DFA research was featured in a Sydney Morning Heald feature today “Banks look vulnerable as lucrative loans market gets personal online” by banking reporter Clancy Yates. The article nicely highlights some of the interesting and potentially disruptive plays in the evolving Australian market, including the peer-to-peer lending sector.

Category: Channel Usage

Digital Disruption

DFA research was featured in a recent The Advisor article.

Brokers have the mortgage market in the palms of their hands – for now – but will the tech-savvy borrowers of the future always need their help? The Adviser reports.

Ask any broker if they can ever see a future in which borrowers go online for their home loan – a complete, end-to-end solution – and the response is always the same: “A mortgage is the biggest financial decision you will ever make, and people want a professional to guide them through that.”

Certainly, this seems to be the case now: broker market share is at an all-time high. What brokers don’t write is written by the banks’ direct channels, with few home loans written online.

As Loans.com.au founder Kim Cannon says, “Many people still get confused with online lending. It is really a lead generation business.”The online offering in Australia remains underdeveloped, and this is good news for brokers and branch managers.

But what do their customers really want? Are they rushing out to see a broker because they want to, or because it is really only one of two options?

This is an interesting, albeit controversial question. But it’s critical to ask it if we are to have an open-minded, mature discussion about the future of mortgage distribution.

Nobody really knows the answer; that will become clearer in time.

What is perfectly clear right now, however, is that a growing number of Australians are using digital devices to source their information.

According to US-based market research firm eMarketer, Australia boasts the highest tablet penetration in the Asia-Pacific region.

The firm found that nearly 60 per cent of Australian internet users will use a tablet this year.In 2014, a Deloitte media survey found smartphone ownership has increased significantly among Australians over the past three years, with 89 per cent now owning a smartphone.

Meanwhile, the same survey found 53 per cent of respondents owned a smartphone, personal computer and tablet.

Of those that did not own a smartphone, 32 per cent plan to purchase one in the next 12 months.

Of those that did not own a tablet, 33 per cent plan to purchase one in the next 12 months and 11 per cent in the next 6 months.

With no end in sight to the digital migration, brokers need to ask themselves where they fit in. What part do you play in all this?

There is a fresh generation of borrowers on the horizon, tablet in one hand, smartphone in the other.

They will soon be demanding a home loan – ASAP. Everything else happens at the click of a button or swipe of the finger, so why not this?

These borrowers have no memory of life before the internet and have been raised on a steady diet of instant access and reward. They have little patience for slow connections. But they need a home loan – now.

Will they visit a broker? Will they go to the bank? Or will some enterprising tech giant meet their demands with a quick and easy, online solution?

Natives, migrants and Luddites

There are three key themes or strands to the issue of online lending.

The first is search, which essentially involves people going online to do comparative searches between different products and then applying direct through one of the lenders.

Then there is the next stage, which is trying to do the whole thing online, applying online and transacting all the way through.

And third, there is peer-to-peer lending: a whole new and quite different kind of animal – and probably the most disruptive one.

Martin North, principal of Digital Finance Analytics (DFA), surveys 26,000 consumers each year and specifically looks at their channel preferences and how they go about buying products.

“The big thing I am noticing is there is a significant rise in those who, as a first point of interaction online, want to go and find things out for themselves,” Mr North tells The Adviser.

“I split the population between digital natives, digital migrants and digital Luddites,” he explains.

Digital natives tend to be a bit younger. They are naturally online and use social networks. These people are very in tune with going online to search the different options and maybe even checking social media and arriving at a conclusion of what they want to do.

From the population base, they make up around 35 per cent of households in the market for financial services.

Then you’ve got the Luddites, who really don’t do much online and aren’t really interested. They never go near the online environment at all. They are going to the branches and the brokers. They are about 30 per cent of the population.

Those in the middle are the digital migrants – they are migrating towards the online environment but are still relatively cautious about online channels.

The average mortgage broker, aged in their early 50s, sits somewhere between the Luddite and the digital migrant, says Mr North.

“So which segments of the population are more inclined to go online? The natives. Therefore, anyone thinking about online has to be thinking about what they are doing because they are the future,” he says.

The online lending space

There are very few end-to-end propositions within which borrowers can go online and apply for a mortgage all the way through. In terms of transacting, it’s clunky.

NAB has been the most successful so far – with UBank, its answer to no-frills online banking.

Last year, UBank mortgages grew from $2.2 billion to $2.7 billion in the six months to March 31, an increase of 22.8 per cent.

That was 12 months ago.

Then-chief executive Alex Twigg said the growth is evidence of a global shift towards online mortgage distribution.

“We have had a significant uptake in our mortgage volumes direct through UBank and you will see that across the globe,” Mr Twigg says.

“Fifteen years ago, across the UK, there was a significant move towards online mortgages; you’ve seen it happen in the US; and you are now seeing it happening in Australia.”

While yet to launch a complete online mortgage solution, CBA is widely considered to be the leader of the major banks in terms of digital.

The lender spent a billion dollars upgrading its systems, giving customers some smart new apps and online banking capabilities in the process.

