Today we start a short series which will review the property market in 2016, and then look forward to 2017. We will start by looking at demand for property, then look at property and funding supply, before examining the risk elements in the market for both property owners, lenders and the broader economy.

Remember that there is more than six trillion dollars invested in residential property in Australia, three times as much as in the whole superannuation system, and close to a third of households rely on income from property, either directly or indirectly, (from rents, or jobs in the sector across construction, maintenance and management), to say nothing of the capital two thirds of Australians are sitting on thanks to strong recent price rises. So what happens to property really matters.

Property Demand

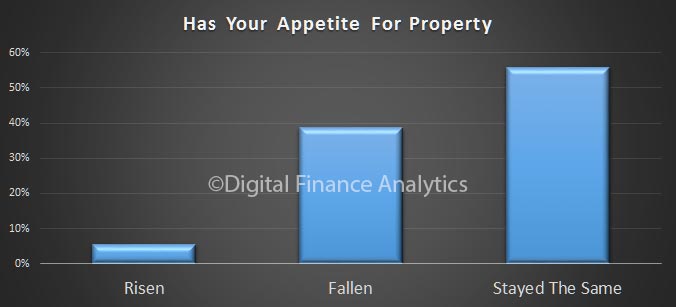

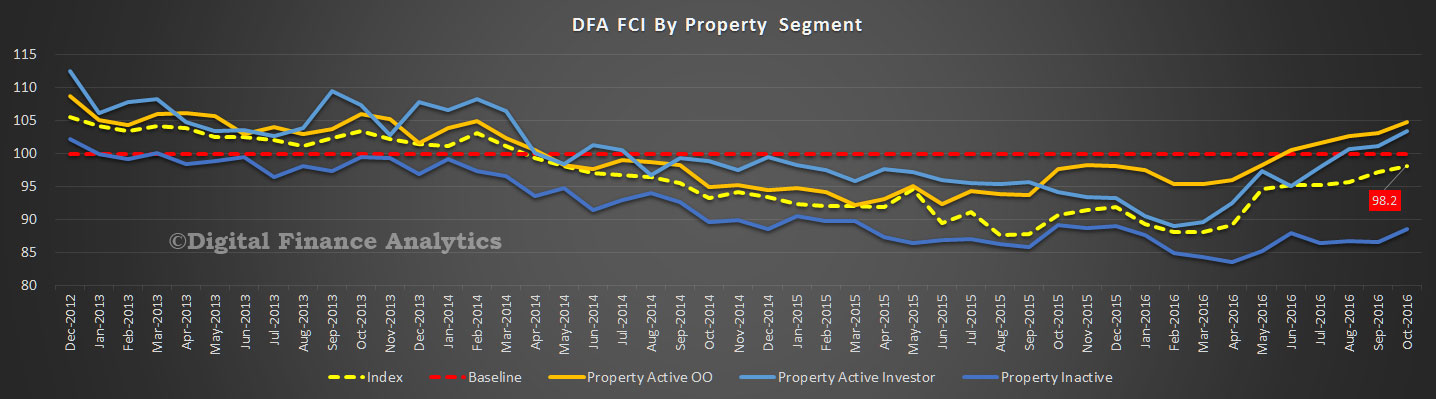

We start with demand for property. The latest data from our household surveys shows that demand for property is very strong. Two thirds of households have interests in property, and about half of these have a mortgage. Owner occupied home owners are a little more sanguine now, but property investors, after a wobble earlier in the year, are still strongly in the market. In addition, there is still demand from overseas investors, and migrants. Overall demand is now stronger than at the start of the year. This is reflected in continued high auction clearance rates, especially down the east coast.

