More and more people of all ages are unable to buy their own home in Britain, and there is no denying the country is in the grip of a nationwide housing crisis.

Already in Britain self-builders build more homes than the largest individual house-builder, but despite these figures, it is still considered a marginal activity and an individual choice rather than a potential large-scale policy solution.

This is short sighted because self-build is a good way to develop more appropriate housing which meets residents’ demands and desires while also being affordable.

In European countries self-build is the norm; in France and Belgium it accounts for about 50% of all new building and in Sweden about a third of new house building is self-built – compare that with England where the figure stands at less than 10%.

We are crying out for more self-build housing in Britain, not only as a way to address the housing shortage but also as a way to deliver low carbon lifestyles – something conventional house construction has failed to do.

Close to home

What is considered self-build varies internationally, but it is generally when a resident has built all or part of their home, sometimes working with or employing others during the build. In Australia, for example, the term custom build more accurately describes how a lot of new houses are built.

With custom build, a developer offers two or three design options and the customer chooses a design and the number of different rooms they want. The difference between self-build and custom-build is the level of resident responsibility, organising and interaction. But all varieties offer useful options for the provision of more affordable housing.

Many people build their own homes with limited building experience, but are keen to get involved because they get to choose the layout, materials and aesthetics of their home – plus self-build is often a much cheaper way to get on the housing ladder.

With residents taking on all, or some of, the jobs themselves and moving away from reliance on the brick – the use of cheaper and quicker methods like prefabricated systems, reclaimed materials, or straw-bales can reduce costs and cut out the need for a company to make a profit.

The significant cost of land can be also mitigated with self-build by developing communal land ownership structures that make it available for affordable housing. And costs can be lowered even further when a collective builds homes, such as co-housing groups, who share the purchase of land, infrastructure and building.

Building for the future

Despite the low number of self-builds, Britain already has a broad variety of homes built in this way – from the large detached houses featured on programmes such as Grand Designs to numerous small homes crafted from low-cost, natural or reclaimed materials.

In an attempt to create housing for local residents some councils have started to allocate land for self-build housing, and others have created exemptions in planning legislation that allow certain forms of self-building in places normally denied building permission.

To tackle the housing crisis we need a complete rethink of the way we build houses in Britain. Self-building shouldn’t be for the reserve of the mega rich, or those looking for a project in retirement. Instead young people, families, couples, anyone should be able to build their own home.

We need to look to our European neighbours to learn a thing or two about self-building and shared ownership. We need to learn how to minimise the amount of materials required by building smaller individuals houses with shared communal space for gardens, laundry, workshops and storage.

And instead of purchasing freehold we could roll out more stakeholder ownership models – just like Lilac in Leeds. At Lilac costs are linked to ability to pay and residents only pay a housing charge equivalent to 35% of their net income. Meaning the higher earners subsidise those on lower incomes.

With a rise in self-build housing we could build our way out of the current housing crisis – but maybe more importantly, we could also avoid a repeat of it in the future.

Author: Jenny Pickerill, Professor of Environmental Geography, University of Sheffield