“If I have a look at how our customers interact with us, you go back five years and a lot more transactions occurred in a branch or maybe online,” says CBA’s group executive of institutional banking and markets, Kelly Bayer Rosmarin. “Now, upwards of 65 per cent of our transactions occur on a mobile phone or iPad in a mobile way.”

However, CBA’s head of mortgages, Clive Van Horen, says digital disruptors represent a real threat, particularly overseas where they have made significant progress in the home loan space.

“In the US you have Quicken Loans,” Mr Van Horen says.

“Fifteen years ago they were an accounting software company and today they are the second biggest writer of mortgages in the United States, behind Wells Fargo.

“They have a digital contact centre – they don’t have branches. I’m not saying they are going to be in Australia in the next few months, but digital disruptors can very quickly enter the market.

“I think the challenge they would have is overcoming the multiple touch-points of the banks,” Mr Van Horen says.

Multiple touch-points marry the digital experience with the face-to-face experience, Mr Van Horen adds, as CBA looks to adapt its offering for customer convenience.

“A customer might want to talk to somebody in person, or pick up the phone, or go online and they don’t want to have to re-enter information and go through everything from scratch, so that is something we have been integrating across all channels,” he says.

“A customer can start a mortgage application online and finish in a branch or a mobile lender can visit them. It is much more integrated.”

This omni-channel experience is one that the big banks have touted for a while, says DFA’s Martin North.

However, most of the majors are completely conflicted because they have the branch and the third-party channel competing with each other and Mr North feels that, as a result, the online element is not getting a fair look-in.

“Most of the people I talk to in the large institutions are talking about an omni-channel experience,” he says. “I think that’s crap. From the research I have done and looking at a forward perspective, we are past omni-channel.

“It is now time to think really hard about the strategic relevance of digital and online and build your strategy around that and move away from branch and broker channels.”

What borrowers want

The majors are still struggling with the digital element, regardless of how much they are investing in new technology.

“The banks will tell you that they believe most customers want to have a face-to-face conversation. Well I’m not sure that’s true anymore,” says Mr North.

He points to the use of digital devices in Australia and argues that the conundrum is that most of the incumbents are still denying a digital revolution is taking place.

When Mr North surveys consumers about their channel preferences, he asks them two questions: what do they currently do, and what would they like to do.

People are frustrated and constrained about what they can do, he says.

“The digital natives tell me they don’t need face-to-face. They say, ‘If I can interact in some other way, that’s fine by me, but in Australia I can’t do that because nobody allows me to’.

“So there is an expectation gap between what most players are offering and what those digital natives particularly want,” he says.

The economic argument, however, is even stronger, Mr North continues.“Profitability is higher among digital natives and digital migrants than digital Luddites,” he says. “So if they are not careful, the major banks are going to effectively continue to try and service customers who become less and less profitable over time.

“It doesn’t make any economic sense to me.”

Another worrying issue for brokers and banks is that new entrants could beat them to the punch.

The Deloitte Australian Mortgage Report 2014 surveyed a panel of major lenders, non-banks and large broker groups and found that new online channels will be the greatest non-major mortgage competitors of the future.

Mortgage Choice’s outgoing chief executive Michael Russell said the strong digital brands are a concern.

“Google, Yahoo, Coles, Woolworths and Apple are the ones that alarm me in terms of their capability to quickly morph into a financial services business,” he says.

ING Direct’s executive director of distribution, Lisa Claes, says the digital giants such as Apple, Google and PayPal could be successful in the mortgage space.

“There is a credible school of thought that they will continue to penetrate financial services,” Ms Claes says. “The digital giants could be successful.”

The threat of new entrants is also on the regulator’s radar and has been a significant theme of the Financial System Inquiry.

Speaking at the ASIC Annual Forum in Sydney last year, ASIC deputy chair Peter Kell said digital players and consumer brands are in the regulator’s sights.

“Do we anticipate that there will be a potential range of new players that we will have to deal with within a fairly short space of time?” Mr Kell said.

“I would say definitely yes, and some of them are already there.

“You can see some of those big supermarkets, for example, wanting to sell insurance and potentially moving into other financial products, and we will be ensuring we have a level playing field and making sure they treat customers fairly.”

Where brokers fit in

There are really only two online lenders that compete with the third-party and direct channels: NAB’s UBank and Firstmac’s Loans.com.au.

According to Sydney-based broker Alex Lambros, the UBank product is not as competitive as the Loans.com.au offering, which is a threat to his business.

“It is a basic type of offering and fits some borrowers,” Mr Lambros says.

“We come up against that every now and again.”

But while the UBank offering does not concern him, the fact that NAB has an online offering is interesting, he says.

“They are in the broker market, they support it – or they say they support it – yet they still provide a cheaper alternative, even though it is a pretty black and white product,” Mr Lambros says.

In fact, the basic, no-frills nature of the current online product range works in a broker’s favour – the rigidity of an online vanilla home loan will essentially limit to whom it appeals.

Kim Cannon, who launched Loans.com.au three years ago, says borrowers drawn to the online lender are not the young, digitally-native first home buyers you might expect.

“There are certain people who need their hand held through the loan process and people who don’t,” Mr Cannon says. “We rarely see a first home buyer or young person come through Loans.com.au.

