Join us for a live discussion as I explore the data from our models to end December 2021, including post code level analysis of mortgage stress. We will have the post code engine on line, and you can ask as a question live.

Category: Household Survey

Our Latest Mortgage Stress Mapping (Nov 2021)

This is a succinct summary of our latest mortgage stress analysis, based on our surveys. We also add some additional comments about how to address stress at a household level.

Go to the Walk The World Universe at https://walktheworld.com.au/ The original live stream is here:

That Stress Conundrum

A deep dive on household financial stress, based on my recent live show https://youtu.be/0RyvpENjl4E plus additional comments.

Go to the Walk The World Universe at https://walktheworld.com.au/

Household Financial Stress Update To Sept 2021

We discuss the September 2021 DFA Household survey results. Many households remain in a difficult position, as cash-flows remain negative thanks to crushed incomes, rising costs and bigger mortgages (despite the lower available interest rates). We examine data at a state, segment and post code level, as well as geo-mapping which highlights the patchwork nature of the problem. Stress lurks in strange places, including some more “affluent” places!

Go to the Walk The World Universe at https://walktheworld.com.au/

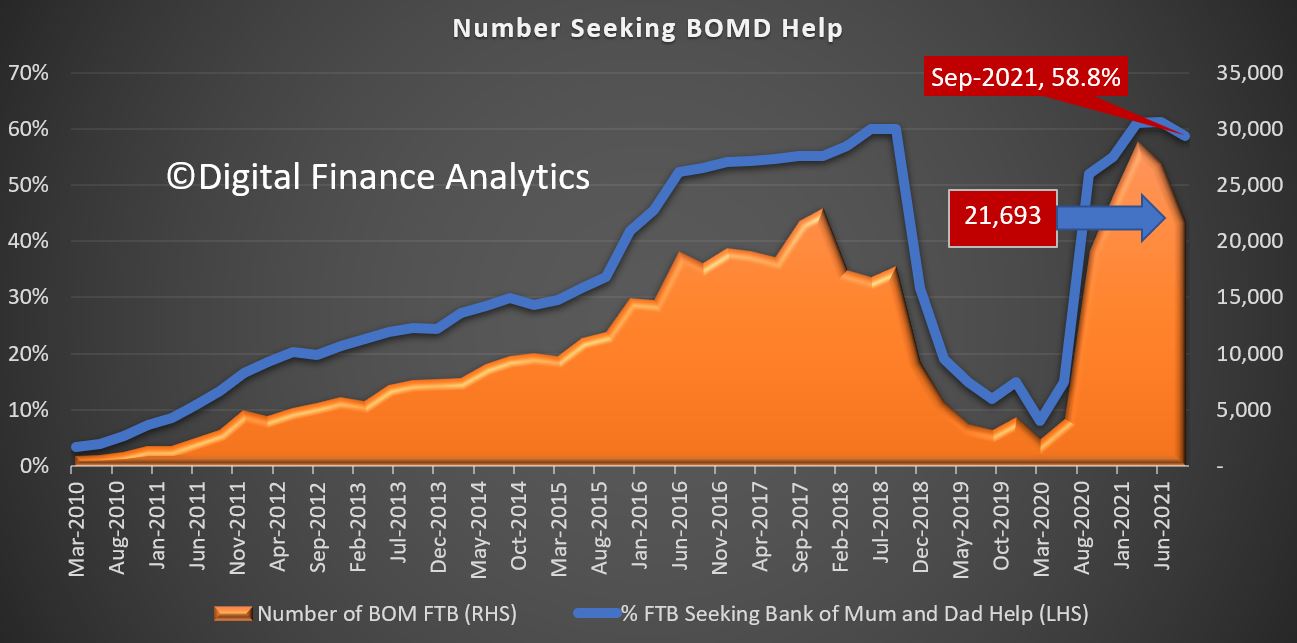

The Bank Of Mum And Dad Goes Through The Roof!

We look at the latest DFA survey data relating to how parents are helping their kids to enter the Australian property market. The totals are growing fast, despite the risks. But there are a number of questions to be asked, and trade-offs to be considered.

Not least the relationship between BOMD and Lenders Mortgage Insurance. https://digitalfinanceanalytics.com/blog/what-you-should-know-about-lmi/

Go to the Walk The World Universe at https://walktheworld.com.au/

Today’s post is brought to you by Ribbon Property Consultants.

If you are buying your home in Sydney’s contentious market, you do not need to stand alone. This is the time you need to have Edwin from Ribbon Property Consultants standing along side you.

Buying property, is both challenging and adversarial. The vendor has a professional on their side.

Emotions run high – price discovery and price transparency are hard to find – then there is the wasted time and financial investment you make.

Edwin understands your needs. So why not engage a licensed professional to stand alongside you. With RPC you know you have: experience, knowledge, and master negotiators, looking after your best interest.

Shoot Ribbon an email on info@ribbonproperty.com.au & use promo code: DFA-WTW/MARTIN to receive your 10% DISCOUNT OFFER.

FINAL REMINDER: DFA Live 8pm Sydney Tonight – Latest Household Surveys And Stress

Join us for a live Q&A as I discuss the latest results from our surveys and modelling. You can ask a question live. https://walktheworld.com.au/ .

If You’re Not Worried About Your Financial Position – Should You Be? With Steve Mickenbecker

I caught up with Steve Mickenbecker from Canstar to review some concerning recent research about household finances. We discussed strategies which may be considered to assist with cash-flow management, especially during these uncertain times.

Steve Mickenbecker is in Canstar’s Group Executive Team, bringing more than 30 years of experience in the Australian financial services industry. As a financial commentator for Canstar, Steve enjoys sharing his expertise across topics such as home loans, superannuation, insurance, mortgages, banking, credit cards, investment, budgeting, money management and more.

