Despite the revelations of the Royal Commission, ASIC is still experiencing deliberate delays from financial institutions in meeting reporting requirements, via Financial Standard.

On Friday, ASIC chair James Shipton told the Parliamentary Joint Committee on Corporations and Financial Services that the regulator is still experiencing “slow and delayed responses from financial institutions and, in some cases, overly technical responses aimed at delay.”

This is despite a key finding of the Royal Commission’s interim report being that the industry has been repeatedly dishonest with both the community and regulators, Shipton said.

“And unfortunately, whilst we are hearing important acknowledgements from leaders of financial institutions about change, such change is not happening as quickly as it should,” he said.

“Due process is important, but it must not be manipulated to disrupt the achievement of fair, appropriate and honest outcomes.”

He then warned institutions of the ramifications if such conduct continues.

“If institutions lie, or are otherwise dishonest with us, we will use every power available to us to punish that behaviour. I am a firm believer in the importance and effectiveness of court-based enforcement tools. They are the foundation of any regulator,” Shipton said.

Further, in defending ASIC on criticisms of its effectiveness in recent years, Shipton questioned whether the entity he leads should be resourced differently to meet community expectations.

Shipton said any comments as to ASIC’s regulatory approach should be considered in the context of its size, stating: “ASIC has been designed over the arc of its history and how Australia’s financial system has evolved over the years to have its own unique characteristics.”

He said now is the right time to discuss whether ASIC and its peers are “right sized” in relation to the new industry funding model; unique characteristics of Australia’s financial system; size of Australia’s financial markets; number of consumers; number of people engaged in the industry; and the clear expectations of the community.

Shipton clarified that he was not demanding greater resources, but instead looking to start an important policy conversation.

“For me, my own experience as a regulator in Hong Kong, in a system that also has an industry funding model, is instructive. There, on an adjusted basis (in terms of financial services GDP and financial services population), Hong Kong’s financial regulators are three times the size of Australia’s,” he said.

The last remaining major bank offering reverse mortgages, and its subsidiary, will withdraw their reverse mortgage products from sale next year, via the Adviser.

The Commonwealth Bank of Australia (CBA) and its subsidiary Bankwest have announced that they will be removing their reverse mortgage products from sale from 1 January 2019.

As such, as of next year, brokers will no longer be able to write new reverse mortgages to Bankwest nor will CBA offer its reverse mortgage product through its proprietary channel (CBA had withdrawn its reverse mortgage offering from the broker channel last year).

The move means that, as of next year, none of the major banks will offer reverse mortgages.

Speaking of the decision, a CBA spokesperson said: “At the Commonwealth Bank, we constantly review and monitor our suite of home loan products and services to ensure we are maintaining our prudent lending standards and meeting our customers’ financial needs.

“As part of our strategy to become a simpler, better bank, we are streamlining our product portfolio and have made the decision to withdraw our Equity Unlock for Seniors (EQFS) product from sale.”

While the major bank noted that it would be withdrawing the product from sale and for limit increases from 1st January, it added that it would continue to support existing customers with this loan.

Likewise, a spokesperson for CBA-subsidiary Bankwest confirmed that the decision had been taken to withdraw its Seniors Equity Release product from sale for both broker and proporietary channels as of 1 January 2019.

“We will continue to support our existing customers who have this product with us,” the bank’s spokesperson said.

The move comes amid ongoing scrutiny of the reverse mortgage market.

In August of this year, the Australian Securities and Investments Commission (ASIC) released its review of the $2.5 billion reverse mortgage market, outlining that although these products can “help many Australians achieve a better quality of life in retirement” and achieve their immediate financial goals, some borrowers had a “ a poor understanding of the risks and future costs of their loan, and generally failed to consider how their loan could impact their ability to afford their possible future needs”.

ASIC suggested that “lenders have a clear role to play here and need to do more” adding that for nearly all of the loan files the regulator reviewed for the report (including those from CBA and Bankwest), the borrower’s long-term needs or financial objectives “were not adequately documented”.

Further, the Australian Prudential Regulation Authority (APRA) proposed earlier this year that reverse mortgages, which are currently risk-weighted at 50 per cent (where LVR is less than 60 per cent) or 100 per cent (for LVRs over 60 per cent), would be treated as ‘non-standard’ in light of “the heightened operational, legal and reputational risks associated with these loans” and subject to a risk weight of 100 per cent.

Last year, Macquarie and Westpac withdrew reverse mortgage offerings from the market, while Auswide Bank tightened up requirements on its equity release products so that prospective borrowers would be required to provide proof of a satisfactory repayment history over the previous six months.

ASIC says that on 13 April 2018, ASIC announced that it had accepted a Court-enforceable undertaking (EU) from Commonwealth Financial Planning Limited (CFPL) arising from its Fees For No Service conduct (18-102MR).

