S&P Global Ratings has just come out with a significant comment on “some weaknesses in the effectiveness of regulation in the banking sector, and the conduct, governance, and risk appetite shown by Australian banks”. Finally!!

The negative rating outlooks on systemically-important Australian banks reflect pressures on the Australian sovereign creditworthiness (Commonwealth of Australia; AAA/Negative/A-1+) and a possible tempering of our current highly supportive opinion concerning the Australian government’s tendency to support banks.

During the past quarter, we revised our economic risk trend for the Australian banking industry to positive from stable. This reflects our expectation that the trend of an orderly unwinding of economic imbalances, including for high property prices and private sector indebtedness, should continue for at least the next year.

By contrast, we recently negatively revised our view of the Australian banking sector’s industry risk. In our view, developments over the past two years in the Australian banking sector, including information coming out of hearings at the ongoing Royal Commission, highlight some weaknesses in the effectiveness of regulation in the banking sector, and the conduct, governance, and risk appetite shown by Australian banks.

Many entrenched motivations for misconduct in the banking sector have been uncovered by the ongoing royal commission. Not least are the conflicts of interest inherent in the major Australian banks providing financial, insurance and mortgage advice and selling related products.

The banks, most recently the Commonwealth Bank (following the lead of ANZ and NAB), are already separating their wealth-management arms – services such as mortgage broking, insurance and financial planning and advice – in a bid to resolve these conflicts of interest.

These restructures are a step in the right direction. But they are not enough to overcome the fundamental problem: the banks’ sales-driven culture. This goes much deeper and seemingly pervades all of their operations, as the royal commission has highlighted.

The nature of this problem lends weight to an Australian Securities and Investments Commission (ASIC) proposal to embed regulatory staff in the major banks to help change the culture.

Bankers’ priorities laid bare

The evidence made public by the forensic analysis of Rowena Orr QC, counsel assisting the commission, has revealed many instances of the banks’ “toxic” culture. It’s one that puts profits and growth – in particular their associated incentive systems – above customers’ interests.

This has been evident from the outset. The first round of hearings in March 2018 revealed allegations of significant cash bribes, forged signatures and manipulation of incentives within NAB’s “Introducer Program”. This generated billions of dollars in home loans for the bank, with introducers paid 0.4-0.6% of home loan totals.

We have had belated “apologies” to customers who were treated unfairly or, worse, fell victim to unscrupulous or wrongful behaviour; admissions that the banks breached their own codes of conduct; and assurances that changes in governance systems aimed at improving culture have been made or will be. Yet the banks are still in denial that systemic cultural issues have been at play or persist in their organisations.

A stark example is provided in the evidence of Rabobank executive Bradley James at the most recent hearings that dealt with issues of farming finance. Orr questioned James about a A$3 million loan made on the advice of a manager of this rural lender to a Queensland grazing family, the Brauers. They had no ability to repay it. The motivation for the manager was to meet his lending KPIs to earn a bonus.

Asked whether he saw any difficulty with that from a customer perspective, James’s response was: “Absolutely not!” This shows a complete failure to understand the bank’s incentive structure – linking staff bonuses to the number of loans brought in – and the culture that goes with it as a potential source of misconduct.

James defended the bank’s system, saying it enabled the business to grow. This demonstrates that, in putting profits and growth ahead of customers’ needs, banking culture is out of touch with community expectations and societal values.

Regulators must step in

Little wonder, then, that trust in the financial sector is at an all-time low. ASIC chair James Shipton speaks of a “trust deficit”.

Shipton is seeking government funding to embed specialist ASIC supervisors in the major banks to help drive cultural change and rebuild trust. This should be done, signalling as it does a new, more intrusive regulatory style.

However, ASIC should do more. It needs to take enforcement action. Most notably this would include prosecution in cases of criminal wrongdoing by the banks and their top executives. The latter have been conspicuously absent at the royal commission, raising important questions about bank accountability.