Go to the Walk The World Universe at https://walktheworld.com.au/

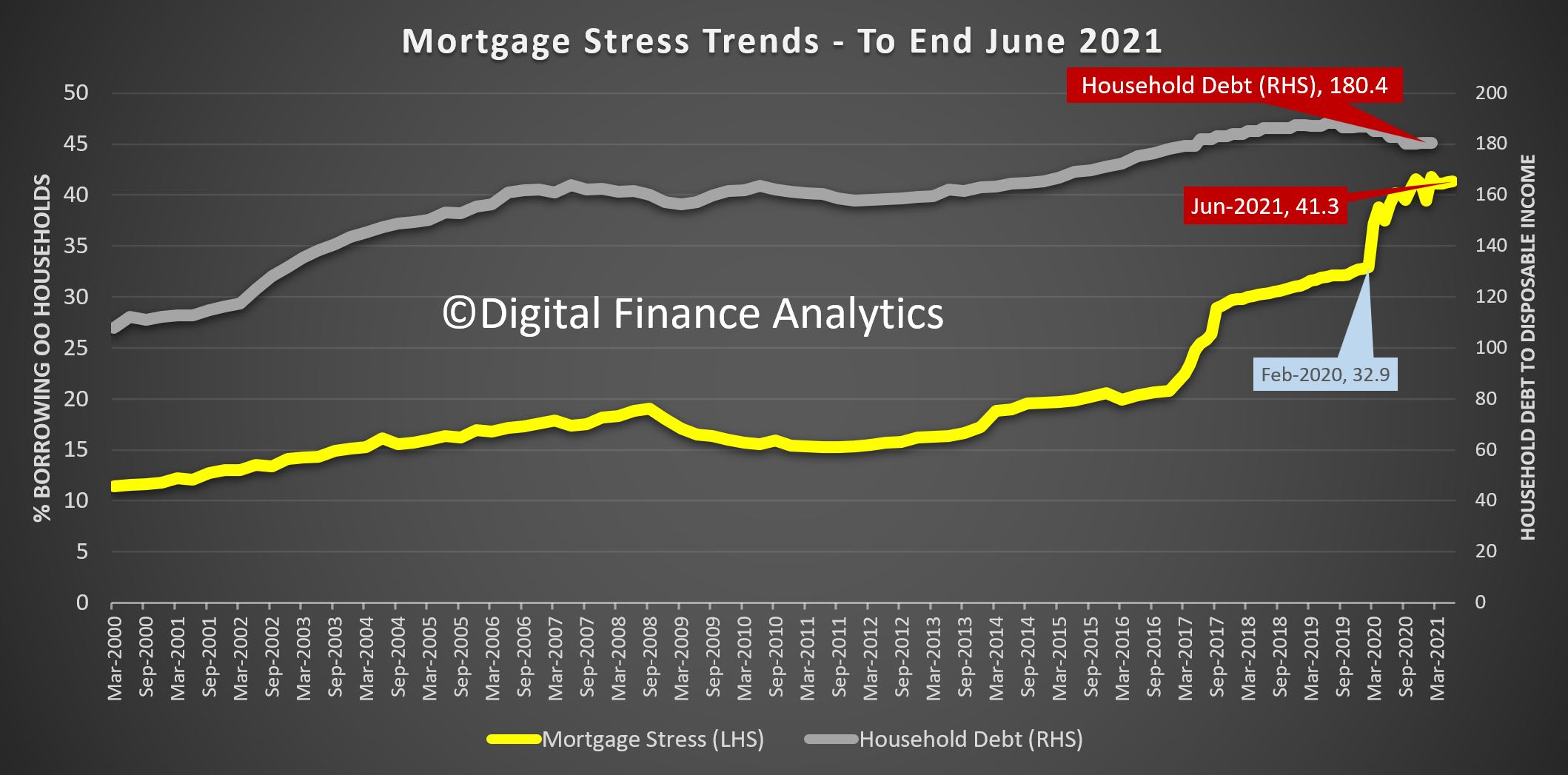

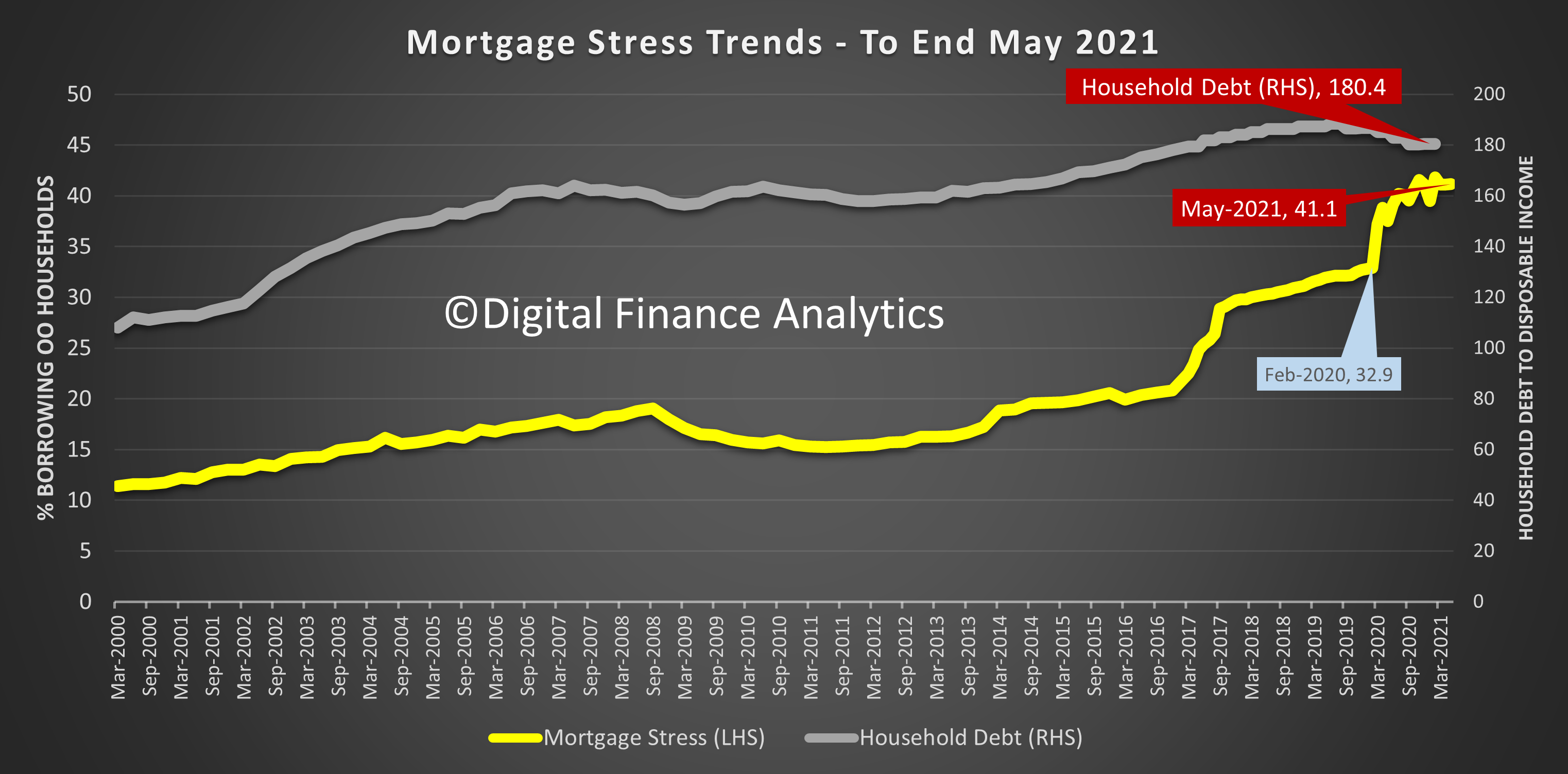

Financial Stress To June 2021

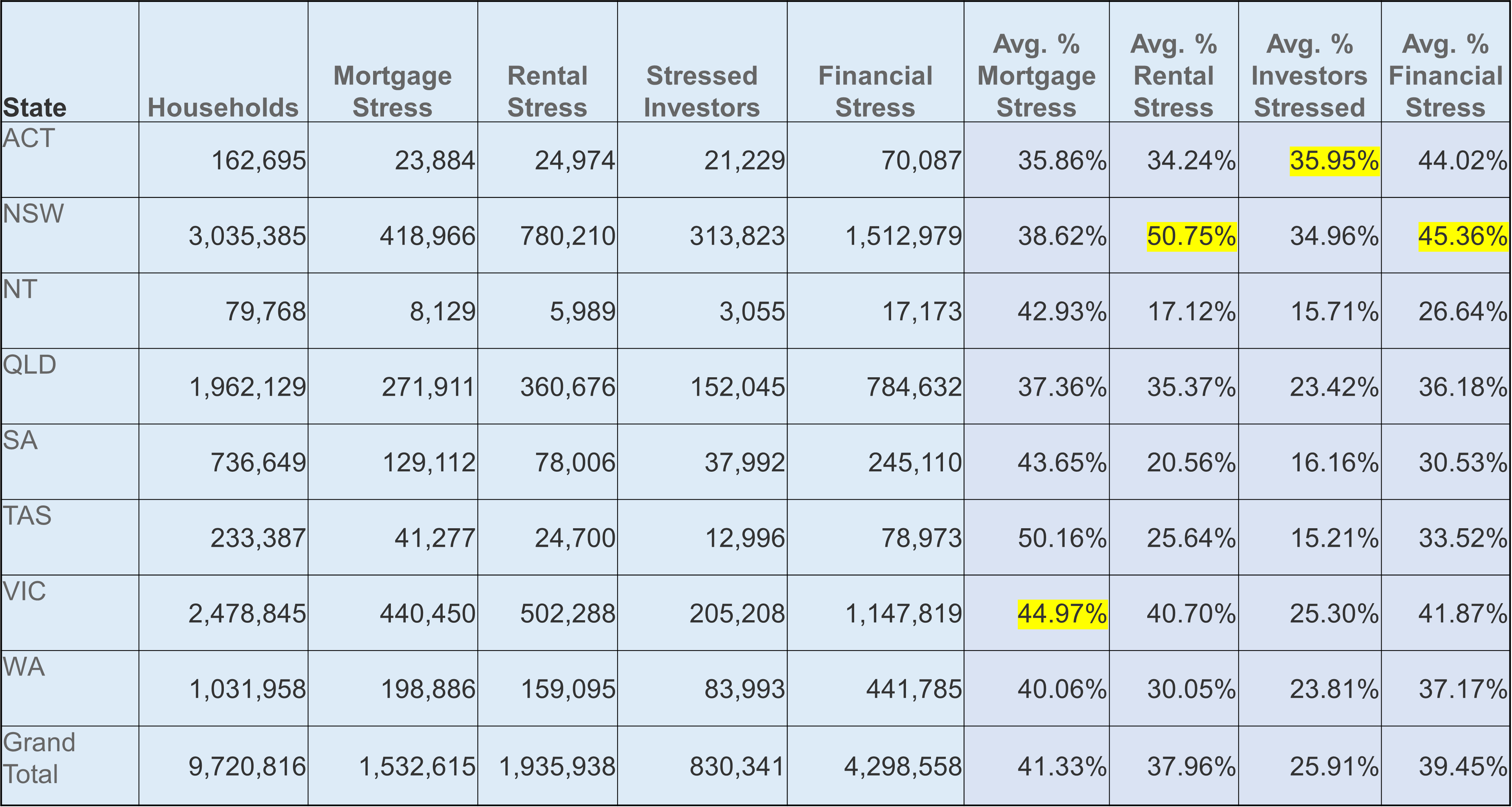

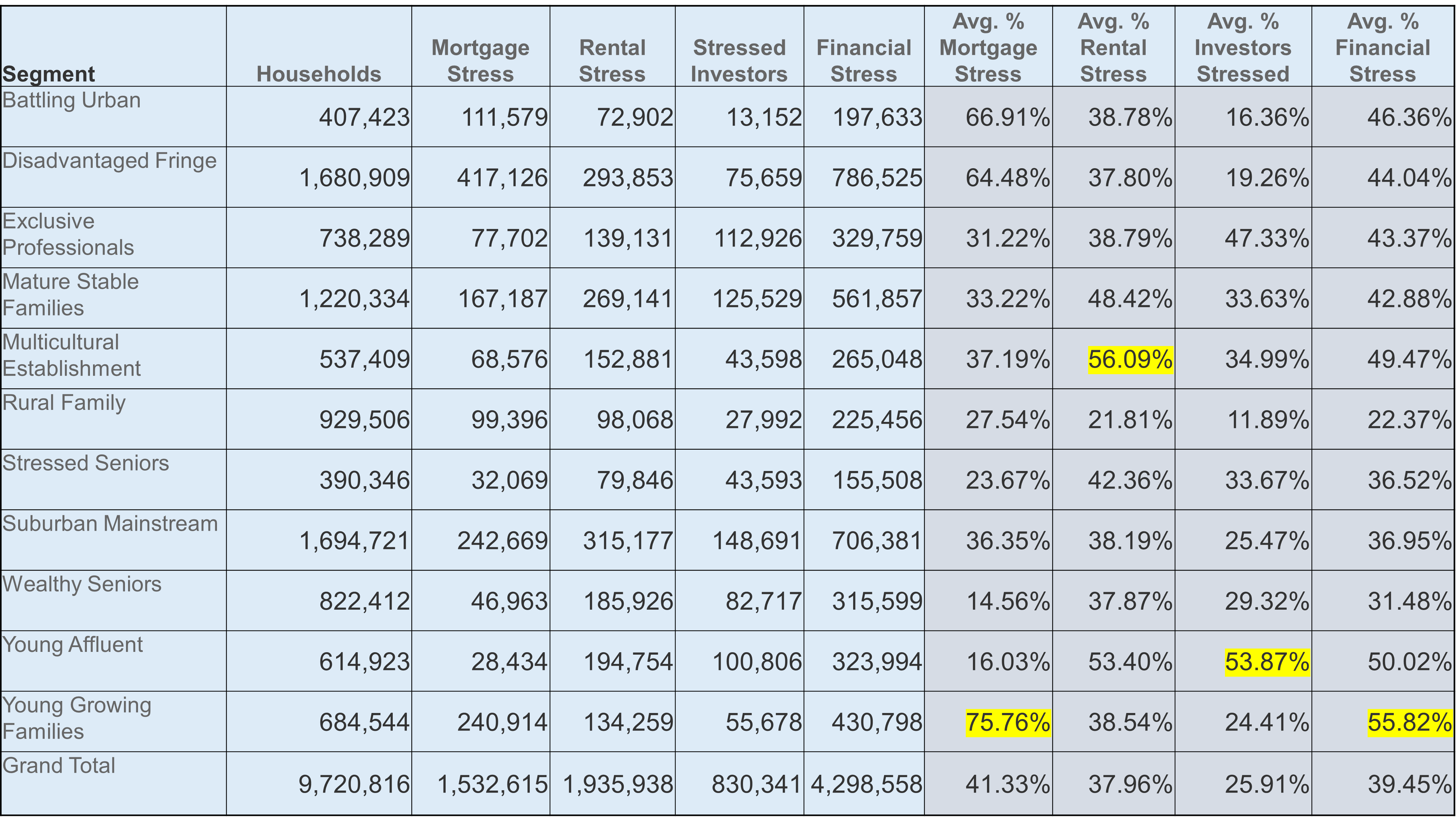

