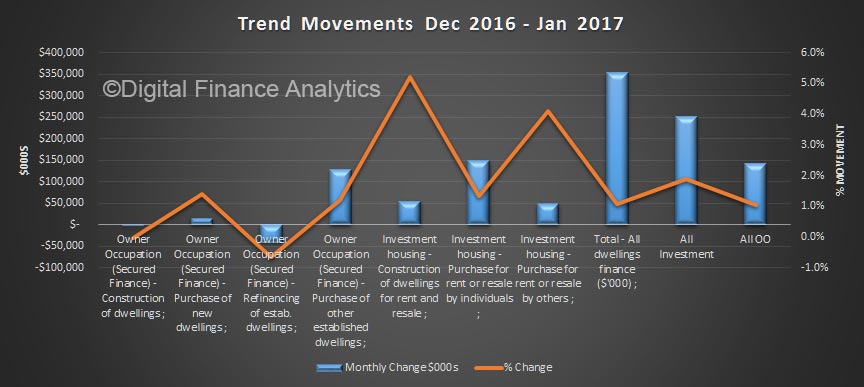

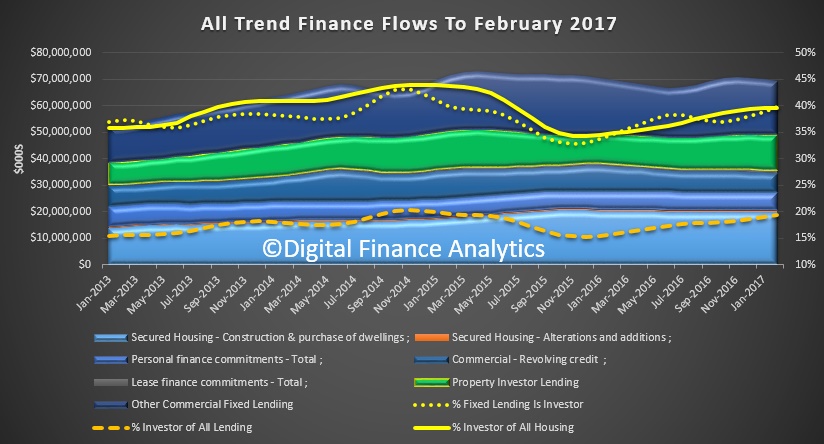

The ABS finalised their finance data today with the overall flows for February 2017. It is not pretty. Overall lending flows, in trend terms, which irons out some of the statistical bumps, shows an overall fall of 1% to $62.2 billion in the month.

Looking in more detail, lending for investment property rose 0.7% to $13 billion, whilst other fixed lending to business fell 2.9% to $20 billion. So overall productive business lending fell again. Not good for productive growth. Actually the bulk of investor lending was in Sydney and Melbourne, highlighting again the lopsided property market, and why investor lending needs real attention from regulators and Government.

As a result of this, the proportion of fixed business lending for investment housing rose again, to 39.7%, and the share of lending for housing investment rose to 19.4%, the highest it has been since 2015

The total value of owner occupied housing commitments excluding alterations and additions rose 0.2% in trend terms, and the seasonally adjusted series fell 0.5%.

The trend series for the value of total personal finance commitments fell 0.3%. Fixed lending commitments fell 0.6%, while revolving credit commitments rose 0.2%.

The seasonally adjusted series for the value of total personal finance commitments fell 3.8%. Fixed lending commitments fell 4.7% and revolving credit commitments fell 2.2%.

The trend series for the value of total commercial finance commitments fell 1.8%. Revolving credit commitments fell 3.2% and fixed lending commitments fell 1.5%.

The seasonally adjusted series for the value of total commercial finance commitments rose 1.8%. Revolving credit commitments rose 25.5%, while fixed lending commitments fell 2.8%.

The trend series for the value of total lease finance commitments rose 6.4% in February 2017 and the seasonally adjusted series fell 31.5%, after a rise of 73.6% in January 2017.