Another corporate regulator, the Australian Competition and Consumer Commission (ACCC), last month brought criminal proceedings against ANZ and several other companies and individuals over an alleged cartel arrangement. Commentator Nathan Lynch observed that, irrespective of the outcome, one message reverberates: senior management accountability:

Governments and regulators have had enough of financial services firms that are still talking about improving culture and conduct. A decade on from the financial crisis … they now want to see a healthy dose of fear and respect in the market.

Regulators are now at the point where they’re saying, ‘It’s impossible for things of this magnitude to happen without the people right at the top knowing what was going on.’

If ASIC also took such action, it would go a long way to overcoming concerns about an accountability deficit for the scandals and wrongdoing. This could be a catalyst for real cultural change in the industry to reduce misconduct in the future.

Why isn’t restructuring enough?

As for the current bank restructures, certain aspects are problematic.

In the first place, not all will result in a full separation of their businesses. The CBA will split off its wealth management, mortgage broking and insurance businesses, but retain its financial advice business. ANZ has sold its wealth management business to IOOF, but will not sell its life insurance business.

In addition, the banks remain keen to distribute products to retail customers. For example, ANZ’s sale to IOOF includes a 20-year deal to make IOOF super and investment products available to its retail customers.

These moves raise concerns that, despite these demergers, conflicts of interest and the banks’ failure to act in customers’ interests will continue.

At a minimum, Shipton’s plan to put ASIC agents in banks is more important than ever when the indications are that the banks cannot be left to self-regulate.

Author: Vicky Comino Lecturer in Corporations Law and Regulation of Corporate Misconduct, The University of Queensland

ASIC has banned former National Australia Bank branch manager, Rabih Awad, from engaging in credit activities and providing financial services for seven years.

The ban is the result of an on-going ASIC investigation, following a breach report lodged by NAB alleging that bank employees in the greater western Sydney area were accepting false documents in support of loan applications and falsely attributing loans as having been referred by NAB introducers in order to obtain undue commissions.

ASIC found that Mr Awad recklessly gave NAB information and documentation in loan applications that was false or misleading. Mr Awad was found to have given NAB false payslips, letters of employment, and entered false referee contact details in NAB’s lending systems in multiple home loan applications.

A majority of the false documentation submitted to NAB by Mr Awad was provided to him by a real estate agent who was previously registered as a NAB Introducer.

ASIC also found that:

Mr Awad received the false documents directly from the NAB Introducer rather than the customer, in violation of NAB’s Introducer Program; and

on occasion, Mr Awad received false documents from the NAB Introducer via email to his personal email account, before forwarding the documents to his NAB email account and subsequently attaching them to various customers loan applications.

Mr Awad has the right to lodge an application for review of ASIC’s decision with the Administrative Appeals Tribunal.

Background

On 16 November 2017, NAB announced a remediation program for home loan customers after an internal review, prompted by whistleblower reports it had received, found that some home loans may not have been established in accordance with NAB’s policies.

NAB identified that around 2,300 home loans since 2013 may have been submitted with inaccurate customer information and/or documentation, or incorrect information in relation to NAB’s Introducer Program.

Mr Awad’s banning follows the permanent bans of former NAB employees, Danny Merheb and Samar Merjan (also known as Samar Awad) from engaging in credit activities and providing financial services (refer: 18-205MR).

ASIC says Commonwealth Bank of Australia (CBA) has entered into a court enforceable undertaking with ASIC in relation to their bank bill trading business and their participation in the setting of the Bank Bill Swap Rate (BBSW), a key benchmark and reference interest rate in the Australian financial system.

As part of the undertaking, CBA will pay $15 million to be applied to the benefit of the community and $5 million towards ASIC’s investigation and legal costs.

CBA will also engage an independent expert to assess changes CBA has made (and will make) to its policies, procedures, systems, controls, training, guidance and framework for the monitoring and supervision of employees and trading in Prime Bank Bills.

On 21 June 2018, the Federal Court in Melbourne imposed pecuniary penalties totalling $5 million on CBA for attempting to engage in unconscionable conduct in relation to BBSW. CBA admitted to attempting to seek to affect where BBSW set on five occasions in the period 31 January 2012 to 15 June 2012.

CBA also admitted that it failed to do all things necessary to ensure that they provided financial services honestly and fairly and that its traders were adequately trained.

