Digital Finance Analytics has released the latest results from our rolling 52,000 household surveys, which examines household financial flow stress. The headline is that more households are feeling the pinch, thanks to higher costs of goods and services, fuel, child care and healthcare costs.

We examine the net cash flows of our households, and if they are consistently spending more than net income, we classify them as “stressed”. This is a better measure of financial health than a set percentage of income going on a mortgage or rental payment – often cited as 30% or more. This broad brush approach tells us very little.

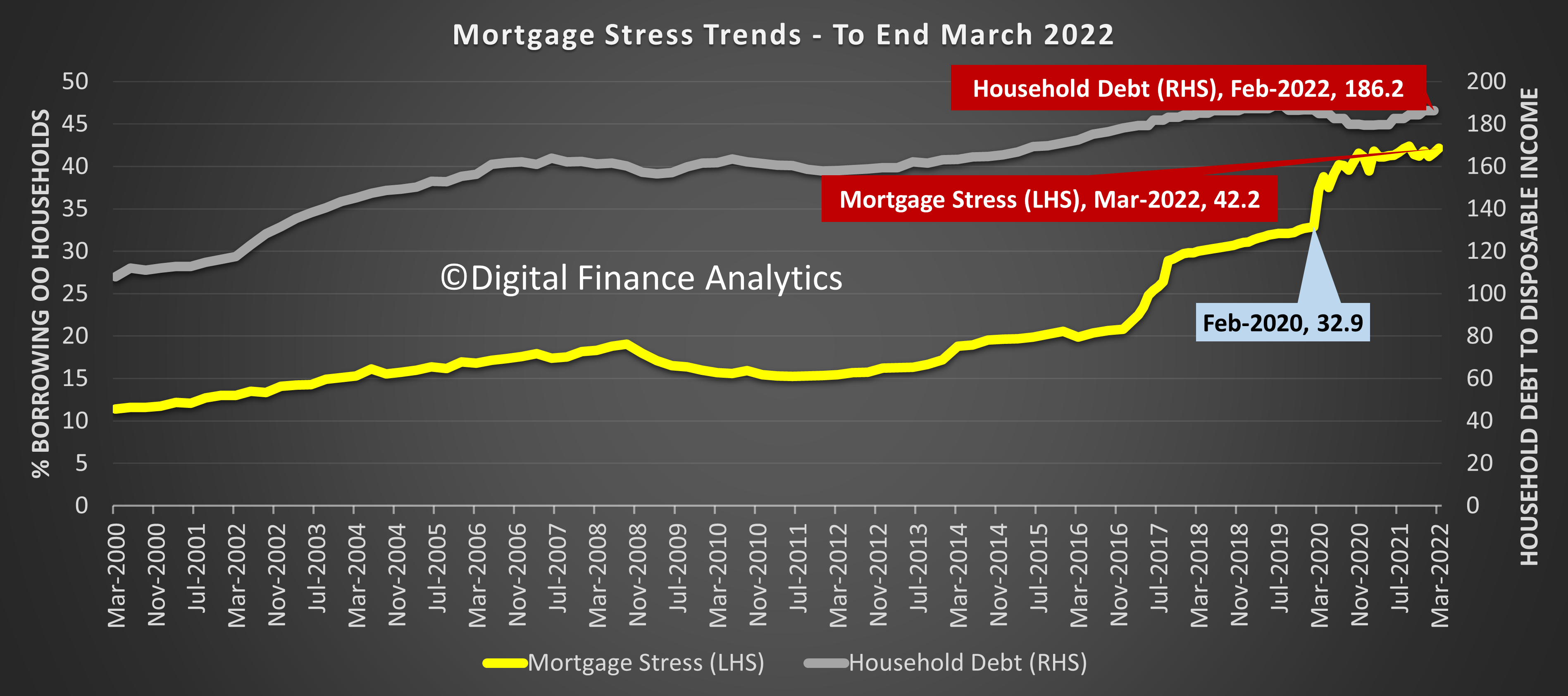

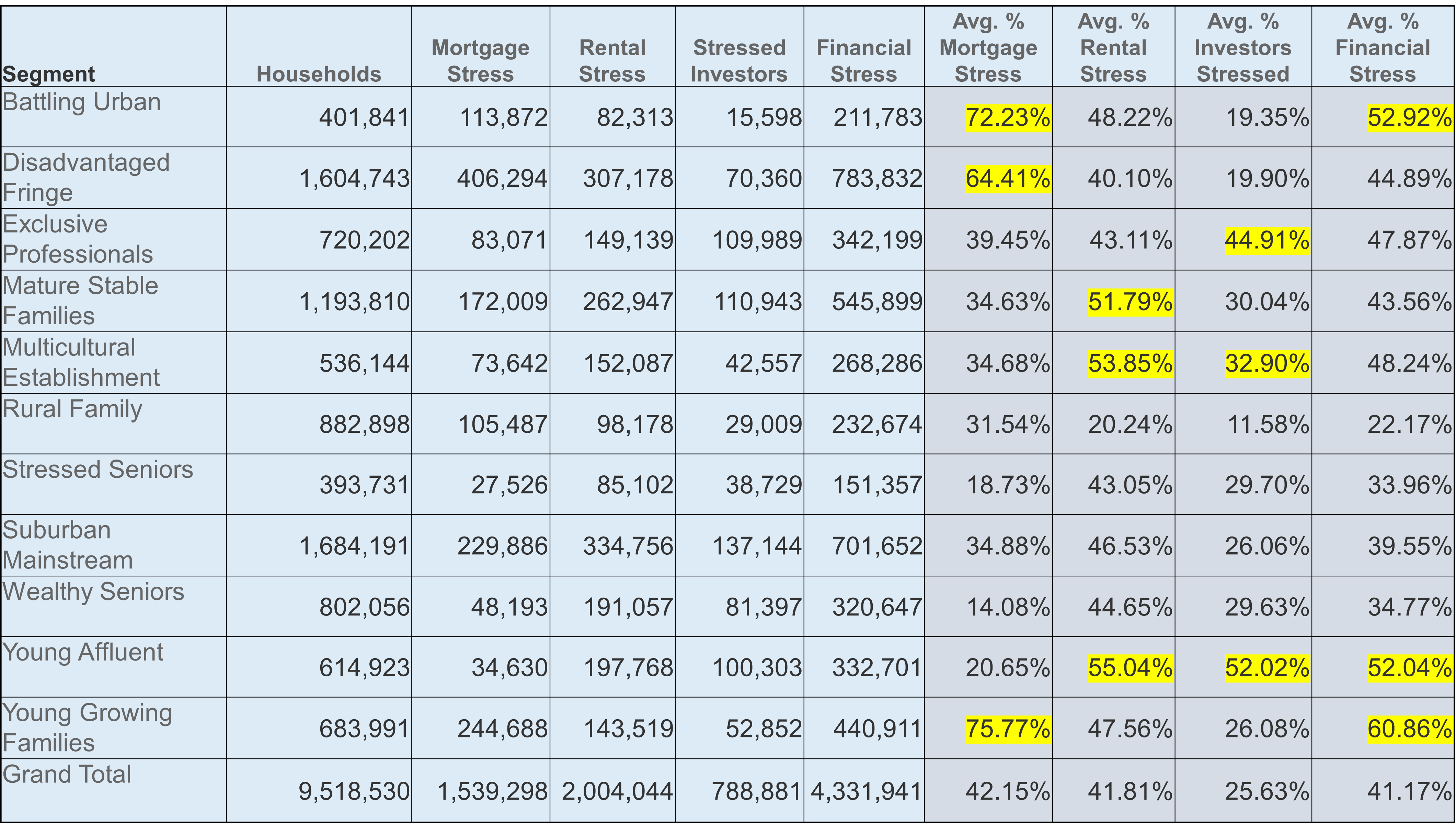

Overall 42.2% of mortgaged households are in financial flow stress, a trend exacerbated by the larger mortgages held by recent borrowers, as illustrated by the RBA’s rising debt to income ratio. This degree of stress is concerning because mortgage interest rates are likely going to rise quite fast, in line with RBA cash rate expectations.

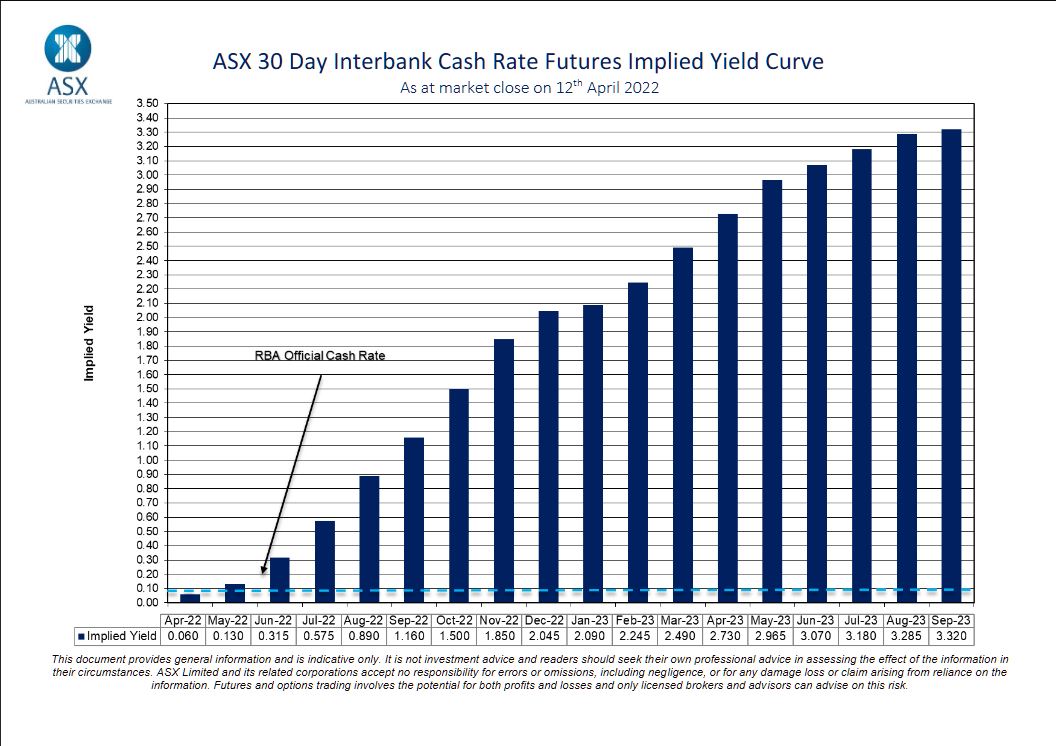

Indeed, the latest ASX market indicator suggests rates could rise by more than 3% in the next 18 month. Our own view is RBA rises will be less significant, else they will break the economy, but given the internationally rising inflation reads, and benchmark rates, we must expect mortgage rates to rise.