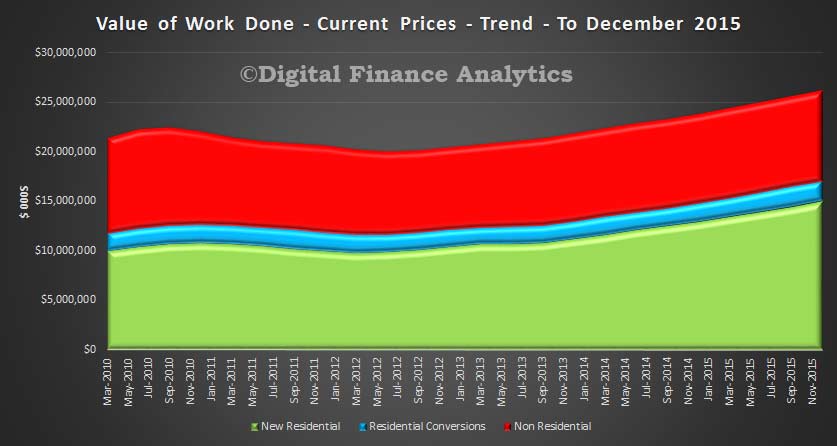

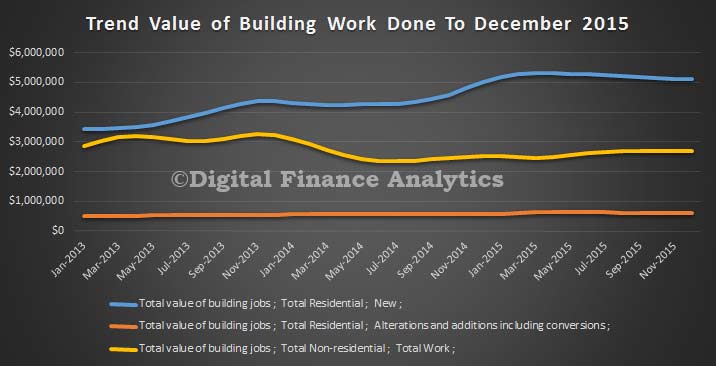

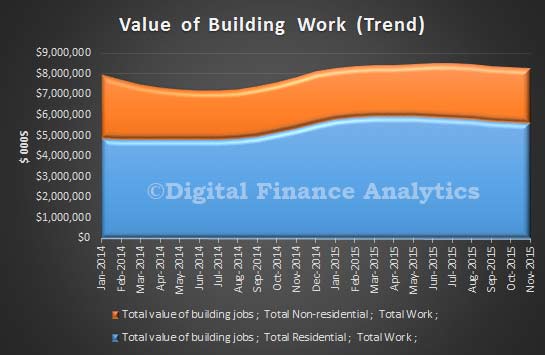

The preliminary ABS data on construction work done, released today to December shows that the trend estimate for total construction work done fell 1.6% in the December quarter 2015 whilst the the seasonally adjusted estimate for total construction work done fell 3.6% to $48,413.4m in the December quarter.

However, the trend estimate for total building work done rose 1.0% in the December quarter, with non-residential building work done rising 0.3% and residential building work up 1.4%. The seasonally adjusted estimate of total building work done rose 2.7% to $24,990.2m in the December quarter.

In contrast, the trend estimate for engineering work done fell 3.9% in the December quarter and the seasonally adjusted estimate for engineering work done fell 9.5% to $23,423.3m in the December quarter. So growth continues to rely on the housing sector.

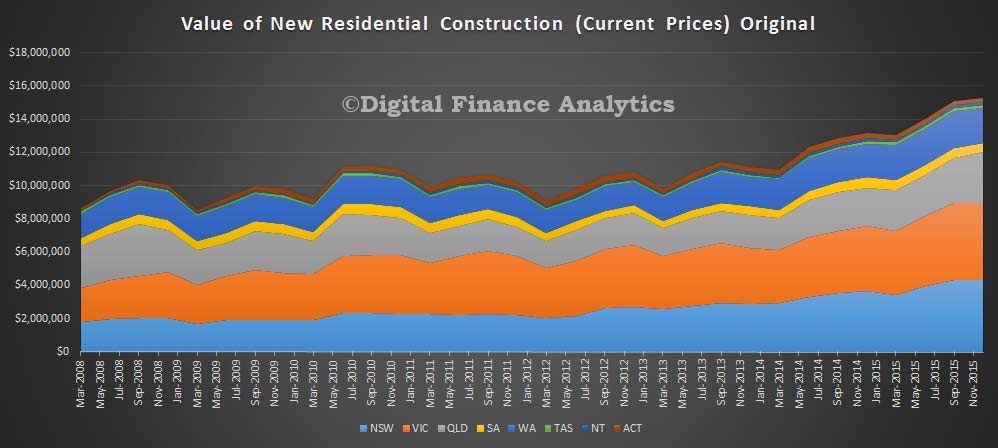

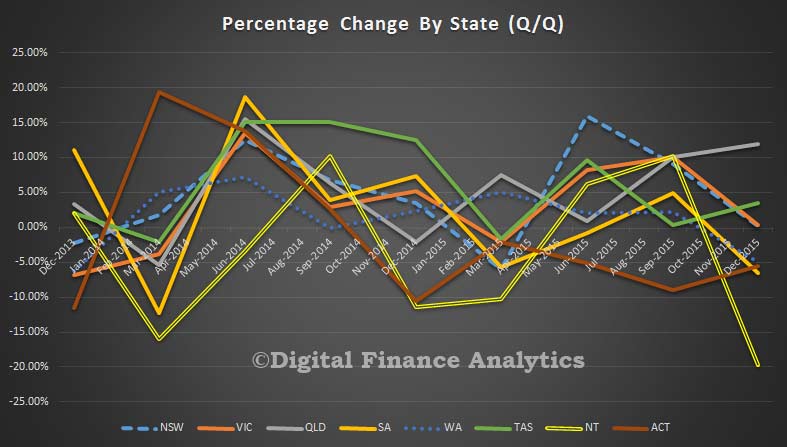

The state by state data on residential construction (original data, so no smoothing) shows some significant movements.

In NSW, total new residential construction rose 0.21%, whilst VIC rose 0.28%. Both states are suggesting slowing momentum. This is in contrast to QLD which has shown growth of more than 10% the past two quarters. SA dropped 6.5% (reversed the 4.9% movement in the prior quarter) whilst WA fell 5%, the first fall since 2013.