Justice Beach of the Federal Court noted the terms of the court enforceable undertaking and, in imposing the pecuniary penalty of $5 million, stated ‘…that sum together with the other payments all totalling $25 million should be an adequate denouncement of and deterrence against the unacceptable trading behaviour of individuals within CBA that ought to have known better and a bank that ought to have better supervised its personnel.’

Background

ASIC commenced legal proceedings in the Federal Court against CBA on 30 January 2018 (refer:18-024MR), alleging that on three specific occasions between 31 January 2012 and October 2012, CBA traded in a manner that was unconscionable and created an artificial price and a false appearance with respect to the market for certain financial products that were priced or valued off BBSW.

This followed proceedings in the Federal Court against the Australia and New Zealand Banking Group (ANZ) on 4 March 2016 (refer: 16-060MR), against the Westpac Banking Corporation (Westpac) on 5 April 2016 (refer: 16-110MR) and against National Australia Bank (NAB) on 7 June 2016 (refer: 16-183MR).

On 10 November 2017, the Federal Court made declarations that each of ANZ and NAB had attempted to engage in unconscionable conduct in attempting to seek to change where the BBSW set on certain dates and that each bank failed to do all things necessary to ensure that they provided financial services honestly and fairly. The Federal Court imposed pecuniary penalties of $10 million on each bank.

On 20 November 2017, ASIC accepted enforceable undertakings from ANZ and NAB which provides for both banks to take certain steps and to pay $20 million to be applied to the benefit of the community, and that each will pay $20 million towards ASIC’s investigation and other costs (refer: 17-393MR).

On 24 May 2018, the Federal Court found that Westpac engaged in unconscionable conduct under s12CC of the Australian Securities and Investments Commission Act 2001 (Cth) by its involvement in setting BBSW on four occasions (refer: 18-151MR). A further hearing of this proceeding on penalty and relief will be held on 12 October 2018.

In July 2015, ASIC published Report 440, which addresses the potential manipulation of financial benchmarks and related conduct issues.

The Government has recently introduced legislation to implement financial benchmark regulatory reform and ASIC has consulted on proposed financial benchmark rules.

On 21 May 2018, the new BBSW methodology commenced (refer: 18-144MR). The new BBSW methodology calculates the benchmark directly from market transactions during a longer rate-set window and involves a larger number of participants. This means that the benchmark is anchored to real transactions at traded prices.

If there is a breach of the undertaking entered into by CBA, then under the ASIC Act, ASIC can apply for orders from the court to enforce compliance.

Customer Executive Regional and Agriculture, Julie Rynski, said it has been a difficult time for people in the affected areas, who are facing severe drought conditions.

“As Australia’s largest Agribusiness bank, we are acutely aware of the challenges and unpredictability of life on the land and the impact of drought on NAB customers, employees and the wider community,” Ms Rynski said.

“Anyone who needs assistance or advice should contact their local banker so we can discuss their circumstances and determine the best way to help.”

Measures that may be available to eligible customers include:

Extension of loan terms, consideration of restructure of loan repayments to interest only and waiver of all associated extension/restructure fees;

Credit card and personal loan relief where appropriate;

Suspension of home and personal loan repayments;

Waiving costs and charges for early withdrawal of Term Deposits (including Farm Management Deposits);

Waiving home loan and personal loan application fees; and

Provision of support and counselling through NAB’s Employee Assistance Program

ASIC has accepted court enforceable undertakings from the Commonwealth Bank of Australia and Australia and New Zealand Banking Group under which the banks have agreed to change the way they distribute superannuation products to their customers.

ASIC investigated CBA’s distribution of its Essential Super product and ANZ’s distribution of its Smart Choice Super and Pension product (Smart Choice Super) through bank branches. ASIC found a common practice of offering those products to customers at the conclusion of a fact-finding process about customers’ overall banking arrangements.

CBA’s fact-finding process was called a ‘Financial Health Check’. CBA staff also sometimes helped customers roll over their other superannuation into the Essential Super account at the time of distribution.

ANZ’s fact-finding process was called an ‘A-Z Review’.

