IT Wire reports that New Zealand cryptocurrency exchange Cryptopia has suffered a breach and its operations have been locked down, with police saying that they are not yet in a position to indicate the quantum of the theft.

The company said in a notice on its site

that there had been “significant losses” but went no further, only

saying that “once identified, the exchange was put into maintenance

while we assessed damages”.

Cryptopia was set up in July 2014 and is based in Christchurch. It

has two directors, Adam Clark and Robert Dawson, according to Blockonomi, a site that covers cryptocurrencies, fintech and the blockchain economy.

The police statement said they were trying to establish what happened and how the site had been breached.

“A priority for police is to identify and, if possible, recover missing

funds for Cryptopia customers; however there are likely to be many

challenges to achieving this,” the statement said.

The website Crypto News cited

a tweet from the chief executive of Binance, another cryptocurrency

exchange, as saying some of the funds stolen from Cryptopia had been

frozen.

These funds had been moved to Binance by the individuals who carried out the hack.

The police statement said: “While police are unable to go into

details about specific steps being taken at this stage, we can say that

our focus includes commencing both a forensic digital investigation of

the company, and a physical scene examination at the building.

“We are dealing with a complex situation and we are unable to put a timeframe on how long the investigation may take.

“We are also aware of speculation in the online community about what

might have occurred. It is too early for us to draw any conclusions and

Police will keep an open mind on all possibilities while we gather the

information we need.”

Neobank Xinja is offering potential investors a chance to buy shares through an equity crowdfunding platform for the second time, via Australian Broker.

Xinja, which was recently granted a restricted banking licence, originally launched its first equity crowdfund in January 2018.

This most recent raise was opened early to existing investors,

customers and people who had registered interest, and it passed the

minimum of $500,000 in less than nine hours.

With shares available on equity crowdfunding platform Equitise, Xinja

chief executive and founder Eric Wilson said he was confident there

would be early and consistent interest from investors who wanted to help

shake up Australia’s banking system.

Wilson said the bank was now a step closer to delivering real competition in the local banking market.

“We are now working towards a full banking license from APRA in 2019

subject to regulatory approval [and] we have ambitious plans in place

for the years ahead.

“We’re all about making banking easy. We’re about banking technology

that more closely resembles what people expect from innovators and

disruptors, like Netflix or Uber, as opposed to old-style, bricks and

mortar-based banking.

“We want people to make better decisions about their money. Getting

them on board, as early shareholders, also helps us build a better

bank.”

As part of these plans, it has released a beta version for its Xinja home loans to friends and family.

The digital bank has an Australian Credit Licence and plans to roll

out home loans to the public alongside bank accounts, subject to

regulatory approval.

Co-founder of leading equity crowdfunding platform Equitise, Jonny

Wilkinson, said since the last raise Xinja has continued to receive

significant interest from investors, customers and the Australian

public.

He added, “Xinja hit the ground running with its first equity

crowdfund and interest continued to remain strong from previous and new

investors who were keen to know when the next raise would be.

“Xinja is a fantastic example of the power of equity crowdfunding

where ‘the crowd’ is given the opportunity to back a company they

believe in.”

Xinja will issue shares at $2.04 each, with a minimum parcel of $255

for each investor, with expectations of raising up to $5 million.

In its raise in 2018, Xinja reached its minimum funding goal within

18 hours, raising a total of $2.7million. It was pitched at $1.25 a

share and added more than 1,220 new investors to the Xinja share

register.

More than 23,000 people have signed up for the Xinja app and over

9,000 tap-and-go Xinja cards have been issued. The card is in use in 17

countries a day, on average.

An alternative to the big banks already exists and it isn’t in neobanks according to the chief executive of a mutual bank, via InvestorDaily.

Heritage Bank chief executive Peter Lock said that neobanks did not offer anything new to the banking system.

“Forget the hype about neobanks. There’s nothing that digital banks

and neobanks offer that customer-owned institutions such as Heritage

Bank don’t already offer to people frustrated by the listed banks,” he

said.

Mr Lock said that mutuals were tried and tested institutions who had

market-leading technology and weren’t owned by investors looking to turn

a profit.

“Unlike many neobanks, mutuals aren’t owned by big investors looking

to make a profit. If you’re turning to them to escape the

profit-maximisation excesses of the big banks, then you should think

again.

Mr Lock said that mutuals offered a different mindset to listed banks as they did not have profit maximisation incentives.

“Regardless of their rhetoric, the listed banks face an inherent

conflict between the interests of their customers and the interests of

their shareholders. At the end of the day, the listed model exists to

serve their shareholders above all else, not customers,” he said.

However, APRA’s general manager of licensing Melisande Waterford

defended new entrants to the market during a panel last year where she

said neobanks offered something new.

“Neobanks have a completely different mindset and a different approach to providing a service,” she said.

This mindset has proven to be popular with consumers as well according to recent data from Nielsen.

Nielsen’s latest data found a five-percentage point increase over

twelve months of Australians looking to switch to a digital bank.

Not only are Australian’s looking to switch to digital banks but 75

per cent of digital bank customers would recommend their bank to others,

compared to just 45 per cent of the big four.

GlobalData’s head of banking content for Asia-Pacific Andrew Haslip

said that conditions in Australia were ripe for neobanks given the lack

of trust in the industry.

“‘The clutch of neobanks waiting in the wings in Australia will have

no better time to launch recruitment drives, while a range of

robo-advisors, none of which have yet broken out into the mainstream,

will have the best conditions yet to draw in new money,” he said.