Data from TAS, NT and ACT are more volatile so probably less significant, with NT falling 19.7% (after a 10% rise last time), ACT 5.6% (the fifth consecutive quarterly fall) and TAS rising 3.5%.

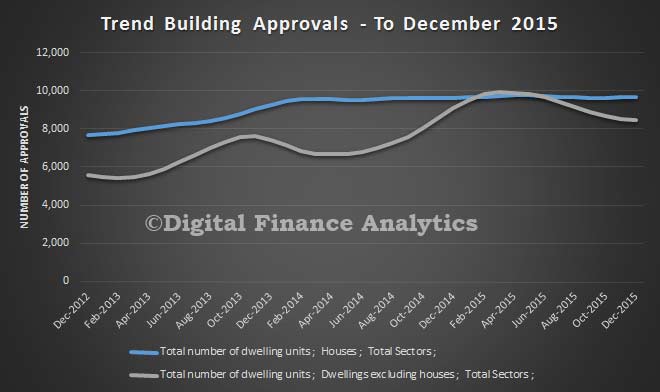

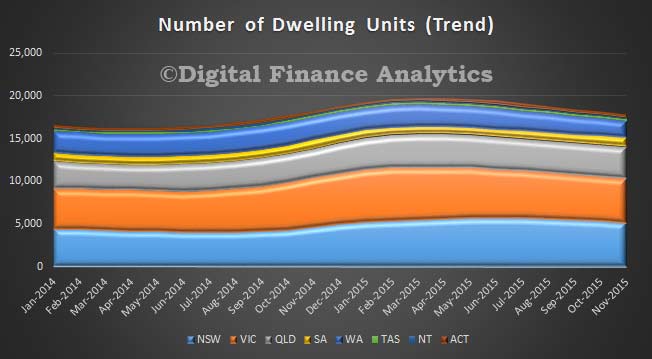

Australian Bureau of Statistics (ABS) Building Approvals show that the number of dwellings approved fell 0.1 per cent in December 2015, in trend terms, and has fallen for eight consecutive months.

Dwelling approvals decreased in December in the Australian Capital Territory (21.9 per cent), Western Australia (3.1 per cent), Tasmania (0.8 per cent), New South Wales (0.4 per cent) and South Australia (0.4 per cent) but increased in the Northern Territory (1.8 per cent), Victoria (1.6 per cent) and Queensland (1.1 per cent) in trend terms.

In trend terms, approvals for private sector dwellings excluding houses fell 0.1 per cent in December. In contrast, approvals for private sector houses rose 0.1 per cent. Private sector house approvals rose in Queensland (0.8 per cent), Victoria (0.7 per cent) and South Australia (0.5 per cent) but fell in Western Australia (1.8 per cent) and New South Wales (0.2 per cent) in trend terms.

The seasonally adjusted estimate for dwelling approvals rose 9.2 per cent in December following a 12.4 per cent fall in November. The rise in December was driven by dwellings excluding houses (13.5 per cent). The largest state contribution to the rise in total dwellings in December came from Victoria (37.4 per cent).

The value of total building approved rose 0.2 per cent in December, in trend terms, after falling for four consecutive months. The value of residential building rose 0.1 per cent while non-residential building rose 0.4 per cent.

Each quarter CommSec attempts to find out by analysing eight key indicators: economic growth; retail spending; equipment investment; unemployment; construction work done; population growth; housing finance and dwelling commencements. The latest data is just released, and NSW has retained top spot as the best performing economy, edging a little further ahead of Victoria. Both states are maintaining a healthy lead over the other states and territories.

The big change over the past quarter has been the lift of the ACT economy to equal third position alongside the Northern Territory. Western Australia has dropped from fourth to fifth. But there is little to separate the ACT and the Northern Territory in the second grouping of economies.

In the third grouping of state and territory economies, Queensland is sixth ranked, ahead of the South Australia (seventh) and Tasmania (eighth).

Their measurement has a strong bias towards housing and finance, with 3 metrics directly linked, and others indirectly influenced. The slowing resources sector is hitting QLD and WA in particular.

