He suggests a turning point has been reached. It is now easier than it has been to conceive of a world in which banknotes are used for relatively few payments; that cash becomes a niche payment instrument.

This morning I would like to speak about the shift towards electronic payments; or as the title of my remarks says, the journey towards a near cashless payments system. For some decades, people have been speculating that we might one day go cashless – that we would no longer be using banknotes for regular payments and that almost all payments would be electronic. So far, this speculation has been exactly that – speculation. But it looks like a turning point has been reached. It is now easier than it has been to conceive of a world in which banknotes are used for relatively few payments; that cash becomes a niche payment instrument.

Given this, I would like to structure my remarks around three broad points.

The first is that the shift to electronic payments is occurring quite quickly and it is likely to continue. This shift is a positive development that should promote our collective welfare.

The second is that if we are to realise the benefits of moving to a near cashless payments system, the electronic system needs to offer the functionality, safety and reliability that people require. People need to have confidence that the electronic payment system will be operating when they want to make their payments and that it will deliver the payment services that they need.

The third point is that as we undertake this journey towards a near cashless payment system, there will be a greater focus on the cost of electronic payments. If almost all payments are electronic, then the cost of making these payments matters more than it used to. The electronic system needs to be as efficient as it can be and to be characterised by strong competition. In my view, there is further work to be done here.

1. The Shift to Electronic Payments

The Reserve Bank conducts regular surveys of how Australians make their payments. The next survey will be undertaken in 2019. Until then, perhaps the best illustration of the declining use of cash for transactions is the sharp decline in the number and value of cash withdrawals through ATMs (Graph 1). Around the turn of decade, Australians went to an ATM, on average, around 40 times per year. Today, we go to an ATM around 25 times a year and the downward trend is likely to continue.

Graph 1

At the same time as the use of cash for payments has been declining, the number of electronic transactions has been growing strongly (Graph 2). Today, Australians make, on average, nearly 500 electronic payments a year, up from around 100 per year around the turn of the century.

Graph 2

New payment technologies are being developed that will further encourage this shift to electronic payments. Perhaps the most significant of these is the New Payments Platform, which has made it possible for people to make real-time person-to-person payments without using banknotes. A range of payment apps are also under development that would have the same effect. So the direction of change is clear.

There also continues to be a decline in the use of cheques (Graph 3).[1] In the mid 1990s, Australians, on average, made around 45 cheque payments per year. Today, we make around three per person. Given this trend is likely to continue, it will be appropriate at some point to wind up the cheque system, given the high fixed costs involved in operating the system. We have not reached that point yet, but it may not be too far away. Before we do, it is important that alternative payment methods are available. Progress has been made on this front, but more is required.

Graph 3

It is worth pointing out that despite the decline in cash use, the value of banknotes on issue, relative to the size of the economy, is close to the highest it has been in fifty years. For every Australian there are currently around thirty $50 and fourteen $100 banknotes on issue (Graph 4).

Graph 4

So there is an apparent paradox between the declining use of cash and the rising value of banknotes on issue. The main explanation is that some people, including non-residents, choose to hold a share of their wealth in Australian banknotes. The opportunity cost of doing this is less than it used to be because of the low level of interest rates.

While it is difficult to predict the future, I expect that banknotes will remain part of our payments system for some time to come.

In some situations, paying with banknotes is quicker and more convenient than paying electronically, although this advantage is less than it once was. Some people also simply prefer paying in cash – our 2016 survey indicated that around 14 per cent of Australians had a preference for using cash as a budgeting tool.

Banknotes also allow payments to be made anonymously in a way that is not possible in systems that leave an electronic fingerprint. This privacy aspect is valued by some people. In some circumstances this desire for privacy is entirely legitimate, but in others it has more to do with tax evasion and illegal activities.

Perhaps a more important source of ongoing demand is the fact that using cash does not require the internet to be up, electricity to be working and the banks’ systems to be operational. Banknotes are therefore an important emergency or back-up payment instrument. They are particularly useful in the event of natural disasters or failure of the electronic system. Perhaps one day the various systems will be so reliable that a backup will not be needed, but that day still seems some way off.

Overall, the shift to electronic payments that is occurring makes a lot of sense – it is similar to other aspects of our lives where things that used to be physical have been supplemented with, or replaced by, technology. This shift is likely to promote our collective welfare. I say that even though the Reserve Bank is the producer of banknotes and earns significant income, or as it’s known, seigniorage, for the taxpayer from their use. The greater use of electronic payments can bring efficiency benefits, with lower costs and more functionality and choice for users. One example of this is the reduced tender time involved in card transactions due to contactless technology. There are also non-trivial production and distribution costs involved in the cash system. Some of these are fixed costs, so the average cost of cash transactions is likely to rise as the volume of cash transactions falls. Looking ahead, there is also more limited scope for fundamental innovation in the cash system compared with the scope for dynamic innovation in electronic payments. So this journey is in our national interest.