One undertaking required of CFPL was to appoint Ernst & Young (EY) to prepare an independent expert report that considered:

whether CFPL had taken reasonable steps to ensure customers who should have received remediation in the 31-month period from 1 July 2015 to 31 January 2018 did receive that remediation. ASIC’s previous oversight of CFPL’s remediation had considered the period to 30 June 2015; and

whether CFPL had put in place systems, processes and controls to meet its contractual obligations to customers who are paying ongoing service fees.

As set out in ASIC’s Regulatory Guide 100: Enforceable Undertakings, ASIC will make available a summary of an independent expert’s report in these circumstances to promote the integrity of, and public confidence in, the financial markets and corporate governance. A copy of the executive summary of EY’s report can be accessed via the Enforceable undertakings register.

EY’s findings on remediation

In relation to the remediation of CFPL customers, EY found that:

for the periods 1 July 2015 to 31 May 2016 and 5 June 2017 to 31 January 2018, there was no evidence to suggest that CFPL had not taken reasonable steps to ensure that customers who should have received remediation did receive that remediation; and

for the period 1 June 2016 to 4 June 2017 (Period 2), there had been a lower level of customer testing during this period and further work by CFPL was required. EY found that CFPL is in the process of taking reasonable steps to identify and remediate those customers who should have received remediation.

EY will re-assess and report on Period 2 in January 2019 once CFPL has undertaken additional remediation work for that period.

EY’s findings on CFPL’s controls environment

EY assessed whether CFPL had put in place adequate systems, processes and controls to meet its contractual obligations to customers who are paying ongoing service fees. EY found that there was nothing to suggest that those systems, processes and controls are not reasonably adequate to ensure that CFPL is able to discharge its obligations to its customers. However, EY noted that CFPL could make further improvements to address:

a low level of control awareness within the business;

a high prevalence of manual processes and controls;

limitations on CFPL’s ability to analyse and report information for tracking and reporting of compliance centrally; and

the sustainability of its manually intensive processes.

EY will assess and report on whether CFPL has addressed EY’s findings, through the implementation of systems and process improvements, in January 2019.

CFPL has requested an extension of time for EY to produce its final report and for CFPL to provide its senior executive attestation as required under the EU, to 31 January 2019.This extension of time will allow CFPL to undertake the additional work required in relation to Period 2 and to implement the recommendations made by EY to further improve CFPL’s systems, processes and controls.

CFPL is required by ASIC to submit a detailed plan setting out the specific actions that it will undertake to ensure that it addresses EY’s findings and recommendations. The EU will be amended to reflect this additional plan, the timing of the final report and senior executive attestation.

“Did you think to yourself that taking money to which there was no entitlement raised a question of the criminal law?” Commissioner Kenneth Hayne asked Nicole Smith, who resigned as chair of NAB’s superannuation trustee, NULIS, a little more than a month before she fronted the banking royal commission.

Smith’s evidence related to NAB skimming A$87 million from superannuation accounts by charging 220,000 members “service fees” for which no service was provided. As head of the board of the superannuation trustee, it was Smith’s job to act solely in the best interests of the members. Instead she acted in the best interests of NAB.

Her admissions and the evidence from the royal commission that more than $A1 billion has been taken from superannuation accounts for no service show we need better supervision of the trustees who oversee more than A$2.7 trillion in superannuation assets.

Trustees are surrounded by temptation, to preference the interests of their sponsoring organisations, to act in the interests of other parts of their corporate group, to choose profit over the interests of members, and to establish structures that consign to others the responsibility for the fund and thereby relieve the trustee of visibility of anything that might be troubling.

The entrenched practice of retail super funds using superannuation trust funds as profit-making enterprises undermines the integrity of the whole superannuation sector. Focused regulatory action and oversight are imperative to protect it.

Super duties

Super trustees are subject to a range of stringent duties.

There are “equitable” duties, which arise from trustees being fiduciaries – responsible for acting in the best interests of the owners of the assets they manage. As fiduciaries, super trustees must avoid conflicts of interest and account for any profit they make.

As trustees specifically, they must act in the best interests of the beneficiaries and exercise powers conferred to them as trustees (trust powers) with real and genuine consideration.

All trustees are legally obliged to act in the best interests of the people whose money they are entrusted with. Superannuation trustees have an even greater obligation, because of the social importance of superannuation. The High Court has ruled that public expectations mean superannuation trustees have “more intense” obligations than other private trusts.

This is underlined by the “statutory” duties of the Superannuation Industry (Supervision) Act 1993. It states directors of corporate superannuation trusts must perform their duties in the best interests of their beneficiaries, superannuation fund members.

The act also establishes supervision and oversight of super trustees by the Australian Prudential Regulation Authority (APRA), the Australian Securities and Investments Commission (ASIC) and the Commissioner of Taxation.

Irregular regulation

Yet clearly this oversight has been failing. The evidence from the royal commission is that many super trustees having been ignoring their duties. They have gone along with rubber-stamping unjustifiable fees purely because their parent institutions wanted the money.