ASIC was concerned that the proximity between the fact-finding process and the discussion about Essential Super or Smart Choice Super was leading CBA staff and ANZ staff to provide personal advice to customers about their superannuation. Branch staff for both CBA and ANZ were only authorised to provide general advice.

Stricter consumer protection laws apply to financial services licensees when their representatives give personal advice about complex financial products such as superannuation than when they provide general advice about those products. This includes the requirement, with personal advice, to give a customer a Statement of Advice and to act in the customer’s best interests. People who give personal advice about complex products are also required to meet higher training standards.

ASIC was concerned that customers may have thought, due to the proximity of the fact-finding process to the offer of Essential Super or Smart Choice Super, that the CBA branch staff or the ANZ branch staff were considering risks specific to the customer when this was not the case.

These court enforceable undertakings prevent CBA from distributing Essential Super in conjunction with a Financial Health Check and ANZ from distributing Smart Choice Super in conjunction with an A-Z Review. They also require CBA and ANZ to each make a $1.25 million community benefit payment. If there is a breach of the undertaking ASIC can, under the ASIC Act, apply for orders from the court to enforce compliance.

CBA chose to suspend the distribution of Essential Super in CBA branches in October 2017.

‘ASIC will continue to proactively monitor how complex financial products such as superannuation are sold,’ ASIC Deputy Chair Peter Kell said.

ASIC’s actions underline the importance for financial services licensees to ensure that customers understand the nature of advice they are receiving about their superannuation.

ASIC’s investigation arose following a surveillance conducted in relation to CBA’s distribution of its retail superannuation product, Essential Super and ANZ’s distribution of its retail superannuation product, Smart Choice Super.

These actions are part of ASIC’s Wealth Management Project. The Wealth Management Project was established in October 2014 to lift the standards of major financial advice providers. The Wealth Management Project focuses on the conduct of the largest financial advice firms (NAB, Westpac, CBA, ANZ, Macquarie and AMP).

ASIC says Perth man Mr Peter Lachlan McDonald has been sentenced in the Perth Magistrates’ Court to 21 months’ imprisonment following an investigation by ASIC into his brokering of motor vehicle finance contracts while an employee of Get Approved Finance.

The sentence was fully suspended for 12 months upon Mr McDonald paying a $5000 bond to the Court. The sentence took into account Mr McDonald’s guilty plea to seven charges of giving false information to Esanda (a business then owned by ANZ) and one fraud charge.

ASIC Deputy Chair Peter Kell said Mr McDonald’s actions abused the trust of his clients, who are entitled to expect brokers to act honestly and in their best interests.

‘Loan fraud, which often involves an intermediary like a finance broker, is a particular focus of ASIC. We are actively working to improve standards in the broking industry and warn anyone tempted to deceive lenders or mislead customers that they will be held to account.’

Since becoming the national regulator of consumer credit in 2010, ASIC has achieved significant loan fraud outcomes resulting in 17 convictions for various related offences. Over this time, 83 individuals or companies have also been banned from providing credit services or precluded from holding a credit licence.

Mr McDonald was sentenced on 5 July 2018. The Commonwealth Director of Public Prosecutions prosecuted the matter.

Background

ASIC’s investigation found that between January 2013 and April 2013, Mr McDonald, in the course of brokering four motor vehicle finance contracts, provided the lender Esanda (a business then owned by ANZ) with information that falsely represented that persons, who had in fact only agreed to be loan guarantors, were the applicant borrowers who would ultimately own the vehicle to be financed. It is alleged that Mr McDonald had previously advised his clients, who had poor credit histories, that they would be approved for vehicle finance if their loan applications were supported by guarantors.

In two further loan applications, Mr McDonald is alleged to have provided information to Esanda that falsely represented that insurance quotes were issued insurance policies, knowing that Esanda required all financed vehicles to be insured before loans were approved. In one additional application it is alleged that Mr McDonald inserted what purported to be his client’s signature on an extended warranty and submitted that document to Esanda (the client having agreed to purchase the extended warranty).

