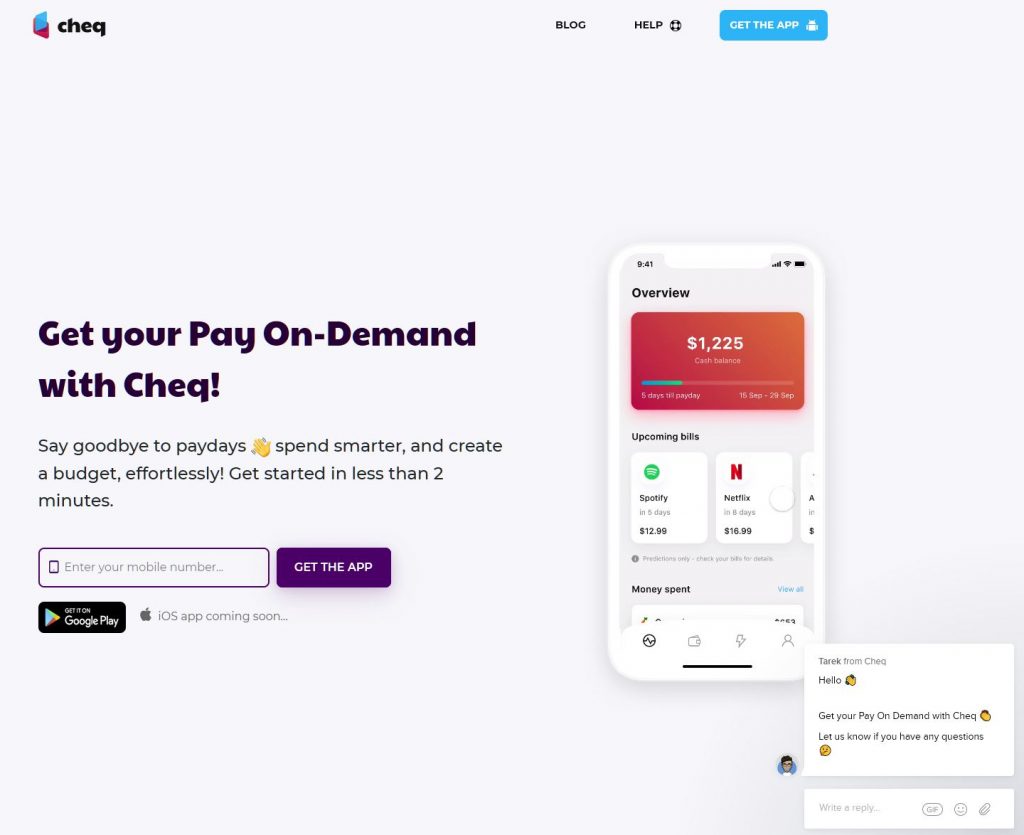

In the latest of our “Fintech Spotlight” series of posts, we look at a new player who is attempting to disrupt Payday lending using a digital platform and smart analytics. As normal, DFA was not paid for this post, and the views expressed are our own.

I caught up with CEO & Co-Founder of Fintech Cheq, Tarek Ayoub, to discuss how Cheq has the potential to prevent thousands of vulnerable Australians from turning to predatory payday lenders, with their sky-high interest rates and fees, and their vicious repayment structures which are designed to keep people trapped in a crippling cycle of debt.

Cheq Founder – Tarek-Ayoub-and-Dean-Mao

In fact, Cheq has just raised $1.75 million in debt and

equity to launch a revolutionary ‘Pay On-Demand’ (POD) solution. This allows

working Australians facing a cash shortfall to access their accrued wages

instantly up to $200. Cheq charges a fixed transaction fee of 5 percent with

absolutely no additional fees or interest, compared to the 52 to 1,000 per cent

annualized percentage rates charged by payday lenders on similar amounts.

We know there are around 5.9 million Australians currently

living paycheck to paycheck who often resort to payday lenders during cash

shortfalls.

Ayoub, an ex-management consultant, with a track record in the finance sector, highlights the rise of the ‘on-demand’ economy. “As our society increasingly embraces the ‘on-demand’ model of consumption, it is only natural that we begin to see this flow over into remuneration. You can get food, TV shows, cleaning services, dog walking, and everything in between on demand. So why is it that we can’t yet access our own money – money we have already physically worked for – as soon as it’s needed?”

Cheq is available via a mobile app, were individuals can register

for the service and link their bank account. Cheq uses the transactional data

from that account to analyse and profile the spending habits of the individual,

using machine learning, AI, and statistical analysis.

As important as the access to cash – up to $200 is, the real

power of Cheq is the personal financial management solutions built into the app

which helps users by predicting upcoming bills, categorising expenses, and

creating budgets for better money management.

As the relationship builds, Cheq is able to offer

suggestions to help manage financial stress. And the $200 advance, ahead of the

next wage, is automatically repaid in one hit, or as stage payments repaid in

2, 3 or 4 wage cycles (which can be weekly, fortnightly or monthly). Money is

only recouped from a user’s bank account once wages are received, so they can’t

exceed their spending capacity or get trapped in debt.