In 2017 the prudential regulator was given the power to directly disqualify directors of superannuation trustee corporations. It already had the power to do so by applying to the Federal Court. Over the past decade, however, it has sought just one disqualification.

The regulator’s deputy chair, Helen Rowell, has argued this is due to APRA trying to protect the public interest, avoiding the risk of a run on a fund. But its inaction has arguably emboldened super trustees to ignore their duties because of the low risk of being penalised.

Previous reform proposals

The royal commission may result in criminal charges against banks and financial institutions. One outcome that must come is stronger oversight of super trustees.

It is therefore critical the royal commission recommend strong action, including reforms proposed by previous inquiries into the financial services sector.

These include the Financial System Inquiry, which recommended in 2015 that super funds must have a majority of independent directors on their trustee boards. It also proposed new civil and criminal penalties for directors failing to act in the best interests of fund members.

Additional reforms might include:

establishing a specific conduct regulator for corporate superannuation trustees

making it mandatory for ASIC to prosecute superannuation trustees and related entities (such as banks) for duty breaches, with much higher penalties

stronger oversight over responsibilities that corporate trustees outsource to third parties

mandatory reporting of corporate fee structures, with regular review to determine if these are justified.

The trust remains the most appropriate legal mechanism to manage savings accumulated over a long time. Much stronger behavioural controls and civil penalties are necessary to ensure super trustees act honestly and in good faith for the benefit of the beneficiaries. That they are, in short, trustworthy.

Author: Samantha Hepburn Director of the Centre for Energy and Natural Resources Law, Deakin Law School, Deakin University