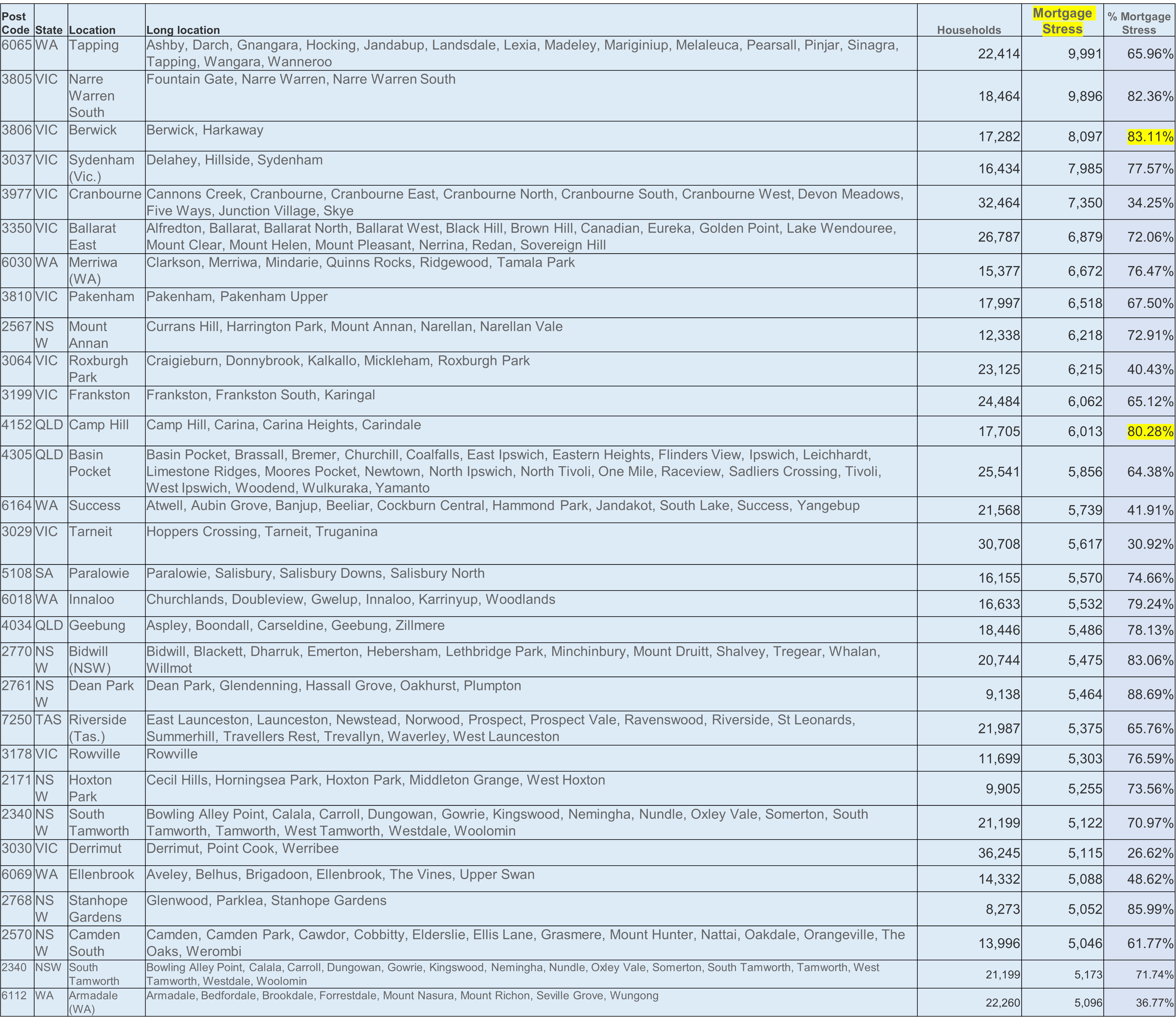

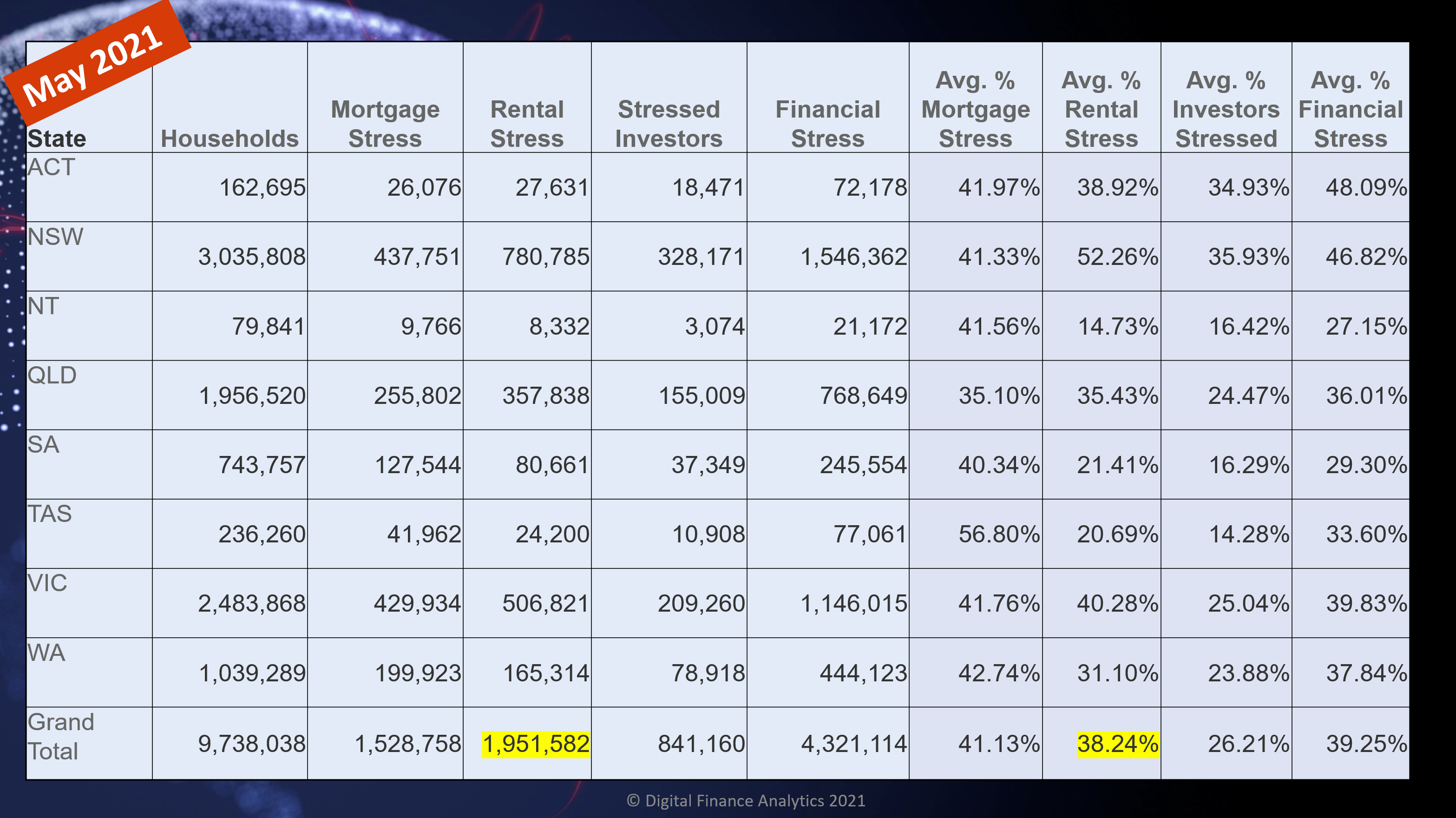

The latest data from our running household surveys reveal that overall levels of household financial stress – measured in available cash flow, continues to trouble many households. Mortgage