2. Functionality, Safety and Reliability

I would now like to discuss three interrelated factors that will influence how quickly we undertake that journey. These are: the functionality offered by the electronic system; the safety of that system, and the reliability of that system. The other factor that is also relevant is cost, and I will touch on this a little later.

Functionality

The rapid adoption of contactless payments in Australia shows that Australians change how they pay quite quickly when new functionality is offered. Contactless card payments were slow to take off but once critical mass was established, they grew very quickly. In our 2013 consumer payment study they accounted for around over 20 per cent of point of sale card payments; three years later they accounted for over 60 per cent. So the functionality of the electronic payments system is key.

The development of the electronic payment system took a major step forward earlier this year with the launch of the New Payments Platform (NPP). This system allows people to make payments 24 hours a day, 7 days a week, using just a simple identifier such as a mobile phone number or an email address. It also allows a lot of information to accompany the payment. I expect that over time this extra functionality will further reduce the use of cash in the economy and also improve the efficiency of the electronic system.

The number of transactions through the NPP is steadily increasing (Graph 5). After a relatively low-key start, there are now around 400,000 NPP transactions per day. Over 2 million PayIDs have also been registered, and we expect further growth as the banks continue to roll out services to their customers.

Graph 5

The concept behind the NPP is that so-called ‘overlay’ services are developed, and that these overlay services offer new functionality that utilise the real time capability of the NPP. The first overlay service provides for a basic account-to-account payment. Among the subsequently planned overlay services are ones that will allow someone to send a request to pay, perhaps to a friend for their share of a meal out. Another overlay service would allow a link to a document to be sent with a payment; this could be a payslip or a detailed record of the transaction.

It was originally anticipated that these two overlay services would be up and running not long after the NPP launch. Unfortunately, this timeline has slipped. A number of the major banks have also been slower than was originally expected to roll out NPP functionality to their entire customer bases. This is in contrast to the capability offered by smaller financial institutions, which from Day 1 were able to provide their customers with NPP services. Given the slow pace of roll-out by the banks, and the prospect of delays for additional overlay services, I recently wrote to the major banks on behalf of the Payments System Board seeking updated timelines and a commitment that these timelines will be satisfied. It is important that these commitments are met.

It is worth observing that in other countries where banks have been slow to develop payment applications that meet the needs of the public, other possibilities emerge. China is perhaps the best example of this, with the emergence of QR-code-based payments. I expect that the NPP infrastructure will be the backbone of our electronic payments system for many years to come. But for this to be the case, the system will need to provide the functionality that people require, and it will need to do this on a timely basis.

There are a range of fintech firms that are excited by the capabilities offered by the NPP and the potential for it to be used for innovative payment solutions. In October, the RBA issued a consultation paper seeking views on the functionality and access arrangements for the NPP. In particular we are interested in views on whether the various ways of accessing the NPP, and their various technical and eligibility requirements, are adequate for different business models.

A topic that I get asked about from time to time is whether the functionality of the electronic system would be enhanced by the RBA issuing an electronic version of the Australian dollar, an eAUD. I spoke about this issue at this conference last year, concluding that we did not see a public policy case for moving in this direction at the time. In particular, it is not clear that RBA-issued electronic banknotes would provide something that account-to-account transfers through the banking system do not, particularly with the emergence of the NPP. Another important consideration was the implications for financial stability. A year on, our views have not changed.

Security

A second important influence on the rate at which we shift to a more electronic payments system is the public’s confidence in the security of the system.

Given this, a recent focus of the Payments System Board has been the high and increasing level of fraud in card-not-present transactions (Graph 6). Card-not-present fraud rose by 15 per cent in 2017 and now represents 87 per cent of total scheme card fraud losses.[2] In contrast, the industry has had successes in addressing card-present fraud, with the introduction of chip technology and the switch to PINs. Despite this, growth in e-commerce activity has provided new opportunities for would-be fraudsters.

Graph 6

The Payments System Board identified the rise in card-not-present fraud as a priority for the industry. In August this year, the Board was pleased to welcome AusPayNet’s publication of a draft industry framework to mitigate card-not-present fraud, and supports continued collaboration on this issue.