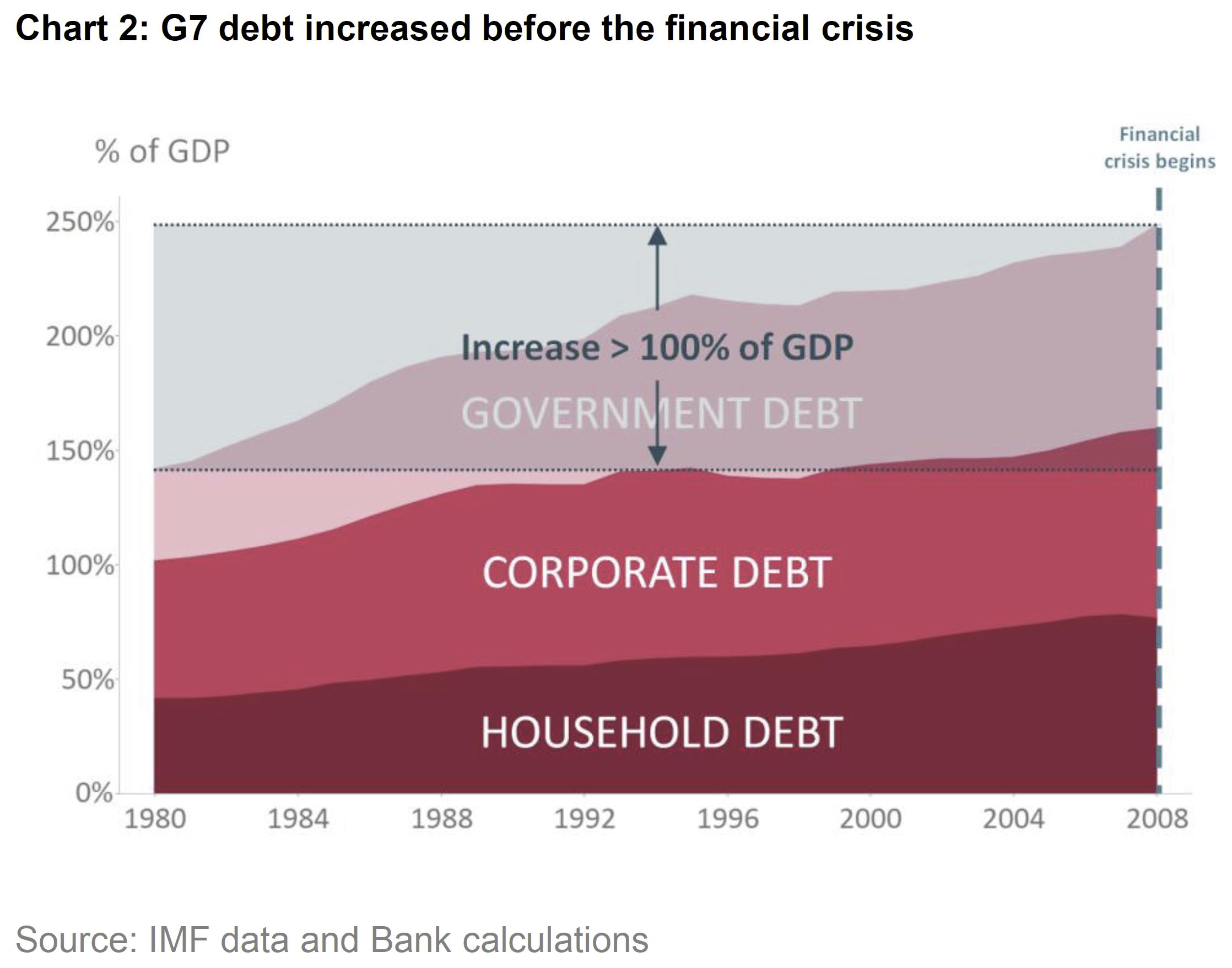

Mark Carney, the Governor of the Bank Of England, and the Chair of the Financial Stability Board – the global peak body worrying about the stability of the financial system – gave a speech in New York – “True Finance – Ten years after the financial crisis“. Within the speech he explained the Three Lies of Finance, and today we discuss them in the Australian context.

He pointed out that we seem destined to have a financial crisis every decade – 10 years ago it was the GFC, 20 years ago the Asian crisis and three decades back the Latin American debt crisis. So, are we due another?

Well, he argues that much has been done to secure the financial system since the GFC, but there are risks that three lies may once again lead to a crisis.

The first lie of finance he says is “This Time Is Different”.

This misconception is usually the product of an initial success, with early progress gradually building into a blind faith in a new era of effortless prosperity. He cites the example of the battles against the high and unstable inflation, rising unemployment and volatile growth of the 1970s and 1980s. Stagflationary threats were tamed by new regimes for monetary stability that were both democratically accountable and highly effective. This included, Clear remits. Parliamentary accountability. Sound governance. Independent, transparent and effective policy-making. The so called Great Moderation.

But these innovations did not deliver lasting macroeconomic stability. Far from it. Price stability was no guarantee of financial stability. An initially healthy focus would become a dangerous distraction. Against the serene backdrop of the so-called Great Moderation, a storm was brewing as total non-financial debt in the G7 rose by the size of its GDP.

Several factors drove this debt super-cycle including demographics and the stagnation of middle-class real wages (itself the product of technology and globalisation). In the US, households had to borrow to increase consumption. “Let them eat cake” became “let them eat credit”.

Financial innovation made it easier to do so. And the ready supply of foreign capital made it cheaper.

Most importantly – and this is the lie – complacency among individuals and institutions, fed by a long period of macroeconomic stability and rising asset prices, made this remorseless borrowing seem sensible.

When the crisis broke, policymakers quickly dropped the received wisdoms of the Great Moderation and scrambled to re-learn the lessons of the Great Depression. Minsky became mainstream.

And in Australia, I still hear many saying our finance sector, and housing sector is different – thanks to high migration, export growth, and great government policy. None of this makes us different, the big lie is many think we are, until we are proved not to be. In fact, today, still many seem unconcerned by the debt bomb we have created. Yet to me, this is one of our greatest challenges.