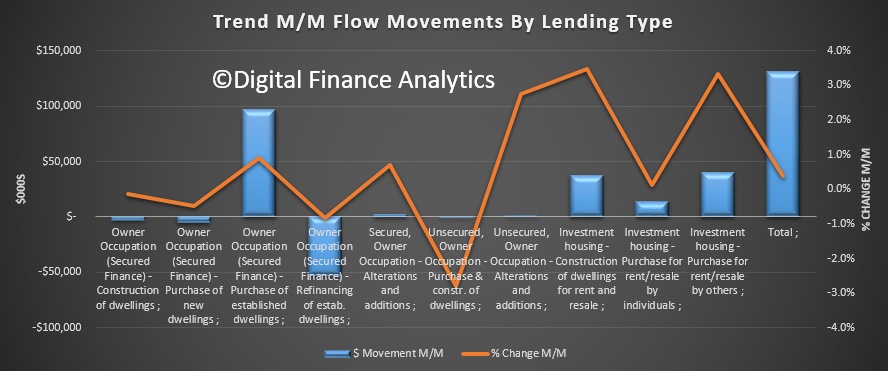

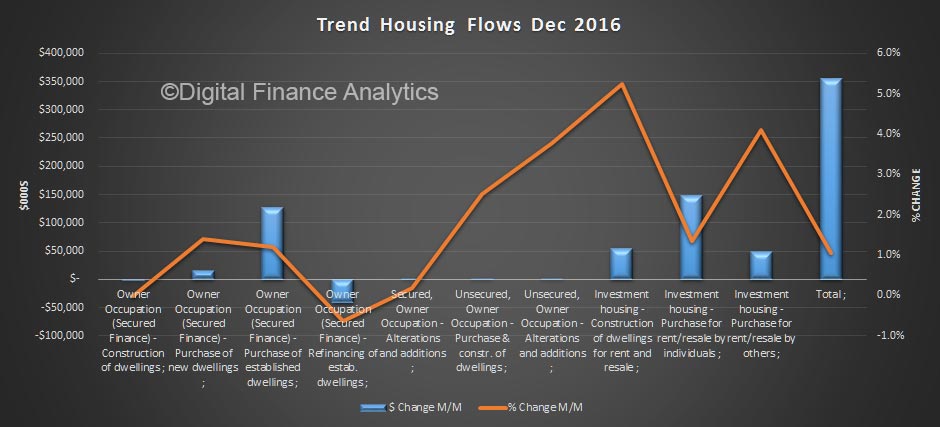

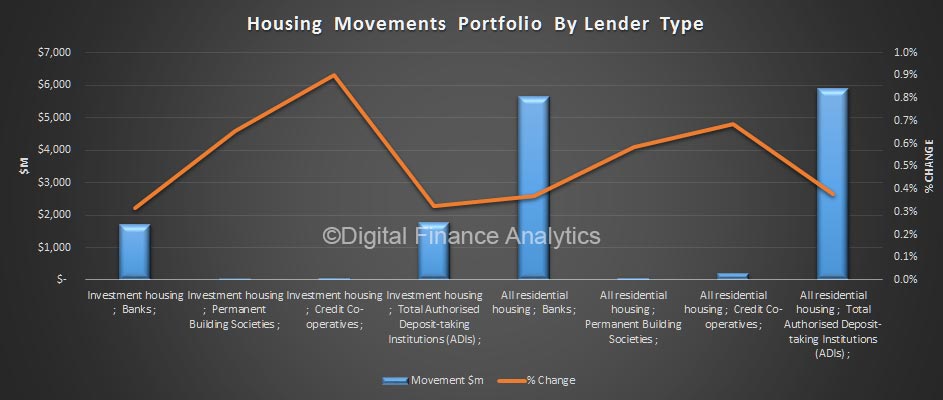

Finally, here are the movements within the housing sector, with falls in new construction and refinance, offsetting rises in investor lending and purchase of existing dwellings.

According to the ABS, the trend estimate of the value of total building work done fell 0.5% in the December 2016 quarter.

The trend estimate for the total number of dwelling units commenced also fell 1.5% in the December 2016 quarter following a fall of 1.5% in the September quarter.

The trend estimate of the value of new residential building work done was flat in the December quarter. The value of work done on new houses fell 0.7% while new other residential building rose 0.7%.

The trend estimate for new private sector house commencements fell 0.9% in the December quarter following a rise of 0.4% in the September quarter.

The trend estimate for new private sector other residential building commencements fell 1.7% in the December quarter following a fall of 3.2% in the September quarter.

The trend estimate of the value of non-residential building work done fell 1.7% in the December quarter.

The trend estimate for the total value of dwelling finance commitments excluding alterations and additions rose 0.4%. Investment housing commitments rose 0.7% and owner occupied housing commitments rose 0.2%. [DFA NOTE: They include owner occupied refinance in these numbers]

In seasonally adjusted terms, the total value of dwelling finance commitments excluding alterations and additions fell 2.7%.

But within the moving parts there are interesting observations – as usual we will focus on the trend series, which irons out some of the statistical bumps, though others will rush to comment on the 13% fall in investor loan flows from the previous month.

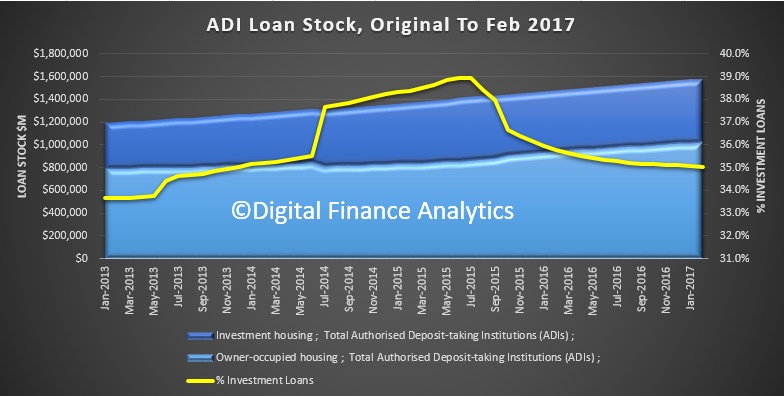

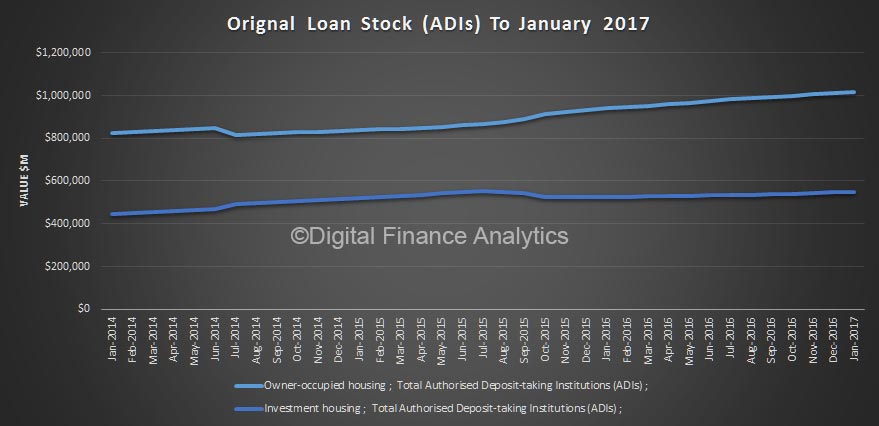

But looking first at ADI loan stock, overall balances rose 0.44% in the month to $1.57 trillion. Investor loans comprise 35% of the total, just down a little, in original terms.