The $1.75m comprised $1.4m equity and a $350k debt facility from investors including VFS Group (an early investor in Grow Super) and Released Ventures. Interest has been received for more funding as the firm has grown to 5 employees and with ambitious plans ahead.

Six hundred users downloaded Cheq from the app store within 2 days of its beta launch and had more than ten thousand downloads in the first month. The typical user of the service is aged 24-35 years, often working in retail, call centres or fast food sectors. 70% of users have also used “Buy Now Pay Later” (BNPL) apps and 60% had also used payday loans. Most funds were used for transport and groceries, though many users left the money untouched in their accounts. But the most fascinating aspect is the fact that Cheq users were often weaned off payday loans in just a few months. This could be a game-changer.

Cheq is quite selective in their customer assessment, with

4,000 rejected so far. Applicants are screened via their proprietary assessment

model, without relying on external credit scores or other financial data such

as property equity or other assets.

By shifting from ‘enterprise first’ to ‘direct-to-consumer’,

Cheq puts the power over accrued wages back in the hands of all workers, says

Mr. Ayoub: “To achieve a future where Australians are free from payday

lender-induced debt traps, the solution must be available to everyone.”

Tarek says Cheq is also aiming to reinvent and pioneer POD

as a new industry category by being first in Australia to offer POD direct to

consumers. And he is eying markets in the US and India, where he believes a

similar solution would have significant take-up.

We think there are some parallels with what AfterPay did

with “Buy Now Pay Later” (BNPL) as a category killer, and once again a

financial services licence is not required, although in practice Cheq says they

would in any case exceed any responsible lending obligations. Cheq is therefore

regulated by ASIC.

On average, individuals who registered and completed on-boarding with Cheq took out their first advance 3 days later, with most users stating they liked the piece of mind they had to know that Cheq is there and can be used only when they have a shortfall in funds, according to Tarek.

The most fascinating aspect of this story is the alignment

to the customer, with the real purpose centred on financial management and

education, rather than turning a quick profit from vulnerable individuals. But it’s an open question whether Cheq is

primarily a data analytics firm, a financial services provider, or a financial

coach. The truth lies within that triangle. Payday lenders are on notice that their

business models are likely to be disrupted.

The New Zealand Reserve Bank has launched a new future-proofed payment settlement system, replacing New Zealand’s inter-bank settlement system and central securities depository.

The new platform replaces a

20-year-old system with two separate systems, ESAS 2.0 and NZClear 2.0. The new

platform comprises the Real Time Gross Settlement (RTGS) and Central Security

Depository (CSD) applications supplied by SIA – a European technology and

banking infrastructure leader and its wholly owned subsidiary Perago.

Infrastructure support services are supplied by Datacom Systems Limited.

The extent of change is

significant, says Assistant Governor/Chief Financial Officer Mike Wolyncewicz.

“Every day, transactions

with a value of more than $30 billion are settled, so there has been a focus on

getting this right, and not rushing out a replacement until we were confident

that it was ready.

“The buy-in from the

industry has been fantastic. This week’s successful changeover is the result of

months of rigorous testing and we appreciate the cooperation of the system’s

key users.”

The Reserve Bank’s payment

settlement system is used by 57 member organisations including banks,

custodians, registries and brokers. This equates to around 600 users of the

system, from New Zealand, Australia and Asia.

“Our members now have access

to far more modern, future-proofed and leading edge systems for them to manage

their day-to-day interactions with the Reserve Bank,” Mr Wolyncewicz says.

The systems replacement

follows a strategic review of the incumbent payment and settlement systems

operated by the Reserve Bank, completed in 2014 in anticipation of the need to

align with today’s operational and technological standards.

The Australian government touts compulsory income management as a way to stop welfare payments being spent on alcohol, drugs or gambling. Via The Conversation.

The Howard government introduced the BasicsCard

more than a decade ago. About 22,500 welfare recipients now use it,

mostly in the Northern Territory. Now the Coalition government has big

plans for a more versatile Cashless Debit Card, trialled on about 12,700 people in four regional communities in Western Australia, South Australia and Queensland.

The 2016 Indue Cashless Debit Card.

indue.com.au

These trials aren’t complete, nor the findings compiled, but a string of senior ministers, including Prime Minister Scott Morrison, have indicated they are already sold on expanding the program.

Over the past year we have conducted the first independent, multisite study

of compulsory income management in Australia. It has involved 114

in-depth interviews at four sites: Playford (BasicsCard) and Ceduna

(Cashless Debit Card) in South Australia; Shepparton (BasicsCard) in

Victoria; and the Bundaberg and Hervey Bay region (Cashless Debit Card)

in Queensland. We also collected 199 survey responses from around

Australia.