A separate but not unrelated priority for the industry is to progress work on digital identity. This is another area where barriers to effective coordination can arise. I am pleased that AusPayNet is undertaking work here, under the auspices of the Australian Payments Council. Digital identity is likely to become increasingly important as more and more activity takes place online. The RBA is highly supportive of industry collaboration on this issue and views it as important that substantive progress is made.

More broadly, individuals, businesses, governments and financial institutions all need to be aware of cyber risks. In the RBA’s most recent Financial Stability Review we noted the increasing sophistication of cyber attacks and that regulatory authorities have increased their focus on cyber issues.

Reliability

A third factor is the confidence that people have that they will be able to use the electronic system when they need to make their payments. As I noted earlier, people will still want to hold and use banknotes if they can’t be sure that the electronic system will be available when they need it. In our consumer payments survey in 2016, we asked people about why they held cash in places outside of their wallet. The most common response, from nearly half of respondents, was that it was for emergency transaction needs.

Over recent times, there have been a number of serious operational incidents that have interrupted the payments system. On some occasions these have been caused by problems with the telecommunications companies and at other times by problems at the banks. An operational incident at the RBA in August as a result of problems with a routine fire test also saw a number of RBA core systems unavailable for some hours, including the Fast Settlement Service supporting the NPP.

We all need to do better here. As we rely less on cash, outages affecting retail transactions can have a significant impact on businesses and individuals. So continued effort needs to be made by all participants in the payments system to reduce operational problems. If this does not happen, then it is possible that the Payments System Board could consider setting some standards.

3. Increased focus on Cost and Competition

My third broad point is about the cost of electronic payments and the importance of competition.

As we move to a predominantly electronic world, there will be more focus on the cost of operating the electronic payments systems and how those costs are allocated between those making and receiving payments.

Looking forward, I expect that over time the cost of electronic payments will decline further, due to both advances in technology and economies of scale. Even so, there are significant costs to operate the electronic systems, including costs for front- and back-end systems to maintain accounts, and to deliver functionality and convenience to users, as well as costs in preventing fraud and ensuring resilience. How these costs are managed and who pays for them will have a significant bearing on the efficiency of the overall system.

In terms of card payments, merchants in Australia currently pay less than merchants in many other countries. The comparison with the United States is particularly stark (Graph 7). For credit cards, Australian merchants, on average, pay 0.8 per cent of the transaction value for Mastercard/Visa transactions. In the United States the figure is much higher at around 2.2 per cent. There are also differences in the cost of debit cards and American Express cards between the two countries.

Graph 7

The main reason for the lower merchant costs in Australia is our lower interchange fees. These fees were reduced in Australia as a result of regulation by the Reserve Bank commencing in 2003. The RBA’s reforms reduced average interchange fees in the Mastercard and Visa systems by around 45 basis points. This has been reflected in merchant service fees; indeed, these merchant fees have fallen by somewhat more than the cuts to interchange, likely reflecting an increased focus on card acceptance costs by merchants (Graph 8). In addition, as a result of competitive pressure, including from the removal of no-surcharge rules, fees on American Express and Diners Club have also fallen over time.

Graph 8

Notwithstanding the reduction in interchange fees, these fees still represent, on average, around 60 per cent of the total merchant service fee on credit cards. So they remain an important part of the total cost to merchants. Conversely, these fees mean that the cardholder’s bank gets paid each time the card is used. This has meant that the cost to consumers of using these cards is often low; in some cases, cardholders are actually subsidised to use their card, through reward points and/or interest-free credit. The subsidy is provided by the cardholder’s bank, but ultimately paid for by the merchant.

The close link between interchange and merchant costs means that there continues to be significant focus on interchange and its implications for the distribution of costs between merchants and consumers. For example, there have been recent recommendations from the Black Economy Taskforce and the Productivity Commission for the Reserve Bank to consider regulatory action to lower, or even ban, interchange fees. The Payments System Board will again examine the arguments for lower interchange fees when it next conducts a formal review of the card payments system.

On the competition front, one area that merits close attention is the market for acquiring services. This has come into sharper focus as a result of concerns about the costs to merchants in the debit card system, where most cards allow for transactions to be processed by either of the two networks enabled on the card. The longstanding view of the Payments System Board has been that merchants should at least have the choice of sending the debit payment through the lower cost system, whether that be eftpos or the international scheme.