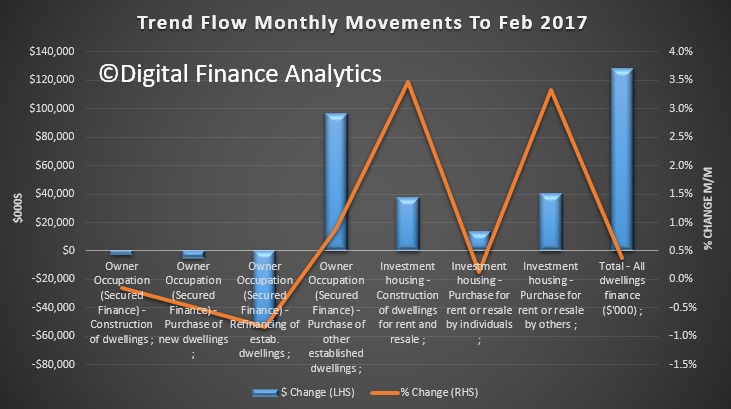

Turning to the trend lending flows, total flows grew by 0.38% compared with the previous month, up $128 million. Within that, refinance fell to 18.7% of flows, down 0.83% or $50 million, owner occupied loans rose 0.65%, up $89 million and investment loans rose 0.69% or $91 million.

The main rise in the owner occupied sector was the purchase of established dwellings, whilst funding for new purchases and construction both fell a little. All categories of investor lending rose.

The HIA highlights that

the number of loans to owner occupiers constructing or purchasing new homes during February 2017 rose in just two states – South Australia (+6.5 per cent) and Queensland (+3.7 per cent). Compared with a year earlier, the largest reduction in lending volumes affected the Northern Territory (-63.8 per cent), followed by the ACT (-23.4 per cent) and New South Wales (-9.7 per cent). There were also falls in Western Australia (-8.7 per cent), Victoria (-2.0 per cent) and Tasmania (-1.7 per cent).