stress stands at 41.33% of households or 1.53 million households.

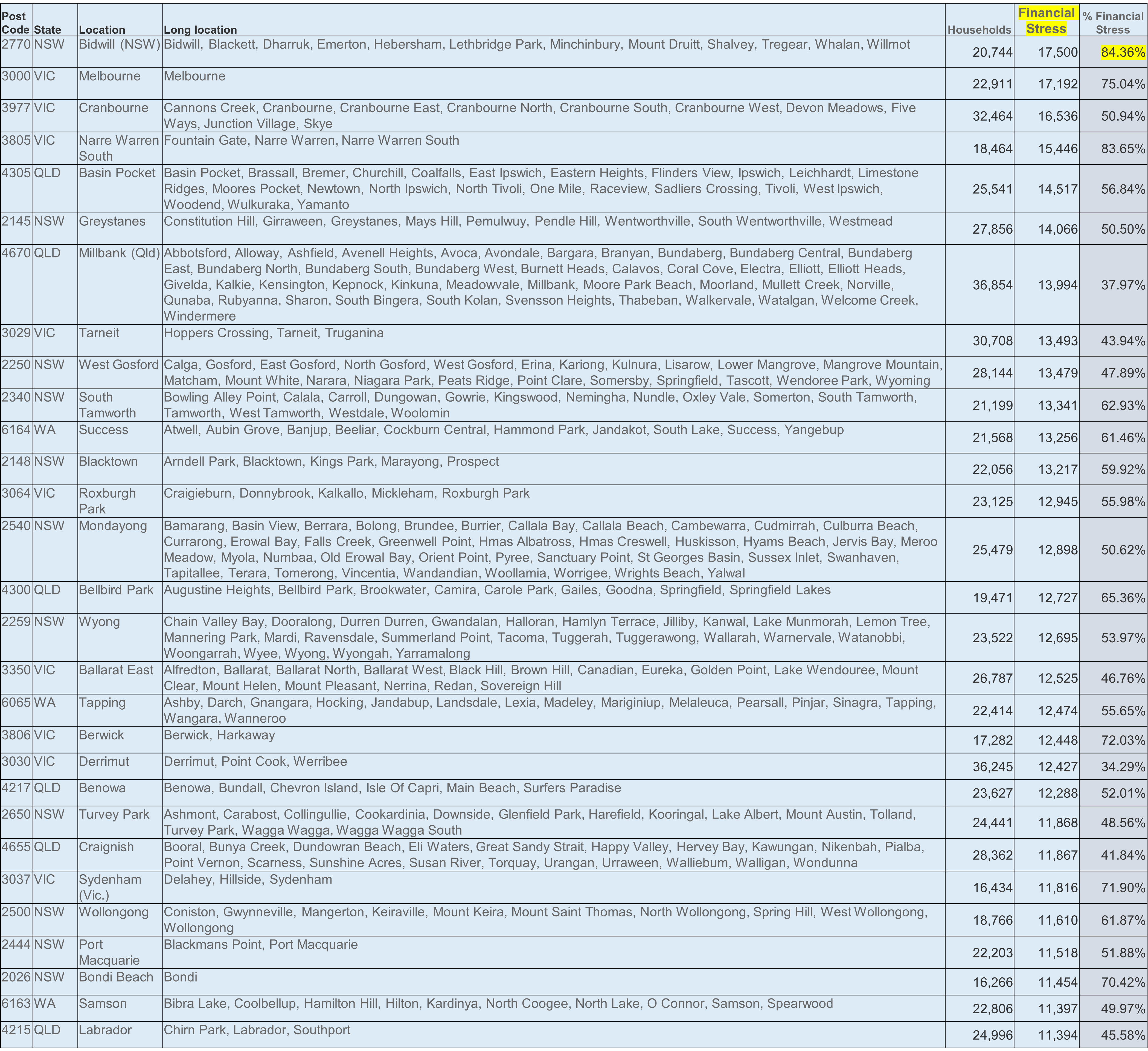

Overall financial stress (an aggregate of our stress metrics, weighted to all households) was highest at 45.4% in NSW, with 1.51 million households under pressure.