“They either go to a branch or a broker because they need that advice.”

More than anything, the online customer is rate-focused and demands a quick and easy process, according to Mr Cannon.

Loans.com.au is undergoing constant improvements to enhance the experience and make it simpler for borrowers to obtain a loan as quickly as possible.

“Every week we are working through a new process, a better way of doing things. You are always looking at gaining that edge – how do we make it faster without denying quality?” Mr Cannon says.

“We are looking at the [valuation firm] ValEx process at the moment and how we can improve that. A valuation may only take a day and a half to go through ValEx, but there are still delays.”

With all these improvements going on, is it not reasonable to expect the online space to develop into a legitimate channel in the not too distant future?

Nevertheless, Mr Cannon believes brokers will always have the upper hand in the mortgage market. Besides, he says, the digital enhancements to his online option flow through to the rest of his third-party business.

“The brokers get the benefit of all of that,” he says. “We have been looking at our credit process and what we were doing and overdoing. Just doing a review like that meant we were able to speed up our decision-making processes and cut a lot of the unnecessary stuff out. Now that has been passed on to the broker channel and brokers are seeing the benefit.

“People may see Firstmac and Loans.com.au as channel conflict but I see it as channel improvement to some degree.”

The opportunity for brokers

So, while online lending may well represent a threat to brokers, it can also be an opportunity.

Borrowers who need mortgage advice, first home buyers and those with more complex borrowing needs will become the target market for the broker of the future.

It is here that diversification comes into play, as brokers with multiple offerings and a diverse skillset develop unique service propositions that compare favourably with online alternatives.

Tailored solutions will always require a specialist.

Online lenders will be looking to ramp up their offerings, enhancing their capabilities and gaining market share as a result.

To combat this, brokers must use diversified offerings as a first line of defence, says Moshe Moses, director of Astute Financial Sydney City Central.

“The home loan broker has to be aware that there are two facets to their business. It is not just about writing a loan – a computer can do that for you now – it is about providing the service and being able to offer more than a mortgage,” Mr Moses says.

“A lot of our customers have come and discussed UBank. But we say to them that they don’t have a face behind it, they don’t have a touch-point.

“CBA came out with HomePath, which fell flat on its face when it was introduced,” he says.

The Commonwealth Bank closed its low-cost online mortgage business in 2008. All HomePath customers were subsequently transferred over to CBA branded loans.

HomePath represented just 0.5 per cent of all CBA loans and posted a $7.8 million profit for the year ended 30 June 2008.

The issue with these online providers is that there is no human interaction, Mr Moses says, and that is why brokers need to have a diversified offering.

“That then provides the interaction that UBank or any of these other lenders cannot provide,” he says.

There is much more that brokers can do to combat the online threat – as long as they are willing to ensure they have a good platform that provides the service and structure for what a client needs, not just the simple transaction they ask for.

Asia’s Digital-Banking Boom

According to McKinsey, among the consumers surveyed in developed Asian markets, including Australia, more than 80 percent said they were willing to shift some of their holdings to a bank that offers a compelling digital proposition. Further evidence for the digital disruption incumbents are facing and highlighted in our “Quiet Revolution” report, which looks in detail at consumer preferences in Australia.

Here is the McKinsey commentary. You can get their full report here.

Since 2011, adoption of digital-banking services has soared across Asia. Consumers are turning to computers, smartphones, and tablets more often to do business with their banks, while visiting branches and calling service lines less frequently. In developed Asian markets, Internet banking is now near universal, and smartphone banking has grown more than threefold since 2011. In emerging Asian markets, the trend is similarly dynamic, with about a quarter of consumers using computers and smartphones for their banking. And despite some structural obstacles, we believe this surge will continue—and incumbents and market entrants alike should prepare for the consequences.

Last year, we surveyed about 16,000 financial consumers in 13 Asian markets,1 and the results showed drastic shifts in behavior compared with a similar survey in 2011. Put simply: Asian financial-services consumers are going digital, and fast. While this rise of digital banking has been anticipated for many years, several factors have combined to accelerate it, most notably the rapid increase in Internet and smartphone adoption and growth in e-commerce. Both have helped demand for digital banking move from early adopters to a broad range of customers.

For incumbent banks, the stakes are particularly high. Among the consumers we surveyed in developed Asian markets, more than 80 percent said they were willing to shift some of their holdings to a bank that offers a compelling digital proposition. In emerging Asia, more than 50 percent of consumers indicated such willingness. Many types of accounts are in play, with respondents saying generally that they could shift 35 to 45 percent of savings-account deposits, 40 to 50 percent of credit-card balances, and 40 to 45 percent of investment balances, such as those held in mutual funds.

Across Asia, we estimate more than 700 million consumers use digital banking regularly, with a significant portion in fast-growing markets like China and India. In developed Asia, 92 percent of respondents in 2014 said they had used Internet banking, compared with 58 percent in 2011. Also, 61 percent had accessed banking services using smartphones, more than three times the penetration seen in 2011. Behaviors in emerging markets showed a faster shift, although from a much smaller base. Internet-banking penetration in these markets rose from 10 percent in 2011 to 28 percent in 2014, and smartphone access rose from 5 percent in 2011 to 26 percent in 2014.