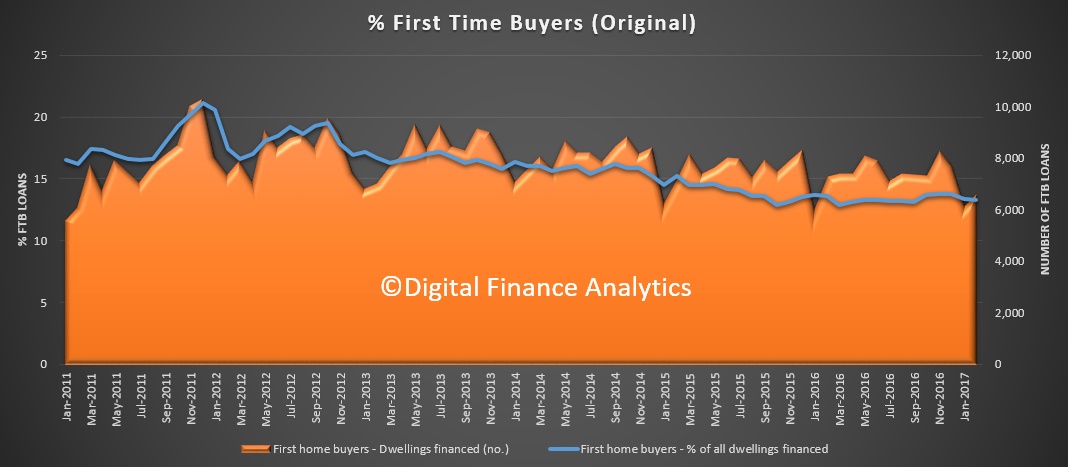

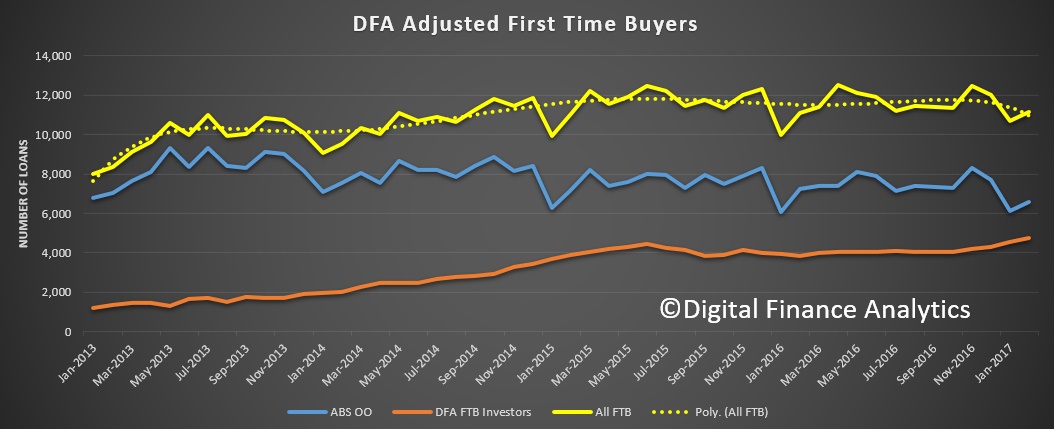

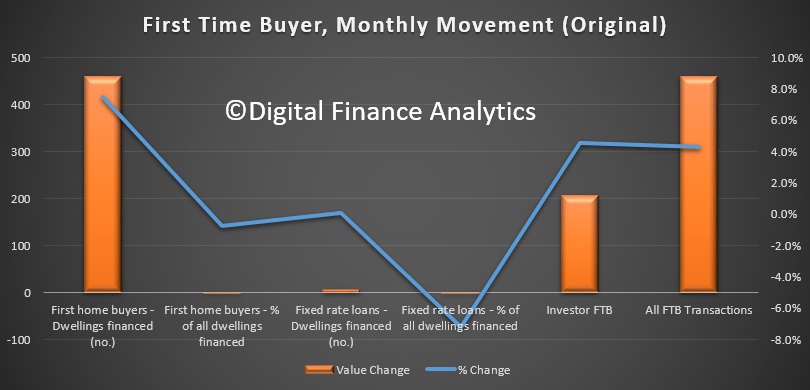

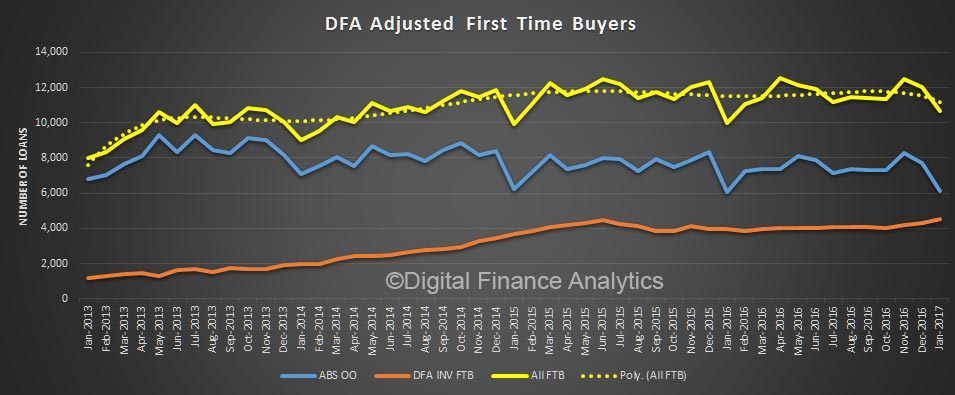

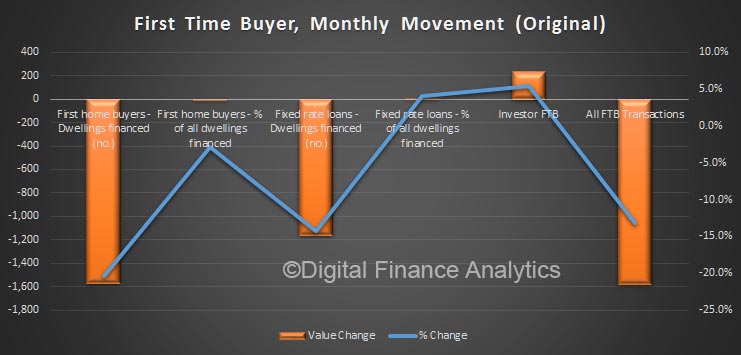

Looking next a first time buyers, the number of transactions rose in the month, in original terms up 7.5% to 6,596, or 13.3% of all transactions, still below previous peaks and lower than last month.

Our surveys also identified another 4,600 first time buyers going direct to the investment sector, so overall volumes are higher than the official figures suggest.

Looking at the movements, month on month, the number of FTB rose, with an increase of 460 over the previous month. Fixed rate lending compared with all transactions was down.

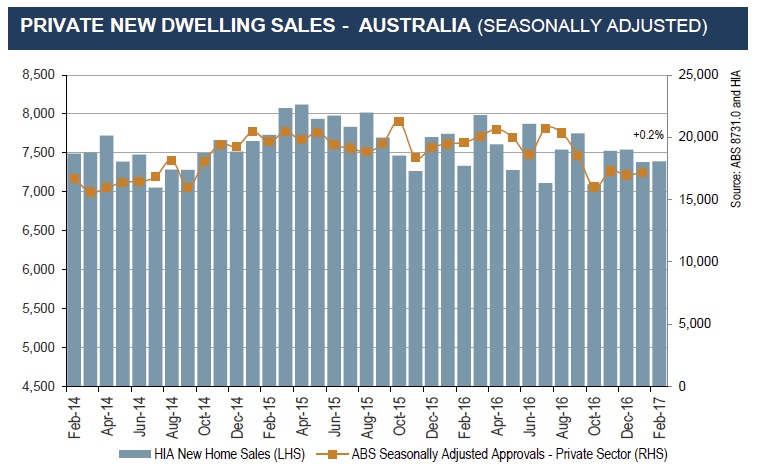

There was little movement in total New Home Sales in February, but Western Australia and Victoria enjoyed positive results, said the Housing Industry Association.

Detached house sales increased in two out of five mainland states in February 2017 – Western Australia and Victoria. Detached house sales in WA increased by 11.3 per cent in February 2017 following a rise of 12.1 per cent in January. Note that these rates of growth are exaggerated by the extremely low base for detached house sales. Detached house sales in Victoria posted a monthly gain of 5.1 per cent in February. Elsewhere for the mainland states, in February detached house sales fell by 12.6 per cent in New South Wales and were down by 5.7 per cent in Queensland and 0.2 per cent in South Australia.

“The HIA New Homes Sales Report – a survey of Australia’s largest home builders – reveals a bare movement of only +0.2 per cent in February 2017,” said HIA Chief Economist, Dr Harley Dale. “There was also very little movement in the two sub-series with detached house sales ticking down by 0.1 per cent in February and the sales of ‘multi-units’ growing by 1.0 per cent.”

“The profiles for HIA detached house sales and ABS detached house building approvals are very similar. In the case of detached house sales, over the three months to February this year the volume fell by 2.2 per cent to a level 5.2 per cent lower than achieved over the three months to February last year,” noted Harley Dale.