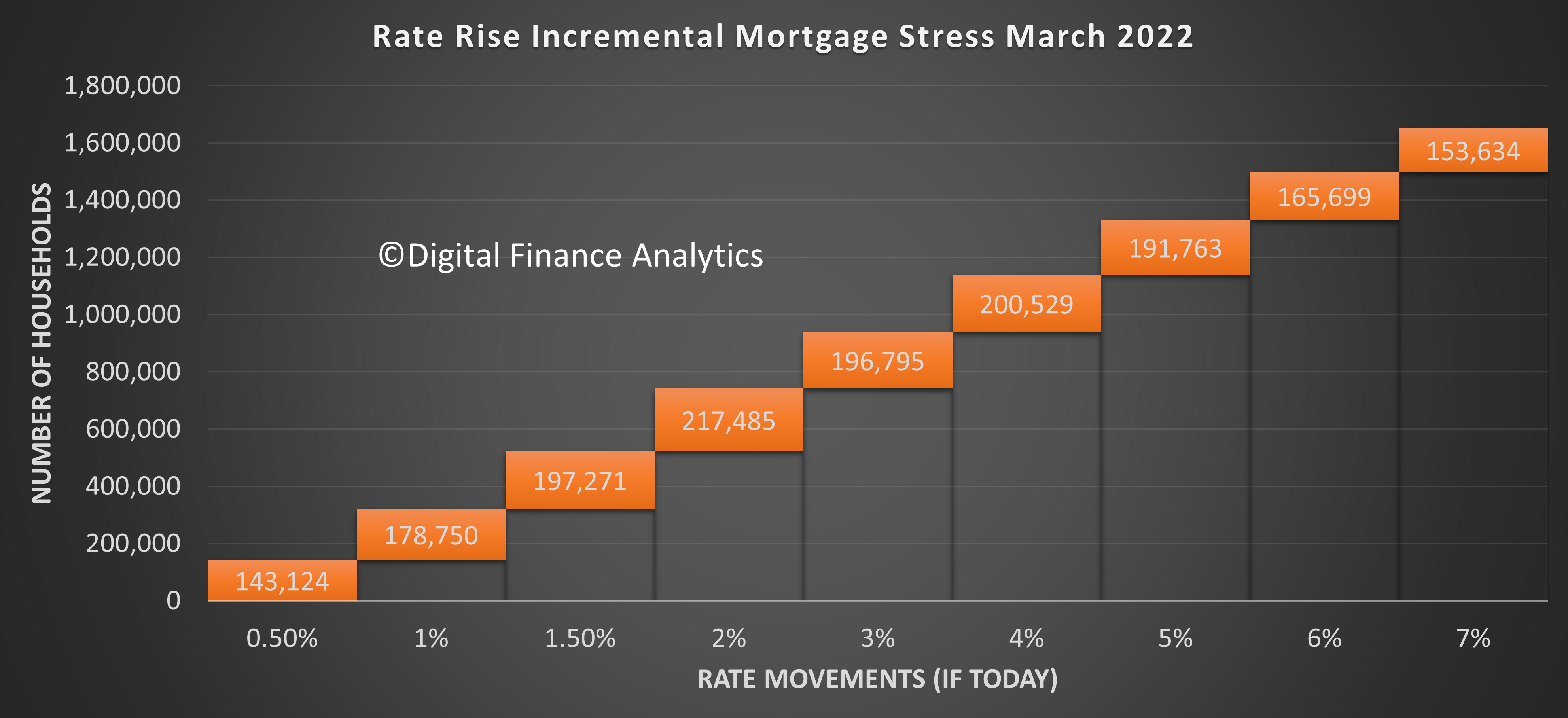

While some households are well able to handle higher rates, those in our stressed categories are less able to cope, thus stress levels would rise. Our modelling illustrated the potential additional number of households impacted by each rate increase.

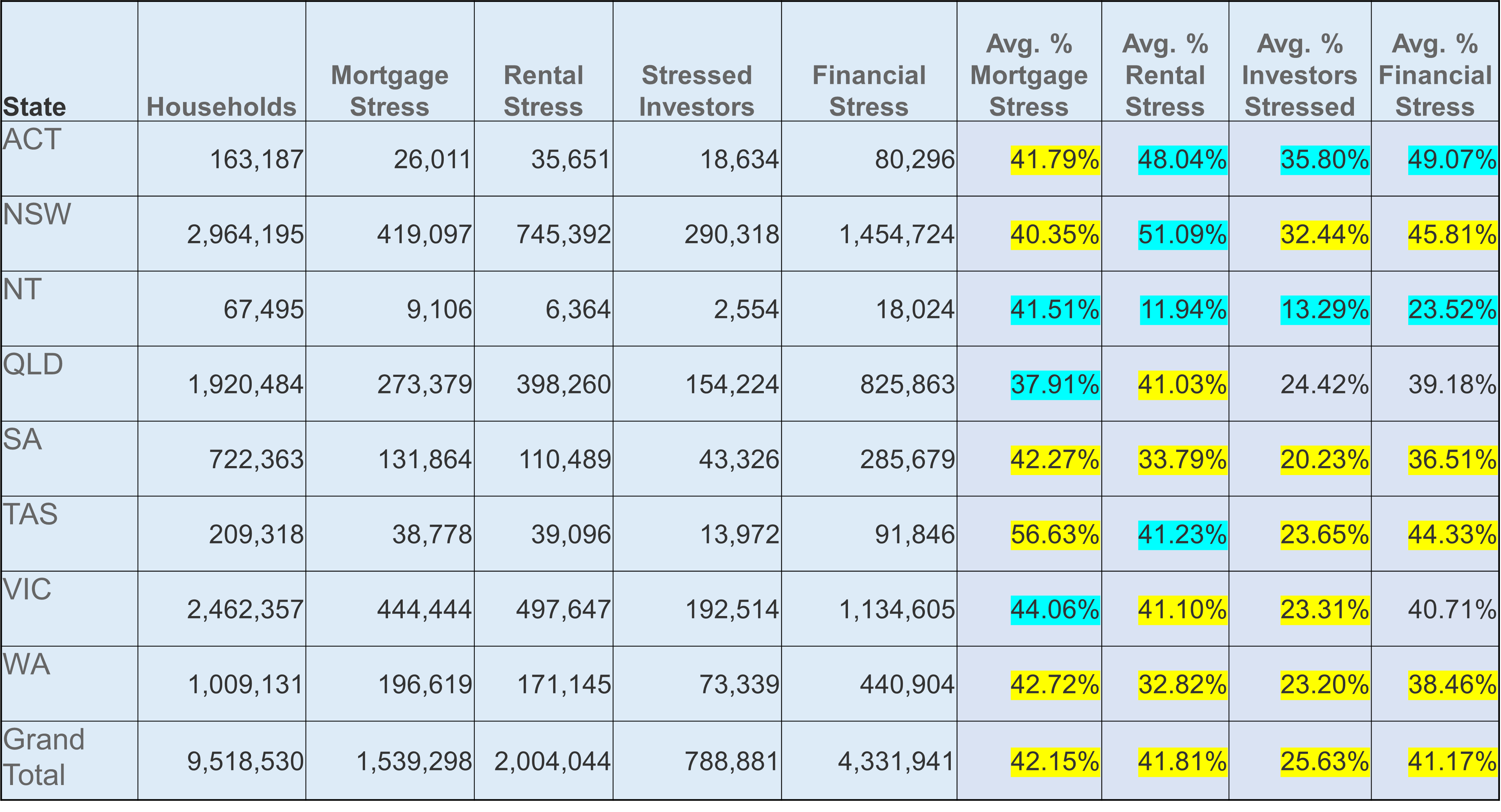

The current levels of stress are spread across most states and territories, with Tasmania the most exposed due to continued price rises, while incomes are flat or falling in real terms. Those highlighted in yellow are higher than the previous month. Rental stress is highest in New South Wales, while Investor Stress is highest in the ACT.

Analysis across our household segments shows significant pockets of stress among younger, often first time buyers many of whom bought in the high-growth development corridors around our major urban centres. That said no segment is untouched, and many first generation Australians are in difficulty.

