising costs, but poor lending practice is the underlying cause. We also believe that as interest rates rise, and property prices fall further, the financial state of households will decline further. This is because many are enjoying the “wealth effect” of property gains in recent years, but this is only a paper gain, and now prices are falling. The expectation is prices will fall further and faster.

The Cause of Property Price Falls

Following many years of over-free lending, the regulators have now intervened to an extent and as a result lending standards are tightening, with up to a 40% fall in borrowing power for many compared with a year ago. In the main though this is a result of the existing regulations now being applied as originally intended, rather than new laws, as incomes and expenses are being tested, as opposed to using a formula based on HEM (Household Expenditure Measures).

This resetting of lending standards marks a significant change in the market, and as a result according to our surveys, demand for property is easing, at the time when foreign buyers are receding, and property investors are getting twitchy. According to Bank of England research, property investors are significantly more likely to exit the market in a down turn compared with owner occupied borrowers.

Property investors, who have driven the market higher in recent years are choosing to exit, sometimes forced by the switch from interest only loans to principal and interest loans (estimated at around ~$120 billion per annum), of the $1.7 trillion total mortgage lending pools.

Our modelling shows that it is credit availability which pumped up property prices (and which allowed the Banks and other Lenders to growth their balance sheets, and profits) and the reverse is also true. The normalising of lending standards will rightly reduce credit, thus driving home prices and banks profitability lower. The catch here is that for more than a decade, Australia’s economic performance has been built on the back of ever greater mortgage and consumer debt, home price growth, and construction. Thus from a policy perspective Government, and the RBA will defend high levels of credit and home prices, despite the risks.

The other factor to consider is that as banks were so reliant on home lending to drive profitability, the incentives were there to over lend, bend the rules, and reward poor behaviour. They have not followed regulatory guidelines nor have they met community expectations. In a word, GREED, as your draft report shows.

The Policy Challenge

Our view is that whilst the restatement of the current lending standards will assist, there are more significant structural questions to be considered. Regulation and changes to the law alone cannot address the issues you call out.

The culture within the finance sector needs to be changed, to put customers at the centre of their business. Whilst talk is cheap however, there is little evidence of substantial change as yet. The removal of commissions should be a corner stone, as conflicted remuneration remains a significant problem. Mortgage brokers, for example, should have a responsibility to act in the best interest of their customers. The industry will resist this, but it is essential.

Currently, the capital adequacy rules favour mortgage lending relative to productive lending to business and as a result according to our Small and Medium Enterprise surveys, many businesses are unable to obtain finance (or can only do so by securing their property). We believe the various risk weights reflect a myopic view of the financial system and they need to be changed. Too much of the bank’s portfolio of loans – up to 65% – is against residential property – this is extraordinarily high by international standards, and presents a significant risk, to say nothing of the lack of business investment which has resulted.

However, we hold the view that the major financial sector players are too complex to be managed effectively, scale is now a disadvantage. Thus we believe there is a case to break up the banks into smaller units. This would involve both vertical disaggregation (separation of advice, sales and product manufacture) and horizontal disaggregation (separate of wealth, insurance, retail banking and investment banking). In addition, there are significant risks from their operations in derivatives, and in an integrated environment, costs, risks and profits are cross linked. Given the size of the derivatives sector (significantly larger than before the GFC), the systemic risks are significant. To counter this, we advocate the implementation of a modern Glass Steagall separation, where the high-risk speculative activities are separated from the normal lending, payment and deposit functions within banking. This would have the added benefit of reducing the potential risks of a bank deposit bail-in in a time of crisis. Evidence suggests that the existence of a modern Glass Steagall separation would reduce risk and limit systemic risk. In a post Glass Steagall world, bank lending would be more aligned with the deposits available, so their ability to make loans “from thin air” as in the current system would be curtailed. They would also be more inclined to make loans for truly productive purposes.

We also need to consider the role of the regulators and the RBA. Murray’s Financial System Inquiry recommended that the effectiveness of the current regulatory system be monitored. The Council of Financial Regulators is the peak body, chaired by the RBA, where key policy is set, with the Treasury, ASIC, APRA and others. However, none of their deliberations are made public, and it appears that all entities have been sharing the same view that growing housing credit was the chosen growth lever of choice following the mining boom. It appears that the weak supervisory approach from ASIC and APRA stemmed from this policy, and was supported by policy rates being set too low. As a result, the systemic risks have been underestimated, and the economic platform for the country narrowed.

We believe that there should be a stronger advocate for the consumer within the regulatory system, perhaps the ACCC should take this role. But more broadly the role of individual regulators and how they connect needs clarity. The Royal Commission highlighted the lack of coherence, and alignment. We also would argue (perhaps beyond the scope the current inquiry) that APRA has myopically focussed on financial stability, at the cost of good consumer outcomes and competition, that the regulations favour large players over small players, that the RBA policy rates are too low, and the ASIC so far is still perceived as a weak and ineffective regulator. Thus the area of appropriate and effective regulation is critical.