“The updates that we are receiving for these two key leading indicators of new home building activity are consistent with a modest reduction in national new detached house commencements in 2016/17. We are forecasting a decline of 2 per cent in detached house commencements in Australia in 2016/17 following a similar-sized fall of 1 per cent in 2015/16.”

“As with all aspects of the current housing cycle there are large differences in conditions for detached housing between states and territories. HIA’s detached house sales series for the five mainland states has been consistently highlighting this point for some years now,” concluded Harley Dale. “In 2017 we expect the profile for leading indicators such as detached house sales to slowly improve for Western Australia and South Australia. At the same time the volume of detached house sales on the eastern seaboard is expected to trend lower.”

We now know how many houses foreign investors are buying in New South Wales and Victoria, the hotbeds of Australia’s housing affordability debate.

According to new research based on data obtained under a Freedom of Information request by Hasan Tevfik and Peter Liu, research analysts at Credit Suisse, foreigners are buying property at an annualised rate of $8 billion per annum, equating to 25% of new supply in New South Wales and 16% in Victoria in the past 12 months.

“We have been able to gather new data from the state revenue offices of New South Wales and Victoria that reveal the size, source and changes in foreign demand for Aussie housing,” the pair wrote in a research note on Thursday.

“The data is new and is available because state governments now collect taxes from foreign buyers.”

The bombshell figures suggest that, along with local investors, the level of foreign investor activity in the housing markets has been a significant driver of the price growth of recent years, and the overwhelming majority — a staggering 80% in NSW — is coming from China.

In a note to clients, Tevfik and Liu write:

Now there is credible, official data on the amount of foreign demand for Aussie housing. We made a Freedom of Information Act request for this data and you can imagine our excitement (we are nerds and love new data) when the state governments of NSW and Victoria complied. Here is what the data reveals.

1. Foreign demand for housing in NSW is currently running at an annualised rate of $4.9bn and is the equivalent of 25% of new supply. We think this is extraordinary given that current supply is nearing peak cycle. In Victoria foreign buyers are hoovering up 16% of new supply.

2. When we talk about foreign buyers we are really talking about Chinese buyers. The Chinese have accounted for almost 80% of foreign demand in NSW. The second biggest group, the Indonesians, account for just 1.7% of foreign demand.

3. It is clear foreigners have been able to settle on their Aussie properties more recently despite the numerous impediments of capital controls and the lack of lending by Aussie banks. There is little evidence so far to suggest the flows have stopped.

“The taxes collected imply foreigners are currently purchasing an annualised $4.9 billion of New South Wales housing and $3.1 billion in Victoria,” say Tevfik and Liu.

According to recent data from CoreLogic, the median dwelling price in Sydney increased by 18.9% in the 12 months to mid-March, and by 14.7% in Melbourne. From January 2009, prices in Sydney have surged by 106%. Melbourne price growth has been similarly strong, increasing by 89%.

The rate of price growth has concerned policymakers, with the federal government examining a range of policy responses in its forthcoming budget to address affordability, and the central bank flagging increasing concerns about financial stability.

“In New South Wales there were 1,503 properties settled involving foreign buyers from October 2016 to January 2017 and they totaled $1.63 billion in value.

“Chinese buyers settled on 1,211 or 80% of them and accounted for 77% of the total purchase value.”

Source: Credit Suisse

Tevfik and Liu say that the Chinese figures include buyers from not only mainland China but also Hong Kong, Macau and Taiwan.

There is also little indication that they are having trouble in meeting their settlement obligations, yet.

“In New South Wales there were $225 million of foreign settlements in October 2016 and this rose to more than $450 million in both November and December. In Victoria the value of December settlements was 50% higher than in November,” they say.

“So despite the capital controls put in place in China, and the local banks refusing to lend to purchasers from abroad, foreign buyers were still able to find the financing to complete their transactions.”

Those restrictions were tightened further at the beginning of this year with regulators stipulating that people could not purchase foreign exchange for overseas investment, including for buying houses.

With the tax data on foreign purchases now several months old, whether this is impacting the ability of Chinese investors to settle is, as yet, unknown.

According to a report in The Australian earlier this month, many Chinese buyers were struggling to settle upon apartments that they had previously purchased in Melbourne.