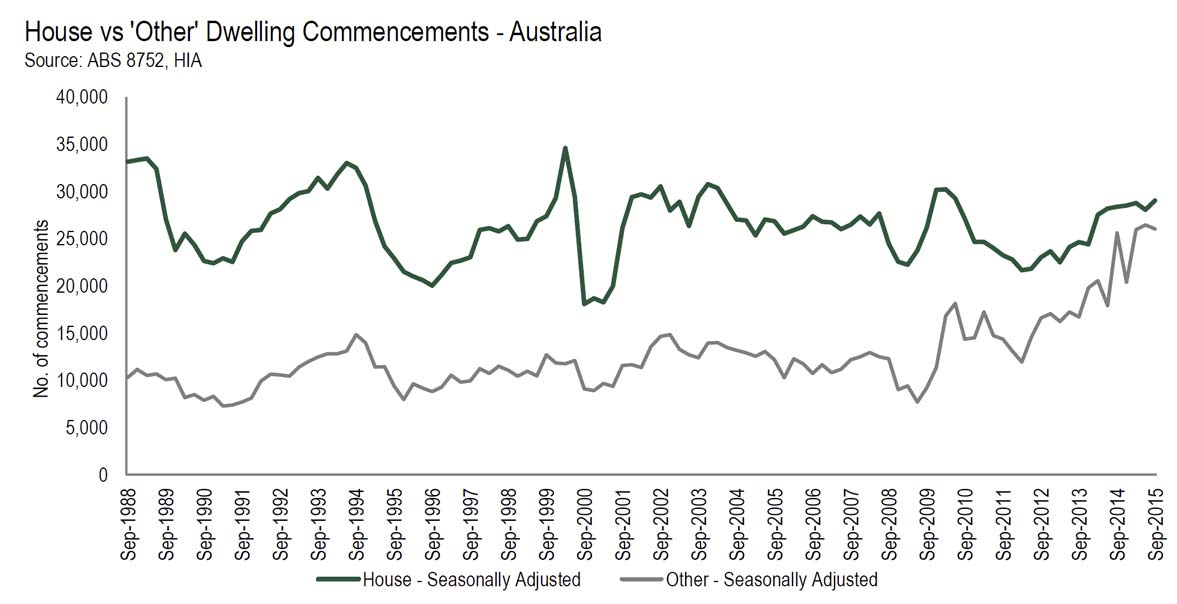

The latest ABS housing figures show new dwelling commencements reached a fresh high in the September 2015 quarter. The trend estimate of the value of new residential building work done rose 1.2% in the September quarter. The value of work done on new houses fell 0.4% while new other residential building rose 3.5%. The seasonally adjusted estimate of the value of new residential building work done rose 1.8% to $13,554.8m. Work done on new houses rose 0.1% to $7,779.6m, while new other residential building rose 4.2% to $5,775.2m.

The HIA goes to town on the back of the latest seasonally adjusted data:

“Today’s update for national new home building is a stellar result not only for the residential construction industry, but for the wider economy,” said HIA Chief Economist, Dr Harley Dale. “New dwelling commencements hit a quarterly record level of 55,532 in the September quarter last year. The historical high of 215,329 commencements for the year to September 2015 is 15 per cent above the previous peak of just over 187,000 ‘starts’ in 1994.”

“Over recent years households and businesses have faced a barrage of negative chatter about below trend growth and downside risks to the economic outlook,” noted Harley Dale. “Throughout this time new home construction has posted one of its longest upcycles in history – providing substantial support to Australia’s economic output and levels of employment.”

“In a federal election year where there is a focus on options for economic and taxation reform, the new housing sector needs to be front and centre,” commented Harley Dale. “We need a visionary outlook regarding the homes Australia has to build over the coming decades to house its growing and ageing population, while not forgetting to celebrate the fact that new home construction and its massive spin-off benefits has propped up the Australian economy at a time when no other sector has come to the party.”

“As has been the case throughout the current cycle, the profile for national dwelling commencements masks large regional differences. In the September 2015 quarter new dwelling commencements increased in New South Wales (+2.4 per cent), Western Australia (1.7 per cent), South Australia (+1.2 per cent), the Northern Territory(+17.4 per cent), and the Australian Capital Territory (+0.4 per cent). Commencements fell in Queensland (-1.0 per cent), Victoria (-3.8 per cent) and Tasmania (-20.7 per cent).

The resignation of Australia’s first minister for cities and the built environment after just 99 days is a setback for federal leadership in these areas. Yet enough momentum and goodwill have been generated to keep the flag flying. The greatest hope is that an urban consciousness in national public policy will be lodged permanently.

Even before state planning ministers assemble within months to hammer out the ground rules for federal engagement, the mutual understanding will be that the states are Australia’s primary urban governments.

In August 1945, a conference of Commonwealth and state ministers in Canberra confirmed that arrangement. The states rejected a generous proposal for a central planning bureau to provide advice, training and information resources plus cover half the costs of employing technical experts to assist local authorities.

Prime Minister Ben Chifley’s summation sealed the fate of the bold reconstruction initiative hatched by Nugget Coombs:

… the matter ought to be left to the states.

How cities became ‘orphans of public policy’

Regardless, the federal government has retained a periodic interest in cities, with mixed outcomes. Historically, most initiatives have been linked to Labor.

Gough Whitlam’s Department of Urban and Regional Development (DURD, 1972-75) injected valuable locational and equity perspectives into policy. However, a big-spending command, control and co-ordinate mission proved problematic.