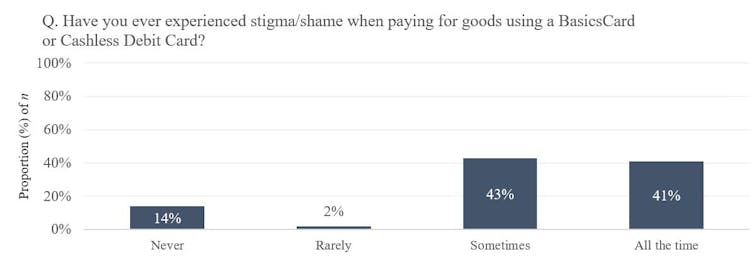

Proponents of compulsory income management

champion its potential to “provide a stabilising factor in the lives of

families with regard to financial management and to encourage safe and

healthy expenditure of welfare dollars”, as the then social services

minister, Paul Fletcher, said in March last year.

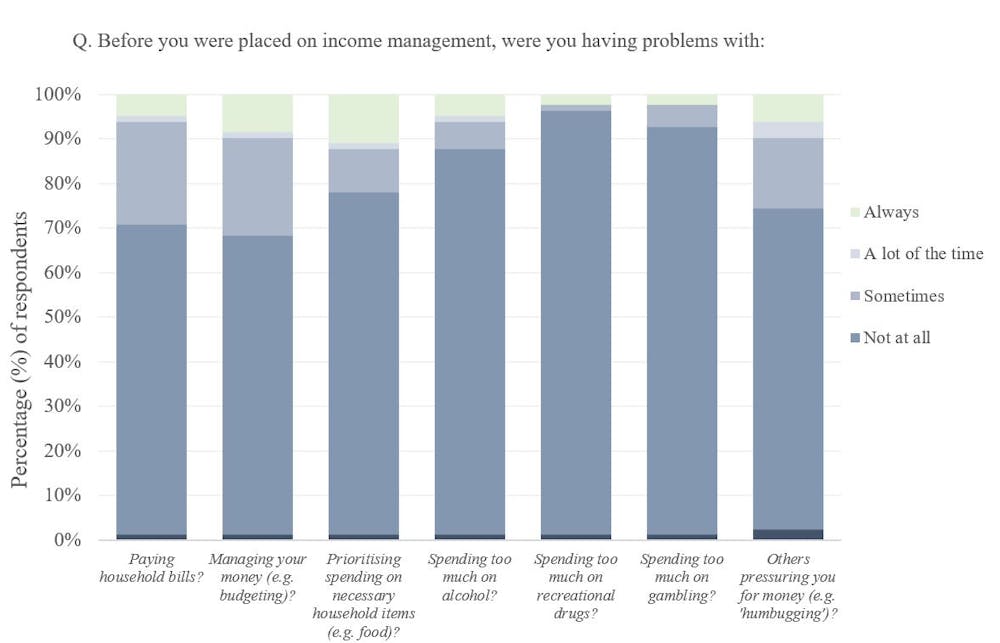

Our study found some individuals

experience these benefits. But most face extra financial challenges.

These include not having enough cash for essential items, being unable

to shop at preferred outlets, being unable to buy second-hand goods, and

cards being declined even when they are supposed to work.

Survey respondents reported a range of challenges related to compulsory income management.

Hidden Costs: An Independent Study into Income Management in Australia

In Playford, Jacob* told us about being on

the BasicsCard, which can only be used with merchants that have agreed

to not allow cardholders to buy excluded goods.

The limits on where he could shop made it harder for him to manage his finances.

“I couldn’t make decisions about saving

money,” he told us. He and his wife used to catch the train to shop at

the Adelaide markets, for example, but vendors there couldn’t take the

BasicsCard.

The Cashless Debit Card is intended to

overcome the limitations of the BasicsCard. It’s like a debit card

except it can’t be used to withdraw cash or at businesses that sell

prohibited items.

But Emma*, a single mother in the

Bundaberg and Hervey Bay area, told of her struggles to make basic

purchases using the card. It often failed – even at businesses that

purportedly accepted it – and her family went without. She also felt

excluded from the markets and second-hand retailers where she used to

shop.

Her greatest stress, however, was rent.

Emma* said she had always been on time with rental payments until the

Cashless Debit Card. She described one occasion when, two days after

paying the rent, the money “bounced back” into her account. When she

rang the card’s administrator (card payment company Indue), she was told: “It’s just a minor teething issue, just keep trying.”

The extra stress from “worrying about

which payments were going to get paid” was considerable. Others shared

similar experiences.

Social (dis)integration

Supporters of compulsory income management

claim it brings people back into the community by combating addiction

and encouraging pro-social behaviour and economic contribution. As

federal Attorney-General Christian Porter said in 2018:

“The cashless debit card can help to stabilise the lives of young

people in the new trial locations by limiting spending on alcohol, drugs

and gambling and thus improving the chances of young Australians

finding employment or successfully completing education or training.”

However, our study found the card can also

stigmatise and infantilise users – pushing people without these

problems further to the margins.

One of the problems is that compulsory

income management is routinely applied based on where a person lives and

their payment type, and not on any history of problem behaviour. The

large majority of our respondents indicated they did not have alcohol,

drug or gambling issues.

The majority of survey respondents had been managing finances well before compulsory income management.

Hidden Costs: An Independent Study into Income Management in Australia

But as Ray* in Ceduna explained, having the card meant others viewed him as a problem citizen.