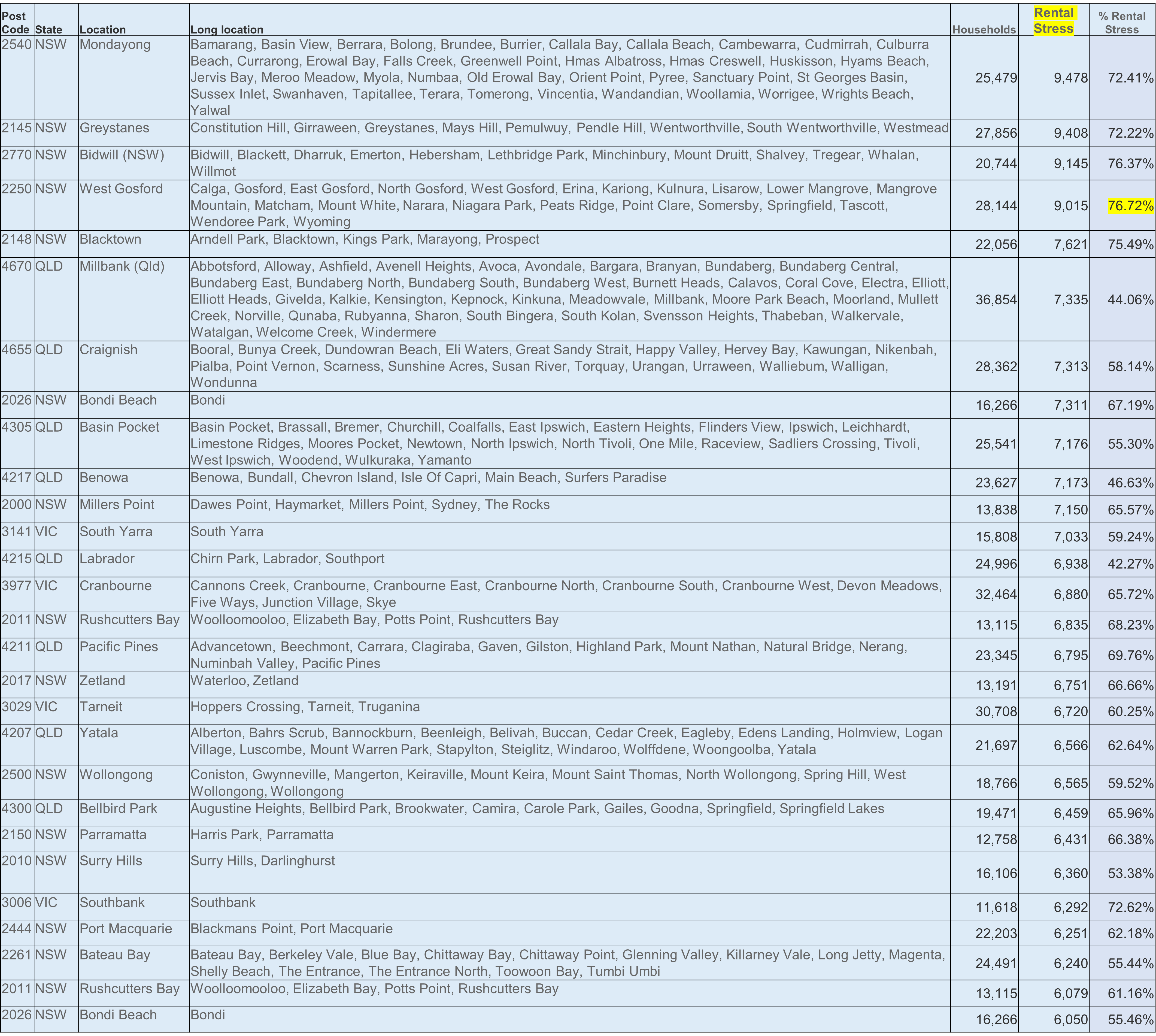

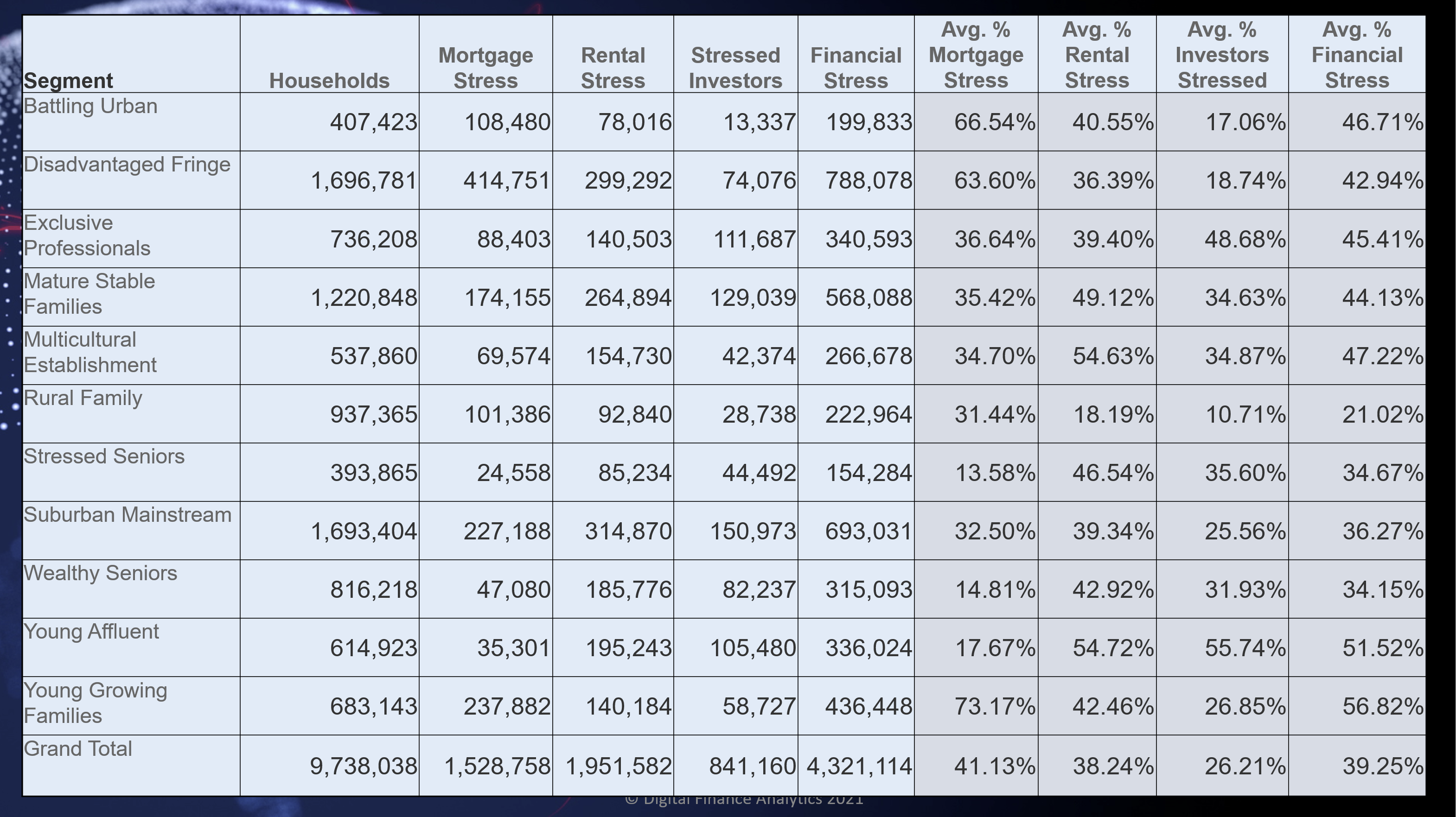

We continue to see many younger households who are highly leveraged into either buying their first home, or into property investment. Rental stress at 56.09% is highest among first generation Australians. Financial stress overall is highest among Young Growing Families.