Bob Hawke delivered AMCORD and Green Street as best-practice guidelines for residential development. This helped change the culture of the development industry. But the Hawke government’s main legacy, driven by Deputy Prime Minister Brian Howe, was Building Better Cities, centred on strategic housing, environmental and infrastructure projects.

Paul Keating gave us the Urban Design Task Force (1994) and the Australian Urban and Regional Development Review (1995) of federal programs for infrastructure, planning and transport.

By the time of the Rudd-Gillard governments, an actual National Urban Policy emerged to guide public intervention and private investment. Its quartet of themes remain widely accepted: productivity, sustainability, liveability and governance.

The Coalition’s contributions have been more muted.

The enduring love affair was between Robert Menzies and Canberra. The capital received extraordinary largesse to become an exemplar of modernist architecture, design and planning. Most everywhere else was ignored.

Late in his term, William McMahon instituted a National Urban and Regional Development Authority, which lingered as a commission for new cities alongside DURD.

Tony Abbott’s narrow focus on roads undercut any claim to being a modern ‘infrastructure PM’.AAP/Dan Himbrechts

The Fraser government wound down Labor’s perceived excesses but still found a rationale for inquiries into the Commonwealth and the urban environment (1978) and a pioneering study on urban environmental indicators (1983). John Howard offered various charters and best practice initiatives, notably the Development Assessment Forum (1998).

Cities have been called “orphans of public policy”, so the decisive and acclaimed entry of the Turnbull government into the fray is remarkable. Malcolm Turnbull has the credibility, nous and drive to supplant Tony Abbott as the first infrastructure prime minister. In a sense, Abbott ignored cities – except to champion motorways – at his peril.

Turnbull invigorates urban agenda

Turnbull’s transformative move has been to declare officially what has been long known: cities are “crucibles” of innovation and enterprise.

Productive cities are smart, innovative, prosperous and great places to live. Less productive cities are accordingly less liveable, sustainable and connected.

While a new cities minister will lay claim to one ear of Turnbull, wife Lucy will command the other. A former lord mayor and “city expert” adviser to the COAG Reform Council, she chairs both the Committee for Sydney and the NSW government’s new Greater Sydney Commission.

The problems of Australian cities are well documented: density (the drawbacks of low joined by the challenges of high), transport (needing greater mass transit connectivity and walkability while reducing dependence on cars), housing (affordability and variety), inequality (divided by income, health and mobility), the spatial mismatch between jobs and homes, fractured metropolitan governance, open space, environment, heritage, design.

Australia’s “broken cities”, to quote the Grattan Institute report City Limits, are:

… caught between the three tiers of Australian government, hardly registering on the agenda of many politicians.

What to do next?

The solutions are wickedly challenging. In December, the then-minister, Jamie Briggs, distilled the state of play in his keynote address to the State of Australian Cities conference. The Commonwealth was not set to take over from the states, create new bureaucracies or become a “planning approver”. Rather, there would be better co-ordination between federal agencies and across all tiers of government.

Briggs flagged collaboration with the private sector, researchers, and the wider community. He spoke of the need to secure “better outcomes” and “measure our performance”. The gaze was on the long run and locking in agreed planning and co-ordination of projects.

Smarter, more flexible and adaptable financial arrangements will come into play. The buzzwords “value uplift” and “value capture” pinpointed the need to extend federal intervention beyond cash handouts. This is code for differential tax increment financing to tap into revenues generated by rising property prices from infrastructure improvements.

Labor’s National Urban Policy framework will need to be revisited. The way forward is through intergovernmental agreements that link specified outcomes to robust and streamlined planning systems. These will need to connect up issues of housing, employment, environment and infrastructure.

This agenda has been taking shape for some time. Bellwethers include:

the Australian Sustainable Built Environment Council (ASBEC) report, Investing in Cities (2015), aimed at “maximising the benefits created by the world’s most urbanised nation”; and

COAG’s review of metropolitan planning strategies to ensure matching and orderly infrastructure provision (2011).

Ideas and inspirations abound

Several seers lit the ideological torches for the new infrastructural urbanism. Ed Glaeser’s Triumph of the City is a paean to proximity, density and light-handed regulation. In The Rise of the Creative Class, Richard Florida broadcast the competitive advantage of attracting human capital. Enrico Moretti’s The New Geography of Jobs (2012) demonstrated the multiplier effects of urban “brain hubs”.

In the UK, the Cameron government’s City Deals policy highlights an attractive model of bespoke multi-target programs for competing cities. It is aimed squarely at economic growth underpinned by enhanced tax revenue from development.

While the cities component of the new portfolio is crystallising publicly, what of the built environment? In exploring a model that works for the Coalition another exemplar is the UK’s Commission for Architecture and the Built Environment (1999-2011). Although emasculated in a purge of quangos, it was widely respected as an adviser and advocate for quality design and valuation of the public realm.