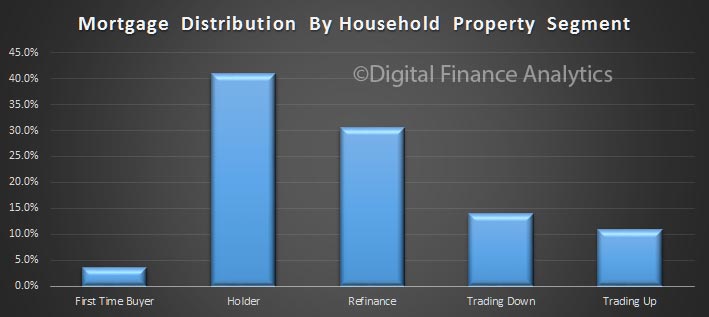

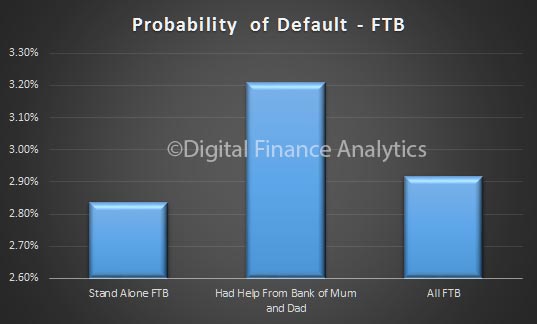

First time buyers are finding it difficult to compete with cashed up investors, and with incomes static and tighter underwriting standards, it is harder than ever for them to enter the market. Down traders – people looking to sell and release capital – are active, and are in the market for smaller homes, and investment property. Households seeking to trade up are also active, driven by the expectation of ongoing capital gains. Investors are attracted by the generous tax breaks, including negative gearing and capital gains. This despite rental incomes falling again, and the fact that about half of investors are underwater on a cash-flow basis, though bolstered by continued capital gains.

So overall demand is strong, and it has not yet been impacted by the rising mortgage interest rate bias that we have seen in the past couple of months.

Property Supply

Turning to property supply, there have been a significant surge in new building, mainly in and close to the central business districts in Melbourne, Brisbane and to some extend in Sydney, though here new building is more widely spread. Well over two hundred thousand new properties are coming on stream and more than half of these will be high-rise apartments. That said forward approvals are slipping now, so we may have passed “peak build” in the current cycle.

We are also seeing significant subdivision of existing residential land, and a rise in new house construction as well. The average plot size continues to fall, but we still place larger buildings on these smaller plots.

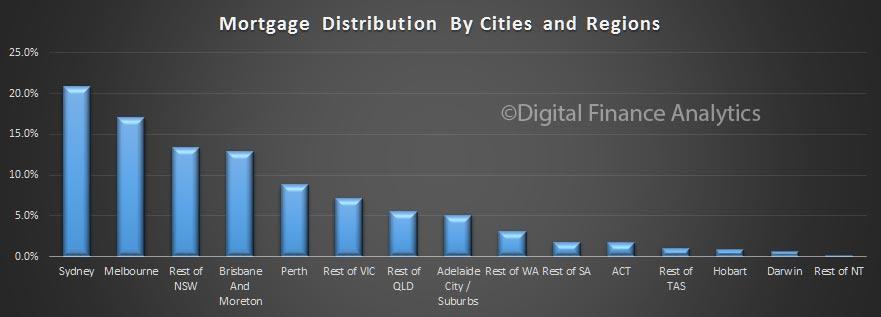

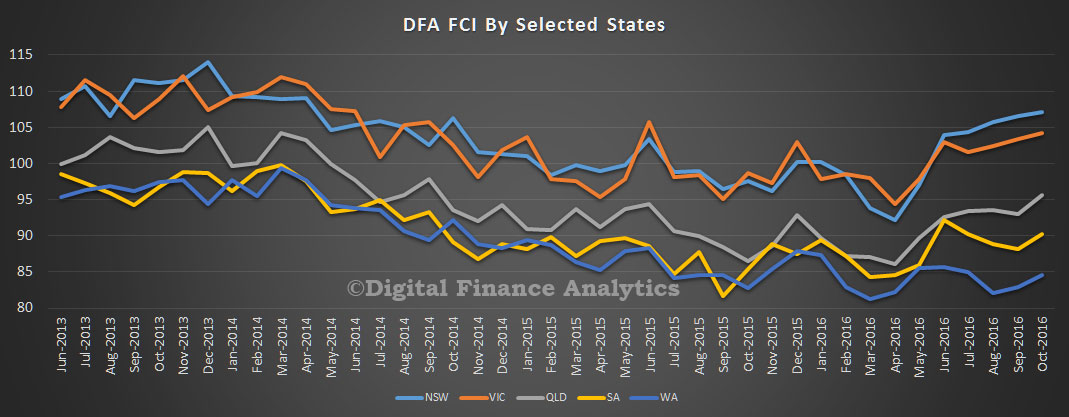

In Sydney and Melbourne, the amount of housing on the market is not meeting demand, though this is not true in some other markets – for example in areas of Western Australia and Queensland, especially in the mining belts. The Reserve Bank is concerned about the impact of potential oversupply in apartments in the main centres.