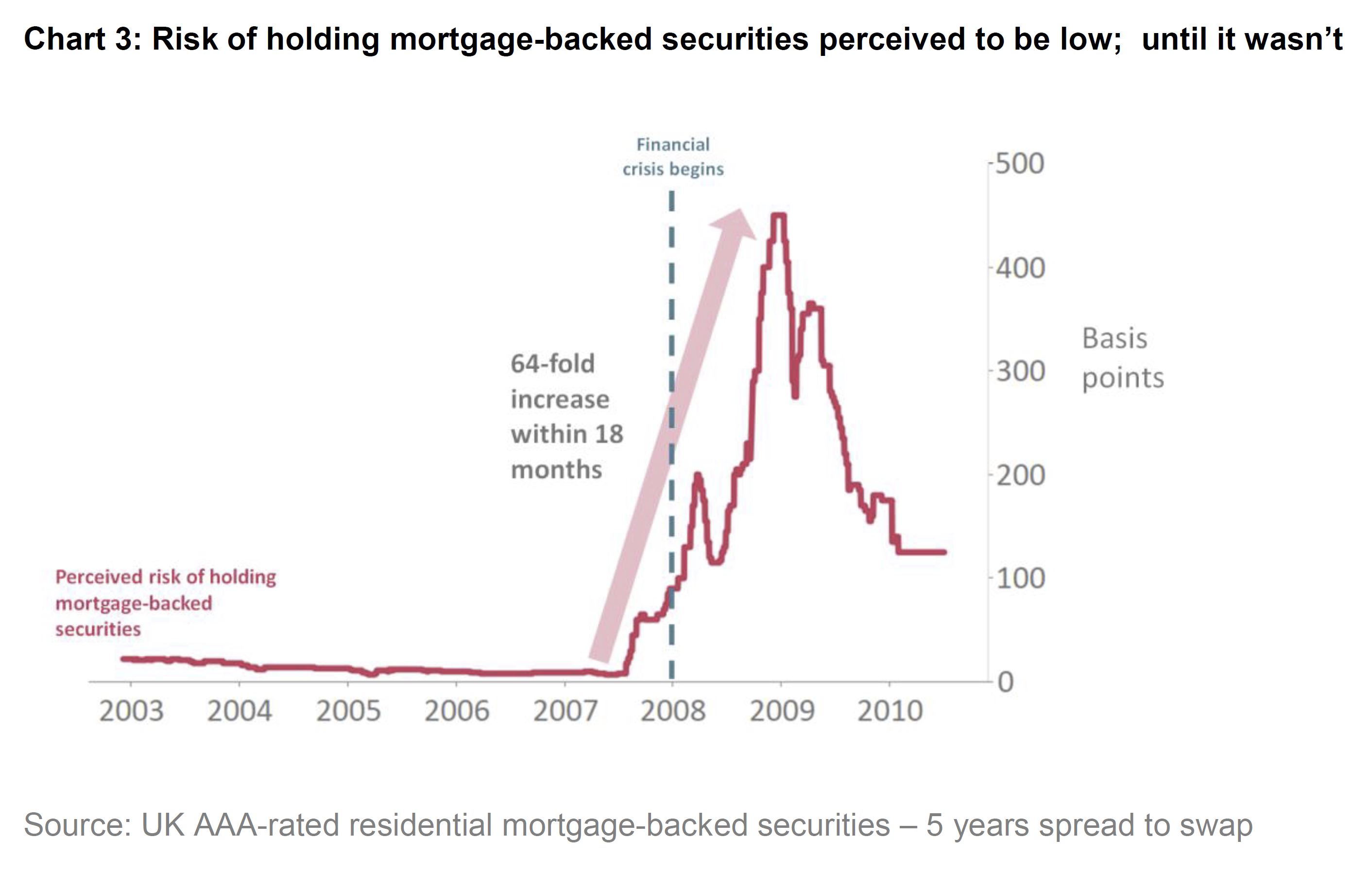

The second lie is that “Markets Always Clear”. There was a deep-seated faith in markets that lay beneath the new era thinking of the Great Moderation. Many argued that you must allow the market free reign, because finance can regulate and correct itself spontaneously, and so authorities retreated from their regulatory and supervisory responsibilities. Does this sound familiar – ASIC and APRA?

Carney says there are two dangerous consequences. First, if markets always clear, they can be assumed to be in equilibrium— or said differently “to be always right”. If markets are efficient, then bubbles can neither be identified nor can their potential causes be addressed. Such thinking dominated the practical indifference to the clear housing and credit booms.

Second, if markets always clear, they should possess a natural stability. Evidence to the contrary must be the product of either market distortions or incomplete markets. Much of financial innovation springs from the logic that the solution to market failures is to build new markets on old ones. He calls this progress through infinite regress.

So we saw light touch regulatory agenda in quest for a perfect real world of complete markets. But in reality, people are irrational, economies are imperfect, and nature itself is unknowable. When such imperfections exist, adding markets can sometimes make things worse.

Take synthetic credit derivatives, which were supposed to complete a market in default risk and thereby improve the pricing and allocation of capital. Financial alchemy appeared to have distributed risk, parcelling it up and allocating it to those who wanted most to bear it.

However, the pre-crisis system had only spread risk, contingently and opaquely, in ways that ended up increasing it. Once the crisis began, risk quickly concentrated on the balance sheets of intermediaries that were themselves capital constrained. And with the fates of borrowers and lenders tied together via hyper-globalised banks and markets, problems at the core spread violently to the periphery.

A truth of finance is that the riskiness of an asset depends on who owns it. When markets don’t clear, agents may be surprised to find what they own and for how long. When those surprises are – or are thought to be – widespread, panic ensues. The swings in sentiment that result – pessimism one moment, exuberance the next – do not reflect nature’s odds, but our own assessments of them, inevitably distorted by Keynes’ optimistic “animal spirits” and his cynical “beauty contests”.

These are dynamics that can afflict not just sophisticated investors, but mortgage lenders and homebuyers, especially during a “new era”. If house prices can only go up, it is possible to borrow large multiples and pay off future obligations with the capital gains that will follow. Such so called “rational” behaviour fuelled the credit binge that ultimately led to the global crisis.

In the end, belief that “markets are always right” meant that policymakers didn’t play their proper roles moderating those tendencies in pursuit of the collective good. The right regulation is essential, as the Royal Commission into Financial Services Misconduct has been highlighting. And breaking up the too big to fail structures is essential. And yet many commentators are STILL arguing for a hands off approach to let the markets rip. This is a lie.

The third lie is “Markets Are Moral”

This argues that markets are always moral, and have a social licence, but the crisis showed that if left unattended, markets can be prone to excess and abuse. In financial markets, means and ends can be conflated too easily. Value can become abstract and relative. And the pull of the crowd can overwhelm the integrity of the individual.