Recently neobanks like Volt and Xinja have been granted restricted

ADI licenses, making them one step away from a full banking licence.

Could new innovators create a wave of disruption in the banking sector? APRA’s new rules provides an on-ramp and players are already appearing. The high penetration of mobile devices offers potential, perhaps. This from Investor Daily.

On Tuesday (18 December), the prudential regulator announced that

Xinja Bank Limited has been officially authorised as a restricted

deposit-taking institution (RADI).

Xinja is only the second Australian neobank to receive this status.

Volt Bank was granted a RADI in May, literally days after APRA finalised

the framework, which was created in response to the government’s push

for greater innovation and new entrants to the banking industry.

However, as its name suggests, a restricted ADI licence has

significant limitations. A RADI is really a stepping stone on the

journey to acquiring a full banking licence. It allows neobanks like

Xinja and Volt to conduct limited banking capabilities for a maximum

period of two years while they develop their capabilities and resources.

It also gives them time to raise the significant levels of capital

required to meet APRA’s demands for a full banking licence.

RADI’s must hold a minimum $3 million in capital, or 20 per cent of

adjusted assets, and can only hold $2 million worth of customer

deposits. When you consider that Australia’s largest bank, CBA, holds

more than $150 billion in customer deposits, you get an idea of the

competitive dynamics at play here.

However, the royal commission has severely damaged the reputations of

the incumbent banks like CBA and customers are arguably more open to

alternative offerings. Neobanks like Volt and Xinja could be poised to

capture a decent share of the banking sector – provided they have their

ducks in a row.

Volt, led by former NAB and Barclays executive Steve Weston, is

arguably the frontrunner in the race to obtain the much-coveted full

banking licence. The speed at which Volt was able to secure a RADI is

worth noting. Investor Daily understands that the group has been working

tirelessly to secure a banking licence as soon as possible.

The word on the street is that Volt could be given full ADI status by

the end of the year after it brought in KPMG’s corporate finance team

to facilitate a capital raise of around $40 million.

Anyone looking to make a bet on whether or not a brand-new challenger

bank can succeed in a market as oligopolistic at Australia’s needs to

consider two things: how willing customers are to try them out and if

they have succeeded in other markets.

The customer demand is clearly there. The royal commission has

provided the perfect platform for neo-banks tell their story, which is

the antithesis of what we heard from the banks during the Hayne inquiry.

A quick look at Volt’s website shows the bank is tapping directly

into the complaints of Australian banking customers and addressing them

head-on.

“We’ll always give you honest recommendations to protect your money and your data,” the company promises.

“We’ll remove speed bumps and will use the best available tech to make things easy and simple.

“We’ll suggest ways to save you time and money, both when you borrow and when you spend.”

Where incumbents have been slammed for predatory lending tactics and

high credit card fees, neobanks are looking at ways to harness

technology to provide a disciplined approach to lending, saving,

spending and investing money. Responsibility is high on their agenda.

I’ve heard that one potential Volt Bank feature will allow customers to

set parameters that lock them out of their account for a 24-hour period

if they know they’ll be in a situation where spending could get out of

control, like a pub or casino.

Challenger banks have made significant inroads in the UK, which is

always a good market to follow for clues about what will happen in

Australia. Our British cousins were a few years ahead of us on mortgage

reform, macro prudential measures and the rise of the neobank.

Groups like Aldermore, Atom Bank, Metro Bank and Monzo have cropped

up since the GFC. Metro Bank launched in 2010, when the shocks of the

financial crisis were still being felt by many, and became the first new

‘high street’ bank to launch in Great Britain in over 100 years.

From a standing start less than a decade ago, the bank has grown

customer deposits to over £11.7 billion ($20.6 billion) and recorded

£16.4 billion ($28.8 billion) in asset in FY17.

While Metro Bank competes directly with the UK’s high street

incumbents like HSBC and Santander, Australia’s neo-banks will offer a

completely digital service.

With more and more Australians using their smartphone for everyday

banking, a simplified customer-friendly approach to financial services

could be the winning ticket for groups like Volt and Xinja. Particularly

as the majors face the challenging task of transforming from large,

slow-moving machines to nimble, more efficient operators.

Despite the moves last year, CBA has now confirmed that from next year Apple Pay will be available to CBA customers.

CBA says “When Tap & Pay is turned on, you can make purchases up to $100 by tapping the back of your phone against a PayPass reader. The transaction will work even if the phone is locked, turned off or if the battery has run out”.

The Commonwealth Bank appears to have thrown in the towel as far

as keeping Apple Pay out goes, and has said the payment option will be

made available to its own customers and those of Bankwest.

In a statement issued on Friday, the bank said this move constituted

part of its “commitment to becoming a better, simpler bank and providing

the best digital banking experience for our customers”.

The CBA, along with Bendigo and Adelaide Bank, National Australia

Bank and Westpac, attempted to cut a deal with Apple over Apple Pay, but

the Australian Competition and Consumer Commission last year denied them the right to negotiate collectively.

Subsequently, Bendigo and Adelaide Bank quietly adopted Apple Pay.

ANZ was not part of this cartel, and has been offering Apple Pay since April 2016.

No mention was made of the tussle in Friday’s statement. Angus

Sullivan, group executive of Retail Banking Services at CBA, said: “We

recently wrote to our customers asking them what the bank could do

differently and we received lots of excellent suggestions.

“One of the things we heard repeatedly from our customers is that

they want Apple Pay and we’re delighted to be making it available in

January 2019.

“We are committed to making changes that benefit our customers and

simplify our business. We will continue to look for more opportunities

to innovate and listen, to ensure our customers get the best experience

when they bank with us. Responding to customer demand for Apple Pay

underscores our commitment to becoming a better, simpler bank.