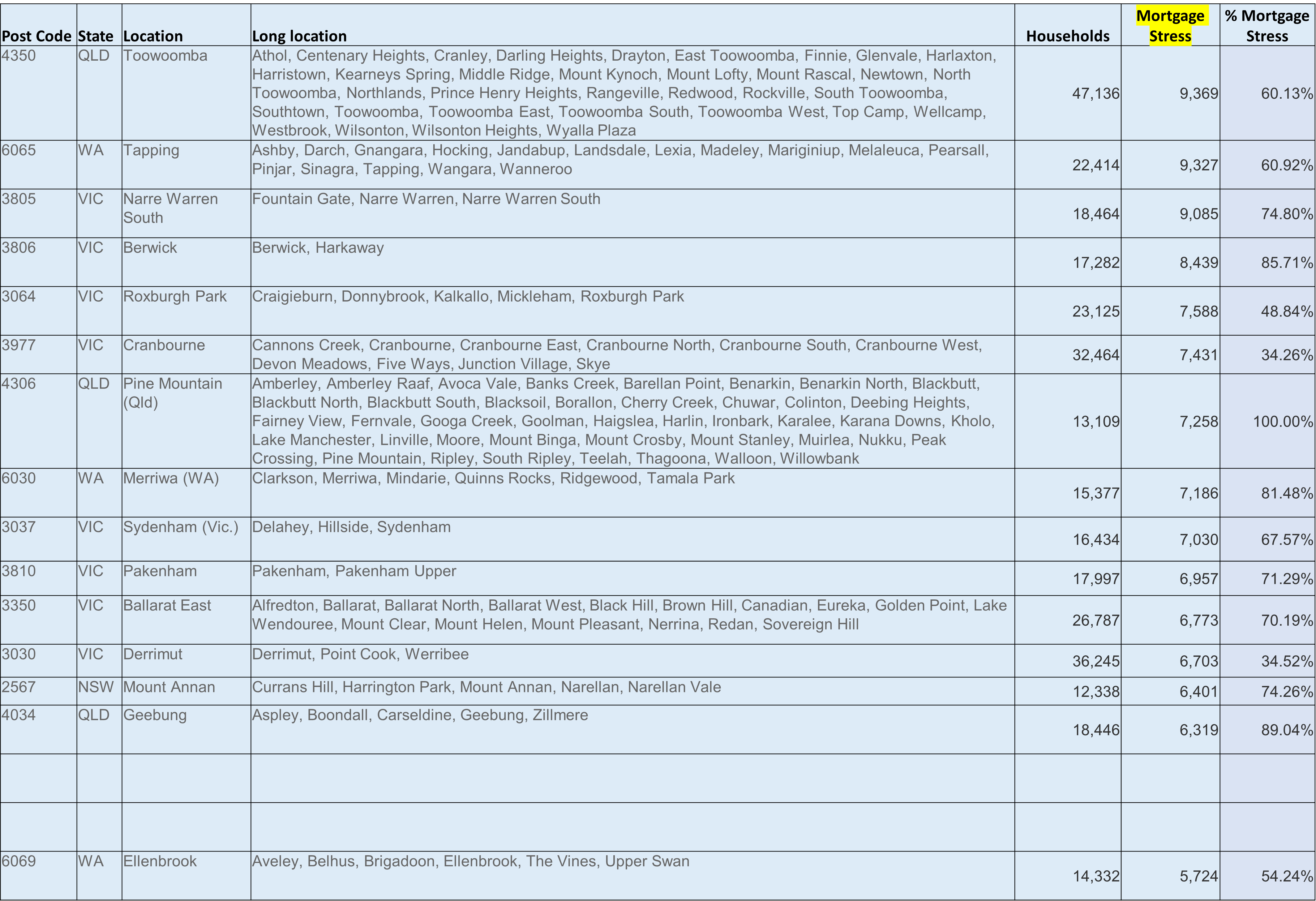

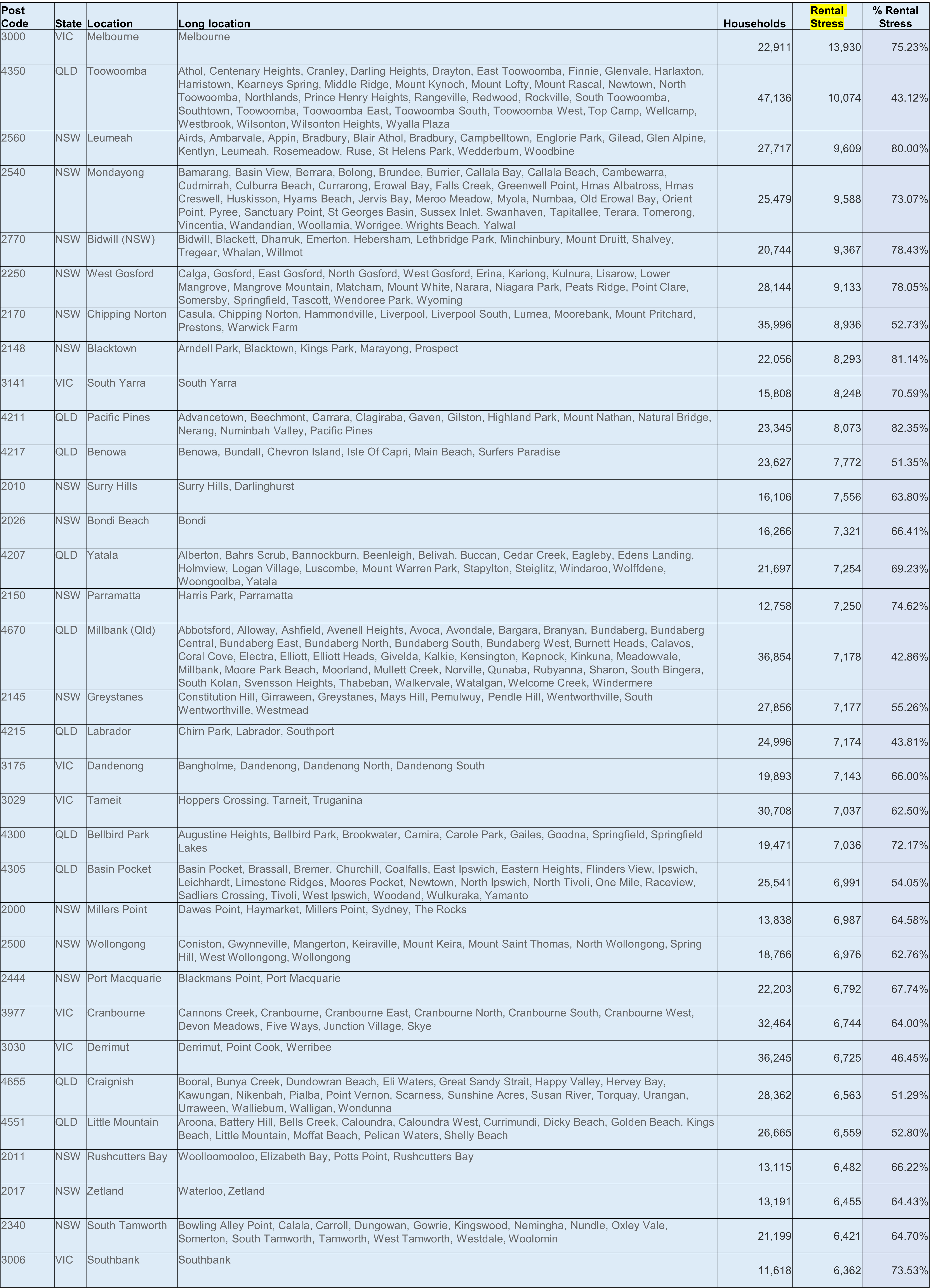

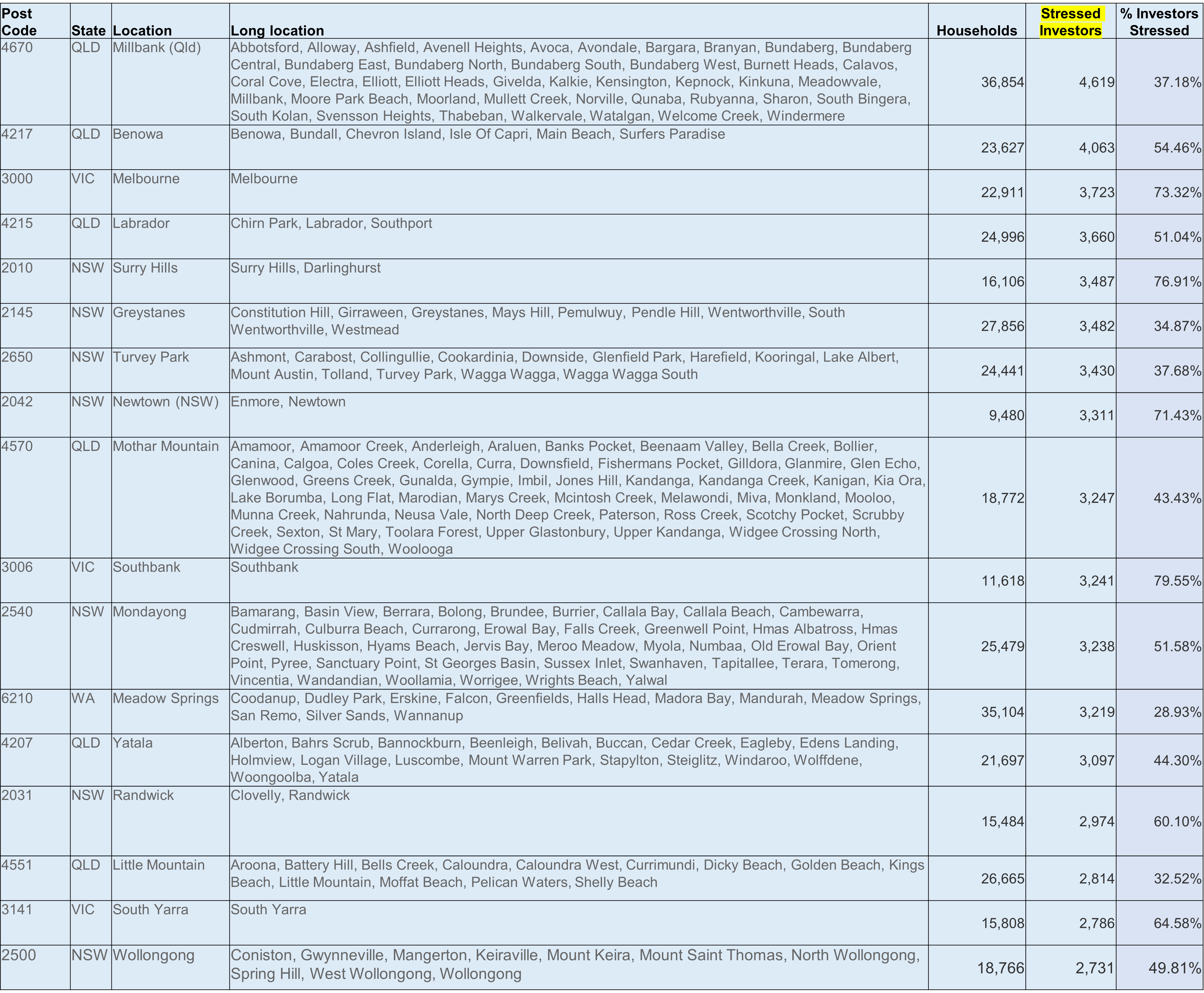

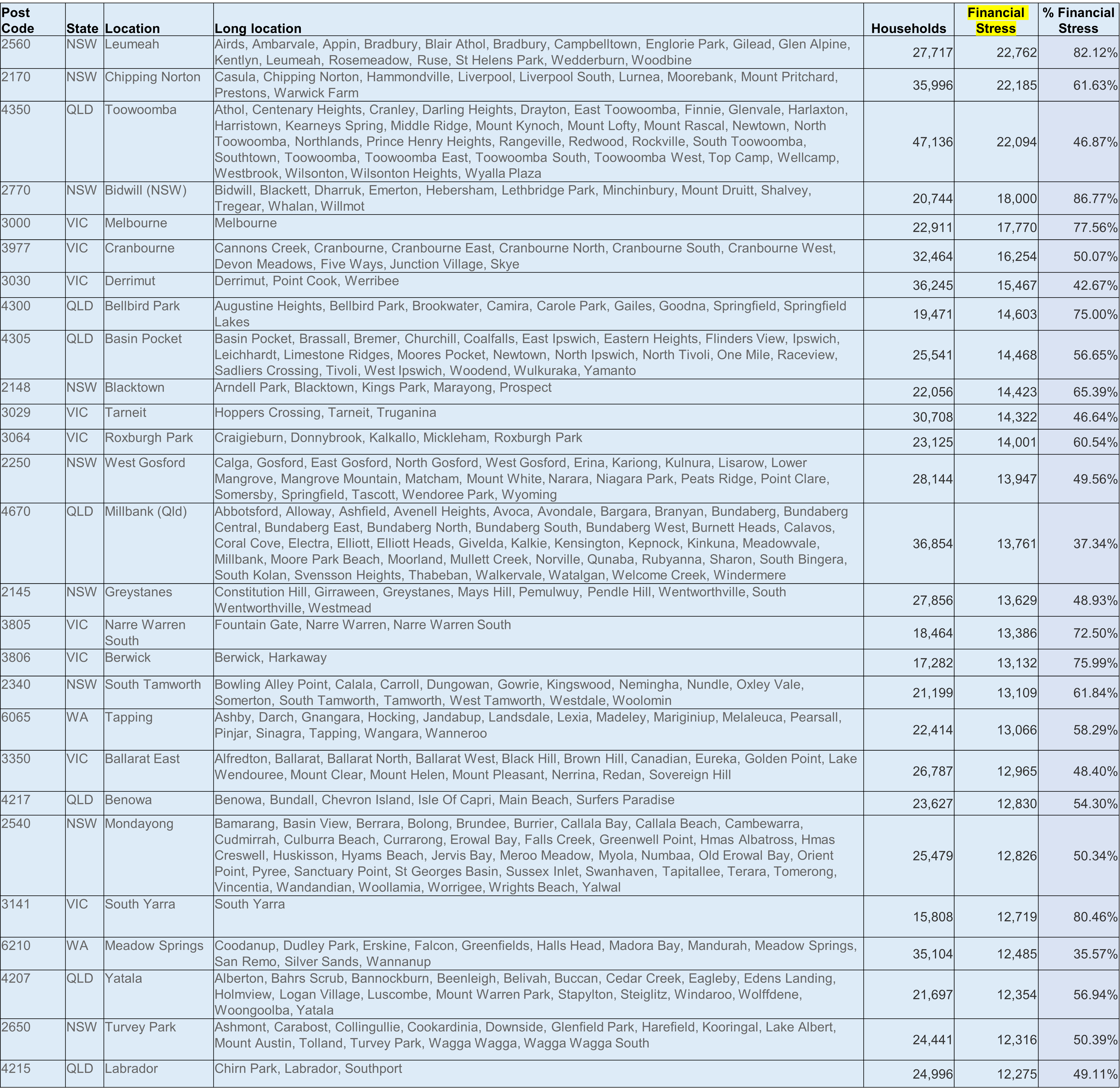

To complete the picture, we feature data on the top – most stressed post codes for our four stress categories.

Mortgage Stress – Top Household Counts

Rental Stress – Top Household Counts

Investor Stress – Top Household Counts

Financial Stress – Top Household Counts

Financial stress is an aggregate of mortgage, investor and rental stress, compared to all households.

Finally, we underscore that pressures on households are going to continue to build as inflation strengthens, and costs rise. Incomes in real terms are not. And mortgage rates are set to rise.

So households would do well to record their income and expenditure, because around half in our surveys have no clear view of their spending patterns, which makes prioritization impossible.

Households under stress with a mortgage should talk to their lender, as they have an obligation to assist – though refinancing or equity draw down are unlikely to be permanent solutions. In some cases a controlled property sale is a better option.

New borrowers would do well to ensure they have adequate buffers and not over commit at this point in the cycle, especially bearing in mind that the RBA has recently indicated property prices may well ease as rates rise.

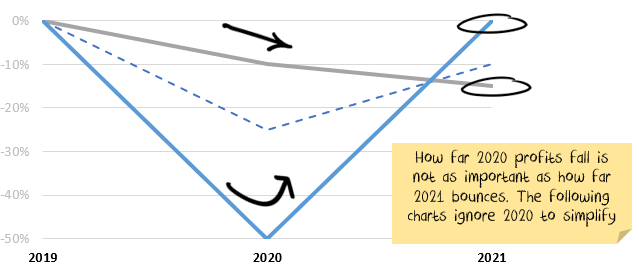

Investment markets have a host of both positive and negative factors fighting for supremacy. The real question is whether central banks and governments will engineer a continued suspension of capitalism. I was sceptical six months ago. I’m less sceptical now that capitalism will return anytime soon. On balance, however, there is still plenty of room for caution.