We saw this in the Royal Commission where greed drove unacceptable behaviours, with profit overriding the interest of customers and community expectations, leading to excess returns at any costs, never mind the social damage. Worse those in charge of these financial firms, and the regulators were all singing from the same hymn sheet. Australia Inc. has paid dear for this lie.

Carney says episodes of misconduct – such as the Libor and FX scandals – called into question the social licence that markets need to innovate and grow. Rather than being professional and open, markets became informal and clubby. Rather than competing on merit, participants colluded online. Rather than everyone taking responsibility for their actions, few were held to account.

The crisis reminded us that real markets don’t just happen; they depend on the quality of market infrastructure for their effectiveness, resilience and fairness. Robust market infrastructure is a public good in constant danger of under-provision, not least because the best markets innovate continually. This risk can only be overcome if all market actors, public and private, recognise their responsibilities for the system as a whole.

By undervaluing the importance of hard and soft infrastructure to the functioning of real markets, light touch regulation led directly to the financial crisis. We need the right regulation, we cannot leave it to the market, to self-police.

Now this is very important as we contemplate the deflating housing sector. As a nation we have been allured by the three lies.

But let’s be clear. Our property and finance sector is not unique or different. The market is subject to a host of vested interests from Government, to construction, to finance, all worshipping the free market that exploits unfairly. And we absolutely need the right – and better checks and balances to ensure fairness and equity. Self-regulation and light touch regulation are not going to do it.

The Australian Prudential Regulation Authority (APRA) has released an information paper to assist authorised deposit-taking institutions (ADIs) to meet their obligations under the Banking Executive Accountability Regime (BEAR).

The BEAR, which establishes heightened standards of accountability among ADIs and their most senior executives and directors, came into force for the largest banks from 1 July.

It will apply to all other ADIs from 1 July 2019. The regime was established under legislation and is administered and enforced by APRA.

The information paper, based on APRA’s experience in implementing the regime for the largest banks, is aimed at assisting all other ADIs prepare to implement the BEAR, and helping the largest ADIs refine and embed the regime.

It clarifies APRA’s expectation of how an ADI can effectively implement the accountability regime on matters including:

identifying and registering accountable persons;

creating and submitting an accountability statement for each accountable person, and an accountability map for the ADI;

establishing a remuneration policy requiring that a portion of accountable persons’ variable remuneration be deferred for a minimum of four years, and reduced commensurate with any failure to meet their obligations; and

notifying APRA of any accountability-related changes or breaches of accountability obligations.

The information paper also includes questions and answers based on some of the issues commonly raised by ADIs during implementation. APRA will address enforcement-related issues, including the disqualification of accountable persons and civil penalties under the BEAR, in a subsequent paper.

APRA Chairman Wayne Byres said the BEAR presented an opportunity for a major strengthening of accountability among the directors and senior executives of ADIs.

“Many problems that have arisen in the financial system over recent years have had, at their heart, organisational complexity and diffused responsibility. By effectively implementing the BEAR, ADIs will genuinely enhance their governance and risk management through much clearer understanding and agreement on individual accountabilities,” Mr Byres said.

Westpac CEO Brian Hartzer faced the firing line of a parliamentary committee where he was asked to explain why branch staff are still required to meet sales targets; via InvestorDaily.

Most of the questions directed at Brian Hartzer by the House of Representatives standing committee on Thursday were about the royal commission.

Labor MP Matt Thistlewaite read from the witness statement of Carol Separovich, Westpac’s head of performance & rewards, who appeared before the Hayne inquiry in May.

“She said there is still a variable reward and an opportunity for employees to gain financial advantage from elements that are at risk and related to certain targets,” Mr Thistlewaite said. “What proportion of frontline staff salary is at risk?”

Mr Hartzer confirmed that for Westpac personal bankers it’s about 10 to 15 per cent.

“If you’ve got someone who is in a very focused sales role like a home finance manager, it’s probably around 20 per cent,” he added.

Mr Thistlewaite moved on to Westpac’s key performance indicators (KPIs), as outlined in Ms Separovich’s witness statement.

“For personal bankers, this includes things like total branch first-party net home loan and deposits growth, total net growth percentage of branch customers, referrals to specialist business partners such as wealth business premiums,” he said “Those referral opportunities and growth KPIs are still there.”

“In terms of credit card products, one KPI is cards systems growth. It appears to me that you’ve done a bit of window dressing but there is still that notion within branches, within banks that an element of your job is to push these products onto customers and if you do it and do it well you’ll be rewarded for it.”

Mr Hartzer rejected this characterisation of the bank.

“I certainly wouldn’t characterise it as window dressing. We are a commercial organisation. We want to grow. The strategy here is around encouraging people to consolidate their business with us.

“We are trying to get that balance of rewarding people who do a great job and look after customers and allow them to benefit from that success. But at the same time not create perverse incentives that cause them to push a product onto someone who doesn’t need it. We have changed the structures so that people are agnostic about the products they are talking to customers about.”