“Launching Apple Pay, alongside our No.1 rated CommBank app, will

ensure our customers have the very best mobile banking experience.”

A survey conducted by analyst group Telsyte in February indicated the CBA customers were likely to switch banks if their existing bank did not provide their choice of payment mechanism.

When CBA was asked at the time about the reaction from customers, a spokesman told iTWire:

“When customers consider who they want to bank with, they take into

account a number of factors. A bank’s digital banking and payments

offering is an important factor.

“Our award-winning CommBank app is the number one free banking app in

Australia, with 4.8 million CommBank app users able to take advantage

of its tools including Spend Tracker and PayID.”

Jennifer Bailey, Apple’s vice-president of Internet Services, said on

Friday: “Apple Pay is the No.1 mobile contactless payment service

worldwide and we are thrilled Commonwealth Bank customers will soon be

able to benefit from a convenient and secure way to pay using the Apple

devices they love or within their favourite apps or on the Web.”

It remains to be seen what Westpac and NAB will do with regards to Apple Pay. All four of the big banks offer Samsung Pay and NAB last month signed an agreement with Alipay to make the service available in 2019.

Nearly 170 years before the invention of Bitcoin, the journalist

Charles Mackay noted the way whole communities could “fix their minds

upon one object and go mad in its pursuit”. Millions of people, he

wrote, “become simultaneously impressed with one delusion, and run after

it, till their attention is caught by some new folly more captivating

than the first”.

His book Extraordinary Popular Delusions and the Madness of Crowds,

published in 1841, identifies a series of speculative bubbles – where

people bought and sold objects for increasingly steep prices until

suddenly they didn’t. The best-known example he cites is the tulip mania

that gripped the Netherlands in the early 17th century. Tulip bulbs

soared in value to sell for up to 25,000 florins each (close to A$45,000

in today’s money) before their price collapsed.

The Bitcoin bubble surpasses this and all

other cases identified by Mackay. It is perhaps the most extreme bubble

since the late 19th century. In four years its price surged almost

2,800%, reaching a peak of US$19,783 in December 2017. It has since

fallen by 80%. A month ago it was trading at more than US$6,000; it is

now down to US$3,500.

That’s still a fantastic gain for anyone who bought Bitcoin before

May 2017, when it was worth less than US$2,000, or before May 2016, when

it was worth less than $500.

But will it simply keep dropping? What makes Bitcoin worth anything?

To begin to answer this question, we need to understand what creates

the values that drive speculative price bubbles, and then what causes

prices to plunge.

The above chart shows the magnitude of the Bitcoin bubble compared

with the price movement of Japanese property and dot-com bubble from

four years prior to their peak until four years after.

When asset values diverge

We typically think about bubbles in financial assets such as stocks

or bonds, but they can also occur with physical assets (such as

property) or commodities (like tulip bulbs).

A bubble begins when the price people are willing to pay for something deviates significantly from its “intrinsic value”.

The intrinsic value of an asset is theoretical, based its

“fundamental” value. Fundamental value includes: the ability to generate

cash flow (e.g. interest or rental income); scarcity or rarity value

(e.g. gold or diamonds); and potential use (e.g. silver and platinum are

used in both jewellery and industrial operations).

A house may have fundamental value owing to the scarcity of land, its

use as a home, or its ability to generate rental income. A tulip (or

Bitcoin) has none of those things; even the presumed scarcity does not

exist when you consider all of the alternative flowers (or

cryptocurrencies) available.

A bubble tends to occur after a sustained period of economic growth,

when investors’ get used to the price an asset always increasing and

credit is easily accessible.

To these conditions something more must be added for a bubble to

form. That is typically a major disruption or innovation, such as the

development of a new technology. Think of railways in the 19th century,

electricity in the early 20th century, and the internet at the end of

the 20th century.

Initially most investors tend to be cautious and “rational” about a

new technology. For instance, early investment in railways took

advantage of limited competition and focusing on profitable routes only.

It was gradual and commercially successful.

This creates higher growth and profitability, leading to positive

feedbacks (from greater investment, higher dividend payouts, and

increased consumer spending), which raises confidence further.

If conditions allow, this develops into a period the economic historian Charles Kindleberger described as “euphoric”: investors become fixated on the ability to make a profit by selling the asset to a “greater fool” at an even higher price.

South Cryptocurrency values are

displayed in the Seoul shopfront of Bithumb, South Korea’s leading

cryptocurrency exchange, in January 2018.

Jeon Heon-Kyun/EPA

That is, they are attracted not by “fundamental” motives – the

benefits from potential cash-flows such as dividend or rental income –

but by “speculative” motives – the pursuit of short-term capital gains.

Higher prices attract a greater number of speculators, pushing prices

higher still. Uncertainty around the significance of the new technology

allows extreme valuations to be rationalised, although the

justifications seem weaker as prices rise further.

The virtuous cycle of ever-rising prices continues, often fuelled by

credit, until there is an event that leads to a pause in price rises.

Kindleberger suggests this can be a change in government policy or an

unexplained failure of a firm.

When asset prices stop rising, investors who have borrowed to finance

their purchases realise the cost of interest payments on their debt

will not be offset by the capital gain to be made by holding onto the

asset. So they cut their losses and start to sell the asset. Once the

price starts falling, more investors decide to sell.

Bitcoin’s bubble

The possible triggers for a pause in Bitcoin price rises included

concerns about increased government regulation of crypto-assets and the

possibile introduction of central bank digital currencies, as well as

the large theft of assets and collapse of exchanges that have dogged Bitcoin’s short history.