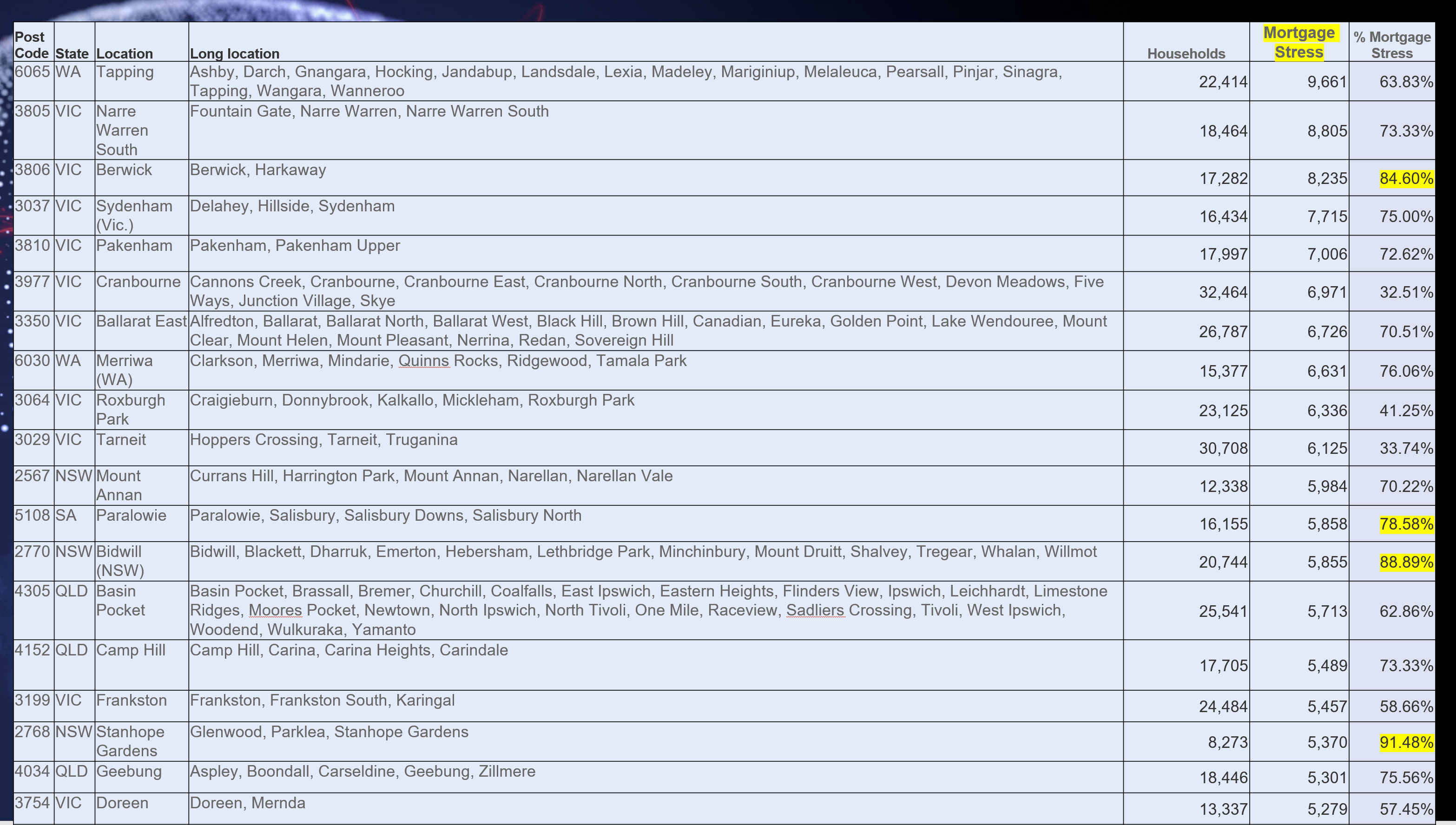

Top mortgage stressed post codes (by number of households stressed) are concentrated in the high growth corridors of Melbourne, as well as regional centres such as Ballarat.

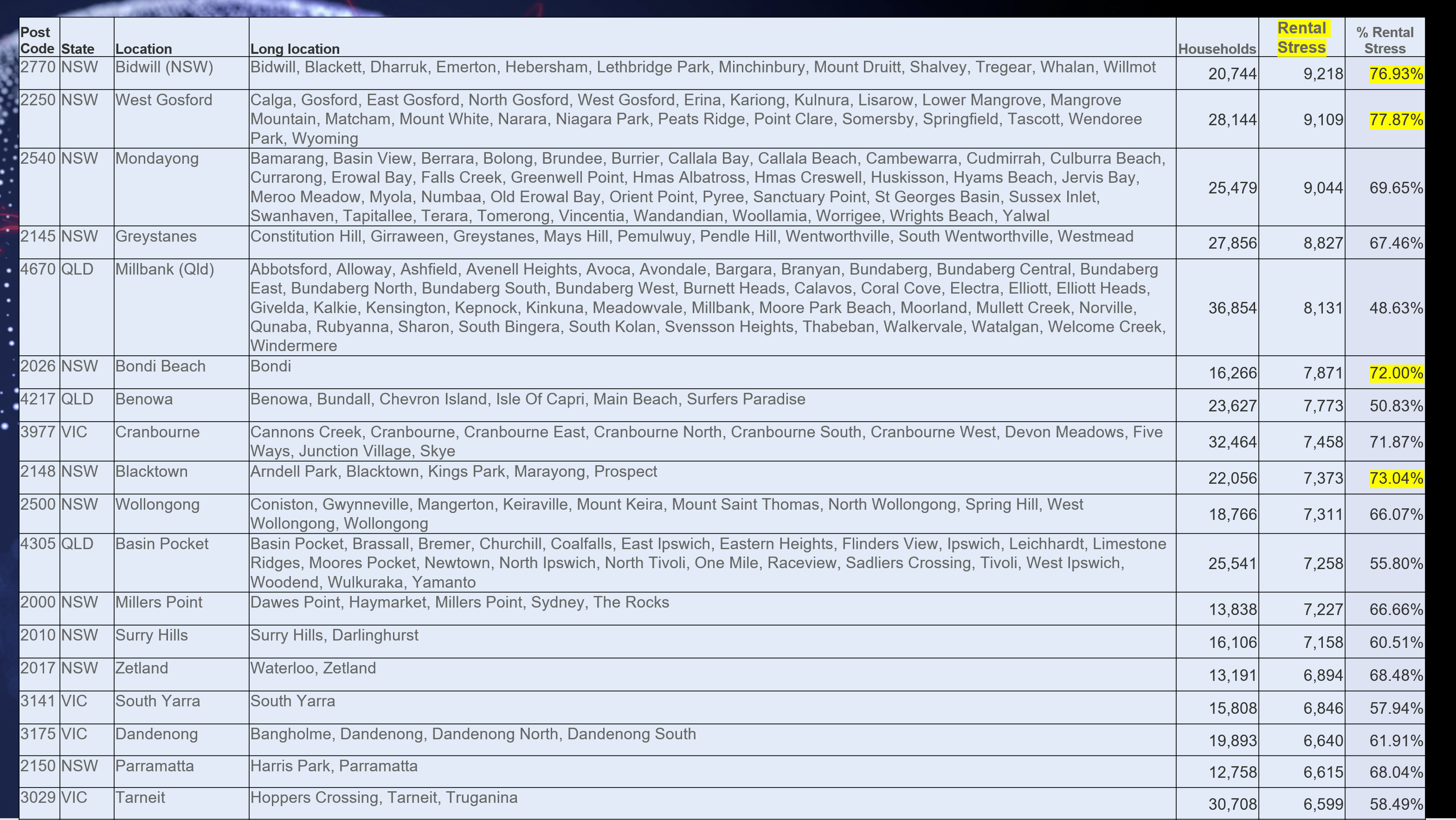

Rental stress is centred on areas of New South Wales, including in regional areas, including the South Coast and Central coast as well as high growth corridors, and some more central areas such as Bondi (2026) Central Sydney (2000) and Central Melbourne. Family formation is varied in different areas, from singles, through to larger family blocks.

