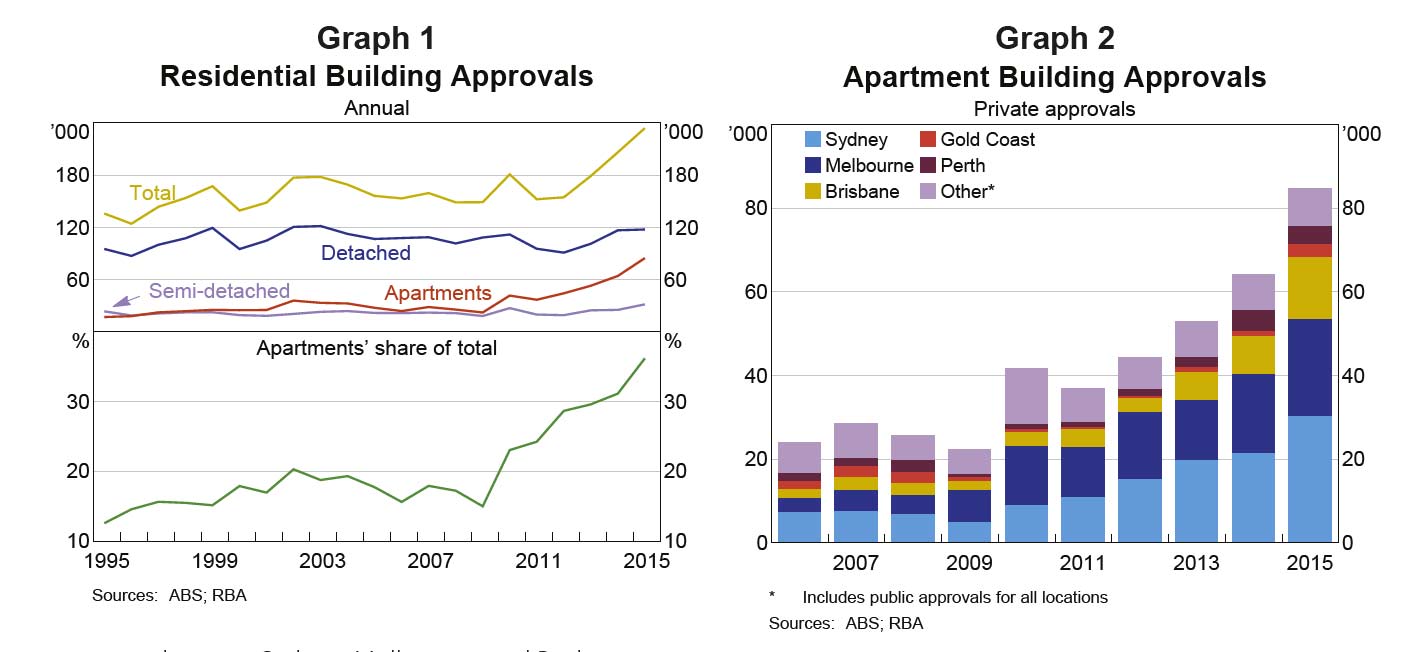

Initially, approvals for apartments increased in Melbourne in 2010, followed by Sydney, and then Brisbane more recently. Apartment approvals in Perth also increased in recent years, but from a relatively small base. The effect of this increase on the stock of apartments in each city has varied. Cumulative approvals since 2011 in Melbourne and Brisbane have added around one-third to the stock of apartments in those cities compared with an addition of around one-fifth of the 2011 stock for Sydney and Perth.

The location of activity within each of the cities has varied. This has been determined by a variety of factors, including proximity to employment centres and transport infrastructure, planning frameworks and the availability of suitable sites for apartment projects. In Sydney, approvals have been relatively spread out across the inner and middle suburbs – a large area ranging from Parramatta in the west to Chatswood in the north and Mascot in the south. In contrast, a relatively large share of apartment approvals in Melbourne has been in the city (which includes the CBD, Southbank and Docklands – an area of around 30 square kilometres), although construction activity in the middle-ring suburbs has picked up more recently. In Brisbane, activity has been concentrated in the city and in a few of the surrounding inner suburbs, as has been the case in Perth.