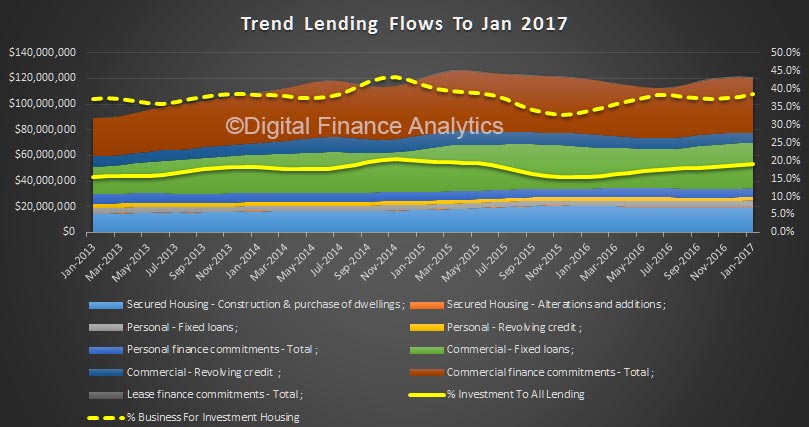

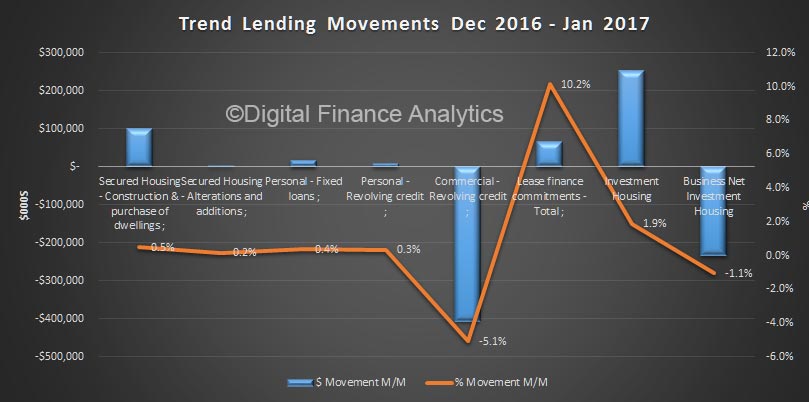

The latest data from the ABS for Lending Finance in January just reinforces the story that investor loans were so, so strong. Owner occupation housing finance grew 0.5%, to $20.1 billion, personal finance was up 0.4% to % 6.9 billion and overall commercial lending fell 0.9%, down to $43 billion (thanks to significant falls in non-investment housing)

However, the share of lending for investment properties, of fixed commercial lending rose to 38.4%, the highest proportion since May 2015, and the share of commercial lending for investment property now stands at 19.1% of all lending, again the highest since May 2015.

The individual monthly movements reinforce how strong investment lending was. There was also a 5.1% fall in revolving commercial lending.

Another view, which looks just at housing confirms the story, with construction lending for investment up 5%, and investment lending for investment up well over 1%.

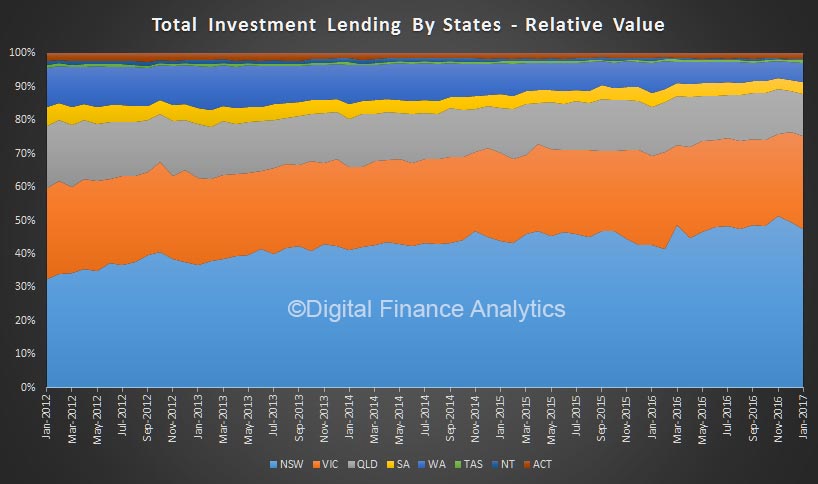

The state level data also confirms that the bulk of the investment property lending is in Sydney and down the east coast to Melbourne.

We say again, this is not good news, because such strong growth in finance for investment properties simply inflates banks balance sheets and home prices, raises household debt, and escalates systemic risks. We need to funnel investment into productive business enterprise, not more housing.

Expect regulatory intervention soon. Better (very) late than never.

The Victorian State Government is taking action to protect the much-loved backyard and keep more garden space in local suburbs.

Minister for Planning Richard Wynne announced the changes today, which follow a review of suburban Residential Zones. The review found the zones had been implemented in an inconsistent manner across Melbourne, but the proposed changes will protect suburban character, no matter your postcode.

The changes are linked to the Government’s refreshed Plan Melbourne, a blueprint for ensuring our suburbs develop and grow, but never at the expense of neighbourhood character.

There will no longer be a cap on how many dwellings can be built on a block, but new requirements mean developments must have a mandatory percentage of garden space.

It’s all about giving more Victorians access to the outdoor space that is the cornerstone of great homes, and giving kids more opportunities to form their childhood memories in backyards every day all over the state.

Under new rules, blocks between 400-500 square metres require a 25 per cent minimum garden area, blocks between 501-600 metres need 30 per cent, and blocks larger than 650 square metres must have a 35 per cent garden area.

The former Liberal government’s version of Plan Melbourne failed to address housing affordability, and ignored the need for a long-term plan that allows for growth but prevents over-development.

We’ve listened to councils, industry and members of the public to right those wrongs – and to maintain our renowned liveability.

Plan Melbourne aims to deliver:

Jobs and services closer to where people live

A fixed urban boundary

Sustained investment in infrastructure, such as Melbourne Metro Rail and level crossing removals

Clarity about where growth can occur in the suburbs

Responses to climate change by reducing Melbourne’s carbon footprint and growing a green economy

A greater focus on social infrastructure such as parks

Well-connected, 20-minute neighbourhoods

The Victorian Government’s plan to change some requirements of the residential zones will improve housing outcomes in our suburbs says the Housing Industry Association (HIA).

The Government’s announcement today that elements of the residential zones will be amended is seen as a logical starting point to improve residential planning outcomes.

HIA has argued that the new zone provisions introduced in 2014 have had the effect of limiting the design of new homes together with restricting the location of small medium density developments.

Figures released today by the ABS indicate that the volume of loans for new homes eased back during January, said the Housing Industry Association.

During January 2017, the total number of owner occupier loans for the purchase or construction of new homes fell by 1.0 per cent and was 0.4 per cent lower than a year earlier. The volume of loans for new home purchase declined by 0.3 per cent during January with lending for the construction of new dwellings dipping by 1.4 per cent.