Short-term government policies to suspend capitalism (increased hurdle for bankruptcies, mortgage holidays, eviction moratoriums, banks not recognising bad debts, etc.) have morphed into medium-term policies. And, it is hard to see any government ready to exit. There is a quiet extension to each policy that lapses.

We took advantage of pre-election weakness to increase our risk exposure a little. But given the rise in markets since the election, the positive factors have mostly been reflected already. And, the positive factors tend to be short-term, the negative aspects tend to be medium-term.

Key positive factors for share prices

Government stimulus: Global governments continue to add stimulus. The US has some question marks, and the stimulus won’t be as large as if Biden won Senate majority. But it would seem additional stimulus is highly likely.

Low probability of US tax hikes: Subject to the Georgia senate run-offs, it looks unlikely the US Senate will pass Biden’s company tax rate increases. If passed, these would have reduced US earnings by around 10%.

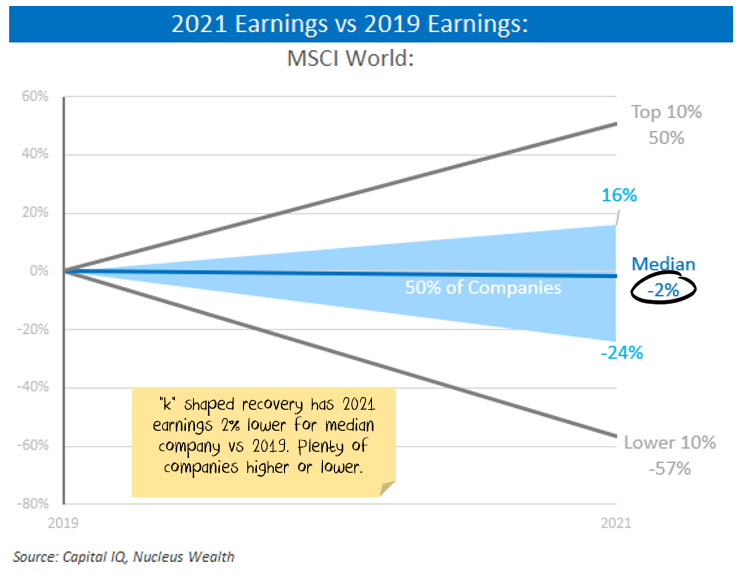

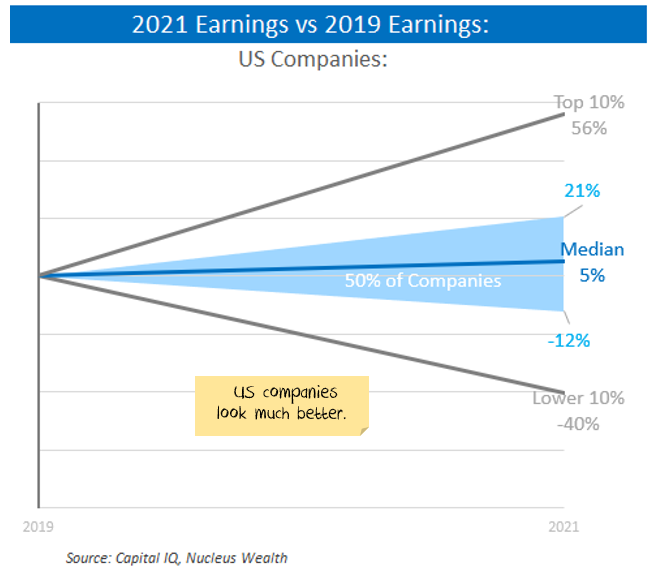

Earnings very good: 3rd quarter earnings were much better than expected. Analyst forecasts haven’t changed much, but that is better than usual! Typically, later year forecasts are far too optimistic and get revised down as they get closer. Forecast growth is 24% for 2021 and then 15% for 2022.

Inequality to remain high: No changes to taxes in the US = economic inequality likely to remain high. In Australia, there are tax cuts for the rich, reduced support for the poor. Travel limitations depressing spending for the rich. Plus stimulus tends to be relatively indiscriminate; some ends up in the right hands, some in the hands of those that don’t need it. Net effect: the rich have more money to put into investment markets.

Other positive factors for share prices

Bankruptcies, evictions limited: in many countries bankruptcies are down 30%+, driven by a mix of stimulus and rule changes. Businesses feel richer if they haven’t had to write down bad debts. Not fixing the problem, just delaying the pain.

Mortgage repayment holidays: as above.

Wage growth very low: helpful to company profits.

Productivity: forced change/digitisation often results in better outcomes. Having to fire staff usually results in the least productive going first, increasing overall company productivity.

Low oil prices: keeping transport costs down.

Vaccine hope: successful trials give hope to an end of the virus.

Policy certainty: President Biden is far less likely than Trump to be unpredictable.

Key negative factors for share prices

COVID in the Northern Hemisphere: It is ripping through populations. Importantly, hospitals are reaching capacity, which means lockdowns have begun again in Europe and seem highly likely in the US.

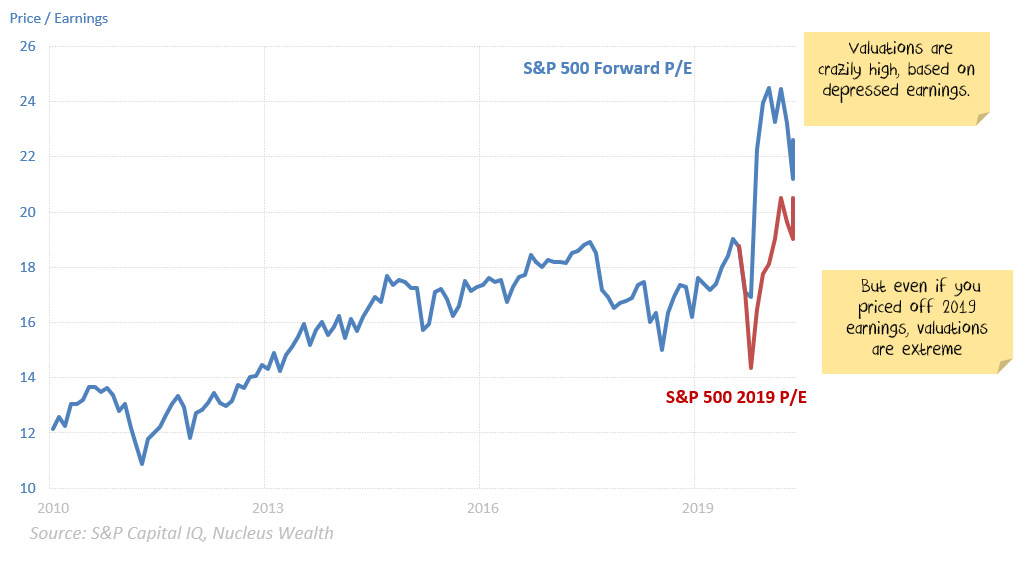

Valuation: Share market valuations are extraordinarily high.

Latent bankruptcies: Changing the rules so that companies and individuals who are otherwise bankrupt are allowed to increase their debt does not fix the problem. It also runs the risk that the bad actors not paying their bills start to pull down the good actors.

Low genuine credit growth: credit growth has been poor; banks are still tightening lending standards. But the credit growth also includes mortgage holidays. And companies borrowing to survive rather than to make productive investments. Which means genuine credit growth is lower than the already weak headline numbers. Economic growth has been tied at the hip to credit growth for the last decade. It is difficult to see what will replace easy money as the only thing holding economic growth up.

Other negative factors for share prices

Short term gap in US economic conditions: There may not be stimulus until Biden takes power. If so, there are three months with limited government support while the virus sets new records. This might be enough to tip the economy into a funk and result in more job losses.

Inequality longer-term effects: the short term effect of increased inequality increases savings and investment and (probably) increases stock market valuations. The longer-term impact is depressed demand and profits. And more political upheaval.

Structural change: leading to weak demand, higher unemployment. There are industries like travel and tourism which will have to deal with lower sales and employment. The means job losses continue as former employees have to give up on finding a job and retrain for a new industry.

Net effect

It bears repeating: the positive factors for investment markets tend to be short-term, the negative ones medium-term. Will there be “clear air” for a few months before the consequences begin? Maybe. The stock market has had a lot thrown at it and is still holding up.

On the flip side, the risks are not symmetrical. The upside appears more limited than the downside.

Damien Klassen is Head of Investments at Nucleus Wealth.

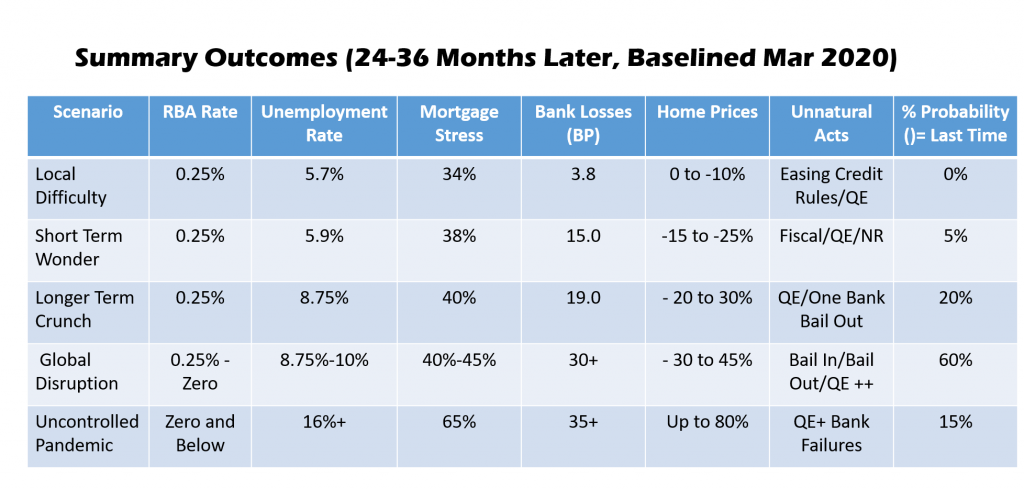

We ran our live show, complete with updated data and scenarios, plus answering questions real time via YouTube chat. How much will mortgage stress be up? What is the trajectory of potential defaults? Which post codes are most in the front line? All are answered

The latest results from the DFA household surveys examining property sentiment, reveals how much things have changed in the past month, from a pre-COVID to a COVID world.

These results are from our rolling 52,000 survey database, and we are able to track sentiment across our various household segments, and across owner occupier and investor cohorts. And I should note that although we run the analysis down to a post code level, the shifts are pretty uniform across the country.

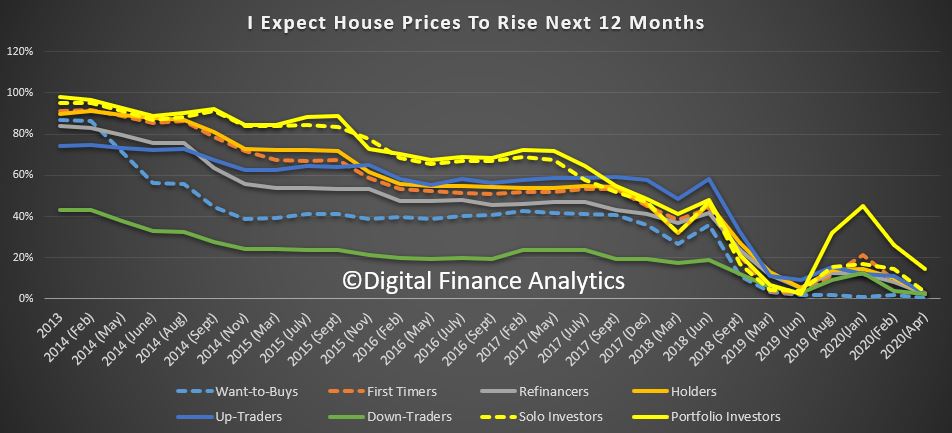

First, we see that the intention to transact has dropped, across all property segments, and there are significant shifts among those seeking to trade downwards in order to to release equity, as fears of equity reduction rise. That said, some here are still seeking to exit now, fearing greater falls later. We covered this in our recent forced sales analysis. Property investors are also stepping back – no real surprise given the fall in rents, and the rises in listings we are seeing. First time buyers are also backing off. Thus sales volume will drop, significantly.