In relation to one of the seven loan applications, Mr McDonald is also alleged to have acted fraudulently by artificially interposing a third party vendor while representing to his client that the vehicle being purchased on credit was being sourced directly from a car dealership. In doing so, he gained a pecuniary benefit for himself.

In July 2015, ASIC permanently banned Mr McDonald and a colleague from engaging in credit activities and providing financial services (refer: 15-189MR).

At the time of the conduct, Get Approved Finance was the trading name and operated under the Australian credit licence of West Australian-based finance broker Jeremy (WA) Pty Ltd. The company was deregistered in September 2017.

A number of other former Get Approved Finance brokers have also been banned by ASIC from both the credit and financial services industry (refer: 15-374MR, 16-116MR, 16-132MR).

In October 2015, ANZ agreed to compensate more than 70 borrowers for car loans organised by Get Approved Finance (refer: 15-312MR).

The BIS is worried by the current low interest rate environment, and in a new report by a committee chaired by Philip Lowe warn of the impact on financial stability across the financial services sector, with pressures on banks via net interest margins, and on insurers and super funds. They warn that especially in competitive markets, risks rise in this scenario. Low interest rates may trigger a search for yield by banks, partly in response

to declining profits, exacerbating financial vulnerabilities.

In addition, keeping rates low for longer may create the need to lift rates sharper later with the risks of rising debt costs and the broader economic shock which follows. A salutatory warning!

Interest rates have been low in the aftermath of the Global Financial Crisis, raising concerns about financial stability. In particular, the profitability and strength of financial firms may suffer in an environment of prolonged low interest rates. Additional vulnerabilities may arise if financial firms respond to “low-for-long” interest rates by increasing risk-taking.

The decade following the Great Financial Crisis (GFC) has been marked by historically low interest rates. Yields have begun to recover in some economies, but they are expected to rise only slowly and to stabilise at lower levels than before, weighed down by a combination of cyclical factors (eg lower inflation) and structural factors (eg productivity, demographics). Moreover, observers put some weight on the risk that interest rates may remain at (or fall back to) very low levels, a so-called “low-forlong”

scenario. An environment characterised by “low-for-long” interest rates may dampen the profitability and strength of financial firms and thus become a source of vulnerability for the financial system. In addition, low rates could change firms’ incentives to take risks, which could engender additional financial sector vulnerabilities.

In light of these concerns, the Committee on the Global Financial System (CGFS) mandated a Working Group co-chaired by Ulrich Bindseil (European Central Bank) and Steven B Kamin (Federal Reserve Board of Governors) to identify and provide evidence for the channels through which a “low-for-long” scenario might affect financial stability, focusing on the impact of low rates on banks and on insurance companies and private pension funds (ICPFs).

Now a report by the Committee on the Global Financial System finds that low market interest rates for a long time could have implications for financial stability as well as for the health of individual financial institutions. Philip Lowe, Chair, Committee on the Global Financial System and Governor, Reserve Bank of Australia said:

“The adjustment of financial firms to a low interest rate environment warrants further investigation, especially when low rates are associated with a generalised overvaluation of risky assets. I hope that this reports provides both a sound rationale for ongoing monitoring efforts and a useful starting point for future analysis”.