I’m embarrassed every time I have to use

it at the supermarket, which is about the only place I do use it. I sort

of look around and see who’s behind me in the queue. I don’t want

anybody to see me using it.

This was a common experience across the interview sites.

Maryanne* in Shepparton told about being judged for shopping for groceries with her BasicsCard.

I got called a junkie and I said: ‘I’m not

a junkie, do you see any marks or anything?’ They were like: ‘No, but

you have a BasicsCard.’ I said: ‘What’s that got to do with it?

Centrelink gave it to me. I can’t do nothing.’

Stigma was a common concern among survey participants.

Hidden Costs: An Independent Study into Income Management in Australia

A path forward

The overwhelming finding from our study is

that compulsory income management is having a disabling, not an

enabling, impact on many users’ lives. As the policy has been extended,

more and more Australians with no pre-existing problems have been caught up in its path.

This does not mean a genuine voluntary

scheme could not be maintained, but it would need to sit alongside

evidence-based measures to tackle poverty.

Names have been changed to protect individuals’ privacy.

Authors: Greg Marston, Head of School, School of Social Science, The University of Queensland; Michelle Peterie, Research Fellow, The University of Queensland; Phillip Mendes, Associate Professor, Director Social Inclusion and Social Policy Research Unit, Monash University; Zoe Staines, Research fellow, The University of Queensland

Australia’s

first neobank, Volt,

is partnering with Australia’s largest global retailer, the Cotton On Group,

to introduce team members and customers to the Volt experience.

It

will be the first partnership of this type between a neobank and major retailer

in Australia, putting both companies at the forefront of digital innovation in

the retail banking sector and taking an important step to support the financial

literacy and good spending and saving habits of millennials.

Cotton

On team members, and in time Cotton On Perks members, will be introduced to the

Volt Savings Challenge in an effort to help them create better financial

habits. The Volt Savings Challenge encourages customers to set targets and

sends gentle reminders for weekly saving, tracking their progress over a 6 week

period by which time the savings ‘habit’ should be embedded behaviour.

According to Steve Weston, CEO & Co-Founder of Volt, the partnership is also heavily centered on a deep philosophical and values alignment between the two customer-focused companies.

CEO Steve Weston and the Volt Team

“Both

Volt and the Cotton On Group are built upon a foundation of delivering great

value to customers, a foundation that starts with a commitment to genuinely solve

customer pain points whilst dealing ethically and transparently with customers,

staff, and suppliers,” said Mr. Weston. “We feel really comfortable partnering

with a company that’s as customer-focused as we are.

“The

partnership will help us continue to show millions of Australians how to

quickly develop and improve their savings and spending habits with Volt. We

recently introduced to our waitlist a “no catches” 2.15 per cent variable

interest rate, which complements our savings challenges that are designed to

help people become financially healthy and masters of their own money.

“We

look forward to bringing this experience to many more Australians in the coming

years,” Mr Weston concluded.

The

Cotton On Group is partnering with Volt to bring a roadmap of innovation and

value to customers in Australia by introducing banking services tailored to

millennials that provide a supportive environment for healthy savings habits,

said Brendan Sweeney, General Manager, E-Commerce, who leads the Group’s digital

and loyalty strategy.

“Our

millennial team and customers are highly engaged, digital-first and have told

us that they are looking for trusted partners who can help them achieve their

financial goals,” said Mr. Sweeney.

“We

really like the Volt approach of simplicity, trust, and great value coupled

with a digital customer experience designed to help customers understand their

finances and achieve their goals. We look forward to making the Volt experience

available to our team members and customers over the coming months.”

The

Cotton On Group partnership follows others Volt has signed including PayPal.

The partnership strategy is an important element in delivering competition to

the banking sector.

Commonwealth

Bank has today launched X15 Ventures, an Australian technology venture

building entity, designed to deliver new digital solutions to benefit

Australian consumers and businesses.

X15

will leverage CBA’s franchise strength, security standards and balance

sheet to build stand-alone digital businesses which benefit from and

create value for CBA’s core business. CBA customers will benefit from a

broader range of solutions which complement the bank’s core product

proposition.

The bank will partner with Microsoft and

KPMG High Growth Ventures to deliver X15 Ventures. Microsoft will bring

its platform and engineering capability to the initiative, while KPMG

will provide advisory services.

CBA Chief Executive Officer Matt Comyn

said: “We remain focused on bringing together brilliant service with the

best technology to deliver exceptional customer outcomes in the core of

our business. X15 will enable us to innovate more quickly, and continue

to offer the best digital experience for our customers.”

X15 will be a wholly-owned subsidiary of

CBA, with funding provided from CBA’s $1 billion annual technology

investment envelope, its own delivery model, and a dedicated management

team. X15 will be headed by Toby Norton-Smith who has been appointed

Managing Director of X15 Ventures.

Mr Norton-Smith said: “X15 allows us to

open the door and partner more easily with entrepreneurs than ever

before. Under its umbrella, we will create an environment for new

businesses to flourish, we’ll empower Australia’s innovators and bring

new solutions to market designed to empower customers as never before.