Property price expectations are shifting down, with a massive drop in those expecting any rise in the next 12 months (we may need to change the question to falls in the months ahead!). Portfolio investors remain a little more bullish, but it is all relative.

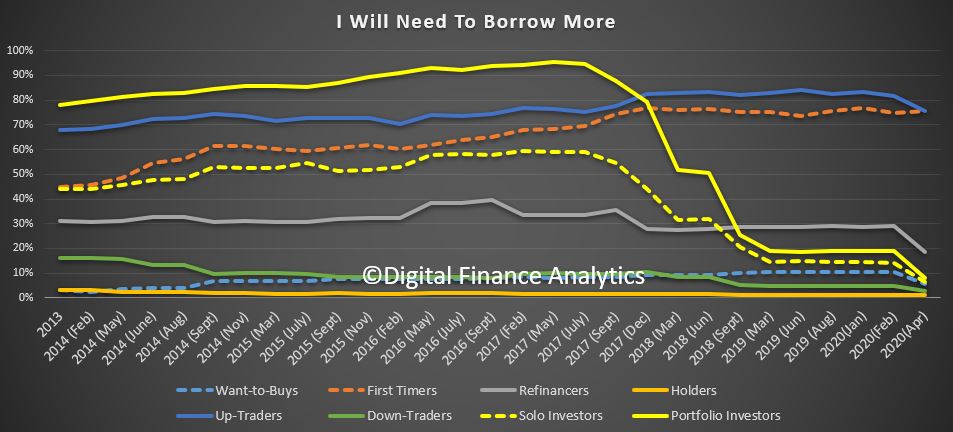

Demand for credit for property purchase also fell, though those seeking to refinance to gain rate discounts are still evident. In two segments, those seeking to trade up, and first time buyers, will still need to borrow more – if they were to transact. As above though the number borrowing is low for now.

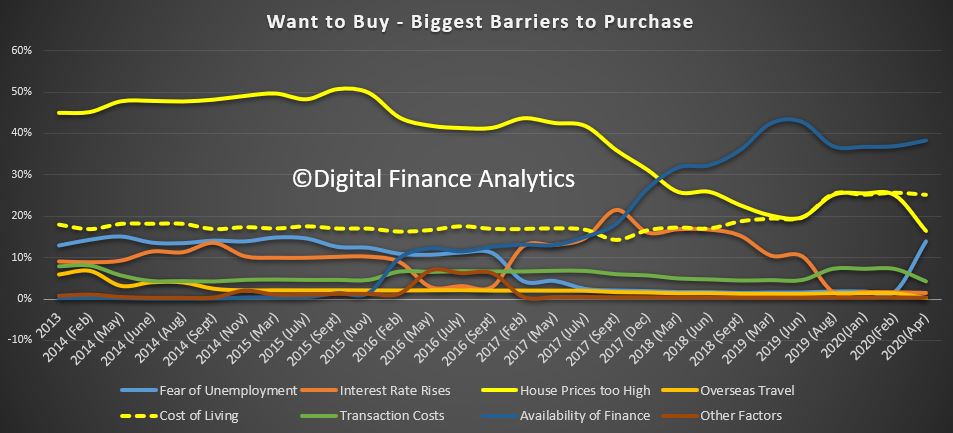

Across the segments, those wanting to buy saw a significant acceleration of concerns about the fear of unemployment – no surprise there.

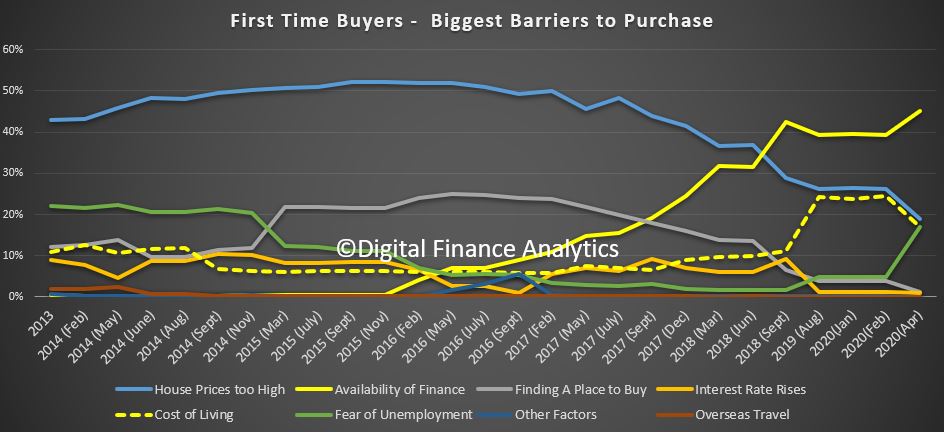

The barriers for first time buyers include the availability of finance (we know some lenders are asking more questions about employment, and income than a month back). Again we see the fear of unemployment lifting consistent with other segments.

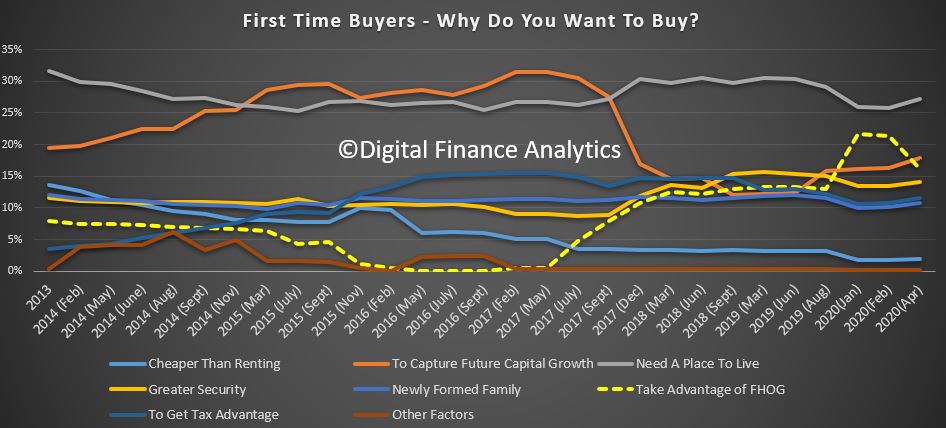

First time buyer motivations show that the attractiveness of the First Owner Grants tailed off, and there was a slight uptick in future capital growth expectations.

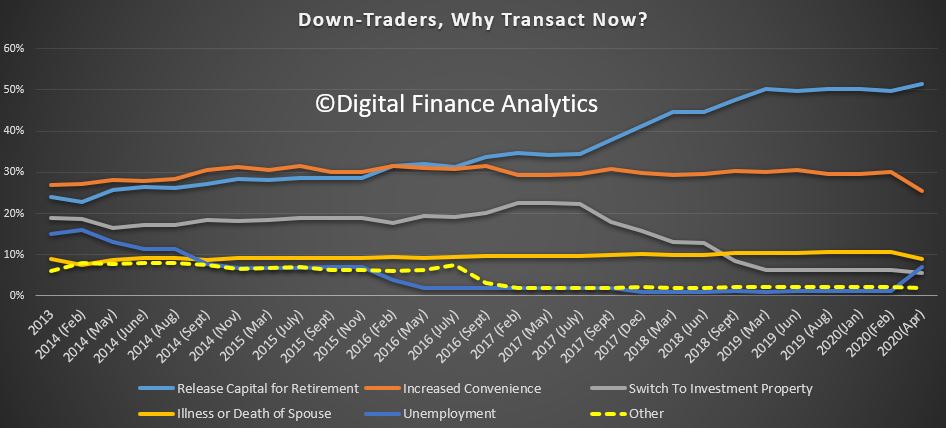

Down traders are driven mainly by a need to release capital for retirement (good luck with that!) and again we see the uptick in unemployment driving the decision to transact.

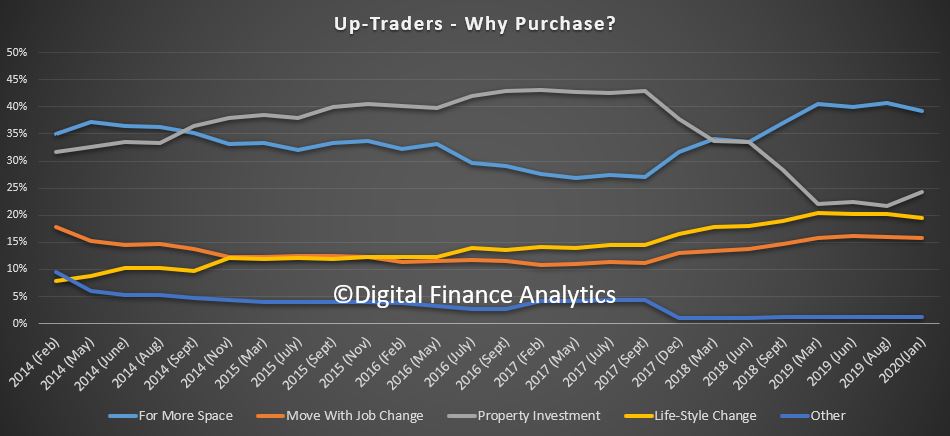

Those seeking to trade up still have the same basic motivations.

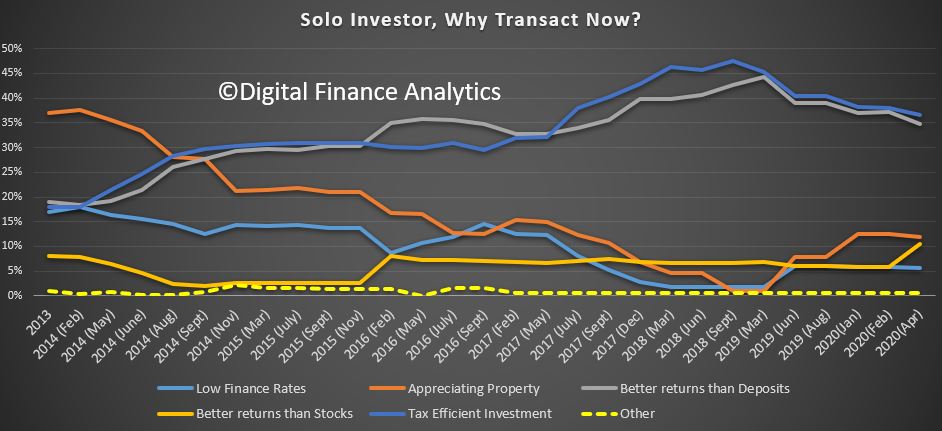

Property Investors are swinging a little towards equity investments, and under 20% are expecting future capital gains for now. Low finance rates, and prospective better returns than deposits remain the stronger themes, though as I have highlighted before, many property investors would be disappointment if they did but calculate the real returns on property. They are overstated, especially if capital values continue to fall.