Further, customers across Asia are using digital banking more frequently. In developed Asia, customers connect with their banks over the Internet or via smartphones more often each month than over traditional channels. In emerging Asia, these traditional channels, especially ATMs, still dominate, but customers are using Internet and smartphone banking almost five times more often than in 2011. Across Asia, consumers made fewer branch visits and calls in 2014 than in 2011.

The rapid shift toward digital banking might suggest the demise of the bank branch, but several factors assure that branches will retain an important role in Asia for the foreseeable future. For example, consumers are using multiple channels, rather than turning solely to online or branch services. Regulatory requirements, demand for personal advice, and a sense of security support the continued need for branches, the survey shows.

Drawing in digital consumers will require more than an online presence, even one that is best in class.2 Our research shows that in developed Asia, consumers value the quality of basic services, the strength of financial products, brand reputation, and the quality of customer service and experience. Among these, they are typically least satisfied with the financial products offered and with customer experience. Survey results from emerging Asia were less conclusive, indicating these markets are at the early stages in digital banking.

Our findings also show that simplicity and security are crucial aspects for online offerings. Of banking customers who have not made any online purchase of banking products, 47 percent in developed Asia and 35 percent in emerging Asia said the primary obstacle is that the products are so complicated that they needed a person to explain them. At the same time, security concerns stopped about 56 percent of the respondents in emerging Asia and 44 percent of those in developed Asia from purchasing products online.

FCC And Net Neutrality

Net neutrality is important because it means that internet service providers need to make all content available from providers to consumers without any differentiation in terms of charging or quality of service for different types of traffic. It can apply to content including telephony, web browsing, video, television, and other digital services. Following legal battles in the USA, the Federal Communications Commission has set sustainable rules of the roads that will protect free expression and innovation on the Internet and promote investment in the nation’s broadband networks. It is an important stake in the ground, and means the internet will be more open, not less. So far as Australia is concerned, we think it is time to consider the right neutrality settings here. Today we have rules which assume television broadcasting is different from other content, and various barriers which limit competition, consumer choice, and keep content pricing higher than they should be. Given the emerging role of the NBN, It’s time that Australia carried out a broad based review into net neutrality and how it should be applied to the local telecommunications and content provider industries.

Here are details of the US announcement.

The FCC has long been committed to protecting and promoting an Internet that nurtures freedom of speech and expression, supports innovation and commerce, and incentivizes expansion and investment by America’s broadband providers. But the agency’s attempts to implement enforceable, sustainable rules to protect the Open Internet have been twice struck down by the courts.

The Commission—once and for all—enacts strong, sustainable rules, grounded in multiple sources of legal authority, to ensure that Americans reap the economic, social, and civic benefits of an Open Internet today and into the future. These new rules are guided by three principles: America’s broadband networks must be fast, fair and open—principles shared by the overwhelming majority of the nearly 4 million commenters who participated in the FCC’s Open Internet proceeding. Absent action by the FCC, Internet openness is at risk, as recognized by the very court that struck down the FCC’s 2010 Open Internet rules last year in Verizon v. FCC.

Broadband providers have economic incentives that “represent a threat to Internet openness and could act in ways that would ultimately inhibit the speed and extent of future broadband deployment,” as affirmed by the U.S. Court of Appeals for the District of Columbia. The court upheld the Commission’s finding that Internet openness drives a “virtuous cycle” in which innovations at the edges of the network enhance consumer demand, leading to expanded investments in broadband infrastructure that, in turn, spark new innovations at the edge.

However, the court observed that nearly 15 years ago, the Commission constrained its ability to protect against threats to the open Internet by a regulatory classification of broadband that precluded use of statutory protections that historically ensured the openness of telephone networks. The Order finds that the nature of broadband Internet access service has not only changed since that initial classification decision, but that broadband providers have even more incentives to interfere with Internet openness today. To respond to this changed landscape, the new Open Internet Order restores the FCC’s legal authority to fully address threats to openness on today’s networks by following a template for sustainability laid out in the D.C. Circuit Opinion itself, including reclassification of broadband Internet access as a telecommunications service under Title II of the Communications Act.

With a firm legal foundation established, the Order sets three “bright-line” rules of the road for behavior known to harm the Open Internet, adopts an additional, flexible standard to future-proof Internet openness rules, and protects mobile broadband users with the full array of Open Internet rules. It does so while preserving incentives for investment and innovation by broadband providers by affording them an even more tailored version of the light-touch regulatory treatment that fostered tremendous growth in the mobile wireless industry.

Following are the key provisions and rules of the FCC’s Open Internet Order:

New Rules to Protect an Open Internet

While the FCC’s 2010 Open Internet rules had limited applicability to mobile broadband, the new rules—in their entirety—would apply to fixed and mobile broadband alike, recognizing advances in technology and the growing significance of wireless broadband access in recent years (while recognizing the importance of reasonable network management and its specific application to mobile and unlicensed Wi-Fi networks). The Order protects consumers no matter how they access the Internet, whether on a desktop computer or a mobile device.