For merchants to be able to do this though, acquirers need to offer terminals and technical systems enabled to allow least-cost routing. Some acquirers have already completed the necessary work and are attracting new merchants. Others, including the major banks, made commitments earlier in the year regarding the timetable for this work to be completed. Partly on the basis of those commitments, the Payments System Board made a decision not to regulate. Since then, I regret to say there has been slippage by some, who have cited technical problems. It is important that the banks get back on track here. A failure to deliver on commitments or to provide the payment services that the community needs will inevitably lead to calls for further regulation.

4. Looking ahead

Looking beyond interchange and acquiring competition, new technologies open up the prospect of new payment options developing. Recently, there has been much discussion on the role that so-called ‘Big Tech’ firms might eventually play.

These firms have potential advantages over existing providers of payments services. In some cases, their technology and systems are more flexible, they have a greater ability to use and process information, they have well established networks which they can leverage and they are often better at interacting with their users and customers. Given this, one scenario is that these firms become significant players in the payments industry. They might be able to do this through developing new payment applications that provide a commercial return, not through charging for payment services, but by commercialising the value of the information that they obtain as a by-product of offering these services. If this scenario were to play out, it could significantly change the payments landscape, providing both merchants and consumers new payment options at low monetary cost. At the same time though it would raise a number of important issues related to data privacy, ownership and security.

The probability of Big Tech firms entering the payments arena is higher if merchants and consumers feel that the existing payment systems do not offer them the services they need and/or the prices that are being charged are too high. As I noted earlier, where banks have been slow to respond, other payment applications have emerged.

This scenario highlights a broader point. The way that people are charged for payments is complex and is changing: among other things, it is influenced by interchange fees, how the value of information is commercialised, and commercial pressures on banks. It is difficult to predict how things will ultimately play out, but these are issues the Payments System Board continues to keep a close eye on.

5. Summing Up

To conclude, I expect the shift to electronic payments will continue. The issues of functionality, security and reliability, and cost are central to the development of the system. The Payments System Board will be keeping a close eye on these issues.

While I have talked about a near cashless payments system, I want to emphasise that we don’t yet envisage a world without banknotes. The RBA is committed to providing cash consistent with demand by users and to support its distribution. Our development of the Next Generation Banknote series is a clear commitment to ensuring that cash continues to have public confidence and to meet the needs of the community.

The launch of the NPP this year was a big step forward for the industry and a credit to all of the staff at participating organisations who worked hard over the life of the project to bring it to fruition. As I mentioned, there are some key things that need to be done for the full benefits of the NPP to be available to end-users, but I am optimistic that these can be achieved and this new infrastructure can provide great functionality for Australia.

A fintech start-up is celebrating a $25million raise as it continues on its pathway to becoming Australia’s “most innovative home loan provider”; via AustralianBroker.

Athena Home Loans, which is still in its pilot phase, has closed its most recent Series B raise led by Square Peg Capital.

Industry super fund Hostplus and venture firm AirTree also joined the round, taking the group’s total capital raised to date to $45m.

The Series B raise comes six months after the company announced a Series A fund raise led by Macquarie Bank and Square Peg Capital and three months after announcing a strategic partnership with Resimac Group.

Powered by Australia’s first cloud native digital mortgage platform, Athena aims to bypass the banks to connect borrowers to superfund backed loans.

The company was founded by two ex-bankers, Nathan Walsh and Michael Starkey, who said they wanted the journey to home ownership to be faster, cheaper and stress free.

Square Peg Capital invested in Athena in Series A and has further solidified its support of the home loan provider by leading the Series B round.

Venture capitalist and co-founder of Square Peg, Paul Bassat, who also sits on the Athena Board, said investing further into Athena proves the potential they see in the business.

He said, “Having worked with Nathan, Michael and the team over the last year I have enormous admiration for the speed at which they have navigated complex financial systems to develop a robust and customer-centric mortgage service.

“Athena is solving a really important problem for home buyers and is certainly one of the most exciting Fintech companies in Australia.

“We are thrilled to back the team again and look forward to supporting them on this extraordinary journey.”

Industry superannuation fund Hostplus has more than 1.1 million members and $37billion in funds under management.

Hostplus has spearheaded investment in the local start-up ecosystem, with more than $1billion of its fully diversified portfolio committed to Australian venture capital managers.

Hostplus chief investment officer, Sam Sicilia, said that “Athena is a great example of disruptive innovation delivering big savings for home loan borrowers”.

Athena COO Michael Starkey said, “We are delighted to have Hostplus and AirTree joining Athena as investors. Athena’s journey has benefited hugely from the insights and support from some of Australia’s smartest investors. It’s clear the timing has never been better to offer a fairer home loan.”