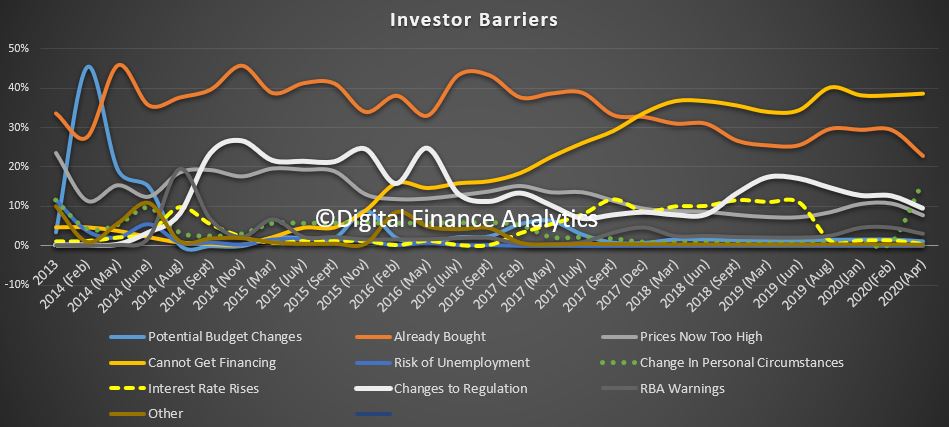

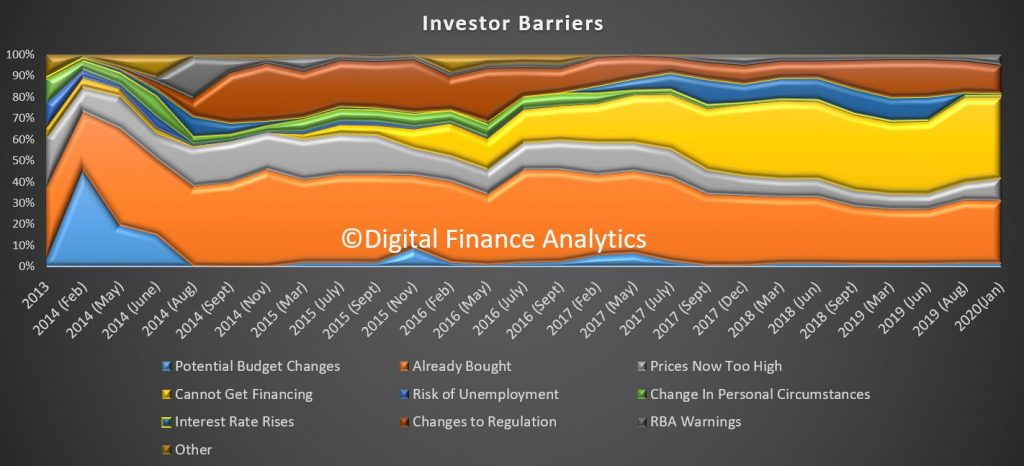

On the other hand, the barriers for investment reveals difficulty in getting financing, and changes in personal circumstances as significant risk factors.

I should caution we may see sentiment swing back in the weeks ahead as things play out, but in summary for now, demand for property is sinking, availability of finance is tightening, and the spectre of unemployment is rising. Property prices are likely to fall, now its a question of how far!

We are releasing the latest data from our household surveys to January 2020 relating to segmented buying intentions and home price expectations. This is using data from our rolling 52,000 households nationally.

In overview, households have got the memo from the Government, that home prices are expected to rise – and this is influencing their forward expectations and buying intentions; to an extent. However, high prices and the significant debt burden, along with no income growth, and overall financial pressures are working against this intent. And property investors remain on the side-lines while first time buyers are lining up to take advantage of the Government scheme which has just commenced. There are 10,000 guarantees available now, and a further 10,000 in the next financial year. Not enough to meet demand.

As normal we will begin with our cross segment comparisons, before looking in more detail at the highlights of specific groups.

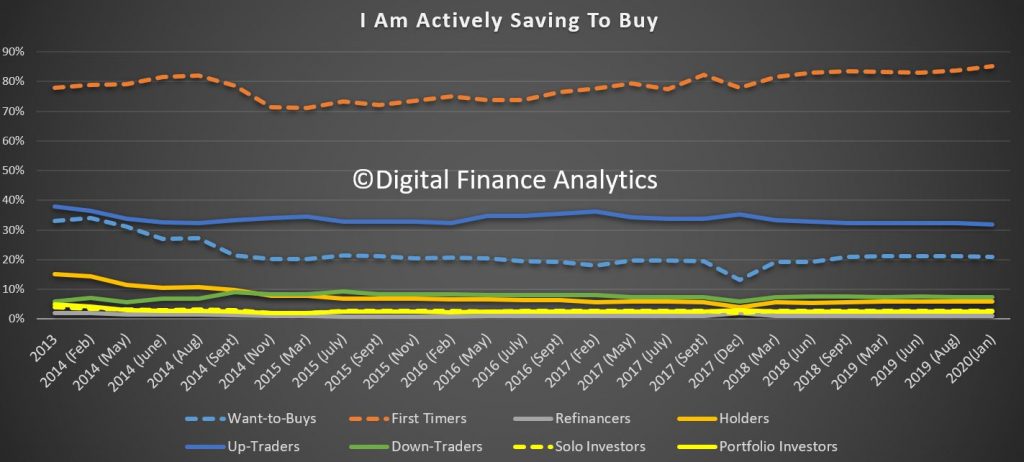

The intention to transact in the next 12 months is supported by two segments, first time buyers and down traders. The former are trying to get into the market for the first time, the latter are trying to exit the market to release capital. There are net more exits than entrants, so this suggests a supply demand disequilibrium. Investors remain sidelined.

We find that first time buyers and want-to-buys are savings hard, though lower interest rates are making the task harder. Up traders (people planning to up-size) are also saving, but at a slightly slower rate.

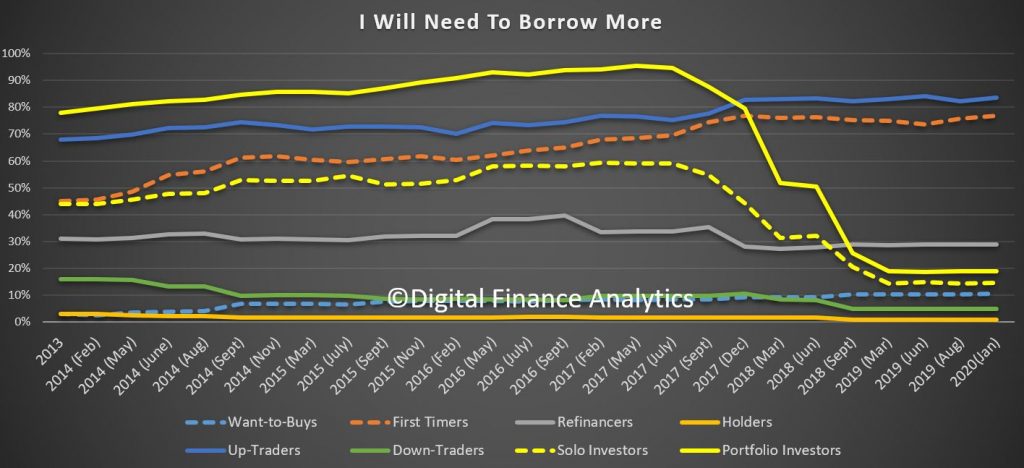

The intention to borrow is an important measure as it drives prospective mortgage growth ahead. The survey results suggests demand will be anemic and be driven by first time buyers and up traders, rather than investors. Not enough to suggest a significant lending recovery, yet.

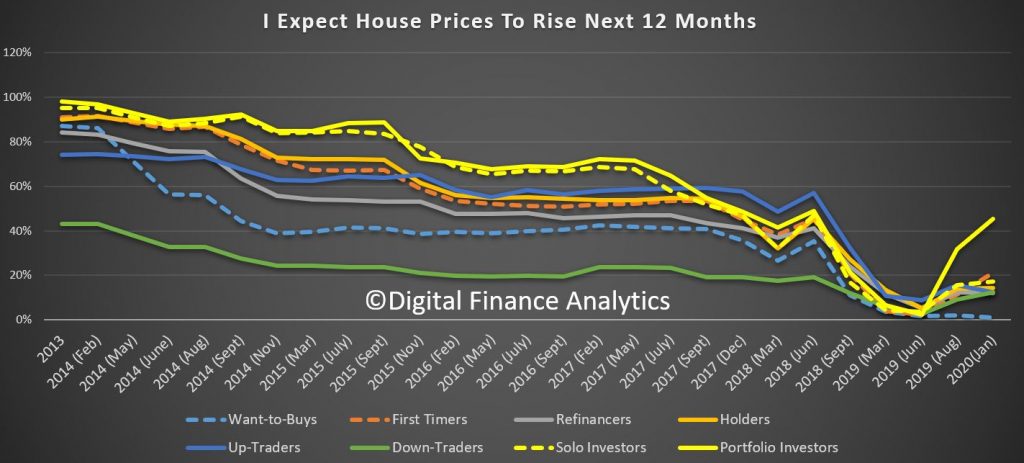

Price growth expectations are rising, led by property investors, up 14% from September, and first time buyers up 10%. Other segments appear less convinced however.

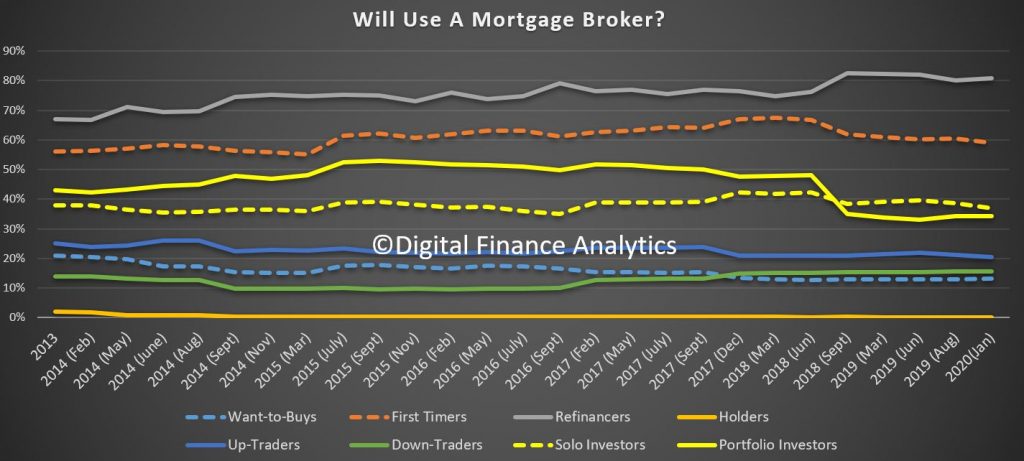

Across the segments, the preference for using a mortgage broker remains close to longer run averages.