In January 2017 the number of loans to owner occupiers constructing or purchasing new homes increased in three states. Compared with January of last year, the volume of loans rose most strongly in Queensland (+13.1 per cent), followed by South Australia (+9.2 per cent) and Victoria (+8.8 per cent). The largest reduction occurred in Western Australia (-9.3 per cent), followed by Tasmania (-3.5 per cent) and New South Wales (-1.2 per cent). The volume of lending rose by 22.1 per cent in the ACT but was down by 54.8 per cent in the Northern Territory over the same period.

“Despite the reduction during January, the actual volume of loans for new homes remains at a very elevated level – about 99,620 loans were made over the year to January 2017,” noted HIA Senior Economist Shane Garrett.

“There are two dynamics going on with respect to new home loans. With 2016 representing the strongest year for new dwelling starts since the end of WWII, a huge number of new homes are now becoming available for purchase making lending volumes in this area accordingly high. However, the number of loans to people constructing their own home has actually been falling back since mid-2014 and this trend has affected overall lending activity,” Shane Garrett concluded.

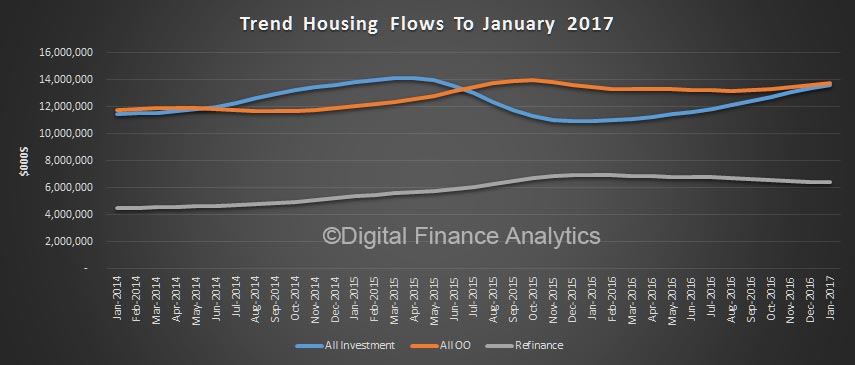

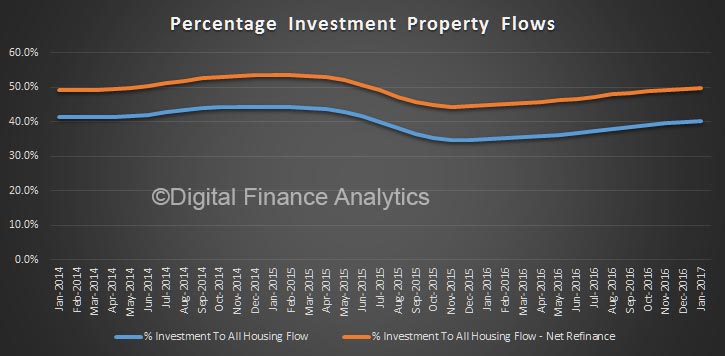

The ABS released their Housing Finance data today, showing the flows of loans in January 2017. Those following the blog will not be surprised to see investor loans growing strongly, whilst first time buyers fell away. The trajectory has been so clear for several months now, and the regulator – APRA – has just not been effective in cooling things down. Investor demand remains strong, based on our surveys. Half of loans were for investment purposes, net of refinance, and the total book grew 0.4%.

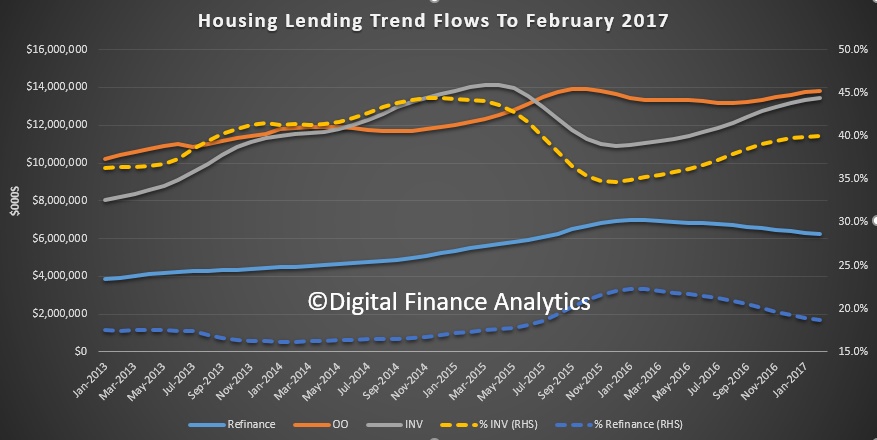

In January, $33.3 billion in home loans were written up 1.1%, of which $6.4 billion were refinancing of existing loans, $13.6 billion owner occupied loans and $13.5 billion investor loans, up 1.9%. These are trend readings which iron out the worst of the monthly swings.

Looking at individual movements, momentum was strong, very strong across the investor categories, whilst the only category in owner occupied lending land was new dwellings. Construction for investment purposes was up around 5% on the previous month.

Stripping out refinance, half of new lending was for investment purposes.

First time buyers fell 20% in the month, whilst using the DFA surveys, we detected a further rise in first time buyers going to the investment sector, up 5% in the month.

Total first time buyer activity fell, highlighting the affordability issues.

In original terms, total loan stock was higher, up 0.4% to $1.54 trillion.

Looking at the movements across lender types, we see a bigger upswing from credit unions and building societies, compared with the banks, across both owner occupied and investment loans. Perhaps as banks tighten their lending criteria, some borrowers are going to smaller lenders, as well as non-banks.

We think APRA should immediately impose a lower speed limit on investor loans but also apply other macro-prudential measures. At very least they should be imposing a counter-cyclical buffer charge on investment lending, relative to owner occupied loans, as the relative risks are significantly higher in a down turn.