Finance Supply

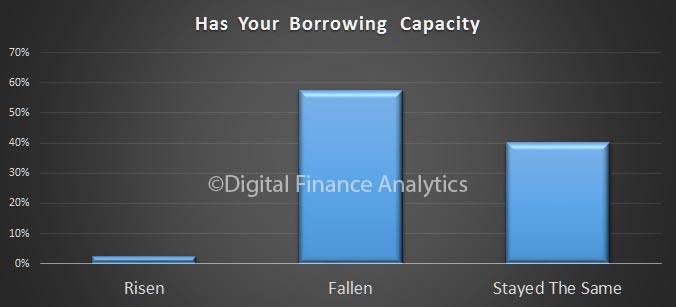

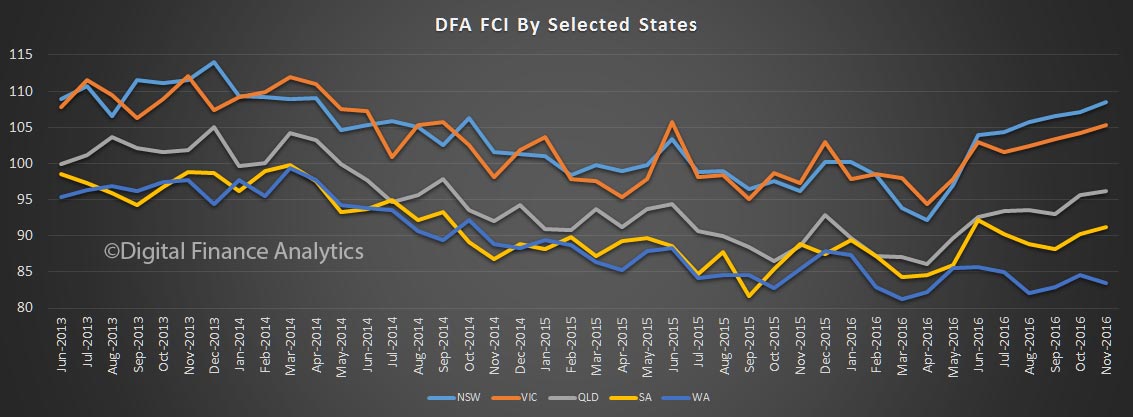

Turning to finance supply, Households can still get mortgage finance, but in recent times there has been a significant tightening of underwriting standards. Interest rate buffers are now higher than they were, income flows are being examined more critically, and lenders who are making interest only loans, which account for about one third of transactions, are looking for greater precision as to how the capital will be repaid later. Foreign investors are finding it harder to get a loan from the major lenders, although a number of smaller banks, and other non-traditional lenders are more than willing to do a deal. In addition, foreign income is now under greater scrutiny, following a number of recent frauds.

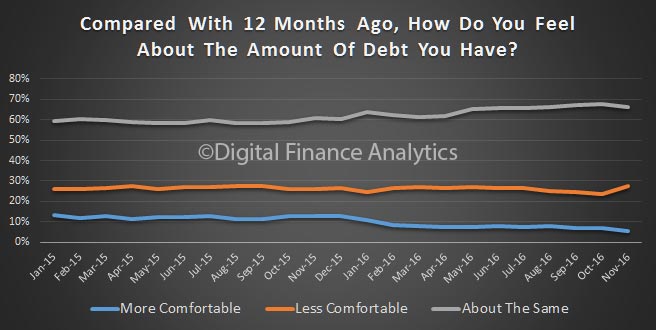

Overall credit growth is a little slower than a year ago, but at above 6% is still well above inflation and income growth. Within the mix, recently, investment mortgages have been growing faster than owner occupied loans. Household debt has reached an all-time high, thanks mortgage growth, with the ratio at 186 percent of debts to disposable incomes, one of the highest ratios in the world. Low interest rates mean that currently the servicing burden is not currently too bad, but this would change quickly if rates were to rise, thanks to excessive leverage. Household savings ratios are falling.