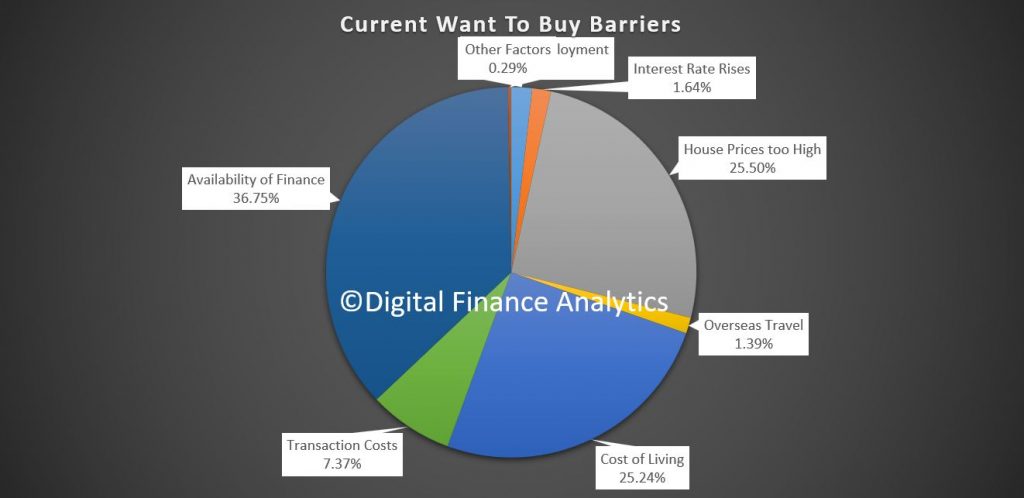

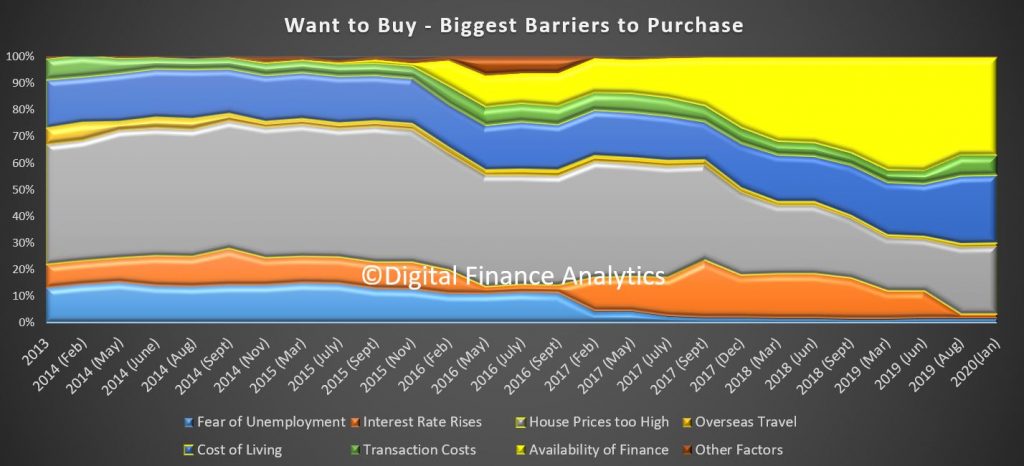

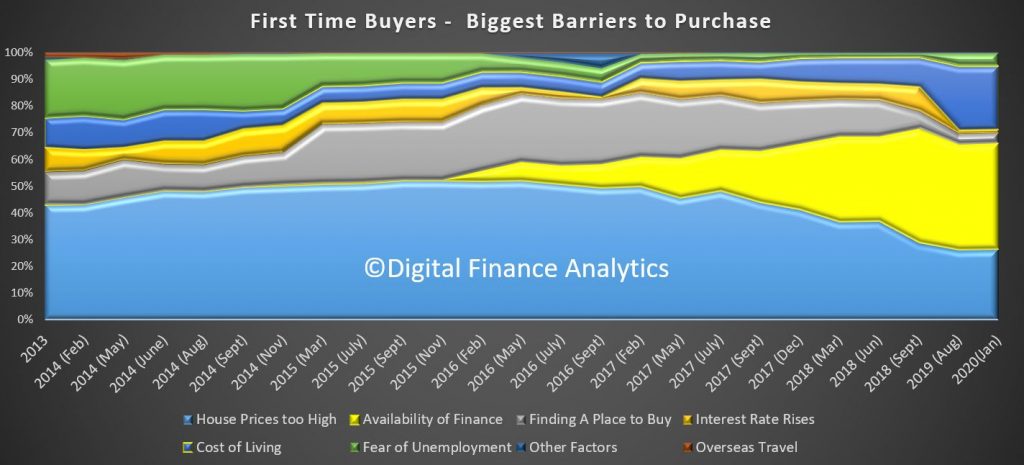

Now, looking in more detail at the segments, those 500,000 households wanting to buy are largely limited by access to finance (37%) (often because their incomes are insufficient or uncertain), that prices are too high (26%), high costs of living (25%) and transaction costs, like stamp duty, LMI premiums, and legal costs (7%).

In trend terms, the availability of finance has eased, down from 43% to 37%, while high home prices and rising costs of living have become a more significant barrier recently.

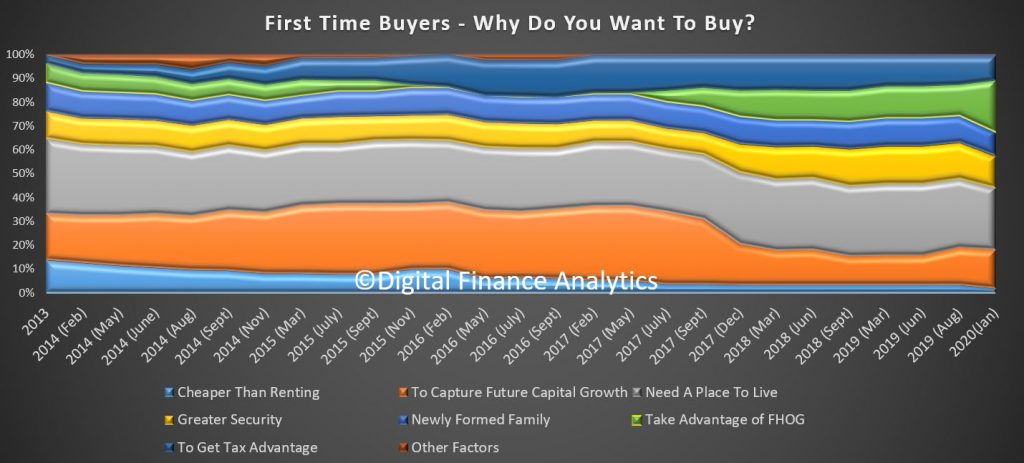

Turning to first time buyers, there are around 350,000 households who are actively saving with an intention to buy when they can, and the count has been rising in the past few months, partly thanks to the announced Government-back deposit scheme, which is discussed recently in our post: First Time Deposit Scheme: Fish Or Fowl? Loan approvals are running around 10,000 per month, so only a small proportion of the first time buyer pool will be able to take advantage of the scheme, which may put upward pressure on property in the target zones! 22% intend to use the scheme, so more than the guarantees available.

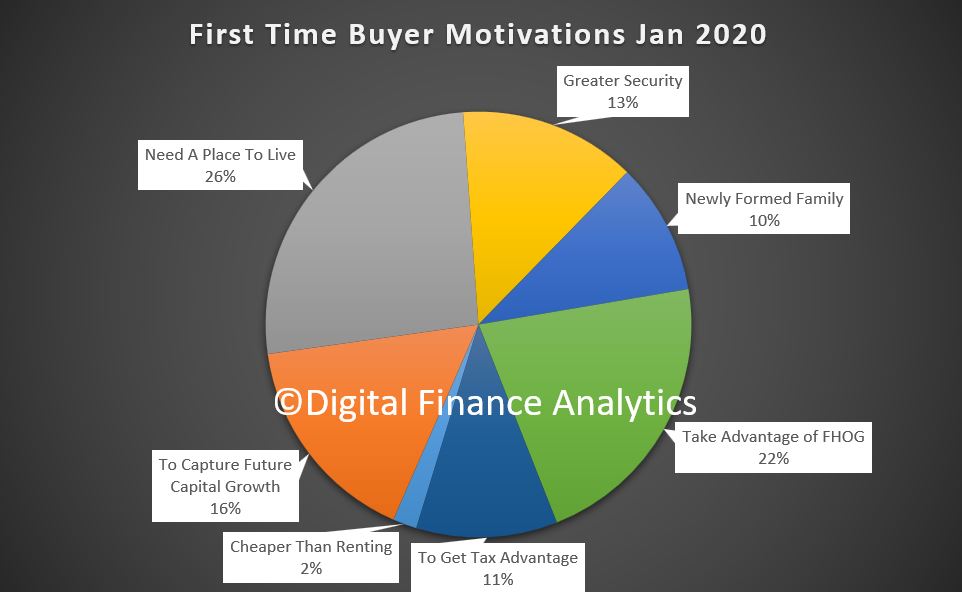

First time buyers are motivated by needing a place to live (26%), with greater security than renting (13%) and to capture future capital growth (16%), or tax advantages (11%). Around 10% transact as part of a newly formed family.

The trends highlight the impact of the new Government scheme, and the rising expectations of future capital gains, compared with a few months ago.

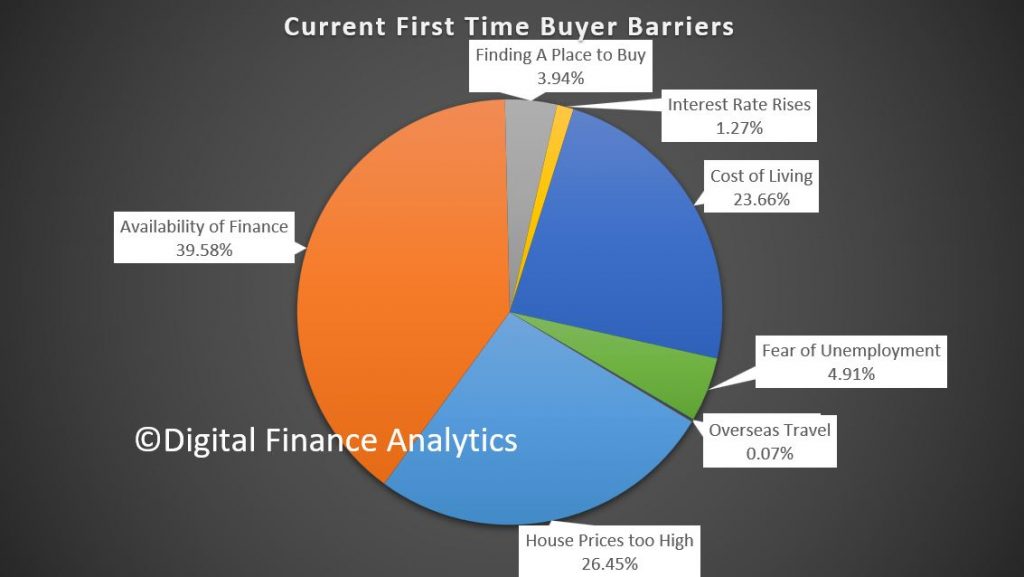

But first time buyers are still facing considerable barriers, including availability of finance (40%), prices too high (26%) and pressure from costs of living rises (24%). Property availability and fear of rising interest rates have both dissipated.

The trends highlight how finance availability remains an issue, and home price concerns are rising again, while there has been a big spike in costs of living in recent times. So many will struggle to buy.

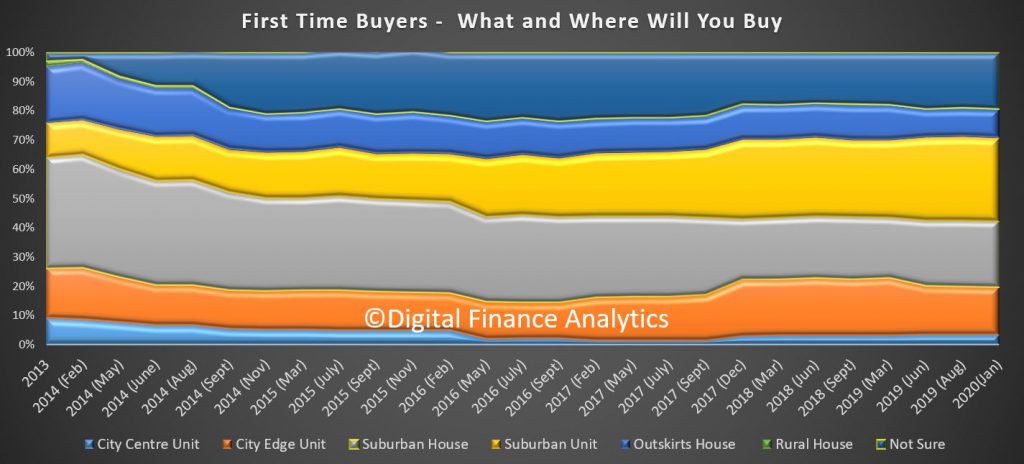

We also see a greater focus on purchasing houses rather than units, a reflecting on the bad publicity in recent times relating to the poor quality of construction and flammable cladding issues.