The location of activity within each of the cities has varied. This has been determined by a variety of factors, including proximity to employment centres and transport infrastructure, planning frameworks and the availability of suitable sites for apartment projects. In Sydney, approvals have been relatively spread out across the inner and middle suburbs – a large area ranging from Parramatta in the west to Chatswood in the north and Mascot in the south. In contrast, a relatively large share of apartment approvals in Melbourne has been in the city (which includes the CBD, Southbank and Docklands – an area of around 30 square kilometres), although construction activity in the middle-ring suburbs has picked up more recently. In Brisbane, activity has been concentrated in the city and in a few of the surrounding inner suburbs, as has been the case in Perth.

Alongside this strong construction activity, competition among developers for suitable sites for apartment projects has intensified and led to increases in site prices. Australian developers account for the majority of apartment projects, though foreign developers have become more active in acquiring sites and developing projects, mostly in Melbourne and Sydney. In addition to competing over the acquisition of suitable new sites and residential land, developers have also sought to purchase lower-grade office and industrial buildings for conversion into apartment projects, thereby supporting prices for these assets.

Turning to buyers, there are a variety of factors that have contributed to increased demand for new apartments from prospective owners and tenants. Employment opportunities and population growth are fundamental drivers of demand for new housing; sustained population growth in Australia’s largest cities has led to increased demand for all dwellings, including apartments. Population growth was strongest in Perth for much of the past decade, in part owing to migration associated with the mining investment boom. That growth has slowed over the past couple of years. In the eastern cities, land supply constraints have led to increased prices for blocks of land and detached houses. This is likely to have driven demand for apartments relative to other dwellings, as apartments use land more intensively than detached houses and are therefore relatively more affordable. A desire to reside close to CBD employment centres is also likely to have stimulated demand for apartments, as residents in increasingly populated cities value the convenience and reduced travel time associated with the proximity to amenities in these areas.

Three types of buyers can be distinguished – owner-occupiers, domestic investors and foreign buyers (‘non-residents’). Liaison with industry contacts suggests that, in recent years, the relative importance of these three groups has varied across different cities. Foreign buyers have played a relatively significant role in the inner city of Melbourne. In the inner suburbs of Brisbane, domestic investors (particularly from interstate) have underpinned demand, driven in part by the higher yields available relative to Sydney and Melbourne. In contrast, sales in Sydney have been more evenly spread across the three groups of buyers.

Whether buyers are owner-occupiers or investors can influence the composition of the net supply of housing. Purchases of new apartments by domestic investors are most likely to lead to an increase in the supply of rental properties. For owner-occupiers, the net effect will depend on the location and size of the existing property from which the purchaser is moving and whether there is a change in the rate of household formation. For example, if the owner-occupier is a first home buyer moving out of their parents’ home, total demand for housing increases alongside the increased supply of housing, whereas if they are moving from a rented property this will create a rental vacancy elsewhere.

Similarly, owner-occupiers who are downsizing will leave an established property that can possibly accommodate a larger household. The net impact from foreign buyers on housing demand will depend on the relative mix of those buyers who plan to occupy their dwelling (or leave it vacant) and those who plan to rent out their property. All foreign buyers, other than temporary residents, are generally restricted to purchasing newly constructed dwellings. The observations on foreign buyer activity in this article are sourced from liaison with property developers and other industry contacts.