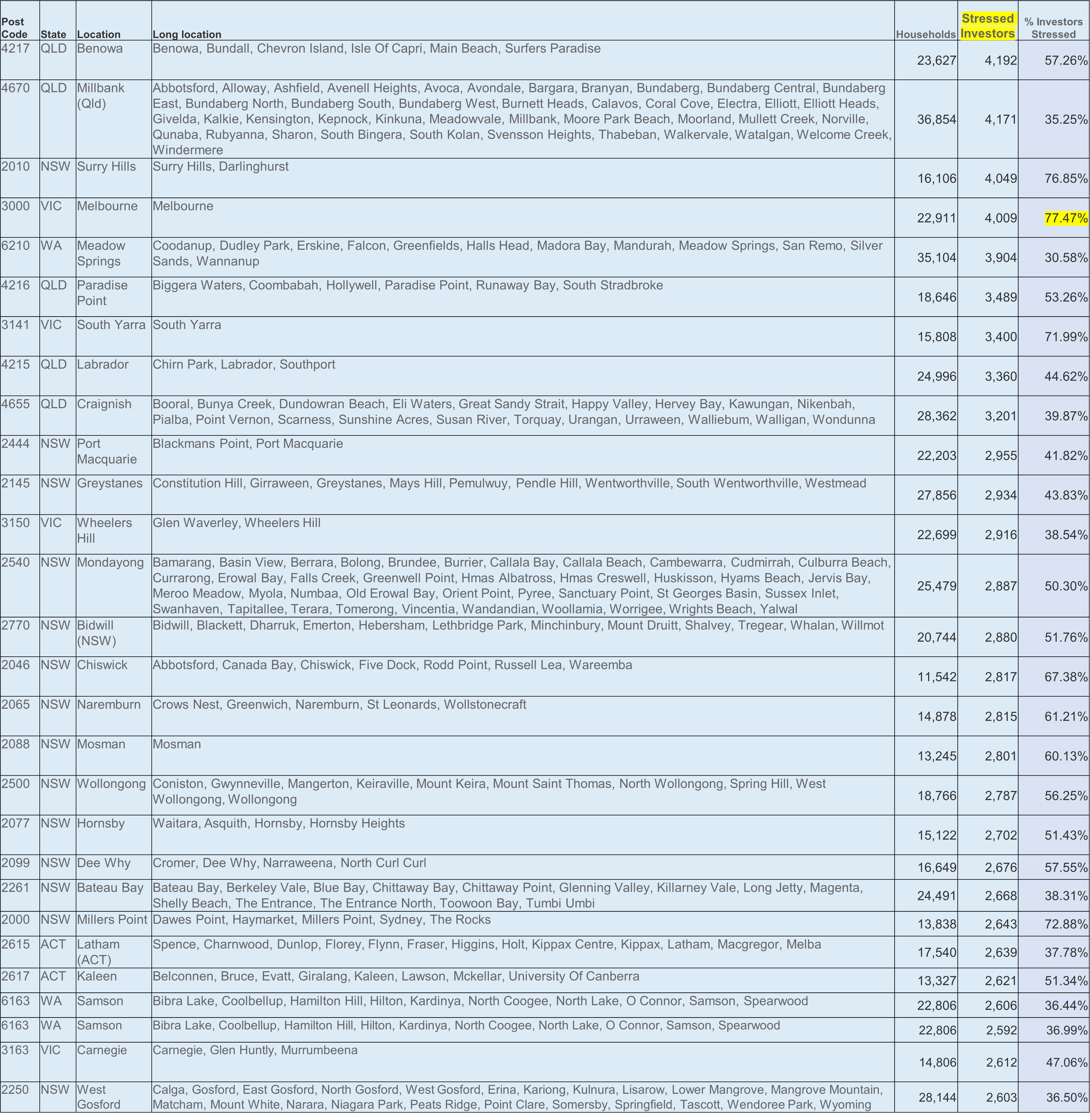

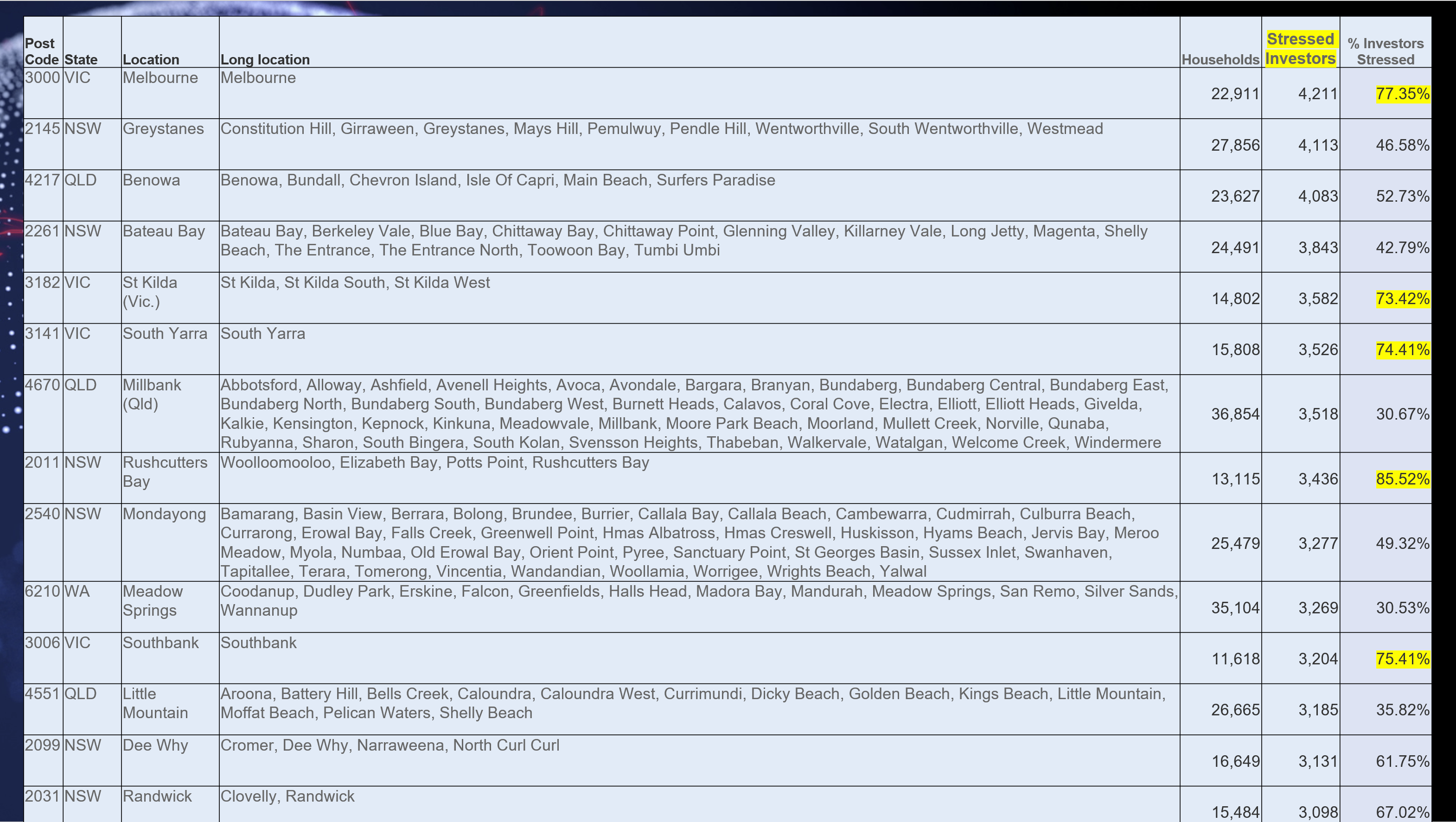

Investor stress (defined as property investors who are under water from a cash-flow perspective, or who cannot let their property, or who are trying to sell) ranges from areas in Queensland around Surfers Paradise (4217) and Bunderberg (4670). Surry Hills in Sydney and Central Melbourne are also pressure points – with many vacant units, either unlet, or deeply discounted.