“X15 businesses will be nurtured and

developed as start-ups but will have the scale and reach of CBA behind

them to achieve rapid growth. We are pleased today to be unveiling our

first two new ventures, Home-In, a digital home buying concierge, and

Vonto, a business insights aggregation tool. We intend to launch at

least 25 ventures over the next five years.”

Microsoft Australia Managing Director

Steven Worrall said: “Commonwealth Bank has always excelled in terms of

its technology vision and we have partnered with the bank for more than

20 years. Today’s announcement takes that innovation and transformation

effort to the next level with the launch of X15 Ventures. I believe that

the next wave of major technology breakthroughs will come from

partnerships such as this, bringing together our deep technical

capabilities and absolute clarity about the business challenges that

need to be addressed.”

Amanda Price Head of High Growth Ventures

KPMG said: “A performance mindset can be the difference between success

and failure for start-ups. We look forward to working with CBA and X15

Ventures to build the ecosystem of support these new ventures need. From

founder programs designed to unlock sustained high performance, to

business and strategy solutions for high-growth ventures, there will be a

wealth of smart tools at their disposal to help them overcome the

challenge of scaling at speed.”

Home-in, which is live for select

customers today, is a virtual home buying concierge that will simplify

the complex process of buying a home. Smart app technology helps buyers

navigate the purchase process more easily from end-to-end, leverage a

platform of accredited service providers like conveyancers and utility

companies, access tailored checklists and a dedicated home buying

assistant who will respond to queries with the touch of a button. More

information is available at www.home-in.com.au.

Vonto, launched today, is a free app

available to all small business owners, not matter who you bank with. It

draws data from Xero, Google Analytics, Shopify and other online

business tools and presents the data and analytics in one location,

allowing users to obtain a quick, holistic and rich view of their

business for ease and increased control. For more information on Vonto,

please visit: www.vonto.com.au.

Today I want to consider the social impact of going digital, and the problems associated with financial stability in a disaggregated digital payments world.

More evidence I think that banning cash is clueless.

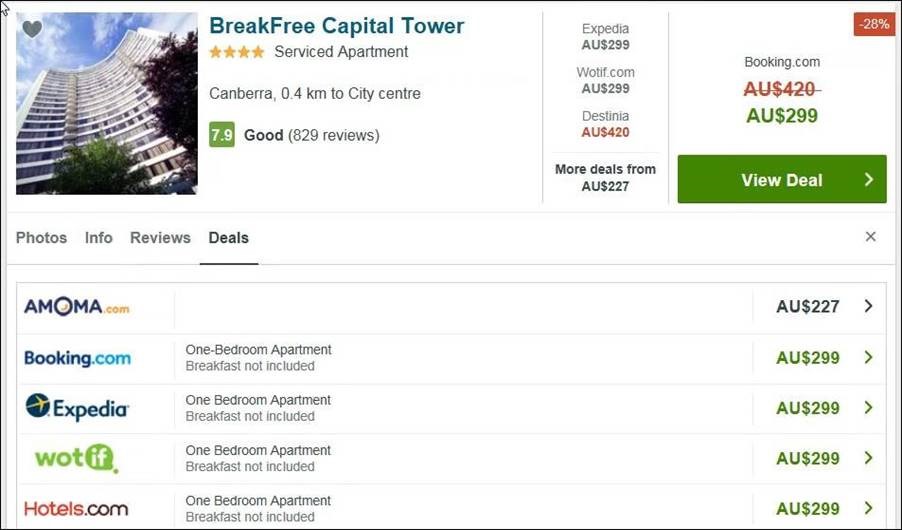

I have warned before of the hidden algorithms which means that some comparison site results may not be providing what you expect. Not impartial, objective and transparent price comparisons. Hence the release from the ACCC should be of no surprise! Trivago misled consumers about hotel room rates.

The Federal Court has found Trivago breached the Australian Consumer Law when it made misleading representations about hotel room rates both on its website and television advertising.

An example of Trivago’s online price display taken on 1 April, 2018. For example, the $299 deal is highlighted below, when a cheaper deal was available if a consumer clicked “More deals” (underneath the offers from other booking sites in the middle panel).

The Court ruled that from at least December 2016, Trivago misled consumers by representing its website would quickly and easily help users identify the cheapest rates available for a given hotel.

In fact, Trivago used an algorithm which placed significant weight on which online hotel booking site paid Trivago the highest cost-per-click fee in determining its website rankings and often did not highlight the cheapest rates for consumers.

“Trivago’s hotel room rate rankings were based primarily on which online hotel booking sites were willing to pay Trivago the most,” ACCC Chair Rod Sims said.

“By prominently displaying a hotel offer in ‘top position’ on its website, Trivago represented that the offer was either the cheapest available offer or had some other extra feature that made it the best offer when this was often not the case,” Mr Sims said.

The Court also found Trivago’s hotel room rate comparisons that used strike-through prices or text in different colours gave consumers a false impression of savings because they often compared an offer for a standard room with an offer for a luxury room at the same hotel.