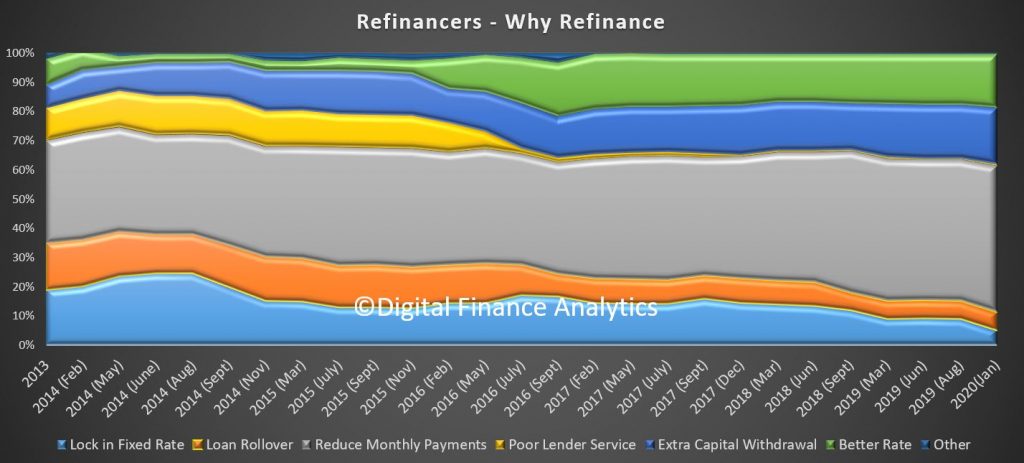

Turning to refinancing, we see the primary motivation is to reduce monthly costs (50%) , capital extraction (19%) and seeking a better rate (19%). Intention to lock in a fixed rate has fallen to 5%, on the expectation that rates will fall further ahead.

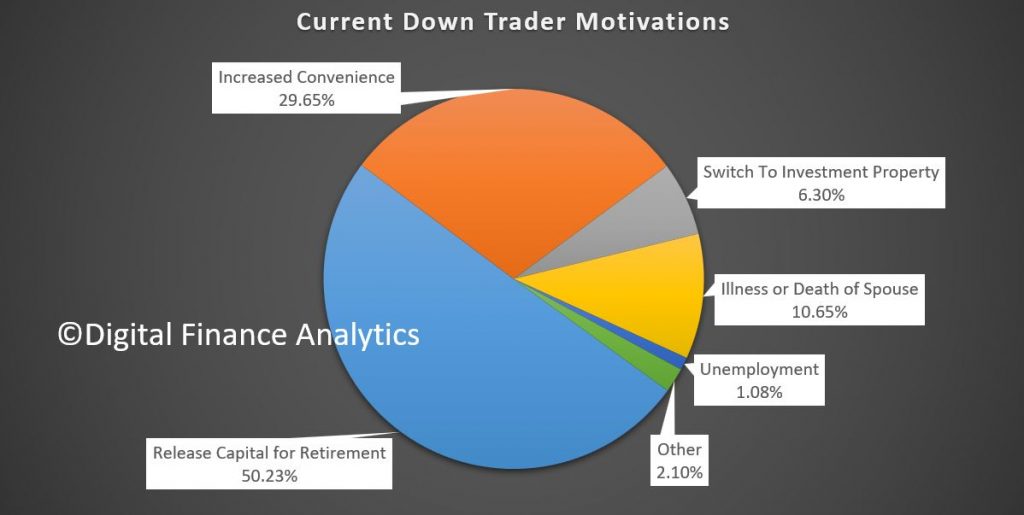

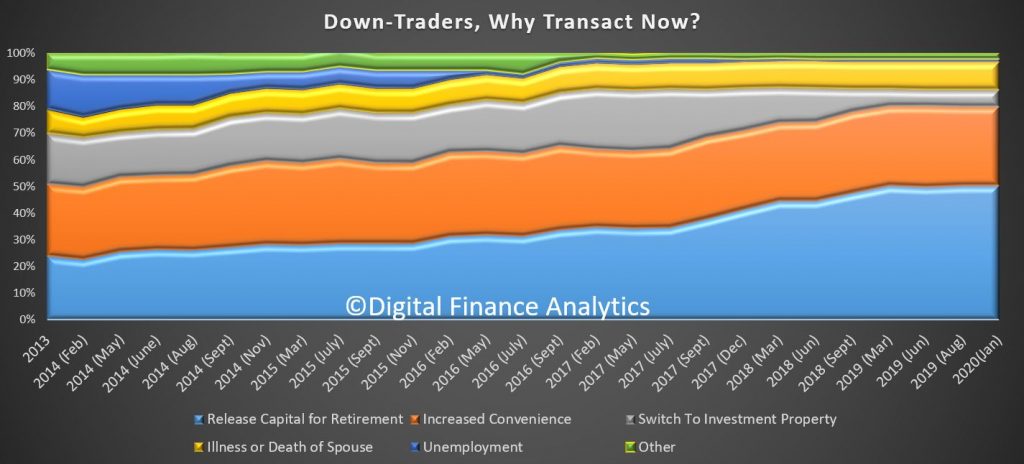

Among those seeking to sell and release capital – and perhaps buy a smaller place – our down trader segment, with more than 1.2 million are in this category, and 56% are hoping to transact. The main drivers are to release capital (56%), increased convenience (30%) and illness or death of spouse (11%).

In trend terms, interest in investment property remains at a low 6%, compared with 23% back in 2017.

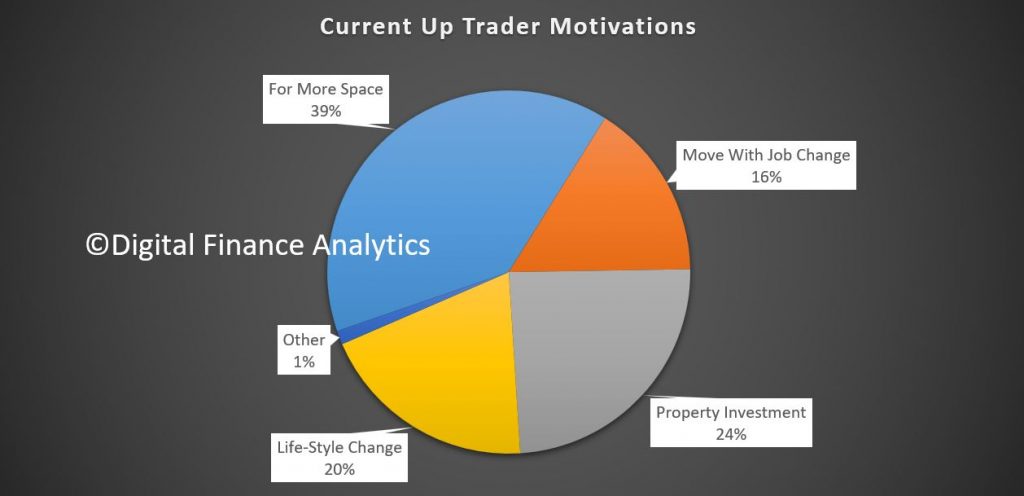

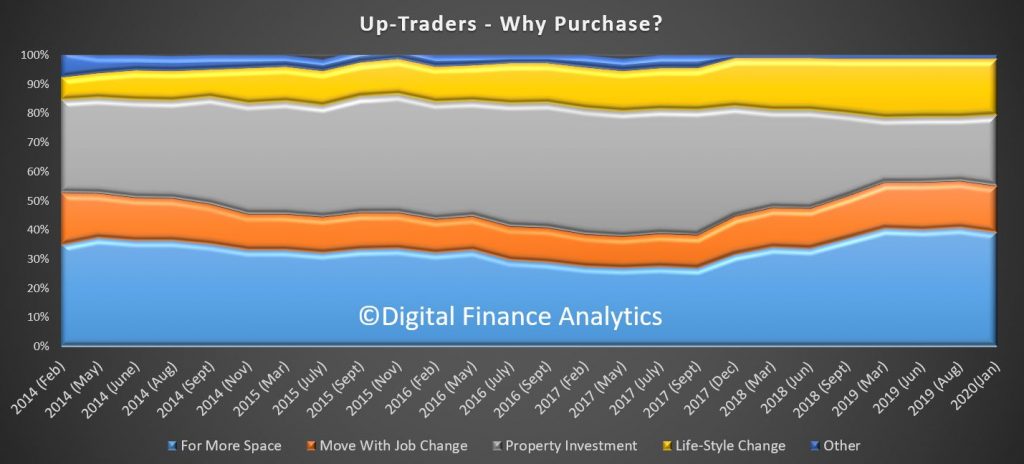

Up traders remain active but there are around 500,000 actively in this category. The main motivations are a desire for more space (39%), life-style change (20%), and job change (16%). 24% are driven by the expectation of future capital growth.

The trend tracker shows the property investment driver is weaker now, while more space and life-style are stronger drivers.

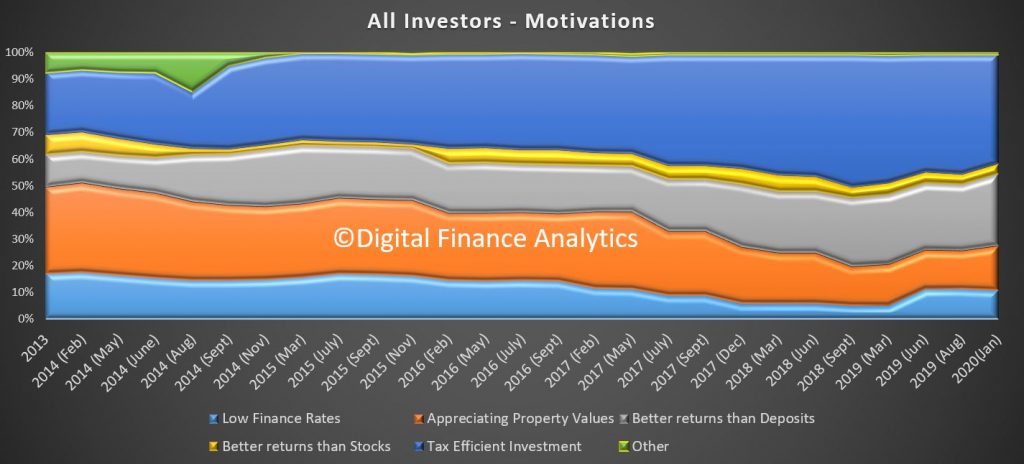

Turning to property investors, tax efficiency features as the strongest driver at 41%, down from 50% back in 2018. Better returns than deposits rose to 27%, reflecting the recent cash rate cuts. Low finance rates also feature at 11% and appreciating property values at 17%, higher than a few months ago. Within the investor segments, portfolio investors (those with multiple investor properties) are most hopeful of capital growth.

Barriers for investors include they have already bought property (30%), they cannot get financing (38%), down 2% from September, and changes to regulation (13%), including tighter rules on income and cost assessments.

There are around 1.3 million property investors, and many remain on the sidelines, due to low rentals, higher vacancy rates, and financial pressures. Of course the switch from interest only loans continues to bite too.

So, in summary, while there are some signs of interest in property, the segments really active are primarily first time buyers, and those trading down and up. There are more sellers than buyers in these groups, so if investors remain on the sidelines, we doubt prices can continue to drive higher, unless mortgage lending really accelerates (who would borrow?) or rules on loan serviceability are loosened further. The first time buyer deposit scheme will not be sufficient to turn the market around, though it may help some builders to shift newly completed or vacant property in the short term.

Nevertheless, households appear more bullish about future home price growth than a few months back – despite the fact the levers of growth appear disconnected from reality judging by these survey results.

John Adams commemorates December 3rd, a fateful day in Australian history, yet an event which marks an important point in the development of democracy. Lest we forget.

The Eureka Stockade, rebellion (December 3, 1854) was when gold prospectors in Ballarat, Victoria, Australia sought various reforms, notably the abolition of mining licenses and clashed with government forces. The rebels’ hastily constructed a fortification in the Eureka goldfield.