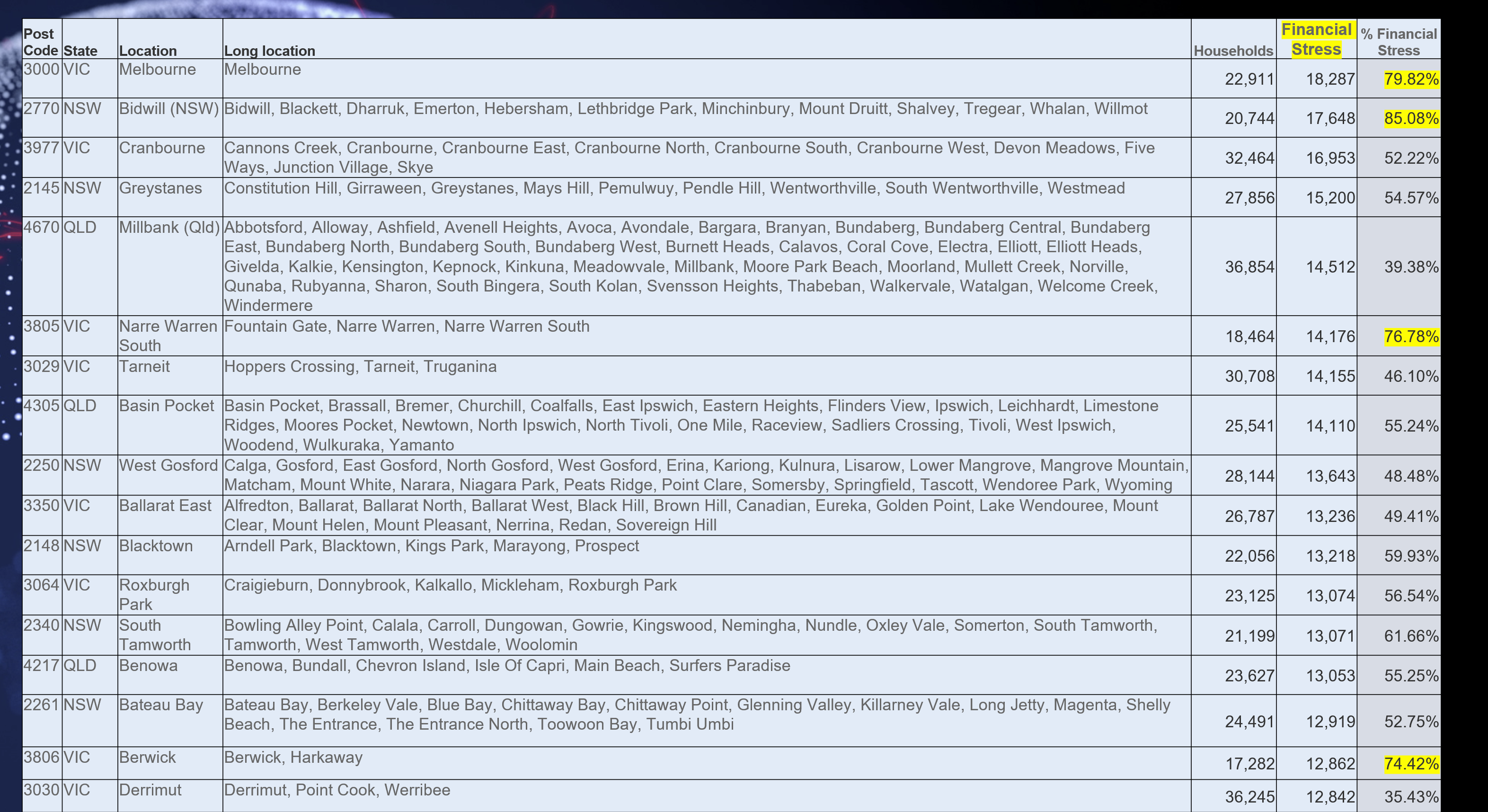

Overall financial stress registered most strongly in areas such as Mount Druitt (2770), central Melbourne (3000) and high growth suburbs including Cranbourne (3977) and Narre Warren (3805). But the stress patchwork is widespread across the country.

We discussed this data in our recent live show, including geo-mapping several areas to illustrate the findings.

The overall conclusion remains that the financial settings in Australia, with raging home prices, and high debt, against an uncertain economic outlook and made worse by recent lock-downs – is putting pressure on many households. This belies the “official narrative” the the recovery is booming.

We continue to see many households trying to get by using more credit (including Buy Now Pay Later) and draining savings for every day expenses. Many still do not maintain cash flow records, so are not clear about their real exposures.

Importantly, those with mortgage commitments who continue to struggle would do well to speak to their bank. Given continued flat income, the virus conditions in some suburbs, and other factors, we do not expect this to change ahead. Many are hoping for a magic bullet but in the current environment this is unlikely.

FINAL REMINDER: DFA Live 8pm Sydney Tonight: Latest Household Stress And Scenarios

Join me tonight as we dissect the latest RBA statement and examine the real-life financial footprint of Australian households. You can ask a question live, and I will have the post code data base on line, as well as our geo-mapping series.

Why Household Financial Stress Remains High

The latest data from our household surveys for May revealed little change in mortgage stress among households – still at around 41%, but there was a shocking rise in rental stress as the JobSeeker and JobKeeper supports were withdrawn, and the random lock-downs continue.

Even Property “experts” accept that affordability has deteriorated recently, as house prices rocket higher in many suburbs, although of course real interest rates are very low, for now, if rising ahead.

Our approach to measuring stress is unique in that we examine household cash flow – money in and money out. Given that many households saved hard last year though the heights of COVID, it is not surprising to see many now draining down those savings, by spending more. This means that their cash flow will in net terms be negative for now, and so will register as stressed. That said, if spending continues unabated financial difficulties will eventuate.

In addition we continue to see more households reaching for credit (from Buy Now Pay Later, to Pay Day loans) as well as equity release from property. In fact the latest hikes in perceived values has led to a run of refinancing, to try and pay down debt, or to provide funds to offspring for property purchase via the Bank of Mum and Dad. Again these one-off moves can adversely impact household stress measures in our methodology.

And we also note that many prefer not to accept the truth that some households are not home and clear in terms of their finances, given the uncertain part-time work, multiple jobs and zero hours contracts which many are on. But we continue to analyze households in net cash flow terms. If more funds drain away, compared with income, they are classified as stressed.

Across our segments we continue to see quite different dynamics emerging, with many younger households (often first time buyers) impacted, alongside the high growth corridors containing many first generation Australians, as well as some more affluent groups. Financial Stress takes no prisoners.

The mortgage stress counts are highest in high growth corridors in WA and VIC – where in some cases more than 80% of households in the area have cash flow issues.

Rental stress is more strongly registered in NSW and QLD, with Western Sydney and the Central Coast and Bundaberg in the top 10.

Property investors are having difficulty in Melbourne 3000, thanks to the lack of students and ongoing lock-downs. A number of VIC suburbs are impacted thanks to high vacancy rates, negative net yields and falling apartment values.

Overall financial stress, our aggregate measure reveals that Melbourne 3000 has the highest stress levels. That is followed by a number of the high growth corridors.

The continued pressure on households from low income growth, and rising living costs will persist, while the risks of interest rate rises grow with the competition of the Term Funding Facility at the end of June.

Households continue to wait for a magic bullet to solve their financial flow issues, and while some can draw on savings and equity, or reach for more credit, unless spending patterns are understood (half have no budgets), we think these trends will continue to bubble away.

Of course, financial stress is not the same a mortgage default, but those with cash flow issues are more likely later to end up having to sell their home, unless remedial action is taken.

Households in financial stress should certainly speak to their lender, prioritise spending, and be cautious about further loan commitments. There is no income growth “get out of jail card” for now.