Going down

In liquid markets such as stocks (where it is inexpensive to buy and

sell assets in large values) the price decline can be steep. In illiquid

markets, where assets cannot easily be sold for cash, the fall can be

brutal. Examples include the mortgage-backed securities (MBS) and

collateralised debt obligations (CDOs) that led to the Global Financial

Crisis.

Bitcoin is particularly illiquid. This is due to a large number of different Bitcoin exchanges competing; often substantial transaction costs, and constraints on the capacity of the Blockchain to record transactions.

A Bitcoin ‘mine’ in China. Miners

are rewarded with new currency for solving the complex math problems

required to validate and record Bitcoin transactions. It requires a

massive amount of computer-processing power.

Liu Xingzhe/Chinafile/EPA

The aftermath

The aftermath of a bursting bubble can be brutal. The stock market

crash of 1929 was a prelude to the Great Depression of the 1930s. The

collapse in Japanese asset values after 1989 heralded a decade of low

growth and deflation. The dot-com crash of 2000-01 destroyed US$8

trillion of wealth.

The effect of a crash depends the size, ownership and importance of

the asset involved. The effect of the tulip crash was limited because

tulip speculations involved a relatively small number of people. But

sharp declines in property values during 2007 led to the worst financial

crisis since the Great Depression.

Bitcoin is more like tulips. The entire market valuation was about

US$300 billion at the peak. To put this into context, the US stock and

housing markets are currently valued more than US$30 trillion each (the

equivalent Australian markets are valued at A$2 trillion and A$6.9

trillion respectively). Relatively few investors own the majority – it

is estimated that 97% of all Bitcoin are owned by just 4% of users. This suggests the effects on the wider economy of the Bitcoin crash should be contained.

Estimating Bitcoin’s intrinsic value

Obtaining a realistic estimate of Bitcoin’s intrinsic value is tricky

because it is not an asset that generates a periodic cash flow, such as

interest or rental income.

This does not provide a positive story for Bitcoin. Though the total

number of Bitcoins is limited, there are many competing, virtually

indistinguishable cryptocurrencies (such as Ehtereum and Ripple).

Bitcoin also fails to meet the criteria of a currency.

Its the price movements are too volatile to be a unit of account. The

transaction capacity of the Blockchain is too limited for it to be a

medium of exchange. Nor does it appear to be a good store of value.

For such an asset, value ultimately depends on what others are willing to pay for it. This often relates to scarcity.

Since it produces no income, has limited scarcity value, and few

people are willing to use Bitcoin as currency, it is even possible that

Bitcoin has no intrinsic value.

Author: Lee Smale, Associate Professor, Finance, University of Western Australia

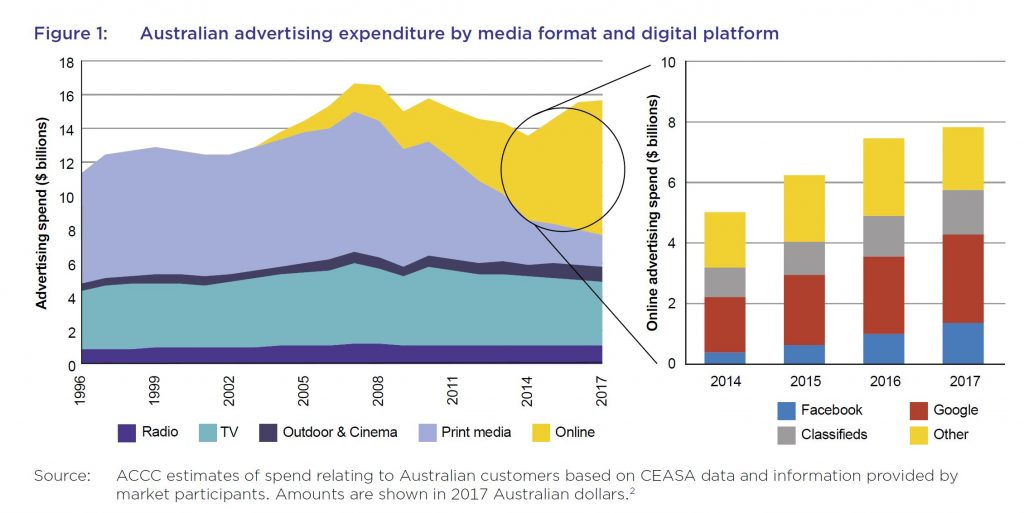

The issues raised are significant and far reaching, and questions the substantial market power players such as Google and Facebook have, the data they capture and monitise and their impact on the media. 94 per cent of online searches in Australia currently performed through Google.

Facebook and Instagram together obtain approximately 46 per cent of Australian display advertising revenue. No other website or application has a market share of more than five per cent.

They say there is a lack of transparency in the operation of Google and Facebook’s key algorithms, and the other factors influencing the display of results on Google’s search engine results page, and the surfacing of content on Facebook’s News feed.

Anti-competitive discrimination by digital platforms in favour of a related business has been found to exist in overseas cases. For example, in the European Commission’s 2017 decision, Google was found to have systematically given prominent placement to its own comparison shopping service (Google Shopping) and to have demoted rival comparison shopping services in its search results.

Monopoly or near monopoly businesses are often subject to specific regulation due to the risks of competitive harm. The risk of competitive harm increases when the monopoly business is vertically integrated. The ACCC considers that Google and Facebook each have substantial market power and each have activities across the digital advertising supply chain. Google in particular occupies a near monopoly position in online search and online search advertising, and has multiple related businesses offering advertising services.