Commissioner Hayne’s interim report, released last month, questioned the role of incentive remuneration and bonus cultures within financial services: “If customer facing staff should not be paid incentives, why should their managers, or those who manage the managers? Why will altering the remuneration of front-line staff effect a change in culture if more senior employees are rewarded for sales or revenue and profit?

The chief executives of ANZ and NAB will appear before the inquiry on Friday, 12 October and Friday, 19 October, respectively.

The ABA says Australia’s banks will change the Banking Code of Practice to overhaul the way they manage a customer’s estate when they have died and end ‘fees for no service’ across the industry. Further to this they will seek new legislation to end grandfathered payments and trail commissions for financial advisers.

Surely this should be just been good business practice, but at least it will be incorporated in the Banking Code now!

These reforms are the first of several key changes in response to the Royal Commission and include:

Ending ‘fees for no service’ – Banks will change the way they manage ongoing financial advice, proactively contacting customers to confirm what advice is required and only charging for what is provided.

Changing the Banking Code of Practice to improve the way banks manage a deceased estate – Once notified of a customer’s death, banks will proactively identify fees that are for products and services that can no longer be provided in the circumstances, stop charging those fees and refund any paid.

Seeking new legislative changes to the Future of Financial Advice (FOFA) reforms to remove all legislative provisions that allow grandfathered payments and trail commissions in financial advice.

CEO of the Australian Banking Association Anna Bligh said these initiatives addressed two of the strongest concerns raised by the Royal Commission’s Interim Report.

“It has always been unacceptable for any organisations to charge fees without providing a service,” Ms Bligh said.

“This announcement will put beyond the shadow of a doubt that this practice has no place in Australia’s banking industry.

“Banks will change the way they manage a customer’s account, proactively contacting them to confirm what services are required for their investments and only charging for those provided.

“This issue of charging fees without service, particularly when customers have recently died, was raised during the Royal Commission and identified as unacceptable.

“When someone loses a loved one, they need support and compassion as they finalise their loved one’s financial affairs. Charging ongoing advice fees to dead people is clearly unacceptable,” she said.

Right now banks are working with customers to refund those charged a fee where no service was provided. Latest ASIC data indicates customers will receive more than $1 billion in refunds.

“In addition to these changes the industry is supporting legislation to remove grandfathering provisions in relation to financial advice,” Ms Bligh said.

“This is another important piece in the puzzle of ensuring there are no conflicts for advisers,” she said

I have to say I am getting a little tired of all the various industry bodies coming out and trying to defend their corner – Mortgage Brokers of course came in for some severe criticism in the Royal Commission, especially about conflicted advice in the context of commissions. Remember the bigger the loan they write, the more they get paid!

The industry association has responded to a suggestion made by Commissioner Hayne that the payment of value-based commissions to brokers “might” be breaching NCCP obligations.

Executive director of the Finance Brokers Association of Australia (FBAA) Peter White has rejected claims made by Commissioner Kenneth Hayne in the interim report of the Royal Commission into Misconduct in the Banking, Superannuation and Financial Services Industry.

Commissioner Hayne alleged that lenders paying value-based upfront and trail commissions could be in breach of section 47(1)(b) of the National Consumer Credit Protection Act (NCCP).

Section 47(1)(b) states that licensees must “have in place adequate arrangements to ensure that clients are not disadvantaged by any conflict of interest that may arise wholly or partly in relation to credit activities engaged in by the licensee or its representatives”.

However, Mr White said that the interim report did not find any systemic evidence to suggest that conflict of interest in the payment of commissions to brokers directly disadvantages clients.

The FBAA director added that he believes licensees already have “adequate arrangements” in place to prevent conflicts of interest.

Mr White added: “The commissioner pointed out that a breach of the NCCP is not an offence or open to civil penalty.

“I would argue that the cancellation or suspension of a broker’s licence by ASIC is a substantial penalty in itself.”

Mr White also sought to dismiss concerns raised by the commissioner over the number of loans submitted via the broker channel with higher loan-to-value ratios (LVRs).

“It’s the broker’s duty to put the client’s interest first and to meet, if not exceed, their expectations,” the FBAA executive director said.

“In meeting client needs, brokers are often asked to source higher leverage loans to appropriately support their needs, taking into account a client’s debt levels and loan-to-valuation ratios.

“It’s a broker’s ability to source a specific loan product to suit their client’s specific needs that gives us a market advantage.”

Mr White concluded by stating that brokers were at the forefront of efforts to improve service delivery and remuneration structures.

The FBAA echoed comments made by the Mortgage & Finance Association of Australia (MFAA), which told its members: “The self-regulatory approach the industry is taking through the [Combined Industry Forum] remains the best way to improve customer outcomes, standards of conduct and culture, while preserving and promoting a vibrant and competitive mortgage broking industry that encourages consumer choice.”