Run leanly and through a similar mix of design reviews, publications, research forums and an adviser network, an Australian adaptation could assume a timely leadership position. It would be a vehicle for many voices to be heard, not just the property and development sector. Turnbull tacitly recognised the value of this when he announced that his summer reading included Marcus Westbury’s primer for DIY urbanism, Creating Cities.

Marcus Westbury talks about the creative renewal of his home city of Newcastle.

Quite a few federal activities might be connected under this umbrella. These include State of Australian Cities reporting; the National Australian Built Environment Ratings System (NABERS); various environmental policies including management of national and Commonwealth heritage lists; leased federal airports, which have become development hotspots; the National Capital Authority; the Australian Housing and Urban Research Institute (AHURI) and the Australian Urban Research Infrastructure Network (AURIN).

Given the importance of evidence-driven policy, it is unfortunate that urban-related research is under-supported by the Australian Research Council. It barely registers in its research priorities.

Urban policy is complex because it potentially links up and intrudes into many arenas of government. The cities ministry and the new interdepartmental taskforce sit within the Environment Department overseen by Greg Hunt. As shadow minister for cities, Anthony Albanese has warned of “convoluted administrative arrangements”, with five ministers sharing responsibilities for cities and infrastructure policy.

Former professor of public administration Martin Painter identified the “impossibility of urban policy” because of insoluble administrative problems flowing from taking too comprehensive a position. His advice was “the simpler the better”.

Briggs’ successor will likely continue down the same path with a discussion paper, a national forum with the prime minister speaking, and that meeting of planning ministers to talk through approaches and decisions. There are now huge expectations that a new urban age has dawned in Australia.

Author: Robert Freestone, Professor of Planning, Faculty of Built Environment, UNSW Australi

Many Australians want to grow old at home with family and friends. Yet most have homes that are inaccessible. Without intervention now, taxpayers will be asked to deal with the unintended consequences for the health, aged care and disability budgets.

We all know people who go to hospital and do not return home because they can no longer climb the stairs, get down the hall, or use the bathroom. The alternative is an extended hospital stay while they wait for expensive modifications, or placement in some distant residential facility.

The fix?

Community and housing industry leaders agreed with the federal government a voluntary national guideline and a plan to provide basic access features in all new housing by 2020. Governments at all levels endorsed this agreement through their housing, aged and disability policies. This includes COAG’s 2010-2020 National Disability Strategy.

Adding these features at the design stage is cheap and easy to do. One cost estimate is A$200-$1,000 per dwelling. This would provide:

An accessible path of travel from the street or parking area to and within the entry level of a dwelling;

Doorways, corridors and living spaces on the entry level which most people can use;

One bathroom, shower and toilet that most people can use, with reinforcement in the walls for easy installation of grab-rails if required.

The agreement does not solve the housing needs of people with significant long-term disability. This requires more thought. But it does allow most people to manage unexpected disability, illness or frailty until more substantial changes can be made.

Just as importantly, it allows friends and family who have mobility difficulties to visit and be part of family life.

Voluntary approach isn’t working

A 2015 review of the agreement indicated that the voluntary approach has failed. It estimated that, without intervention, less than 5% of the agreed 2020 target would be achieved.

Most housing is designed and built long before the buyer comes along. Builders build what has sold in the past and what they think buyers might aspire to in the future. Their experience is that most buyers do not aspire to be old, disabled or frail, so access is not high on their agenda – but it should be.

Although the features are easy and cheap to install, a change to new practices has its risks and can be expensive. Contrary to the notion that a single builder builds a home, housing construction constitutes a complex web of subcontractors and suppliers. Each is dependent on the other to avoid delays or unexpected costs.

A simple change, such as wider doorways, can throw out the preceding and following trades, and both time and money are lost.

From the housing industry’s point of view, the estimated cost of voluntarily providing these features is much greater. It is simpler to keep doing the same – there will always be a buyer at the end.

The housing industry acknowledges that when change is necessary for the common good, regulation is required. The industry first resists, then makes the change. The “conveyor belt” of housing construction adjusts, and business continues as usual.

A home’s design affects people’s lives throughout its lifetime, so many others bear the secondary costs of inaccessible design. Providing access in a home after it is built is 19 times more expensive than if it was included from the start. But it is the tertiary costs to health, ageing and disability programs that are of real concern.

The National Disability Insurance Scheme and the aged care reforms – Australia’s most ambitious and costly social programs in a generation – are based on the premise that it is both socially and economically responsible to keep people connected. This includes participating in community and family life for as long as possible.

What now?

Australia needs only to look to other countries to understand what needs to be done. The UK has legislated for minimum access in all housing since 1999. For three decades, Japan has provided financial incentives for the housing industry to build accessible housing.