“We brought this case because we consider that Trivago’s conduct was particularly egregious. Many consumers may have been tricked by these price displays into thinking they were getting great discounts. In fact, Trivago wasn’t comparing apples with apples when it came to room type for these room rate comparisons,” Mr Sims said.

The Court also found that, until at least 2 July 2018, Trivago misled consumers to believe that the Trivago website provided an impartial, objective and transparent price comparison for hotel room rates.

“This decision sends a strong message to comparison websites and search engines that if ranking or ordering of results is based or influenced by advertising, they should be upfront and clear with consumers about this so that consumers are not misled,” Mr Sims said.

A hearing on relief, including penalties, will be held at a later date.

Background

Trivago’s website aggregates deals offered by online hotel booking sites (like Expedia, Hotels.com and Booking.com) and hotel proprietors’ own websites for available rooms at a hotel and highlights one offer out of all online hotel booking sites (referred to as the ‘Top Position Offer’). However, Trivago’s own data showed that higher-priced room rates were selected as the Top Position Offer over alternative lower-priced offers in 66.8% of listings.

Trivago’s revenue was primarily obtained from cost-per-click (CPC) payments from online hotel booking sites, which significantly affected that booking site’s appearance and prominence in search results.

The ACCC has sought orders for penalties, declarations, injunctions and costs.

Banks have a central role in facilitating activity in modern economies. While that role is just as important today as it was prior to the financial crisis, the nature of banking has changed. And given developments in technology, data and competition, banking will need to continue to evolve. Today, I am going to discuss these changes in banking, past and prospective.

To put these changes in context, first I want to consider the special role that banks play in the

economy. I will then focus on how banks have changed in Australia since the financial crisis, and

outline some of the issues facing banks today that could see banking change in the coming years (my

remarks for Australia apply to all Authorised Deposit-taking Institutions, ADIs, but to fit with the

international literature I will use the term ‘banks’ and also because the word banks rolls

off the tongue more easily). While the Australian banking system remained well capitalised and

profitable through the financial crisis and by and large continued to service the economy, it was still

affected and the lessons learned internationally have resulted in important changes to Australian

banks.

What gives banks their special role?

Four characteristics jointly define why banks have a special role in the economy today:

they accept deposits, which become risk-free liquid assets for households and

businesses

they engage in maturity and liquidity transformation, using (mostly short-term)

liquid deposits and debt to make long-term illiquid loans

they play a central role in the payments system

they have expertise in credit and liquidity risk management, having a long history

and ongoing relationships that generate private information about customers.

The first three of these defining characteristics all relate to three key benefits that come from

public authorities. In particular, banks have: (i) the ability to accept deposits; (ii) an account at

the central bank; and (iii) access to emergency central bank liquidity. The three benefits provide banks

with a special role in the economy.

Bank deposits become a risk-free asset for households and business in Australia because they have an

effective government ‘guarantee’ (up to a limit) and receive the first claim on

banks’ assets.[1] Bank deposits are liquid because banks, in addition to the cash banks hold for

depositors’ physical withdrawals, have accounts at the central bank which enable their customers to

make direct payments to the customers of other banks.[2] It is because banks have accounts at the central bank

that they are central in the payments system. Further, even in tumultuous times, deposits are liquid

because of banks’ access to convert (potentially illiquid) assets into highly liquid deposits at

the central bank and, in the worst case, because the Financial Claims Scheme pays out deposits in a

timely manner. These policies give depositors the confidence that their deposits are safe and can be

withdrawn on demand.

These benefits help to mitigate the core risk of banking: maturity and liquidity transformation creates

the risk of a run. With access to stable deposits and central bank liquidity, banks are able to safely

do more maturity and liquidity transformation.

These three benefits go hand in hand with banks’ critical role in taking deposits and

intermediating and financing economic activity. Because of this role, banks are subject to prudential

regulation. Prudential regulation has benefits and costs. In economics, we typically try to equate

marginal costs and benefits when determining how much of something we should have.

From society’s perspective, prudential regulation has benefits in that it reduces the risks to

depositors and to the economy from bank failures. But there are also ‘costs’ to more

regulation, notably that it makes banks’ intermediation more expensive. To calibrate the optimal

amount of regulation, policymakers try to balance these costs and benefits.

We can also think of the costs and benefits of prudential regulation from the perspective of banks. For

banks, regulation can increase their costs. But it also provides banks with significant benefits. Even

in normal times, because they are prudentially regulated, banks can take in deposits that are a

relatively cheap source of stable funding. But the benefits are even greater in financial turmoil, when

having deposits that are relatively sticky and access to central bank liquidity is particularly

valuable.