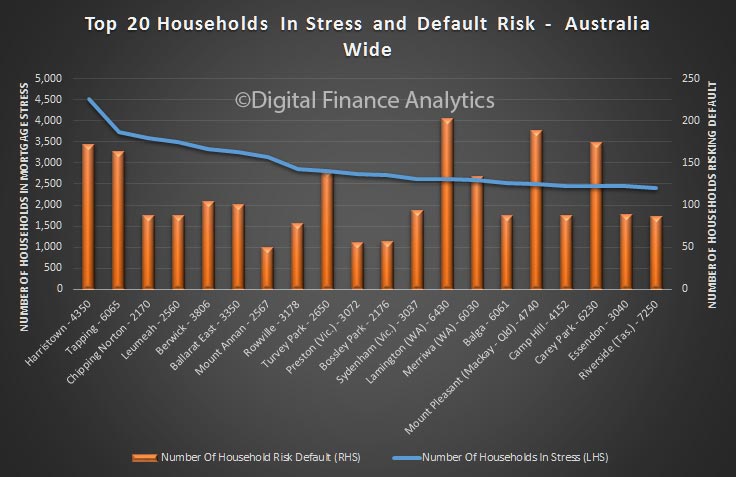

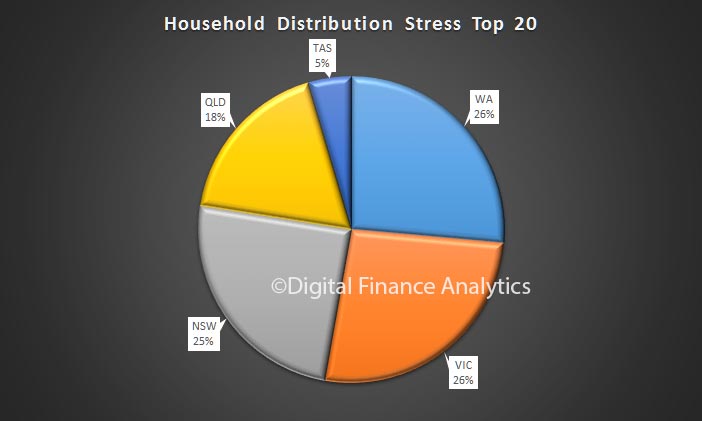

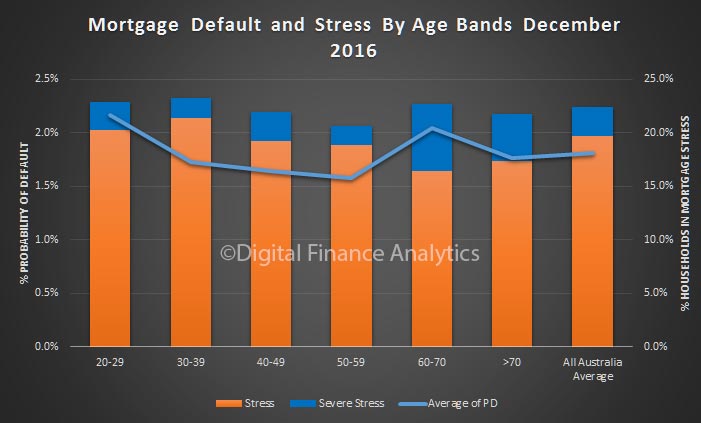

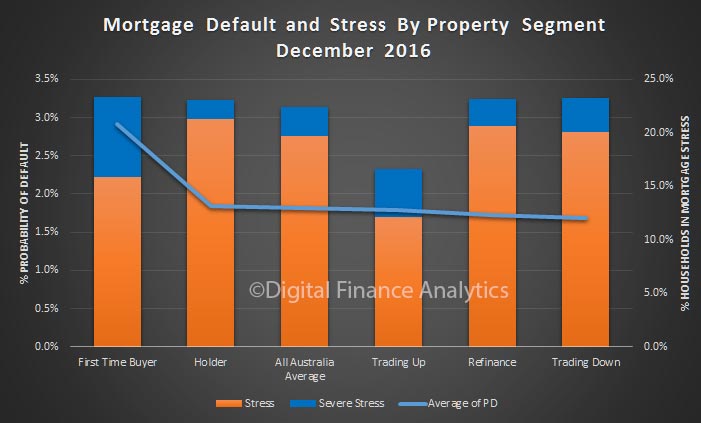

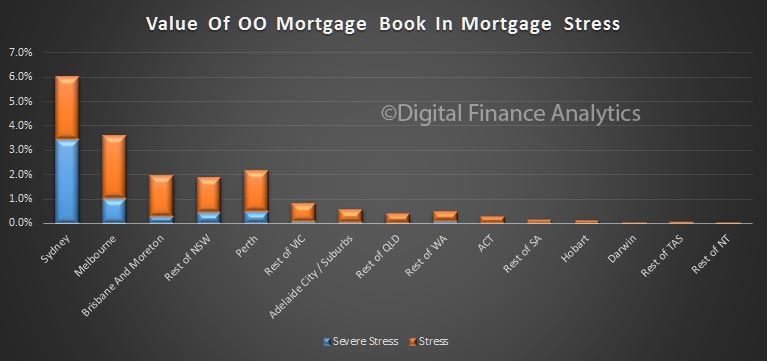

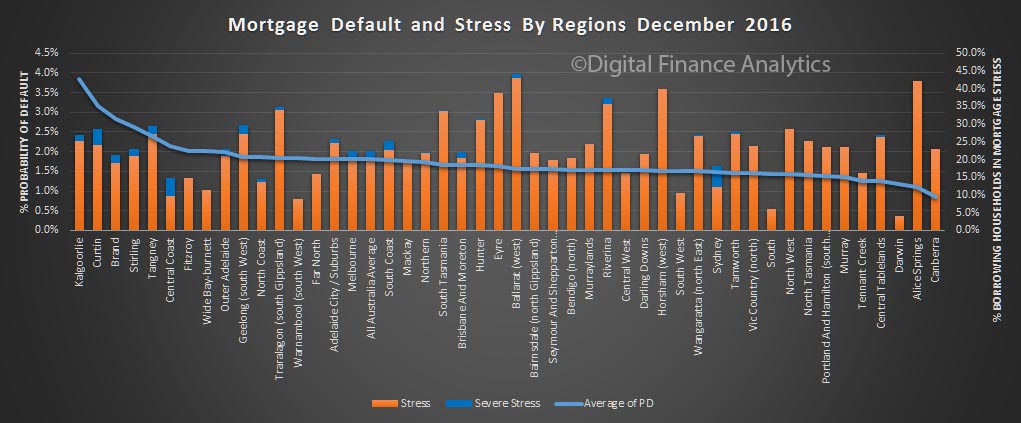

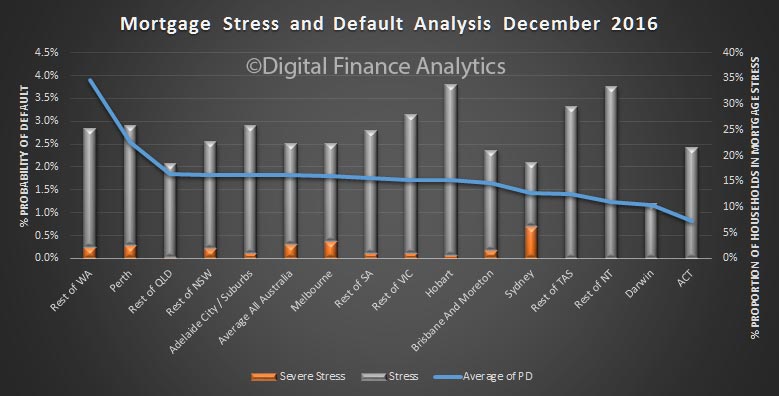

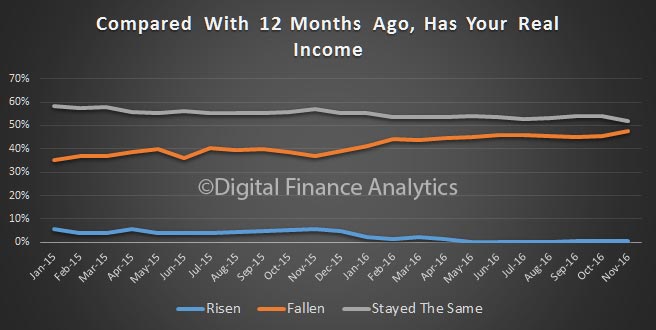

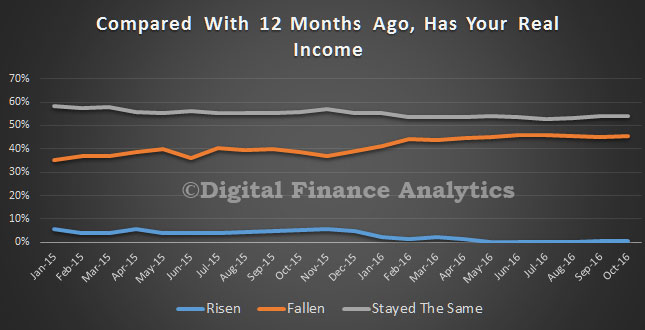

Whilst unemployment rates remain controlled, at 5.6%, the main issue for many households is that real incomes are just not rising, and as a result, some are finding it harder to make their mortgage repayments on time. At the moment mortgage delinquency is rising, just a little, but faster in areas of WA and QLD.

