The ABS building activity data to December 2015, released today, shows the trend estimate for the total number of dwelling units commenced fell 1.5% in the December 2015 quarter following a rise of 0.7% in the September quarter, whilst the seasonally adjusted estimate for the total number of dwelling units commenced fell 5.1% to 53,727 dwellings in the December quarter following a rise of 2.3% in the September quarter.

The trend estimate for new private sector house commencements fell 1.5% in the December quarter following a fall of 1.3% in the September quarter, whilst the seasonally adjusted estimate for new private sector house commencements fell 5.4% to 26,840 dwellings in the December quarter following a rise of 2.8% in the September quarter.

The trend estimate for new private sector other residential building commencements fell 0.7% in the December quarter following a rise of 3.2% in the September quarter, whilst the seasonally adjusted estimate for new private sector other residential building fell 3.8% to 25,733 dwellings in the December quarter following a rise of 3.9% in the September quarter.

However, the trend estimate of the value of total building work done rose 0.3% in the December 2015 quarter, whilst the seasonally adjusted estimate of the value of total building work done rose 1.0% to $24,507.5m in the December quarter, following a rise of 1.0% in the September 2015 quarter.

The trend estimate of the value of new residential building work done rose 1.3% in the December quarter. The value of work done on new houses fell 2.0% while new other residential building rose 5.5%. The seasonally adjusted estimate of the value of new residential building work done rose 2.1% to $13,960.0m. Work done on new houses fell 2.2% to $7,640.8m, while new other residential building rose 7.8% to $6,319.3m.

The trend estimate of the value of non-residential building work done fell 0.9% in the December quarter. The seasonally adjusted estimate of the value of non-residential building work done in the quarter fell 0.1%, following a fall of 1.5% in the September 2015 quarter.

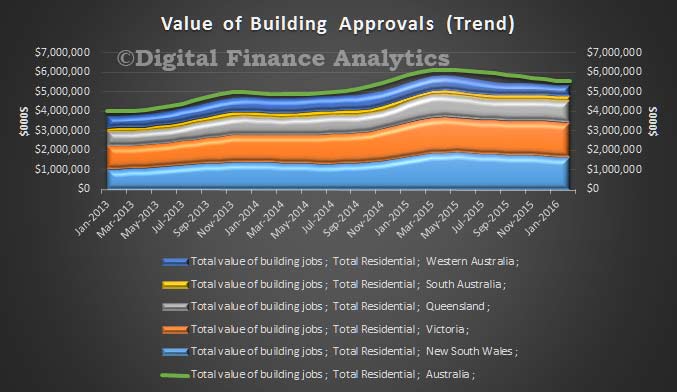

The trend estimate of the value of total building approved fell 0.8% in February and has fallen for seven months. The value of residential building fell 0.7% and has fallen for 10 months. The value of non-residential building fell 1.2% and has fallen for six months.

The trend estimate of the value of total building approved fell 0.8% in February and has fallen for seven months. The value of residential building fell 0.7% and has fallen for 10 months. The value of non-residential building fell 1.2% and has fallen for six months.