Submissions in response to the commission’s interim report can be made on the royal commission website and must be received no later than 5pm on 26 October 2018.

The commission will release a final report, which will include the topics of the fifth, sixth and seventh rounds of hearings (focusing on superannuation, insurance and “policy questions arising from the first six rounds”, respectively) by 1 February 2019.

Are you a major financial institution looking to profit from misconduct? The corporate regulator is open to negotiations.

There are very few surprises in Hayne’s interim report. Fortunately, the document backs up what I’ve long suspected – that ASIC is a toothless tiger of a regulator when it comes to the big end of town; always happy to hit small business where it hurts but equally glad to negotiate bargain basement prices on infringement notices for the big corporates.

Seventy per cent of all of ASIC’s enforcement outcomes come from the Small Business Compliance and Deterrence Team, which focuses very heavily on the prosecution by in-house ASIC legal teams of strict liability offences, primarily in relation to the failure of directors to assist liquidators.

When it comes to regulating the big four banks, however, it’s a different story. Negotiation, rather than prosecution, is the strategy.

As Hayne states in his report: “ASIC issued infringement notices to the major banks as the outcome agreed with the bank.”

We have already seen plenty of evidence of this during the royal commission hearings throughout the year.

Hayne pulls no punches in his interim report, blasting the nonchalant regulator: “When deciding what to do in response to misconduct, ASIC’s starting point appears to have been: How can this be resolved by agreement?

“This cannot be the starting point for a conduct regulator. When contravening conduct comes to its attention, the regulator must always ask whether it can make a case that there has been a breach and, if it can, then ask why it would not be in the public interest to bring proceedings to penalise the breach. Laws are to be obeyed. Penalties are prescribed for failure to obey the law because society expects and requires obedience to the law.”

But the big banks were clearly too big to obey the book and ASIC was unwilling to throw it at them.

If ASIC has a reasonable prospect of proving contravention, Hayne said, then the starting point must be that the consequences of contravention should be determined by a court.

But the courtroom is an unfamiliar environment for the corporate watchdog. It does its best work around the negotiating table.

Over the 10 years to 1 June 2018, ASIC’s infringement notices to the major banks have amounted to less than $1.3 million. By contrast, in a single year (the year ending 30 June 2017) CBA declared a profit about 7,000 times greater – $9.93 billion (net profit after tax on a statutory basis).

Between 1 January 2008 and 30 May 2018, ASIC commenced 1,102 proceedings, an average of about 110 per year. Of those, more than half (587) were administrative proceedings, which include disqualification or bans on individuals from the industry; revocation, suspension or variation of a licence; and public warning notices.

“That is, they were outcomes carried out in-house by ASIC and not through the courts, though they may be appealed to the Administrative Appeals Tribunal,” Hayne states in his interim report.

“In that time, ASIC commenced 238 criminal proceedings and 277 civil proceedings, and accepted 194 enforceable undertakings. Of those proceedings, just 10 were against major banks.”

Hayne found that in a number of cases where ASIC acted against major banks in the form of infringement notices, the regulator included the following disclaimer in its media release: ‘The payment of an infringement notice is not an admission of guilt in respect of the alleged contravention.’

Crikey!

Another important point in Haynes report supports the arguments I made in an earlier editorial, that it is the banks, not the regulator, who really call the shots.

“Too often, entities have been treated in ways that would allow them to think that they, not ASIC, not the Parliament, not the courts, will decide when and how the law will be obeyed or the consequences of breach remedied,” Hayne states.

“Attitudes of this kind have not been discouraged by ASIC’s approach to the implementation of new provisions of financial services laws. Too often, ASIC has permitted entities confronted with new provisions, of which ample notice has been given (such as the unfair contract terms provisions), to take even longer to implement the provisions than the legislation provided.”

ASIC has been aiding the misconduct in financial services by its own weak and possibly even corrupt preference for deal making. If things are to change, ASIC will need to litigate rather than negotiate.

Of course, ASIC, like any other government agency or department, will cry for more resources. Hayne is across this too.

“I do not accept that the appropriate response to the problem of allocating scarce resources is for a regulator to avoid compulsory enforcement action and instead attempt to settle all delinquencies by agreement,” he said.

Hayne knows that ASIC needs to change its ways but is yet to be convinced that this can happen. For several reasons.

“First, there is the size of ASIC’s remit,” he said.

“Second, there seems to be a deeply entrenched culture of negotiating outcomes rather than insisting upon public denunciation of and punishment for wrongdoing.

“Third, remediation of consumers is vitally important but it is not the only relevant consideration. Fourth, there seems no recognition of the fact that the amount outlaid to remedy a default may be much less than the advantage an entity has gained from the default.

“Fifth, there appears to be no effective mechanism for keeping ASIC’s enforcement policies and practices congruent with the needs of the economy more generally.”