Athena CEO Nathan Walsh said, “During our pilot, we are already seeing the power of the Athena proposition to save money and change lives.

“A single mum who will be able to pay off her home loan 19 months earlier and save $130,000 over the life of the loan.

“A family with three young kids who will save $40,000 on their home loan can now take the family on the first holiday in years. It’s powerful stuff.”

Commenting on the company’s upcoming launch in Q1 2019, Nathan said, “Our key priorities with the investment will be to continue to innovate our platform, invest in talent and scale the business.

Australian fintech Tic:Toc – the world’s only fully digital home loan platform – has announced Bendigo Bank will use Tic:Toc’s proprietary technology to power its own instant home loan, Bendigo Bank Express.

The white label partnership will allow Bendigo Bank to be the first Australian lender offering a digital home loan application and assessment process under its own brand, accelerated with Tic:Toc technology.

Tic:Toc launched the World’s first instant home loan™ in July 2017, and is now collaborating with financial institutions to offer their platform as a service; helping bring traditional home loan processes up to speed.

Tic:Toc’s technology offers customers a streamlined digital fulfilment process, while lenders benefit from significant efficiencies in the way they can originate home loan customers. The automated assessment strips cost from the process and delivers higher responsible lending standards via inbuilt reg-tech and digital validation of income and expenses.

Announcing the agreement, Tic:Toc founder and CEO, Anthony Baum, said most importantly, the customer will be the ultimate beneficiary of the collaboration between financial institutions and fintechs.

“Tic:Toc is changing the customer experience when it comes to home loans. It’s no longer necessary to wait weeks for home loan approval, when it can be done digitally and conveniently.

“There’s actually not much difference between home loan options. But there can be a big difference in how that home loan is delivered, and the experience for the customer.

“Our automated assessment and approval technology also creates dramatic cost efficiencies for lenders.

“You only need to look to the United States to see how a digital home loan can change a market: Quicken Loans is now America’s largest home loan lender after launching their online product, Rocket Mortgage.

“Our partner, Bendigo and Adelaide Bank, shares our passion for great customer outcomes, so we’re delighted the Bank has chosen Tic:Toc to offer its customers a truly digital experience, if they want it.”

Bendigo and Adelaide Bank Managing Director, Marnie Baker said, “Our partnership with Tic:Toc is another example of Bendigo and Adelaide Bank investing in innovative technologies to offer Australian consumers more choice, and ultimately, better digital experiences.

“Our strategy means we can provide the best solution to customers by selecting the right partner to offer the right services to meet our customers’ needs and make it easier for them to do business with us. Fintech disruption, combined with banking innovation, is helping us drive better outcomes and we consider relationships with fintechs, such as Tic:Toc, as a mutually beneficial strategy.

“We believe we can grow our business through our vision of being Australia’s bank of choice and we will do this by providing new and existing customers with valued and relevant products and services, all while investing in new capability and innovation,” she said.

Bendigo Bank Express will be available to customers in early 2019.

Since its launch, Tic:Toc has received more than $1.6 billion in value of submitted home loan applications. While the white label product will be available directly from Bendigo Bank, the multi award-winning home loans originated by Tic:Toc are already available throughout Australia at tictochomeloans.com.

