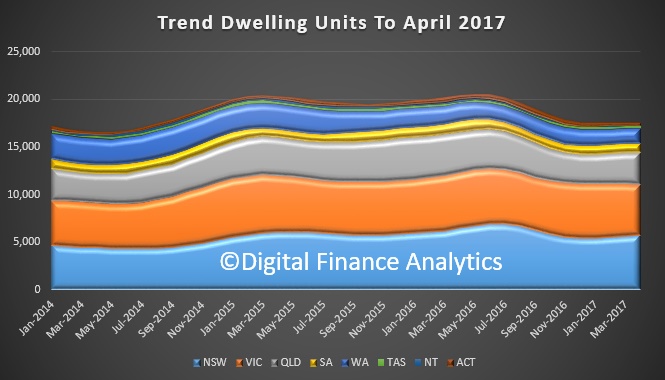

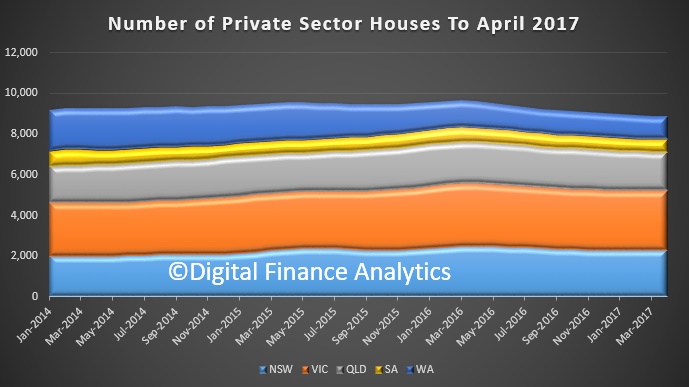

So NSW has perpetuated the “quick fix” approach to housing affordability, alongside taxing foreign investors harder and changes to planning. The removal of stamp duty concessions to property investors may slow that sector, but the fundamental issue is that supply is not the problem many claim it to be.

Lets see if first time buyer property values rise by the amount of the increased incentives, as has happened elsewhere.

Premier Gladys Berejiklian, Treasurer Dominic Perrottet and Minister for Planning and Housing Anthony Roberts announced the far reaching changes on which could save first homebuyers up to $34,360. The package includes:

- Abolishing all stamp duty for first homebuyers on existing and new homes up to $650,000 and stamp duty discounts up to $800,000. These changes, to be introduced on 1 July 2017, will provide savings of up to $24,740 for first homebuyers

- Abolishing the stamp duty charged on lenders’ mortgage insurance, which is often required by banks to lend to first homebuyers with limited deposits, providing a saving of around $2,900 on an $800,000 property

- Doubling the foreign investor surcharge from 4% to 8% on stamp duty and 0.75% to 2% on land tax

- Removing stamp duty concessions for investors purchasing off the plan

- Committing $3bn in infrastructure funding from Government, councils and developers to accelerate the delivery of new housing

- Fast-track approvals for well-designed terraces, townhouses, manor homes and dual occupancy by expanding complying development to include these dwelling types

- Greater use of independent panels for Councils in Sydney and in some regional areas to ensure development applications are done efficiently and to ensure the integrity of the planning process

- Measures to maintain the local character of communities

“I want to ensure that owning a home is not out of reach for people in NSW,” Berejiklian said.

“These measures focus on supporting first homebuyers with new and better targeted grants and concessions, turbocharging housing supply to put downward pressure on prices and delivering more infrastructure to support the faster construction of new homes.

“This is a complex challenge and there is no single or overnight solution. I am confident these measures will make a difference and allow us to meet the housing challenge for our growing State.”

Former Reserve Bank of Australia Governor Glenn Stevens advised the NSW Government in developing its housing affordability package. His report to Government was also released on Thursday.

“I would like to thank Mr Stevens for his valuable advice and insights during the development of this package,” Berejiklian said. “In particular, his advice about avoiding any unintended consequences on the market was greatly appreciated.”

Perrottet said the Government would take advantage of its strong Budget position to give a leg up to prospective first homebuyers while also investing more into targeted infrastructure to support housing growth throughout Sydney and parts of regional NSW.

“As a Government, we have always focused on supporting first homebuyers and this package takes it to the next level,” Perrottet said.

“We know how challenging it can be to enter the property market and are pleased to be providing even more financial support for people wanting to make their first purchase.”

Roberts said the package included measures to speed up planning processes to ensure developments get off the ground as quickly as possible.

“While we have done well to release an unprecedented amount of land over the last six years, we need to do better with our development application process to ensure we are keeping up with demand,” Roberts said.

“That is why we are simplifying complying development rules for greenfield areas and establishing specialist teams to help speed up the rezoning process for residential development, while maintaining the local character of communities.”