The budget has to address investment housing with a focus on trimming capital gain and negative gearing perks. The current settings will drive household debt and home prices significantly higher again.

Politicians and the powerful property lobby continue to argue that building more houses is the solution to Australia’s chronic affordability problems.

But a “supply-side solution” – as propounded by NSW Premier Gladys Berejiklian as well as Prime Minister Malcolm Turnbull and Treasurer Scott Morrison – will only work if affordability is just a supply-side problem. Evidence suggests this is not the case. In fact, our analysis shows that Australia is almost a world leader in rates of new housing production.

How Australia compares

One way to assess Australia’s supply performance is to compare it with other developed countries. The graph below compares the number of dwelling completions per 1,000 persons across 13 countries, for the years 2010 and 2015. On this measure, Australia’s new housing production is second only to South Korea’s.

Australia delivers two-thirds more homes per 1,000 persons than the US and four times more than the UK. When we measure supply as a proportion of existing stock, Australia again ranks second with a rate double that of the US.

OECD questionnaire on affordable and social housing; World Bank population growth and total population figures, Author provided

A slightly different approach takes into account population growth. This involves measuring dwelling completions per head of new population. Here Australia’s performance sits in the middle of the pack.

We are delivering just over 0.5 dwellings per head of new population compared to more than 2 in South Korea. This rate is, however, still ahead of the UK and comparable to the US. Again, that suggests inadequate supply is not the major cause of the affordability crisis.

OECD questionnaire on affordable and social housing, World Bank population growth and total population figures, Author provided

State comparisons of supply

At a national level, supply seems pretty healthy. But there are significant state variations. This might, on the surface, be used to explain different patterns of price growth.

The table below shows that New South Wales has produced fewer new homes per 1,000 people than Australia overall over a 30-year period. The difference was particularly marked between 2005 and 2015.

State comparisons of new housing supply.ABS building activity Australia cat. 8152; ABS Australian Demographic statistics Cat 3101, Author provided

However, higher supply output in the other states has certainly not created affordable markets. In NSW, the last two years have delivered significant supply growth yet prices have continued to rise just as fast. So why do prices rise with supply growth?

Demand drives supply

In a market-driven housing system, price stimulates new housing supply. In Australia new supply has responded relatively quickly to price rises (despite the continuous rhetoric from the property lobby about planning).

But there is always some lag due to the time it takes to secure necessary approvals and physically construct property. There is no such lag with demand meaning there is often a sustained mismatch between the two – positive or negative.

In a rising market, development becomes more profitable and land values rise, meaning greater returns for all concerned. Potential future capital gains stimulate investment activity. Price rises also allow owner-occupiers to trade up as the equity in their own dwelling increases.

In such circumstances, increased levels of housing supply do little to satiate demand created by population growth and the appetite of investors.

Western Australia has had an incredible level of housing completions over the last 30 years, as shown in the table, with 2014 and 2015 particularly strong. In the last 12 months, dwelling commencements have collapsed by more than 25%. Prices have been falling slowly for almost three years driven by the contraction in the resources sector and strong levels of new supply.

However, even under these conditions, WA housing affordability shows little sign of improving for those on low incomes. The market still cannot deliver housing for those at the bottom end of the market.

The housing market is simply unable to deliver housing that is affordable to those on lower (and, increasingly, moderate) incomes because there is a minimum cost of delivering housing that meets minimum community standards. This is made up of the land price, the physical construction costs of the dwelling, and the profit required for taking on the development risk.

This is why market intervention and subsidy are essential to deliver options for those on low incomes.

Targeted interventions are needed

Two strategies are needed to deliver affordable housing to the lower end of the market.

First, demand-side measures need to be better targeted to stimulate investment in new supply, particularly affordable rental housing, rather than simply fuelling demand.

Second, any government serious about improving affordability needs to put more resources into the community housing sector. This could be funded in two ways: partly by taxing the windfall gains from development and partly by reallocating existing demand-side subsidies.

The community housing sector can operate counter-cyclically. This means it can maintain housing supply even when house prices stagnate or fall – which is good for the economy.

Targeting supply to deliver housing for those on low incomes and reining in demand-side incentives that fuel prices will make some difference to affordability for those most affected.

There was some encouragement over the weekend. Scott Morrison discussed the rental market and social housing as part of the affordability solution. This was a welcome change from trotting out the tired old supply arguments and threatening to fuel demand through more home ownership incentives.

Let’s hope the treasurer follows through and delivers some much-needed “whole of housing market” thinking in the May budget.

Authors: Steven Rowley, Director, Australian Housing and Urban Research Institute, Curtin Research Centre, Curtin University; Nicole Gurran, Professor – Urban and Regional Planning, University of Sydney; Peter Phibbs, Chair of Urban Planning and Policy, University of Sydney

Looking in more detail, lending for investment property rose 0.7% to $13 billion, whilst other fixed lending to business fell 2.9% to $20 billion. So overall productive business lending fell again. Not good for productive growth. Actually the bulk of investor lending was in Sydney and Melbourne, highlighting again the lopsided property market, and why investor lending needs real attention from regulators and Government.

Looking in more detail, lending for investment property rose 0.7% to $13 billion, whilst other fixed lending to business fell 2.9% to $20 billion. So overall productive business lending fell again. Not good for productive growth. Actually the bulk of investor lending was in Sydney and Melbourne, highlighting again the lopsided property market, and why investor lending needs real attention from regulators and Government. The total value of owner occupied housing commitments excluding alterations and additions rose 0.2% in trend terms, and the seasonally adjusted series fell 0.5%.

The total value of owner occupied housing commitments excluding alterations and additions rose 0.2% in trend terms, and the seasonally adjusted series fell 0.5%.