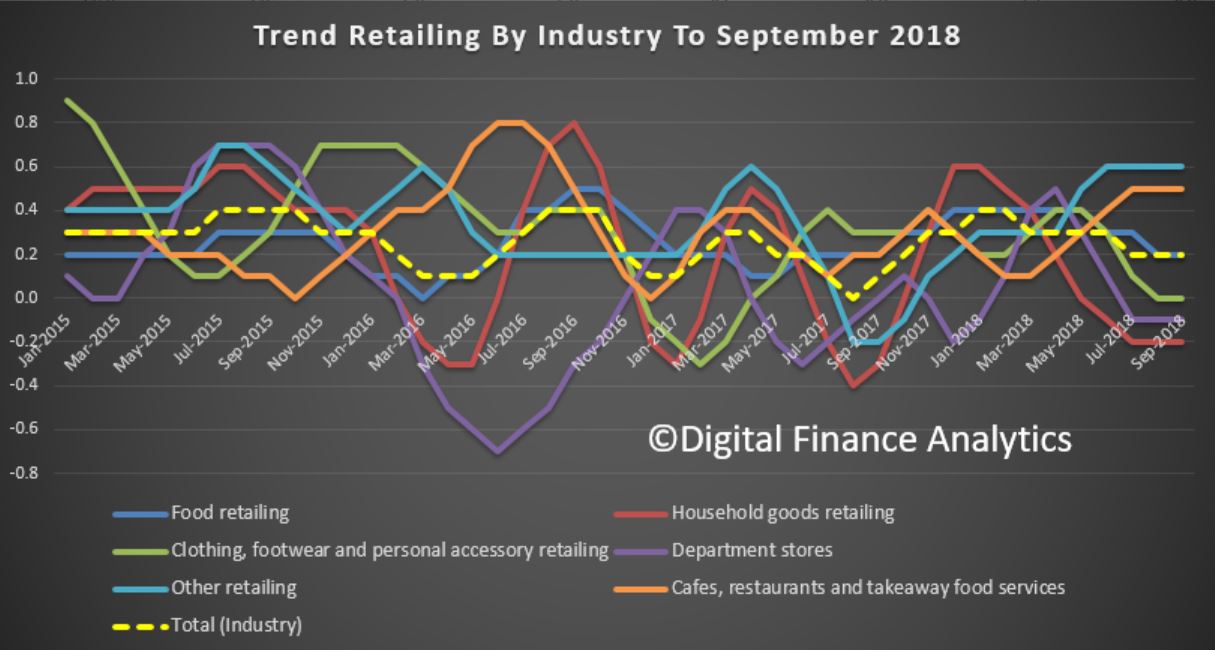

In trend terms, overall retail turnover grew by 0.2% in the month. Within the segments, Other Retailing rose 0.6%, Cafes, Restaurants and Take Away Food rose 0.5%, Food Retailing 0.2%, Clothing, Footwear and Personal services was flat, while Household Goods fell 0.2% and Department stores fell 0.1%.

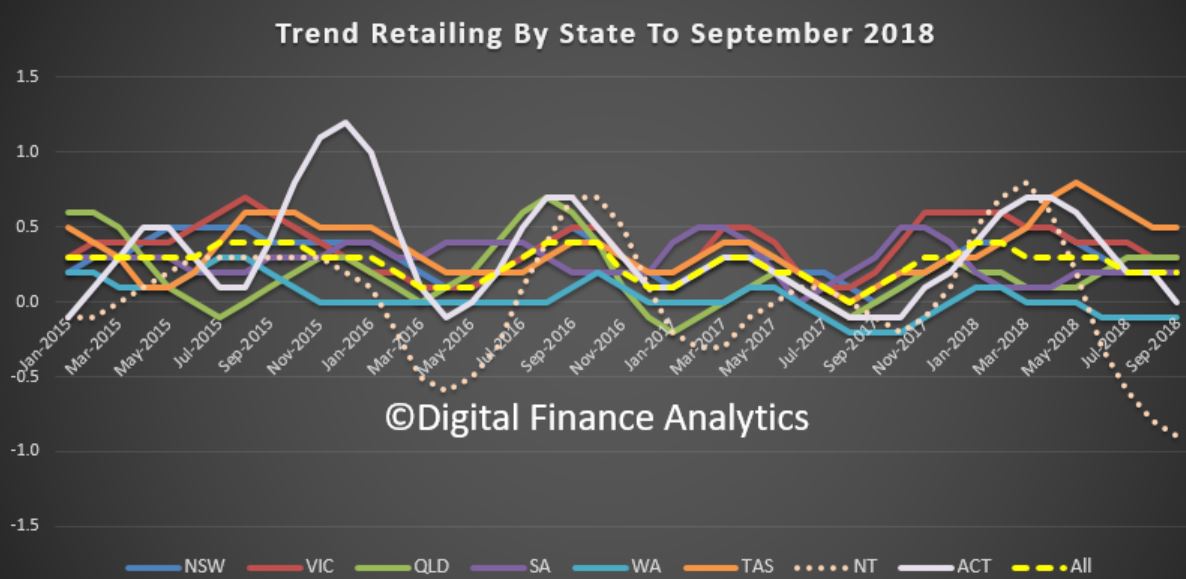

Across the states, TAS rose 0.5%, QLD and VIC both rose 0.3%, NSW rose 0.2% along with SA, ACT was flat, WA fell 0.1% and NT fell 0.9%.

Online retail turnover contributed 5.6 per cent to total retail turnover in original terms in September 2018, an unchanged result from August 2018. In September 2017 online retail turnover contributed 4.4 per cent to total retail.

Property Insider Edwin Almeida discusses the future of the Real Estate Industry sector, given recent falls in sales, extended sales cycles, and the uncertain future outlook.

Expect big changes in the sales and franchise models.