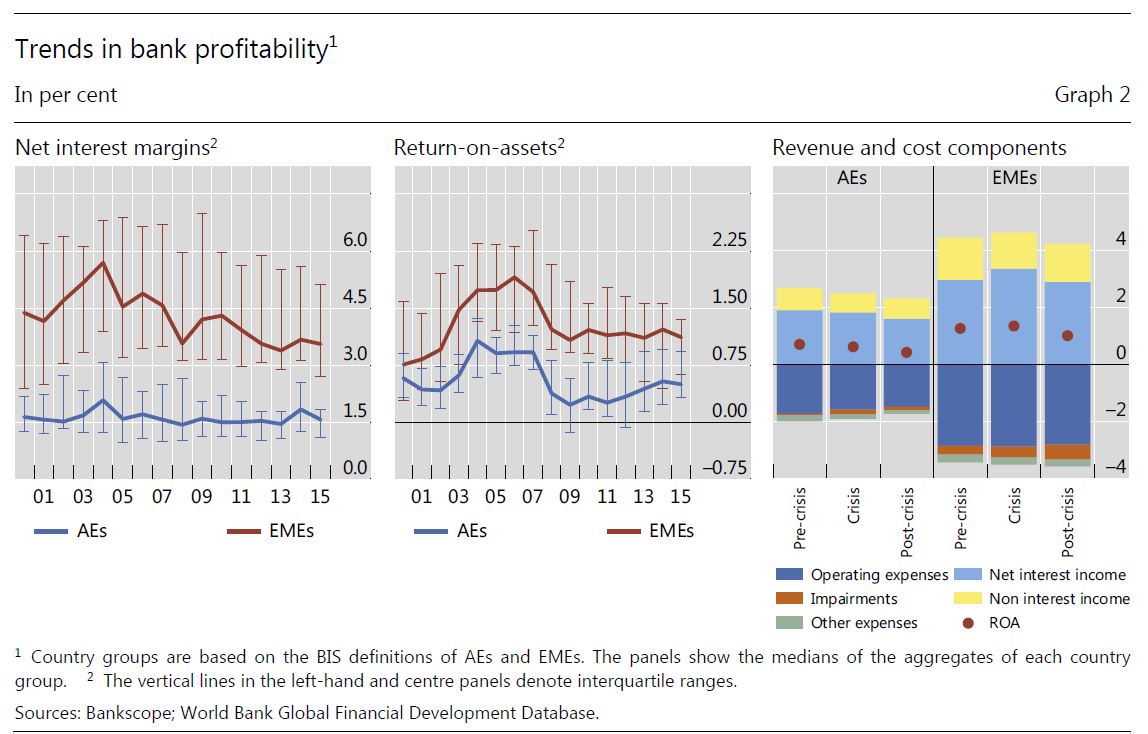

For banks, based on econometric evidence, simulation models, and reviews of past stress tests, the Working Group found considerable evidence that low interest rates and shallower yield curves depress net interest margins (NIMs). This effect was more pronounced for banks facing constraints on their ability to reduce deposit rates, for example, because of very low interest rates or strong competitive pressures. low rates might reduce resilience by lowering profitability, and thus the ability of banks to replenish capital after a negative shock, and by encouraging risk-taking. These effects can be expected to be particularly relevant for banks operating in jurisdictions where nominal deposit rates are constrained by the effective lower bound, leading to compressed net interest margins. For banks in emerging market economies (EMEs), such adverse effects might materialise not only as a result of low domestic interest rates but also as a consequence of “spillovers” from low interest rates in advanced economies (AEs), which can encourage capital inflows into EMEs, excessive local credit expansion, and heightened competitive pressures for EME banks.

Lower for longer would be harder on insurers and pension funds than on banks. Even though the CGFS analysis did not show that measures of firms’ financial soundness dropped significantly, prolonged low rates could still involve material risks to financial stability. In particular, a “snapback”, involving an unexpected sudden increase in market rates from currently low levels, could affect banks’ solvency and create liquidity issues for insurers and pension funds.

“A key takeaway is that, while a low-for-long scenario presents considerable solvency risk for insurance companies and pension funds and limited risk for banks, a snapback would alter the balance of vulnerabilities,”

Chair Philip Lowe, said.

“The first line of defence against these risks should be to continue to build resilience in the financial system by encouraging adequate capital, liquidity and risk management. But the report also underscores the need to monitor institutions’ exposures in a comprehensive way, including through stress tests.”

The CGFS is a central bank forum for the monitoring and analysis of broad financial system issues. It supports central banks in the fulfilment of their responsibilities for monetary and financial stability by contributing appropriate policy recommendations.

And insurance agents were able to exploit and target Aboriginal people because the industry isn’t fully regulated.

The cultural, economic and political arrangements that allow this to happen are called “practice architectures”. They include the complex language used to deceive consumers into buying unsuitable products, incentivised high pressures sales tactics, and a lack of care and concern for vulnerable consumers.

All of these aspects are within the scope of financial regulators. The funeral insurance industry can push dodgy products because no one is watching. Predatory financial practices will continue until governments and/or regulators do something about it.