Bright Line Rules: The first three rules ban practices that are known to harm the Open Internet:

- No Blocking: broadband providers may not block access to legal content, applications, services, or non-harmful devices.

- No Throttling: broadband providers may not impair or degrade lawful Internet traffic on the basis of content, applications, services, or non-harmful devices.

- No Paid Prioritization: broadband providers may not favor some lawful Internet traffic over other lawful traffic in exchange for consideration of any kind—in other words, no “fast lanes.” This rule also bans ISPs from prioritizing content and services of their affiliates.

The bright-line rules against blocking and throttling will prohibit harmful practices that target specific applications or classes of applications. And the ban on paid prioritization ensures that there will be no fast lanes.

A Standard for Future Conduct:

Because the Internet is always growing and changing, there must be a known standard by which to address any concerns that arise with new practices. The Order establishes that ISPs cannot “unreasonably interfere with or unreasonably disadvantage” the ability of consumers to select, access, and use the lawful content, applications, services, or devices of their choosing; or of edge providers to make lawful content, applications, services, or devices available to consumers. Today’s Order ensures that the Commission will have authority to address questionable practices on a case-by-case basis, and provides guidance in the form of factors on how the Commission will apply the standard in practice.

Greater Transparency:

The rules described above will restore the tools necessary to address specific conduct by broadband providers that might harm the Open Internet. But the Order recognizes the critical role of transparency in a well-functioning broadband ecosystem. In addition to the existing transparency rule, which was not struck down by the court, the Order requires that broadband providers disclose, in a consistent format, promotional rates, fees and surcharges and data caps. Disclosures must also include packet loss as a measure of network performance, and provide notice of network management practices that can affect service. To further consider the concerns of small ISPs, the Order adopts a temporary exemption from the transparency enhancements for fixed and mobile providers with 100,000 or fewer subscribers, and delegates authority to our Consumer and Governmental Affairs Bureau to determine whether to retain the exception and, if so, at what level. The Order also creates for all providers a “safe harbor” process for the format and nature of the required disclosure to consumers, which the Commission believes will lead to more effective presentation of consumer-focused information by broadband providers.

Reasonable Network Management:

For the purposes of the rules, other than paid prioritization, an ISP may engage in reasonable network management. This recognizes the need of broadband providers to manage the technical and engineering aspects of their networks.

- In assessing reasonable network management, the Commission’s standard takes account of the particular engineering attributes of the technology involved—whether it be fiber, DSL, cable, unlicensed Wi-Fi, mobile, or another network medium.

- However, the network practice must be primarily used for and tailored to achieving a legitimate network management—and not business—purpose. For example, a provider can’t cite reasonable network management to justify reneging on its promise to supply a customer with “unlimited” data.

Broad Protection

Some data services do not go over the public Internet, and therefore are not “broadband Internet access” services (VoIP from a cable system is an example, as is a dedicated heart-monitoring service). The Order ensures that these services do not undermine the effectiveness of the Open Internet rules. Moreover, all broadband providers’ transparency disclosures will continue to cover any offering of such non-Internet access data services—ensuring that the public and the Commission can keep a close eye on any tactics that could undermine the Open Internet rules.

Interconnection: New Authority to Address Concerns

For the first time the Commission can address issues that may arise in the exchange of traffic between mass-market broadband providers and other networks and services. Under the authority provided by the Order, the Commission can hear complaints and take appropriate enforcement action if it determines the interconnection activities of ISPs are not just and reasonable.

Legal Authority: Reclassifying Broadband Internet Access under Title II

The Order provides the strongest possible legal foundation for the Open Internet rules by relying on multiple sources of authority including both Title II of the Communications Act and Section 706 of the Telecommunications Act of 1996. At the same time, the Order refrains – or forbears – from enforcing 27 provisions of Title II and over 700 associated regulations that are not relevant to modern broadband service. Together Title II and Section 706 support clear rules of the road, providing the certainty needed for innovators and investors, and the competitive choices and freedom demanded by consumers, while not burdening broadband providers with anachronistic utility-style regulations such as rate regulation, tariffs or network sharing requirements.

- First, the Order reclassifies “broadband Internet access service”—that’s the retail broadband service Americans buy from cable, phone, and wireless providers—as a telecommunications service under Title II. This decision is fundamentally a factual one. It recognizes that today broadband Internet access service is understood by the public as a transmission platform through which consumers can access third-party content, applications, and services of their choosing. Reclassification of broadband Internet access service also addresses any limitations that past classification decisions placed on the ability to adopt strong open Internet rules, as interpreted by the D.C. Circuit in the Verizon case. And it supports the Commission’s authority to address interconnection disputes on a case-by-case basis, because the promise to consumers that they will be able to travel the Internet encompasses the duty to make the necessary arrangements that allow consumers to use the Internet as they wish.

- Second, the proposal finds further grounding in Section 706 of the Telecommunications Act of 1996. Notably, the Verizon court held that Section 706 is an independent grant of authority to the Commission that supports adoption of Open Internet rules. Using it here—without the limitations of the common carriage prohibition that flowed from earlier the “information service” classification—bolsters the Commission’s authority.