This is their executive summary:

On 4 December 2017, the then Treasurer, the Hon Scott Morrison MP, directed the Australian Competition and Consumer Commission (the ACCC) to hold an inquiry into the impact of online search engines, social media and digital content aggregators (digital platforms) on competition in the media and advertising services markets. The ACCC was directed to look at the implications of these impacts for media content creators, advertisers and consumers and, in particular, to consider the impact on news and journalistic content.

Digital platforms offer innovative and popular services to consumers that have, in many cases, revolutionised the way consumers communicate with each other, access news and information and interact with business. Many of the services offered by digital platforms provide significant benefits to both consumers and business; as demonstrated by their widespread and frequent use by many Australians and many Australian businesses.

The ACCC considers, however, that we are at a critical point in considering the impact of digital platforms on society. While the ACCC recognises their significant benefits to consumers and businesses, there are important questions to be asked about the role the global digital platforms play in the supply of news and journalism in Australia, what responsibility they should hold as gateways to information and business, and the extent to which they should be accountable for their influence. In particular, this report identifies concerns with the ability and incentive of key digital platforms to favour their own business interests, through their market power and presence across multiple markets, the digital platforms’ impact on the ability of content creators to monetise their content, and the lack of transparency in digital platforms’ operations for advertisers, media businesses and consumers.

Consumers’ awareness and understanding of the extensive amount of information about them collected by digital platforms, and their concerns regarding the privacy of their data, are also critical issues. There are also issues with the role of digital platforms in determining what news and information is accessed by Australians, how this information is provided, and its range and reliability.

Digital platforms are having a profound impact on Australian news media and advertising. The impact of digital platforms on the supply of news and journalism is particularly significant. News and journalism generate broad benefits for society through the production and dissemination of knowledge, the exposure of corruption, and holding governments and other decision makers to account.

It is important that governments and the public are aware of, and understand, the implications of the operation of these digital platforms, their business models and their market power.

The ACCC’s research and analysis to date has provided a valuable understanding of the markets that are the subject of this Inquiry, including information that has not previously been available, and has identified a number of issues that could, or should, be addressed. Many of these issues are complex.

The ACCC has decided that the best way to address these issues in the final report, due 3 June 2019, is to identify preliminary recommendations and areas for further analysis, and to engage with stakeholders on these potential proposals. Such engagement may result in considerable change from the ACCC’s current views, as expressed in this report.

ANZ chief executive Shayne Elliott has conceded that branches are losing their lustre as cash becomes a niche payment solution and consumers opt to bank online, via InvestorDaily.

Counsel assisting Rowena Orr asked why the major bank has been reducing its retail footprint during Mr Elliott’s time on the stand at the royal commission this week.

Mr Elliott estimated 35 ANZ branches closed this year and up to 50 had ceased operating last year.

ANZ has closed around 110 branches in the past decade: 55 in inner regional Australia, 44 in outer regional areas, six in remote locations and four in very remote areas.

Mr Elliott noted that some branches had also opened in that time, describing it as a redistribution of its network.

“Why so many branches this year, Mr Elliot?” Ms Orr asked.

“Well, consumer behaviour is changing very quickly. And not that it has changed just this year but over the last few years we’re seeing a number of fundamental changes,” Mr Elliott said.

“The Reserve Bank governor the other day referred to the fact that the usage of cash is almost becoming a niche payment solution.”

Mr Elliott added that most of what people are doing in branches is cash related, in deposits and withdrawals. He also noted a decrease in retail traffic of around 20 to 30 per cent over the last couple of years in areas where the bank had closed shops.

However, small business usage was said to remain reasonably solid.

“So essentially, we are confronted with a dilemma where we have shops and a distribution network with less and less people in it, and therefore, at some point they become uneconomic,” he said.

“At the same time, what we have seen is a rapid increase in the use of technology for people who prefer to do their banking on their phone or at home, or even in some cases, on the phone.”

Ms Orr asked if people still go into branches to inquire about loans.

“Yes, perhaps, although I would say for ANZ – and we may be different from our peer group – our home loan book only – less than a third of home loans are originated through a branch,” Mr Elliott said.

“Around 55 per cent come through brokers and another roughly 15 per cent come through our mobile banking network, ie, we send somebody to you. So the branch network is not a terribly efficient or well-used avenue for home loans.”

ANZ had considered two proposals with closing branches, one to sell and the other to continue with a branch by branch closure program. Mr Elliott said the organisation had chosen to continue with closures based on customer behaviour and impact data.

Mr Elliott was also asked about the considerations that ANZ takes into account during branch closures. He responded by saying the bank does not consider the financials of the branch, rather the transactions that are available in the area and local alternatives in close by branches and ATMs.

“There’s very little correlation between what happens in the branch and the economic outcome to the bank. What most people do in a branch drives very little value,” he said.

“We don’t charge fees for most of what they do. It is a service that is not necessarily correlated to where we generate our profits or earnings.”

He added that delinkage is accelerating, with more people using brokers.

ANZ’s attitude towards its retail banking division is in stark contrast to that of its largest competitor, CBA.

When CBA boss Matt Comyn gave evidence before the Hayne inquiry last week he made clear the group’s preference for consumers to use its extensive branch network.

Mr Comyn revealed that CBA had sought to introduce a “flat fee” commission-based model in January 2018, before choosing not to go ahead with the change in fear that the rest of the sector would not follow suit.