The release of the third Australian Digital Inclusion Index (ADII) earlier this week adds weight to the Keep Me Posted campaign who are advocating for a ban on paper billing fees. Multinationals profit on the back of struggling Australians and Keep Me Posted is calling on Government to restore sense to the digital divide debate.

Keep Me Posted is heading to Canberra in October to once again call on the Government to protect vulnerable Australians by implementing legislation banning paper bill fees. The campaign is demanding answers, despite being promised answers in April 2018 following Treasury’s Consultation into paper billing fees conducted in December 2017.

Kellie Northwood, Campaign Director, Keep Me Posted commented, “Our most vulnerable Australians can no longer wait as the least able to afford these charges in our community are being impacted the most.”

Whilst some states are improving, there’s still work to be done to ensure all Australians are receiving important communications the way they wish to receive. As the digital divide widens, and while internet connectivity prices are not decreasing, struggling families who can least afford it are being hit the hardest.

The campaign supports Lead Researcher, Professor Julian Thomas’ comments stating there are more than 2.5 million Australians who are not online and therefore missing out on benefits that come with connection. “What we’ve found is that nationally, digital inclusion is improving, but there is much more work to be done. Poorer and more vulnerable communities are more likely to be digitally excluded and are not enjoying all the benefits of being online. As an increasing number of essential services and essential communications move online, the divide is getting deeper.” From this, paper-based alternatives are essential to a large portion of vulnerable communities.

“There are still several Australian communities who like, want and, more importantly, need paper-based communications. All homes come with a letterbox, not everyone has internet connectivity,” Northwood furthered.

“It is unfair for Australians to succumb to everything digital when there are alternatives still available, and the paper bill is a favourable alternative that should be provided free of charge. As companies continue to push Australians online, a greater burden is put on those not connected.”

Keep Me Posted applauded New South Wales earlier this year when premier Gladys Berejiklian announced the end of paper bill charges from energy retailers as part of a series of measures included in the Energy bill relief package and the campaign is now calling on other states to show the same leadership.

The campaign is also calling on new Energy Minister, Angus Taylor, to show similar leadership and implement legislation at a Federal level.

The 2018 ADII is based on data from more than 16,000 Australians captured in the annual cycle of the Roy Morgan Single Source Survey.

Tony Richards, RBA Head of Payments Policy Department spoke at the Chicago Payments Symposium, Federal Reserve Bank of Chicago and described the progress on the new payments platform – NPP. 2 million PayID registrations have been achieved so far, and the volume of payments has already outpaced cheques in the system.

Initial NPP operations

After industry testing through much of 2017, the NPP became operational for industry ‘live proving’ in November 2017. It was launched for public use on 13 February this year. This involved around 50 institutions initially, with this number now having increased to around 65 institutions.

As with any completely new payment system, financial institutions have mostly taken a staged approach in their rollout strategies, gradually introducing services, channels and customer segments. In some cases this was to manage risk and allow them to fine-tune their systems and processes, while in other cases it has reflected different stages of readiness. The major banks have mainly focused initially on providing payment capabilities to consumers ahead of businesses, with the rollout to consumers now at a fairly advanced stage.

At this point, there are more than 50 million Australian bank accounts accessible via the NPP, with that number growing steadily. The number of PayID registrations has just reached 2 million – Australia has a population of 25 million. And monthly volumes and values of NPP transactions have been growing strongly.

One interesting statistic is that the number of payments occurring through the NPP has already surpassed the number of cheques that are being written by Australian households, businesses and government entities

An international comparison also offers another interesting metric. While each country is its own special case, it appears that the adoption of the NPP is proceeding at least as quickly as occurred for some other fast-payment systems

As long as the rollout of NPP to households has not been completed, advertising of Osko by BPAY has been limited, but I would expect that this will be picking up, and that financial institutions will also be doing more promotion of real-time payments to their customers. So I would expect the value and volume of NPP transactions to continue to grow strongly.

Some early lessons learned

While the NPP was launched less than eight months ago, I think one can make a number of observations that may be of interest to this audience regarding its design and build, as well as its operation to date.

The presence of a well-resourced project office (from KPMG as well as from APCA and then NPPA) that was independent of the participants was important in the design, build and test phases. This ensured high quality papers for meetings, brought skills that might not have been readily available from participants, and provided independent perspectives during debates about the design and build

Having three aggregators (or service providers) involved as participants was important in ensuring the broad reach (and public legitimacy) of the NPP. The majority of the institutions that were ready to go on Day 1 were small banks, credit unions and building societies using the services of aggregators.