- Third, the Order’s provisions on mobile broadband also are based on Title III of the Communications Act. The Order finds that mobile broadband access service is best viewed as a commercial mobile service or its functional equivalent.

Forbearance: A modernized, light-touch approach

Congress requires the FCC to refrain from enforcing – forbear from – provisions of the Communications Act that are not in the public interest. The Order applies some key provisions of Title II, and forbears from most others. Indeed, the Order ensures that some 27 provisions of Title II and over 700 regulations adopted under Title II will not apply to broadband. There is no need for any further proceedings before the forbearance is adopted. The proposed Order would apply fewer sections of Title II than have applied to mobile voice networks for over twenty years.

• Major Provisions of Title II that the Order WILL APPLY:

- The proposed Order applies “core” provisions of Title II: Sections 201 and 202 (e.g., no unjust or unreasonable practices or discrimination)

- Allows investigation of consumer complaints under section 208 and related enforcement provisions, specifically sections 206, 207, 209, 216 and 217

- Protects consumer privacy under Section 222

- Ensures fair access to poles and conduits under Section 224, which would boost the deployment of new broadband networks

- Protects people with disabilities under Sections 225 and 255

- Bolsters universal service fund support for broadband service in the future through partial application of Section 254.

• Major Provisions Subject to Forbearance:

- Rate regulation: the Order makes clear that broadband providers shall not be subject to utility-style rate regulation, including rate regulation, tariffs, and last-mile unbundling.

- Universal Service Contributions: the Order DOES NOT require broadband providers to contribute to the Universal Service Fund under Section 254. The question of how best to fund the nation’s universal service programs is being considered in a separate, unrelated proceeding that was already underway.

- Broadband service will remain exempt from state and local taxation under the Internet Tax Freedom Act. This law, recently renewed by Congress and signed by the President, bans state and local taxation on Internet access regardless of its FCC regulatory classification.

Effective Enforcement - The FCC will enforce the Open Internet rules through investigation and processing of formal and informal complaints

- Enforcement advisories, advisory opinions and a newly-created ombudsman will provide guidance

- The Enforcement Bureau can request objective written opinions on technical matters from outside technical organizations, industry standards-setting bodies and other organizations.

Fostering Investment and Competition

All of this can be accomplished while encouraging investment in broadband networks. To preserve incentives for broadband operators to invest in their networks, the Order will modernize Title II using the forbearance authority granted to the Commission by Congress—tailoring the application of Title II for the 21st century, encouraging Internet Service Providers to invest in the networks on which Americans increasingly rely.

- The Order forbears from applying utility-style rate regulation, including rate regulation or tariffs, last-mile unbundling, and burdensome administrative filing requirements or accounting standards.

- Mobile voice services have been regulated under a similar light-touch Title II approach, and investment and usage boomed.

- Investment analysts have concluded that Title II with appropriate forbearance is unlikely to have any negative on the value or future profitability of broadband providers. Providers such as Sprint, Frontier, as well as representatives of hundreds of smaller carriers that have voluntarily adopted Title II regulation, have likewise said that a light-touch, Title II classification of broadband will not depress investment.

We’re Most Likely To Use Multiple Devices – Survey

Reported in eMarketer, according to H2 2014 research from Asia-Pacific programmatic buying service provider Appier, digital device users in Australia are the most likely of those in any country in the region to own more than two—and more than three—devices. Nearly half of multidevice users in Australia reported using three or more digital devices, vs. 28% of those in last-place Japan or Taiwan, for example.

Multidevice users can be a headache for marketers trying to work out multichannel campaigns. Appier sought to determine how similarly—or differently—multidevice users behaved on their various internet access channels. The research found that more than half of users in Australia had completely different behaviors on each device—while 27% exhibited identical behaviors across devices. There was no discernible relationship between penetration of many devices in a market and users’ likelihood of using them similarly.

That can make it difficult for marketers to, first, identify individuals across all their devices, and second, deliver relevant and timely messages to them based on the device they are using. But there were also some patterns across populations in terms of device-related behaviors.

Appier found that across Asia-Pacific, PC traffic was higher on weekdays than weekends. Smartphone traffic, meanwhile, tended to spike on Saturdays, though users in Australia, Hong Kong, Singapore and Japan actually used smartphones most on Wednesdays. Tablet traffic tended to fall most on weekends. And across devices, men were more active than women.

60% of Australian Internet Users Use a Tablet – eMarketer

Australia enjoys the highest tablet penetration rates in Asia-Pacific, in terms of both internet users and the general population, according to eMarketer’s latest estimates of tablet usage around the world. By the end of this year, tablet penetration among internet users will be more than 10 percentage points higher than in second-place China, and among the population at large, the difference will be more than 20 percentage points.

With a projected 10.3 million tablet users this year, Australia is the only country in Asia-Pacific to have tablets reach a majority of the internet population already, and also the only country in the region where we expect a majority of the total population to use tablets at any point during our forecast period. Even other mature markets in the region, like South Korea and Japan, will have relatively low penetration throughout our forecast period, due to several factors including aging population and high usage of phablets. Australia’s relatively small population, however, means that in absolute numbers, the tablet population is the second-smallest in Asia-Pacific, ahead of South Korea.