Although these strategies are not without their problems, they have clearly changed the housing industry for the better.

The federal government must let go of the voluntary approach, to think long-term and regulate for minimum access features in the National Construction Code for all new housing. The agreed 2020 target can then be achieved.

As a nation that prides itself on embracing difference, a national accessible housing code is a good place to start.

Author: Margaret Ward, Research Fellow, School of Human Services and Social Work, Griffith University

Dwelling approvals decreased in November in Australian Capital Territory (-9.3 per cent), Western Australia (-4.5 per cent), New South Wales (-2.8 per cent), Tasmania (-2.6 per cent), Victoria (-2.4 per cent) and Northern Territory (-0.6 per cent) but increased in South Australia (3.2 per cent) and Queensland (0.9 per cent) in trend terms.

In trend terms, approvals for private sector houses was flat in November. Private sector house approvals fell in Western Australia (-2.2 per cent) and New South Wales (-0.5 per cent) but rose in South Australia (1.9 per cent), Victoria (1.3 per cent) and Queensland (0.1 per cent).

The value of total building approved fell 0.8 per cent in November, in trend terms, and has fallen for four consecutive months. The value of residential building fell 1.2 per cent while non-residential building was flat.

The HIA has published “The Residential Outlook for 2016”.

In 2015 new dwelling commencements increased for a third consecutive year in 2014/15 to a record high of 211,860. It is only the fifth time in the past sixty years that commencements (housing starts) have racked up three straight years of growth. The record level of nearly 212,000 starts is 13 per cent higher than the previous cyclical high of 187,000 reached all the way back in 1994.

Renovations activity is still grinding out a recovery, with little sign at this stage of accelerating momentum.

The residential property price growth cycle has peaked, but it’s a very disparate geographical story – if you don’t live in Sydney or Melbourne then you don’t have a boom.

Looking forward, there is upward momentum evident for only three out of thirteen variables (plus we’re calling investment lending for new properties as being ‘neutral’, although some would call it down), compared to six pointing up in the middle of the year and ten last summer. As of the end of 2015, nine variables are now pointing down. This is the weakest HIA/ACI Housing Indicator Profile in over four years.

The key points to note about this housing cycle are:

the changing mix of what we build;

the large geographical divergences across states and territories;

the downside risk to new home construction from 2016/17.

There are very different trajectories evident for the various types of building approvals and dwelling commencements reported by the Australian Bureau of Statistics – semi-detached dwellings compared to units of four storeys or more, for example. The dwelling composition forecasts produced by Australian Construction Insights, the consultancy arm of HIA Economics, suggests further upward momentum in the short term for: detached houses; semi-detached dwellings (of two storeys); and units of one or two storeys.

On the topic of geography, momentum is clearly with the eastern seaboard markets, including some renewed promise for the southeast corner of Queensland. New South Wales is the strongest housing market in Australia, followed by Victoria. The Scorecard has accurately picked the shifting geographical sands for housing markets over the last couple of years, as has the CommSec State of the States report in terms of broader domestic economic conditions.

HIA is forecasting a modest decline of 5.5 per cent in national new dwelling commencements in 2015/16 to a level of just over 200,000. On a calendar year basis commencements are expected to hit 211,490 in 2015, but we see upside risk to this forecast.

In other words, the formal peak for the cycle could turn out to be calendar year 2015 rather than fiscal year 2014/15. The eastern seaboard will drive the short term health of Australia’s new home building sector.

HIA suggest a growth in the value of renovations of 1.6 per cent in 2017/18 and 3.7 per cent in 2018/19 to boost the value of Australia’s renovations market to $31.20 billion.

Australia’s only two strong dwelling price markets – Sydney and Melbourne – will experience a slowing rate of growth in 2016 as the cycle continues to run out of puff. No doubt that trend will provide the doom-sayers with plenty of opportunity to write exaggerated headlines and try to scare the living daylights out of people.

The fact is, outside of Sydney and Melbourne the term ‘housing price boom’ seems like a foreign language. Brisbane was showing signs of joining the eastern seaboard club this time last year – as we noted at the time – but a lack of population growth capped that situation rather quickly. As of November 2015 Brisbane was still the third fastest growing state capital residential property price market in the country behind Sydney (+12.8 per cent yoy) and Melbourne (+11.8 per cent yoy), but at 4.0 per cent per annum you would hardly call Brisbane a boom market.

The aggregate price cycle, heavily masked by Sydney and Melbourne, will continue to experience decelerating growth. Sydney and Melbourne are our two biggest markets and it is appropriate that price growth is slowing. Variable mortgage rates are on the rise under the guise of covering increased funding costs and there may be more of that to come in early 2016. That will dampen price growth. The rationing of credit overseen by APRA has occurred more broadly than justified.