Developers must record the residency of buyers to ensure that they do not exceed Australian banks’ caps on pre-sales to foreign buyers (if funded by an Australian lender). Non-residents and temporary residents must apply to purchase Australian property – the Foreign Investment Review Board records data on approvals for these purchases, though these data are limited and partial. Industry contacts have often reported that many foreign buyers, especially those who reside in East Asia, have additional motivations for buying apartments in Australia. It is commonly reported that foreign buyers purchase Australian property to diversify their wealth and intend to hold the property for a long period. Contacts also suggest that foreign buyers’ motivations can include the prospect of future migration, providing housing for children while they study in Australia, or acquiring holiday apartments. The interest from foreign buyers of property, particularly those from Asia, is not unique to Australia; such buyers are also active in the property markets in other countries, such as the United States, the United Kingdom, Canada and New Zealand. Other features that have been cited as attracting foreign buyers include the lower prices of apartments in Australia in recent years relative to major cities in some other countries (particularly following the depreciation of the Australian dollar), geographic proximity to Asia and a stable political and regulatory environment.

Apartments have driven the increase in new dwelling construction in Australia since 2010 and have provided an important contribution to economic growth and employment. The increase in apartment construction has reflected a range of factors, including land supply constraints, affordability considerations and a desire to reside in close proximity to established amenities and employment centres. This has delivered many new dwellings to the market, which has had an effect on housing prices and rents, with growth in these indicators slowing of late. The majority of recent activity has been located in areas with existing links to transport, infrastructure and services, particularly the inner suburbs of Sydney, Melbourne and Brisbane, and, to a lesser degree, Perth. The increase in apartment construction in these cities has been characterised by differences in the geographical concentration of activity, the proportional increase in the apartment stock, the types of buyers purchasing the new dwellings and the planning frameworks, which can affect the behaviour of developers and the supply response. Apartments are likely to continue to play an important role in providing new housing as land supply constraints motivate prospective home owners to purchase higher-density dwellings (which use land more intensively and are therefore less expensive relative to larger, lower-density houses), and as tenants and residents choose to live closer to employment centres and amenities for convenience.

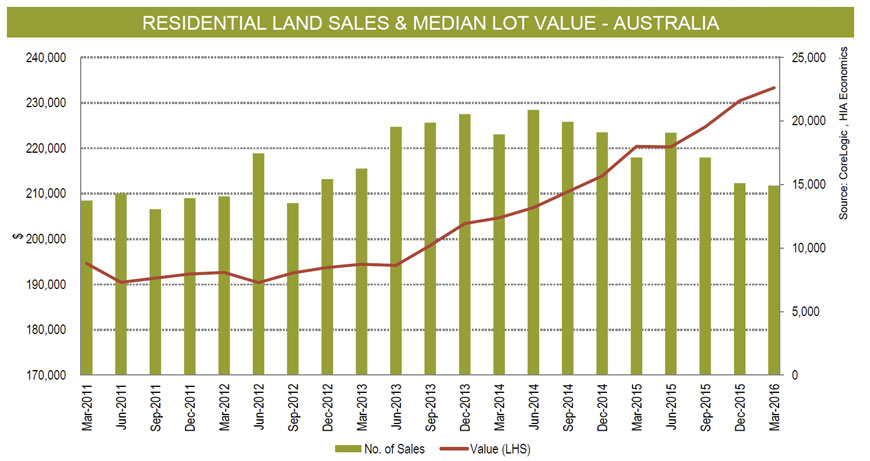

During the March 2016 quarter, vacant residential land sales increased most strongly in Perth (+22.3 per cent) followed by Melbourne (+5.2 per cent). However, land market turnover fell in Hobart (-28.4 per cent), Adelaide (-8.3 per cent), Sydney (-5.9 per cent) and Brisbane (-3.4 per cent) over the same period.

During the March 2016 quarter, vacant residential land sales increased most strongly in Perth (+22.3 per cent) followed by Melbourne (+5.2 per cent). However, land market turnover fell in Hobart (-28.4 per cent), Adelaide (-8.3 per cent), Sydney (-5.9 per cent) and Brisbane (-3.4 per cent) over the same period.