With a projected 10.3 million tablet users this year, Australia is the only country in Asia-Pacific to have tablets reach a majority of the internet population already, and also the only country in the region where we expect a majority of the total population to use tablets at any point during our forecast period. Even other mature markets in the region, like South Korea and Japan, will have relatively low penetration throughout our forecast period, due to several factors including aging population and high usage of phablets. Australia’s relatively small population, however, means that in absolute numbers, the tablet population is the second-smallest in Asia-Pacific, ahead of South Korea.

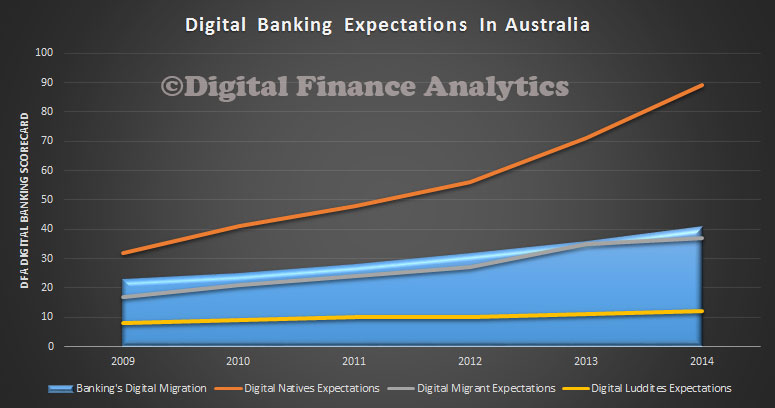

Digital Banking Gap Is Accelerating

Using the latest data from the DFA channel preferences survey, last published in the report “The Quiet Revolution“, today we chart the top line digital banking scorecard, from the demand side, looking at different household groups, and on the supply side what banks are doing to embrace digital. The rate of change in terms of bank participation in digital, is tracking the rate of adoption of those who are Digital Migrants, and they are moving faster than those households in the Digital Luddite segments. However, it appears that whilst the Australian banking sector is moving towards digital, those who are digitally literate – the Digital Natives – have ever more enhanced desire to do more digitally. Indeed, the digital gap between expectations and delivery is widening. You can read about our digital segmentation here.

The rate of digital migration is closely tracked by the uptake of smart phones and tablets. Digital Natives are the most likely to be using one of these smart devices, and they have a strong desire to manage their entire financial service footprint digitally. This is true whether it is buying a mortgage, making a payment, or checking a transaction. We know from our profitability analysis that Digital Natives are on average more valuable to the industry, tend to be younger, and better educated, and are significantly less likely to enter a bank branch for any purpose. They use social media and online search tools, and trust these information channels more than a typical bank. They also have high expectations in terms of customer service delivery, and personalization. Many banking players are not meeting these expectations.

The rate of digital migration is closely tracked by the uptake of smart phones and tablets. Digital Natives are the most likely to be using one of these smart devices, and they have a strong desire to manage their entire financial service footprint digitally. This is true whether it is buying a mortgage, making a payment, or checking a transaction. We know from our profitability analysis that Digital Natives are on average more valuable to the industry, tend to be younger, and better educated, and are significantly less likely to enter a bank branch for any purpose. They use social media and online search tools, and trust these information channels more than a typical bank. They also have high expectations in terms of customer service delivery, and personalization. Many banking players are not meeting these expectations.

DFA is of the view that banks need to accelerate their rate of migration to the digital world, and position to respond to the rising number of new entrants which have the potential to disrupt significantly. We recently discussed Apple Pay, PayPal and Ratesetter. Each of these have potentially disruptive impact. As we said recently:

“DFA has just updated the 26,000 strong household survey examining their channel preferences. This report summarises the main findings.

We conclude that the move towards digital channels continues apace, facilitated by new devices including smartphones and tablets, and the rise of “digital natives” – people who are naturally connected.

We outline the findings across each of our household segments, and also introduce our thought experiment, where we tested household’s attitudes to the various existing and emerging brands in the context of digital banking. We found a strong affinity between digital natives and the emerging electronic brands, and a relative swing away from the traditional terrestrial bank players.

These trends create both threat and opportunity. The threat is that traditional channels, especially the branch, become less relevant to digital natives, and becomes the ghetto of older, less connected, less profitable customers. The future lays in the digital channels, where the more profitable and digitally aware already live. Players need to migrate fast, or they will be overtaken by the next generation of digital brands who are looking towards becoming players in financial services. The game is on!”

Apple and the Payments Revolution

Apple’s latest product announcements included some details about their Apple Pay service, which as we highlighted previously is clearly part of an innovation strategy which will potentially have a profound impact on the payments business and consumer behaviour. Whilst initially US based, Apple Pay is something which has potentially broader consequences. To day we outline the main features of Apple Pay, and reflect on the future impact.