The value of banks’ special role

Globally, the financial crisis delivered a severe shock to the banking system, and to the economy, that far exceeded what was generally thought likely or even possible. Before the crisis, it was widely thought that banks had become more sophisticated in managing their risk and that financial and macroeconomic volatility had declined. As a result, a severe financial shock was judged to be exceptionally unlikely. But then the financial crisis came along, which internationally resulted in bank failures and severe recessions. This led to a re-evaluation of how likely and extreme banking shocks could be. Globally, authorities recognised that the benefits of tighter prudential regulation – avoiding banking crises – would outweigh the costs.[3]

Similarly, from the banks’ perspective, it became apparent that the benefits that came with

their special role in the economy were even greater than previously appreciated, because shocks to the

financial system, and hence the impact on their balance sheets, could be more severe than was previously

thought likely. Indeed, in some countries the benefits of being a bank were so great that some non-banks

converted to being a bank to get those benefits.[4]

The international reassessment of banking regulation led to the ‘Basel III’ reforms. The

reforms focused on improving banks’ resilience, limiting banks’ maturity transformation and

ensuring that they improved their credit assessment and management of risk.

Recent changes in Australian banks

Despite the extreme shock globally, the Australian banking system performed remarkably well through the

crisis. In Australia, there was significant fiscal and monetary stimulus, and various measures were

enacted to support the banking system, and there was also a bit of luck. However, the good performance

of the Australian banks, to a large extent, reflected the strength of prudential regulation prior to the

crisis and banks’ own management of risks. But given the lessons learned internationally, it was

apparent that there were still improvements to be made in Australian banking.

The Basel III reforms have been adopted in Australia, on or ahead of schedule, strengthening a

prudential regime that was already tighter than global minimum standards. The reforms encouraged banks

to put greater emphasis on incorporating the cost of capital and liquidity into all aspects of their

operations.

Tier 1 capital ratios have increased by 50 per cent since 2006, with most of this being

CET1 capital (Graph 1). At current levels, banks’ Tier 1 capital ratios are

estimated to be well within the range that research has shown would have been sufficient to withstand

the majority of past international banking crises.[5]

Graph 1

A consequence of this has been a reduction in risk-taking. Banks sold some of their higher risk assets that were not providing sufficient rates of return. Notably, Australian banks have pulled back from international banking activity in the United Kingdom and Asia, where the returns had been disappointing and had often not met banks’ cost of capital (Graph 2). They also expanded their exposure to mortgage lending, which requires much less capital because of the collateral protecting these loans.[6] Most of the major banks have also sought to divest their life insurance and wealth management operations. These divestments were precipitated by changes in capital rules that required more capital to be held to support intra-group investments. But they also reflected that these investments had failed to deliver the anticipated benefits, including from cross-selling, and an appreciation of the non-financial risks that they involved.

The introduction of liquidity regulations – the Liquidity Coverage Ratio (LCR) and Net Stable

Funding Ratio (NSFR) – contributed to a substantial rise in the banks’ liquid asset

holdings, to around 20 per cent of total assets (from 15 per cent pre-crisis)

(Graph 1). The vast majority of this increase has comprised High Quality Liquid Assets (HQLA), in

particular, government securities.

The liquidity regulations contributed to a reduction in liquidity and maturity transformation. This has

substantially changed the composition of banks’ liabilities. Banks have significantly reduced their

use of (more flighty) short-term debt, while increasing their use of (sticky) domestic deposits

(Graph 2). By applying transfer pricing across their whole businesses, banks are now seeking to

ensure that all lending decisions take account of the extent of liquidity or maturity

transformation.

Graph 2

The regulatory changes and banks’ better recognition of financial risks and returns have restricted growth in Australian banks’ (headline) profits since 2014. The divestment of their wealth management businesses reduced total profits. However, even focusing on return on assets (ROA), profitability has declined by more than one-fifth since the financial crisis (Graph 3). Two important contributors have been the increased holdings of (safer but lower yielding) HQLA and a more general decline in risk-taking and hence reward. The fall in profitability has been even larger (about one-third) when measured by return on equity (ROE), because of the increase in banks’ equity outstanding.

However, the decline in profitability does not equate to reduced costs of financial intermediation for

customers. Rather, the spread between lending rates and funding costs (or the cash rate) has increased a

little. This combination of higher costs to customers and lower profits to banks reflects the

(anticipated) costs of tighter prudential regulation.[7]

Graph 3

Banks’ absolute cost of equity (COE) has also declined. The decline in absolute COE has, however,

been less pronounced than the fall in risk-free rates (Australian Government Security (AGS) yields). So

the risk premium on banks’ equity has actually risen. This is consistent with equity investors

having revised up their assessment of the riskiness of investing in banks, even as banks have been

forced to deleverage and hold more liquid assets.

Since ROE has fallen by more than COE, banks have become less valuable. One way to think about this is

that, since banks are now obliged to hold more equity (that is, they are less leveraged), they generate

a lower expected return on equity in excess of the risk-free rate. If the cost of financing a bank were

independent of the mix of debt and equity, that is, we lived in a world where the Modigliani-Miller

theorem held,[8] then issuing more equity would reduce the cost of the bank’s debt and equity, so

keeping the total cost of funding unchanged. There are many reasons why the Modigliani-Miller theorem

may not hold, including government protection of banks’ deposits. This means that deposits

don’t become less risky as the banks issue more equity, and so the cost of debt doesn’t

decline. But with the bank issuing more relatively expensive equity, the cost of funding banks rises

overall, which explains why they become less profitable when they are obliged to reduce their

debt-equity ratios.