Potentially trailblazing plans for state-assisted financing of affordable housing are emerging in New South Wales. In what looks to be a landmark policy announcement with possible national ramifications, the NSW government last week outlined the first phase of Premier Mike Baird’s March 2015 election commitment to establish a A$1 billion fund for social and affordable housing.

But for the short-lived GFC housing stimulus, this is the first significant rental housing supply subsidy in Australia since the 2008 National Rental Affordability Scheme (NRAS).

While full details are yet to be disclosed, it appears the Social and Affordable Housing Fund (SAHF) will be something like a “future fund” or endowment scheme. Government will invest a capital sum in revenue-generating assets. The resulting returns will underpin annual payments to approved consortia over 25-year terms.

This ongoing subsidy will help community housing providers bridge the gap between rental revenue and operating costs. Most importantly, it includes repayment of construction debt raised from private financial institutions such as banks and super funds. Perhaps in awareness of research evidence on ways to minimise the cost to taxpayers of private finance for affordable housing, officials acknowledged the possibility of a government guarantee or other credit support on loans to consortia.

In principle this is quite a big deal. The more familiar policymaking style involves one-off or pilot initiatives. The SAHF is presented as an ongoing budget commitment to state-supported social and affordable housing growth, with phases two, three and four of the program signalled at the launch.

Second, as the name implies, SAHF is centred on “social” housing: it has a 70% minimum social housing requirement. Unlike schemes such as the NRAS, most of the homes will be financed to allow rents set at levels manageable for very low-income groups rather than affordable only to moderate-income earners.

In the post-GFC world this is highly unusual. For example, only in Scotland does a significant UK social housing investment program remain intact.

Third, and most important, the fund’s creation reflects a long-overdue official recognition that, left to itself, the market does not and cannot provide decent housing that low-income groups can afford.

Big plans, but starting small

Having promised voters a $1 billion housing fund, the Baird government has announced phase one plans for 3,000 homes – a fraction of what’s needed.AAP/Nikki Short

While potentially important in principle, the SAHF is decidedly modest in practice, at least in its initial phase. The statewide target – implicitly to be achieved over several years – is for just 3,000 homes. This will barely scratch, let alone seriously dent, the backlog of 60,000 applicants marooned on the NSW public housing waiting list.

And that’s before you even consider the tens of thousands of unregistered low-income private tenants pushed into poverty by high rents across the state. In Sydney alone, 94,000 families and single people were in this position in 2011. Many if not most will be additional to those on the public housing list.

Nevertheless, there’s a lot to like in the NSW government’s approach. It puts non-profit community housing providers (CHPs), which have a strong track record of high-quality tenancy management, front and centre. Registered CHPs will manage all SAHF housing.

The scheme offers a long-term (up to 25 years) operating subsidy that can be matched to a private financing deal. This gives private investors like super funds the certainty they need. “We’ve listened and we’ve read the reports on that,” officials said.

And it recognises the cost to social landlords of co-ordinating services for tenants who have support needs: the operating subsidy will include a component for this. The 2010 Henry review of taxation recommended this.

Limits to affordable land must be overcome

Having access to land at an affordable price is fundamental to successful affordable housing strategies. Phase one of the SAHF relies on unlocking land to develop social housing owned by churches, NGOs and other philanthropic sources. This is a finite strategy and we query whether well-located sites for 3,000 dwellings will be forthcoming? What then?

The state government has the two-part answer in its power. First, it must require all medium- and large-scale residential projects to include a reasonable component of affordable housing. For Sydney, we suggest a city-wide target in the region of 15-25%.

There is a once-in-a-generation opportunity right now in Sydney to do this as large-scale redevelopment plans unfold along transport corridors, in precincts and renewal areas. Once developers have bought up that land it will be too late. They need to be able to factor into their feasibility plans the cost of providing the affordable housing, and thereby reduce the price they offer for sites.

Second, state and local government-owned land made available for affordable housing (for example, public housing estates slated for renewal, surplus government sites and air spaces above public sites) must be priced at a level that affordable housing developers can afford to pay to keep their costs (and therefore the government operating subsidy exposure) to a minimum.

Only by linking its financing strategy with favourable pricing of state land offers and planning policy changes will the SAHF be scalable and durable – offering potential to reduce the unacceptably high levels of unmet housing need.

Premier Baird is expected to announce further details of the fund early in the new year. With worsening affordable housing shortages around the country, it must be hoped that the prime minister, his treasurer and his cities minister, as well as premiers and treasurers across Australia, will tune in to learn more on this constructive initiative.

Authors: Hal Pawson, Associate Director – City Futures – Urban Policy and Strategy, City Futures Research Centre, Housing Policy and Practice, UNSW Australia; Vivienne Milliga, Associate Professor – City Futures Research Centre, Housing Policy and Practice, UNSW Australia.