MFAA CEO Mike Felton said that CBA’s position was “not surprising”, but was “entirely self-serving” and was “designed to destroy competition and reduce the bank’s reliance on the broker channel”.

Commenting on CBA’s attempt to introduce a flat-fee remuneration model, Mr Felton said: “CBA’s model is anti-competitive and designed to drive consumers back into their branch network, which is the largest branch network of the major lenders.

“Mr Comyn’s solution for better customer outcomes is a new fee of several thousand dollars to be paid by consumers to CBA for the privilege of becoming a CBA customer.”

Mr Felton added: “Cutting what brokers earn by two-thirds would save CBA $197 million, which is good for CBA’s shareholders. However, it would destroy competition, leaving millions of customers without access to credit outside of major lenders.”

He suggests a turning point has been reached. It is now easier than it has been to conceive of a world in which banknotes are used for relatively few payments; that cash becomes a niche payment instrument.

This morning I would like to speak about the shift towards electronic payments; or as the title of my remarks says, the journey towards a near cashless payments system. For some decades, people have been speculating that we might one day go cashless – that we would no longer be using banknotes for regular payments and that almost all payments would be electronic. So far, this speculation has been exactly that – speculation. But it looks like a turning point has been reached. It is now easier than it has been to conceive of a world in which banknotes are used for relatively few payments; that cash becomes a niche payment instrument.

Given this, I would like to structure my remarks around three broad points.

The first is that the shift to electronic payments is occurring quite quickly and it is likely to continue. This shift is a positive development that should promote our collective welfare.

The second is that if we are to realise the benefits of moving to a near cashless payments system, the electronic system needs to offer the functionality, safety and reliability that people require. People need to have confidence that the electronic payment system will be operating when they want to make their payments and that it will deliver the payment services that they need.

The third point is that as we undertake this journey towards a near cashless payment system, there will be a greater focus on the cost of electronic payments. If almost all payments are electronic, then the cost of making these payments matters more than it used to. The electronic system needs to be as efficient as it can be and to be characterised by strong competition. In my view, there is further work to be done here.

1. The Shift to Electronic Payments

The Reserve Bank conducts regular surveys of how Australians make their payments. The next survey will be undertaken in 2019. Until then, perhaps the best illustration of the declining use of cash for transactions is the sharp decline in the number and value of cash withdrawals through ATMs (Graph 1). Around the turn of decade, Australians went to an ATM, on average, around 40 times per year. Today, we go to an ATM around 25 times a year and the downward trend is likely to continue.

Graph 1

At the same time as the use of cash for payments has been declining, the number of electronic transactions has been growing strongly (Graph 2). Today, Australians make, on average, nearly 500 electronic payments a year, up from around 100 per year around the turn of the century.

Graph 2

New payment technologies are being developed that will further encourage this shift to electronic payments. Perhaps the most significant of these is the New Payments Platform, which has made it possible for people to make real-time person-to-person payments without using banknotes. A range of payment apps are also under development that would have the same effect. So the direction of change is clear.

There also continues to be a decline in the use of cheques (Graph 3).[1] In the mid 1990s, Australians, on average, made around 45 cheque payments per year. Today, we make around three per person. Given this trend is likely to continue, it will be appropriate at some point to wind up the cheque system, given the high fixed costs involved in operating the system. We have not reached that point yet, but it may not be too far away. Before we do, it is important that alternative payment methods are available. Progress has been made on this front, but more is required.

Graph 3

It is worth pointing out that despite the decline in cash use, the value of banknotes on issue, relative to the size of the economy, is close to the highest it has been in fifty years. For every Australian there are currently around thirty $50 and fourteen $100 banknotes on issue (Graph 4).

Graph 4

So there is an apparent paradox between the declining use of cash and the rising value of banknotes on issue. The main explanation is that some people, including non-residents, choose to hold a share of their wealth in Australian banknotes. The opportunity cost of doing this is less than it used to be because of the low level of interest rates.

While it is difficult to predict the future, I expect that banknotes will remain part of our payments system for some time to come.

In some situations, paying with banknotes is quicker and more convenient than paying electronically, although this advantage is less than it once was. Some people also simply prefer paying in cash – our 2016 survey indicated that around 14 per cent of Australians had a preference for using cash as a budgeting tool.

Banknotes also allow payments to be made anonymously in a way that is not possible in systems that leave an electronic fingerprint. This privacy aspect is valued by some people. In some circumstances this desire for privacy is entirely legitimate, but in others it has more to do with tax evasion and illegal activities.

Perhaps a more important source of ongoing demand is the fact that using cash does not require the internet to be up, electricity to be working and the banks’ systems to be operational. Banknotes are therefore an important emergency or back-up payment instrument. They are particularly useful in the event of natural disasters or failure of the electronic system. Perhaps one day the various systems will be so reliable that a backup will not be needed, but that day still seems some way off.

Overall, the shift to electronic payments that is occurring makes a lot of sense – it is similar to other aspects of our lives where things that used to be physical have been supplemented with, or replaced by, technology. This shift is likely to promote our collective welfare. I say that even though the Reserve Bank is the producer of banknotes and earns significant income, or as it’s known, seigniorage, for the taxpayer from their use. The greater use of electronic payments can bring efficiency benefits, with lower costs and more functionality and choice for users. One example of this is the reduced tender time involved in card transactions due to contactless technology. There are also non-trivial production and distribution costs involved in the cash system. Some of these are fixed costs, so the average cost of cash transactions is likely to rise as the volume of cash transactions falls. Looking ahead, there is also more limited scope for fundamental innovation in the cash system compared with the scope for dynamic innovation in electronic payments. So this journey is in our national interest.