Despite the decline in ROE, Australian banks continue to generate ROE well in excess of their

risk-adjusted COE. They trade at price-to-book ratios exceeding one, higher than banks in many other

countries around the world, highlighting the value that investors still see in Australian banks.

Prospective drivers of further change in Australian banks

While the past decade has seen substantial changes in banking in Australia, there are several issues

facing banks that could potentially lead to even greater change in coming years. The first is the

general increased access to, and ability to process, vast quantities of data. This is facilitating the

emergence of new, technology-driven competitors to banks which could potentially impact their dominant

position in the financial system.[9] A second is the impact of tighter regulation on banks. A third is

expectations for banks’ obligations to the community.

A substantial influence on banking at the moment is the rapid pace of technological change. We are

currently seeing a massive increase in the availability of, and ability to process, data. This could

erode, or maybe even eradicate, banks’ historical advantage in credit risk assessment. There are

two parts to this: regulatory changes mean that banks’ private customer data can be made available

to others and, second, that non-banks have some data that is useful for banking business.

The first part is the Consumer Data Right (CDR) and Open Banking. The CDR makes it clear that the

consumer owns their own data and Open Banking provides bank customers with the ability to share their

account data with other institutions, including non-banks.[10] Using these data, a non-bank could,

for example, suggest accounts or cards that better suit a customer’s needs or use the information

for detailed credit assessment. In addition, Comprehensive Credit Reporting (CCR) will provide (bank

and) non-bank lenders with greater information about potential borrowers’ credit history.[11]

The second part is non-banks’ data that are becoming more valuable for ‘banking’

services. Much of this data is collected by ‘big tech’ firms such as Google, Apple and

Facebook. For example, PayPal and Amazon have substantial data on the sales of their merchant customers,

while social networking interactions can be used to predict borrowers’ commitment to repay their

loans.[12] Technology firms for which collecting and analysing data is in their DNA are a new

type of competitor for banks that have historically struggled to take full advantage of the private data

they hold. How well individual banks respond to technology challenges will no doubt influence their

relative success.

Technological changes in payments are also challenging banks’ core role in facilitating payments.

To date, this erosion has been most apparent in emerging market economies where payments systems were

not meeting customers’ needs. For example, in China and several African countries, online

marketplaces or mobile phone companies have come to dominate payments (largely bypassing the banks).

However, in Australia, and other developed economies, existing electronic payment systems (including new

real-time payment systems such as Australia’s New Payments Platform (NPP)) are already meeting

customers’ needs. Still, new payments providers engaging with banks and card companies could reduce

the banking systems’ revenue from the payments system.

Where banks have provided poor service, such as in cross-border transfers, new competitors may capture

market share. This is already occurring with specialist firms undercutting the banks’ very wide

spreads in cross-border payments. Cross-border payments are also a potential entry point for

‘stablecoins’ which could be used to make low-cost payments across borders, completely

bypassing the banking system.[13]

A second issue for banks is the impact that tighter regulation has on the cost of intermediating

borrowing and saving. Tighter prudential regulations, such as holding more capital and liquid assets,

was anticipated by regulators to increase the cost of intermediation.[14] These expected higher costs were

taken into account in calibrating regulations and are judged to be appropriate given the reduced chance

of financial crises. But higher costs for banks can push more borrowing to non-bank financial

institutions or into capital markets. The share of credit intermediated by non-banks is currently small

in Australia and so there are limited implications for financial stability. But if it were to grow

significantly, we would have to carefully assess what this might mean for financial stability.

A third issue for banks comes from expectations in terms of their obligations to the community. Banks

will need to adapt to a range of reforms designed to strengthen governance and culture at financial

institutions. These should lead to less and better-managed non-financial risk. The measures include the

Banking Executive Accountability Regime (BEAR), the Australian Prudential Regulation Authority’s

(APRA) proposed standards for how variable remuneration is structured and the response required to

shortcomings identified by the Financial Services Royal Commission. While these measures require banks

to adapt, they will make banks more resilient, increasing their chance of responding to new

competitors.

Final remarks

Summing up, while banks are facing various challenges, their special role in the economy gives them

several advantages. Deposits are overall a lower cost, and stable, form of funding. And providing

depositors with a liquid asset puts banks at the centre of the payments system and gives them a

connection to customers.

Banks have adapted following the financial crisis. And they will need to continue to evolve given the

challenges they will continue to face in the coming years. Greater availability of data reduces one of

banks’ advantages. And changes in technology introduce a different type of competitor. For now, the

banking system remains core to modern economies. Australian banks in particular serve critical functions

in the Australian economy by providing credit intermediation and more generally facilitating economic

activity. Australian banks are profitable and resilient and a strong banking sector has contributed to

Australia’s extended run of economic growth. It’s hard to imagine a modern economy without a

banking sector. The eight largest Australian banks can trace their history back, on average, over

140 years. But what role today’s individual banks play in the provision of banking services in

the coming decades will depend on how they adapt to the challenges they face today.