Apple Pay will be built into its new iPhone 6, iPhone 6 Plus, and Apple Watch devices to pay for items via Near Field Communications (NFC), which works by transmitting a radio signal between the device and a receiver, when the two are fractions of an inch apart or touching and will also enable online payments as well. Apple’s motivation, as explained by Tim Cook, was to completely change the current old payments technology, and remove the need to own a physical credit card. Apple said it will speed up the check out process, make payments more secure and ultimately replace physical wallets. Volumes and value of mobile payments are set to rise according to market analysts. Here is a summary from the WSJ.

Here are some of the public comments from Apple:

Here are some of the public comments from Apple:

Gone are the days of searching for your wallet. The wasted moments finding the right card. The swiping and waiting. Now payments happen with a single touch. Apple Pay will change how you pay with breakthrough contactless payment technology and unique security features built right into the devices you have with you every day. So you can use your iPhone 6 or Apple Watch to pay in an easy, secure, and private way.

One touch to pay with Touch ID. Now paying in stores happens in one natural motion — there’s no need to open an app or even wake your display thanks to the innovative Near Field Communication antenna in iPhone 6. To pay, just hold your iPhone near the contactless reader with your finger on Touch ID. You don’t even have to look at the screen to know your payment information was successfully sent. A subtle vibration and beep lets you know.

Double-click to pay and go. You can pay with Apple Watch — just double-click the button below the Digital Crown and hold the face of your Apple Watch near the contactless reader. A gentle pulse and beep confirm that your payment information was sent.

Convenient checkout. On iPhone, you can also use Apple Pay to pay with a single touch in apps. Checking out is as easy as selecting “Apple Pay” and placing your finger on Touch ID.

Passbook already stores your boarding passes, tickets, coupons, and more. Now it can store your credit and debit cards, too. To get started, you can add the credit or debit card from your iTunes account to Passbook by simply entering the card security code.

To add a new card on iPhone, use your iSight camera to instantly capture your card information. Or simply type it in manually. The first card you add automatically becomes your default payment card, but you can go to Passbook any time to pay with a different card or select a new default in Settings.Every time you hand over your credit or debit card to pay, your card number and identity are visible. With Apple Pay, instead of using your actual credit and debit card numbers when you add your card, a unique Device Account Number is assigned, encrypted and securely stored in the Secure Element, a dedicated chip in iPhone and Apple Watch. These numbers are never stored on Apple servers. And when you make a purchase, the Device Account Number alongside a transaction-specific dynamic security code is used to process your payment. So your actual credit or debit card numbers are never shared with merchants or transmitted with payment.

Protect your accounts. Even if you lose your device. If your iPhone is ever lost or stolen, you can use Find My iPhone to quickly put your device in Lost Mode so nothing is accessible, or you can wipe your iPhone clean completely.

Apple doesn’t save your transaction information. With Apple Pay, your payments are private. Apple doesn’t store the details of your transactions so they can’t be tied back to you. Your most recent purchases are kept in Passbook for your convenience, but that’s as far as it goes.

Keep your cards in your wallet. Since you don’t have to show your credit or debit card, you never reveal your name, card number or security code to the cashier when you pay in store. This additional layer of privacy helps ensure that your information stays where it belongs. With you.

Apple Pay works with most of the major credit and debit cards from the top U.S. banks. Just add your participating cards to Passbook and you’ll continue to get all the rewards, benefits, and security of your cards.

Reading further about the service, clearly security is a big focus because instead of storing your card on the phone, Apple Pay creates a dynamic security code. You can add in a new card just by taking an image of it. Touch ID will be used to confirm transactions (fingerprint reading technology) for added security).

Apple Pay will start in the U.S. with Visa, American Express, and Mastercard. As with any e-wallet, the key is getting business to adopt it. Apple has six banks on board and thus far including Bank of America, Capital One Bank, Chase, Citi and Wells Fargo, with more banks later, including Barclaycard, Navy Federal Credit Union, PNC Bank, USAA and U.S. Bank. In terms of merchants, they have named Bloomingdales, Panera, Sephora, Groupon, Subway, Disney, Target, McDonald’s, Whole Foods, Macy’s, and Walgreens. Apple will also accept payments and they will integrate Apple Pay into the Apple ecosystem.

This is Apple’s first foray into NFC payments, in the USA, payments have evolved more slowly than in other countries. For example in Australia, we can use VISA’s PayWave, and Mastercard’s PayPass, collectively known as PayWave. Just touch your card and pay for anything to a limit of $100. Beyond that, you will still need to enter your PIN to confirm the payment. There have been a few phantom payments, and there is a risk of fraud if someone gets hold of your card, but it is highly convenient. In the Apple video about Apple Pay, they suggest existing PayWave devices will be able to handle Apple Pay. The current terminal standards (Ingenico and ViVOPay) are based on global standards and if Apple Pay is compliant to these, no updates to existing systems will be needed.

Consider this, already PayWave looks likely to supplement and even replace the current dedicated smartcards on transport systems like the Oyster card in London, where from mid September, PayWave will be implemented. It could be a simple step to using you phone to pay for trips directly.

There is no word on if and when Apple Pay may arrive in Australia, but the writing is on the wall for a significant shakeup, perhaps. For example, will the NSW Transport Opal transport card now be subsumed? But the real insight is the integration of consumer data, merchant data and the rest, as we highlighted in out earlier post the payments revolution around the corner.