2. Functionality, Safety and Reliability

I would now like to discuss three interrelated factors that will influence how quickly we undertake that journey. These are: the functionality offered by the electronic system; the safety of that system, and the reliability of that system. The other factor that is also relevant is cost, and I will touch on this a little later.

Functionality

The rapid adoption of contactless payments in Australia shows that Australians change how they pay quite quickly when new functionality is offered. Contactless card payments were slow to take off but once critical mass was established, they grew very quickly. In our 2013 consumer payment study they accounted for around over 20 per cent of point of sale card payments; three years later they accounted for over 60 per cent. So the functionality of the electronic payments system is key.

The development of the electronic payment system took a major step forward earlier this year with the launch of the New Payments Platform (NPP). This system allows people to make payments 24 hours a day, 7 days a week, using just a simple identifier such as a mobile phone number or an email address. It also allows a lot of information to accompany the payment. I expect that over time this extra functionality will further reduce the use of cash in the economy and also improve the efficiency of the electronic system.

The number of transactions through the NPP is steadily increasing (Graph 5). After a relatively low-key start, there are now around 400,000 NPP transactions per day. Over 2 million PayIDs have also been registered, and we expect further growth as the banks continue to roll out services to their customers.

Graph 5

The concept behind the NPP is that so-called ‘overlay’ services are developed, and that these overlay services offer new functionality that utilise the real time capability of the NPP. The first overlay service provides for a basic account-to-account payment. Among the subsequently planned overlay services are ones that will allow someone to send a request to pay, perhaps to a friend for their share of a meal out. Another overlay service would allow a link to a document to be sent with a payment; this could be a payslip or a detailed record of the transaction.

It was originally anticipated that these two overlay services would be up and running not long after the NPP launch. Unfortunately, this timeline has slipped. A number of the major banks have also been slower than was originally expected to roll out NPP functionality to their entire customer bases. This is in contrast to the capability offered by smaller financial institutions, which from Day 1 were able to provide their customers with NPP services. Given the slow pace of roll-out by the banks, and the prospect of delays for additional overlay services, I recently wrote to the major banks on behalf of the Payments System Board seeking updated timelines and a commitment that these timelines will be satisfied. It is important that these commitments are met.

It is worth observing that in other countries where banks have been slow to develop payment applications that meet the needs of the public, other possibilities emerge. China is perhaps the best example of this, with the emergence of QR-code-based payments. I expect that the NPP infrastructure will be the backbone of our electronic payments system for many years to come. But for this to be the case, the system will need to provide the functionality that people require, and it will need to do this on a timely basis.

There are a range of fintech firms that are excited by the capabilities offered by the NPP and the potential for it to be used for innovative payment solutions. In October, the RBA issued a consultation paper seeking views on the functionality and access arrangements for the NPP. In particular we are interested in views on whether the various ways of accessing the NPP, and their various technical and eligibility requirements, are adequate for different business models.

A topic that I get asked about from time to time is whether the functionality of the electronic system would be enhanced by the RBA issuing an electronic version of the Australian dollar, an eAUD. I spoke about this issue at this conference last year, concluding that we did not see a public policy case for moving in this direction at the time. In particular, it is not clear that RBA-issued electronic banknotes would provide something that account-to-account transfers through the banking system do not, particularly with the emergence of the NPP. Another important consideration was the implications for financial stability. A year on, our views have not changed.

Security

A second important influence on the rate at which we shift to a more electronic payments system is the public’s confidence in the security of the system.

Given this, a recent focus of the Payments System Board has been the high and increasing level of fraud in card-not-present transactions (Graph 6). Card-not-present fraud rose by 15 per cent in 2017 and now represents 87 per cent of total scheme card fraud losses.[2] In contrast, the industry has had successes in addressing card-present fraud, with the introduction of chip technology and the switch to PINs. Despite this, growth in e-commerce activity has provided new opportunities for would-be fraudsters.

Graph 6

The Payments System Board identified the rise in card-not-present fraud as a priority for the industry. In August this year, the Board was pleased to welcome AusPayNet’s publication of a draft industry framework to mitigate card-not-present fraud, and supports continued collaboration on this issue.

A separate but not unrelated priority for the industry is to progress work on digital identity. This is another area where barriers to effective coordination can arise. I am pleased that AusPayNet is undertaking work here, under the auspices of the Australian Payments Council. Digital identity is likely to become increasingly important as more and more activity takes place online. The RBA is highly supportive of industry collaboration on this issue and views it as important that substantive progress is made.

More broadly, individuals, businesses, governments and financial institutions all need to be aware of cyber risks. In the RBA’s most recent Financial Stability Review we noted the increasing sophistication of cyber attacks and that regulatory authorities have increased their focus on cyber issues.

Reliability

A third factor is the confidence that people have that they will be able to use the electronic system when they need to make their payments. As I noted earlier, people will still want to hold and use banknotes if they can’t be sure that the electronic system will be available when they need it. In our consumer payments survey in 2016, we asked people about why they held cash in places outside of their wallet. The most common response, from nearly half of respondents, was that it was for emergency transaction needs.

Over recent times, there have been a number of serious operational incidents that have interrupted the payments system. On some occasions these have been caused by problems with the telecommunications companies and at other times by problems at the banks. An operational incident at the RBA in August as a result of problems with a routine fire test also saw a number of RBA core systems unavailable for some hours, including the Fast Settlement Service supporting the NPP.

We all need to do better here. As we rely less on cash, outages affecting retail transactions can have a significant impact on businesses and individuals. So continued effort needs to be made by all participants in the payments system to reduce operational problems. If this does not happen, then it is possible that the Payments System Board could consider setting some standards.