Changing exploitative and predatory financial practices

To change predatory financial practices requires regulatory action to constrain the ability to exploit vulnerable consumers. Educating consumers about predatory financial practices and fostering critical thinking skills is also needed.

But financial literacy education alone is not enough when deliberate deception in financial products and services is permitted.

Research shows Indigenous Australians are too trusting in the role of government to regulate financial matters and can fall prey to predatory lenders. For example, the researchers found there was a belief the Australian Securities Investment Commission would check the accuracy of all prospectuses and that personal loan interest rates are legislated.

To ensure vulnerable consumers are protected requires a lot more than financial education. It requires regulation.

This meant an applicant going to a broker was more likely to end up with a larger mortgage over a longer term than one who dealt directly with their bank, a finding that was revealed in a review of the industry.

Consumers best interest must put be above those of the agents when it comes to insurance products and mortgages.

Much like how certified financial planners are now mandated under the corporations act to work in the best interest of their clients.

The royal commission has also revealed funeral insurance agents gave the appearance of being an Aboriginal organisation, while deliberating exploiting Aboriginal people.

Fixing the problem requires the Australian Securities Investment Commission to change the predatory financial practices so the financial landscape can operate ethically.

In the case of mortgage brokers, exploitative practices were encouraged based on the way brokers are remunerated. So how brokers are remunerated has been changed to align with the best interest of the client.

Selling insurance similarly has a number of cultural, social and financial elements that can be acted upon. There are the cultural aspects of what it means to be a broker, the economic incentives to push clients towards certain products, and social elements that encourage agents to put their own needs ahead of those wanting insurance to protect and cover their loved ones.

Together, these arrangements form practice architectures which make it possible to constrain the practices used in mortgage broking and the insurance industry. Different practice architectures are required to make possible other, non-predatory, methods of mortgage-broking and selling insurance.

Once what it means to be an ethical mortgage broker or an ethical funeral insurance agent becomes the norm, then the social and cultural concern for others’ well-being may be realised.

Predatory financial practices will not go away without effective regulation. The finance and insurance industry needs more effective regulation that forces higher ethical standards to be met in order to establish new financial practices.

This change can begin by asking whether the financial practices that have already been exposed are rational, reasonable, productive, sustainable, socially just or inclusive. And since they aren’t, what action can be taken to change the unjust financial practices? More and better regulation to protect consumers.

Author: Levon Ellen Blue Lecturer, Queensland University of Technology

ASIC says an investigation into loan fraud has resulted in a permanent ban of former National Australia Bank employees, Danny Merheb and Samar Merjan (also known as Samar Awad) from engaging in credit activities and providing financial services.

NAB alerted ASIC to the misconduct of its former employees, alleging that bank staff in the greater western Sydney area were accepting false documents in support of loan applications.

Mr Merheb was found to have recklessly given NAB false payslips, letters of employment, bank statements and statutory declarations in respect of home loan applications. Ms Merjan was found to have knowingly and recklessly given NAB false payslips and letters of employment in respect of personal loan and credit card applications.

The false information and documentation submitted by Mr Merheb and Ms Merjan were primarily provided to them by a third person who had no association with NAB.

ASIC also found that:

Mr Merheb falsely attributed a loan as being referred to NAB by an introducer who was a friend in order for the friend to receive commissions dishonestly;

Ms Merjan assisted the third person in the creation of two false documents, which she subsequently provided to NAB in support of lending applications; and

Ms Merjan was twice offered cash by the third person to process lending applications.

ASIC’s investigation is continuing.

Background

Mr Merheb and Ms Merjan were permanently banned on 29 June 2018. They both have the right to lodge an application for review of ASIC’s decisions with the Administrative Appeals Tribunal.

On 16 November 2017, NAB announced a remediation program for home loan customers after an internal review, prompted by whistleblower reports it had received which found that some home loans may not have been established in accordance with NAB’s policies.

NAB identified that around 2,300 home loans since 2013 may have been submitted with inaccurate customer information and/or documentation, or incorrect information in relation to NAB’s Introducer Program.