Recently the Trump Effect has led to a rise in US bond yields, and this has had a knock-on effect in the capital markets, lifting the rates banks must pay for capital. As a result, we have seen the yield curve move up, and banks have been lifting their mortgage rates – somewhat selectively so far – with investors taking the brunt, but the trend is widening. The recent RBA cash rate cuts are being offset by these rises, and we think it unlikely the RBA will lower rates again, so mortgage rates will continue to rise. We will discuss the possible impact in 2017 later.

Summary

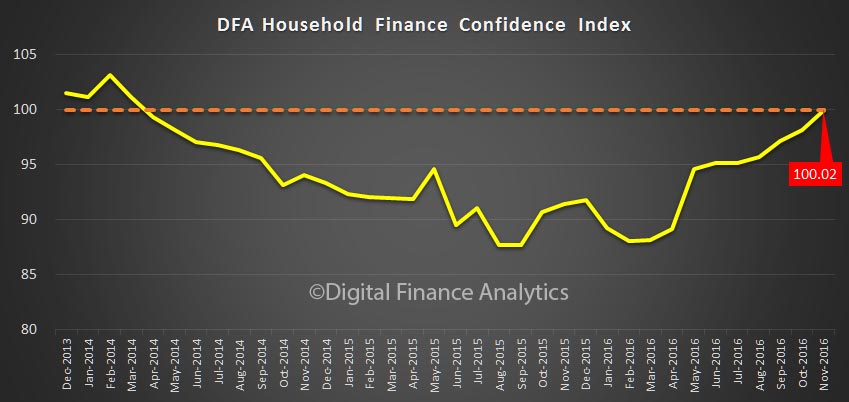

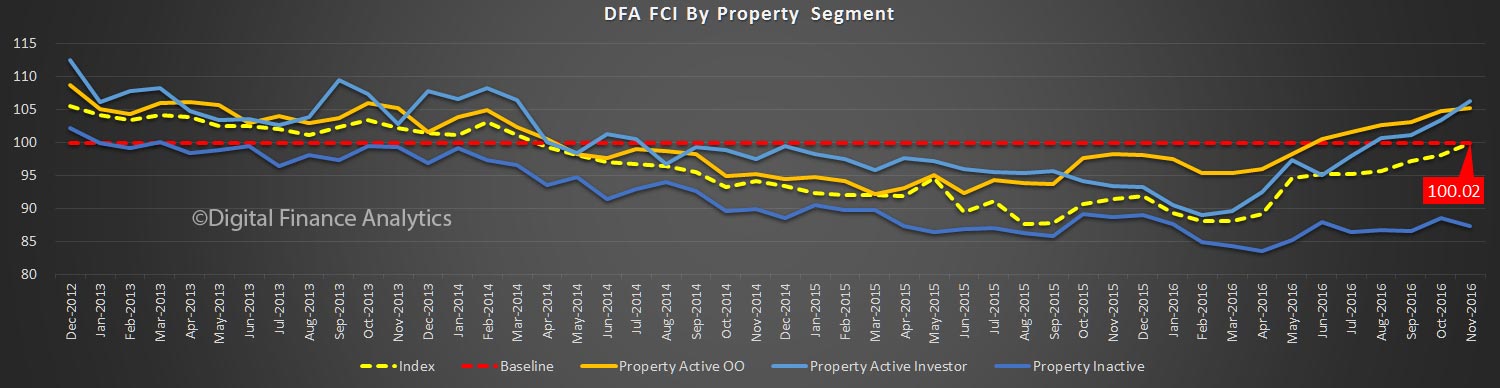

So we can say that 2016 has been a positive year for those in the market, with sizable capital gains for many, significant transaction momentum and construction, and in line with the RBA’s intention part of the re-balancing of the economy away from mining construction. The cost has been, first higher home prices, as well as larger pools of debt and more households excluded from the market. Banks have 62% of their assets in residential property, a high, and are more exposed to the sector than ever, despite holding more capital than they did. We believe regulators should be doing more, but only reluctantly, and lately, are they coming to the party.

Next time we will look at prospects for 2017.