3. Increased focus on Cost and Competition

My third broad point is about the cost of electronic payments and the importance of competition.

As we move to a predominantly electronic world, there will be more focus on the cost of operating the electronic payments systems and how those costs are allocated between those making and receiving payments.

Looking forward, I expect that over time the cost of electronic payments will decline further, due to both advances in technology and economies of scale. Even so, there are significant costs to operate the electronic systems, including costs for front- and back-end systems to maintain accounts, and to deliver functionality and convenience to users, as well as costs in preventing fraud and ensuring resilience. How these costs are managed and who pays for them will have a significant bearing on the efficiency of the overall system.

In terms of card payments, merchants in Australia currently pay less than merchants in many other countries. The comparison with the United States is particularly stark (Graph 7). For credit cards, Australian merchants, on average, pay 0.8 per cent of the transaction value for Mastercard/Visa transactions. In the United States the figure is much higher at around 2.2 per cent. There are also differences in the cost of debit cards and American Express cards between the two countries.

Graph 7

The main reason for the lower merchant costs in Australia is our lower interchange fees. These fees were reduced in Australia as a result of regulation by the Reserve Bank commencing in 2003. The RBA’s reforms reduced average interchange fees in the Mastercard and Visa systems by around 45 basis points. This has been reflected in merchant service fees; indeed, these merchant fees have fallen by somewhat more than the cuts to interchange, likely reflecting an increased focus on card acceptance costs by merchants (Graph 8). In addition, as a result of competitive pressure, including from the removal of no-surcharge rules, fees on American Express and Diners Club have also fallen over time.

Graph 8

Notwithstanding the reduction in interchange fees, these fees still represent, on average, around 60 per cent of the total merchant service fee on credit cards. So they remain an important part of the total cost to merchants. Conversely, these fees mean that the cardholder’s bank gets paid each time the card is used. This has meant that the cost to consumers of using these cards is often low; in some cases, cardholders are actually subsidised to use their card, through reward points and/or interest-free credit. The subsidy is provided by the cardholder’s bank, but ultimately paid for by the merchant.

The close link between interchange and merchant costs means that there continues to be significant focus on interchange and its implications for the distribution of costs between merchants and consumers. For example, there have been recent recommendations from the Black Economy Taskforce and the Productivity Commission for the Reserve Bank to consider regulatory action to lower, or even ban, interchange fees. The Payments System Board will again examine the arguments for lower interchange fees when it next conducts a formal review of the card payments system.

On the competition front, one area that merits close attention is the market for acquiring services. This has come into sharper focus as a result of concerns about the costs to merchants in the debit card system, where most cards allow for transactions to be processed by either of the two networks enabled on the card. The longstanding view of the Payments System Board has been that merchants should at least have the choice of sending the debit payment through the lower cost system, whether that be eftpos or the international scheme.

For merchants to be able to do this though, acquirers need to offer terminals and technical systems enabled to allow least-cost routing. Some acquirers have already completed the necessary work and are attracting new merchants. Others, including the major banks, made commitments earlier in the year regarding the timetable for this work to be completed. Partly on the basis of those commitments, the Payments System Board made a decision not to regulate. Since then, I regret to say there has been slippage by some, who have cited technical problems. It is important that the banks get back on track here. A failure to deliver on commitments or to provide the payment services that the community needs will inevitably lead to calls for further regulation.

4. Looking ahead

Looking beyond interchange and acquiring competition, new technologies open up the prospect of new payment options developing. Recently, there has been much discussion on the role that so-called ‘Big Tech’ firms might eventually play.

These firms have potential advantages over existing providers of payments services. In some cases, their technology and systems are more flexible, they have a greater ability to use and process information, they have well established networks which they can leverage and they are often better at interacting with their users and customers. Given this, one scenario is that these firms become significant players in the payments industry. They might be able to do this through developing new payment applications that provide a commercial return, not through charging for payment services, but by commercialising the value of the information that they obtain as a by-product of offering these services. If this scenario were to play out, it could significantly change the payments landscape, providing both merchants and consumers new payment options at low monetary cost. At the same time though it would raise a number of important issues related to data privacy, ownership and security.

The probability of Big Tech firms entering the payments arena is higher if merchants and consumers feel that the existing payment systems do not offer them the services they need and/or the prices that are being charged are too high. As I noted earlier, where banks have been slow to respond, other payment applications have emerged.

This scenario highlights a broader point. The way that people are charged for payments is complex and is changing: among other things, it is influenced by interchange fees, how the value of information is commercialised, and commercial pressures on banks. It is difficult to predict how things will ultimately play out, but these are issues the Payments System Board continues to keep a close eye on.

5. Summing Up

To conclude, I expect the shift to electronic payments will continue. The issues of functionality, security and reliability, and cost are central to the development of the system. The Payments System Board will be keeping a close eye on these issues.

While I have talked about a near cashless payments system, I want to emphasise that we don’t yet envisage a world without banknotes. The RBA is committed to providing cash consistent with demand by users and to support its distribution. Our development of the Next Generation Banknote series is a clear commitment to ensuring that cash continues to have public confidence and to meet the needs of the community.

The launch of the NPP this year was a big step forward for the industry and a credit to all of the staff at participating organisations who worked hard over the life of the project to bring it to fruition. As I mentioned, there are some key things that need to be done for the full benefits of the NPP to be available to end-users, but I am optimistic that these can be achieved and this new infrastructure can provide great functionality for Australia.

{kind=link}