While the build of the Basic Infrastructure and FSS in the centre were major projects, the internal builds for NPP participants were the most challenging tasks. The systems of large banks are inevitably extremely complex, and upgrading them to allow real-time posting and 24/7 operation has taken longer than expected for some. Banks have also placed significant focus on ensuring that their fraud detection systems can support real-time payments.

Ubiquity (or near-ubiquity) is important. It is hard for a new payment system or for individual participants to go out and market aggressively to customers until a critical mass of institutions and accounts are on board. However, balancing this point and the previous one is a challenge. Decisions to launch to the public can only occur once a critical mass of participants is ready, but a program cannot be expected to move at the pace of the slowest participant.

Real-time settlement is going well. The challenges raised by out-of-hours and weekend operations can be met by appropriate central bank liquidity arrangements. Banks can easily move the balances in their Exchange Settlement accounts between the FSS and the RBA’s main RTGS system during normal business hours. These balances are then all moved into the FSS overnight and on weekends. In addition the Reserve Bank introduced a new liquidity facility for open-dated repos, which are available to holders of Exchange Settlement accounts at no penalty relative to the Bank’s policy rate.

Five or six years ago, some banks may have questioned the case for moving to real-time payments, however no one is questioning that case now. Indeed, the early signs are that banks are looking to move their Direct Entry payments over to the fast rails sooner than was earlier expected. Similarly, the decision to move to the ISO 20022 message format and richer data will be an important one for future innovation.

It was important to have the Addressing Service ready to launch on Day 1. PayIDs get around the problems of end-users having to enter lots of numbers, give certainty about the recipient, help avoid ‘fat finger’ problems and mistaken payments, and can reduce fraud.

The involvement of the central bank – from the policy side, as well as in the delivery of settlement arrangements and as a banking service provider – has been important. I suspect that some industry participants may initially have had some concerns about having the Reserve Bank involved, but that they would recognise now that our involvement helped to get some key aspects of the design, build, and business rules right.

The fact that the Basic Infrastructure will be operated as an industry utility available to all, with commercial payment services to be provided by separate overlay services, was also helpful in getting agreement among participants in the design phase.

With the initial build mostly complete, the industry has ambitious plans for additional NPP functionality. While some of this could potentially be delivered via overlay services, it is likely that there will be additional central functionality provided or arranged by NPPA – for example, possibly a central consent and mandate service that could be used to enable direct debits though the NPP. As NPPA increases its capabilities, it may also look to new means of providing functionality. On Friday it announced an API framework with three sample APIs.

The chairman of the prudential regulator, Wayne Byres, was speaking at the 2018 Curious Thinkers Conference in Sydney on Monday (24 September) when he outlined a “clash of predictions” for the future of the financial sector.

Stating that the pace of change “makes predicting the future difficult, and is why the crystal balls of even the most well informed are cloudy”, Mr Byres said that “everyone agrees major change is inevitable”.

Noting that it was “clear” that companies, regulators and international agencies are “all grappling to predict the impact that technology-enabled innovation will have on the structure of the financial sector and the viability of existing business models”, Mr Byres conceded that the “consensus also seems to be that it is too soon to tell whether the financial world faces evolution or revolution”.

Despite this, the chairman of the Australian Prudential Regulation Authority (APRA) told delegates that whatever the future scenario is, the “production and delivery of financial services will change”.

“Put simply, many traditional business models will no longer be competitive without significant change driven by technological investment,” Mr Byres said.

“Moreover, some incumbents will struggle to afford that investment; for others, the challenge will be successfully managing a large transformation program.”

Later in his speech, the APRA chairman forewarned that while most technological advancements in finance have previously “worked to enhance the market positioning of the major incumbents”, the future will “likely be different”.

Despite several futurists suggesting that brokers will survive digital disruption and others outlining that brokers will become more crucial in the future as trust in finance deteriorates, Mr Byres suggested that broker networks could be under threat in the future.

He stated: “New technologies have dramatically lowered barriers to entry. Cloud computing, for example, allows small organisations to operate innovative financial services without the need to maintain their own costly infrastructure and support staff.

“The advent of digital distribution and servicing removes the need for branch and broker networks.

“Open banking and comprehensive credit reporting will help new competitors to challenge established players. And, of course, regulators are making it easier to navigate the process of entry into the regulated financial system. Taken together, competition in the supply of financial services will only intensify.”

In conclusion, Mr Byres said that APRA’s role was to “make sure regulated entities are resilient and responsive to change, but not protected from it”, adding that while the regulator is responsible for promoting stability, “that does not mean standing in the way of change”.

He added: “Ensuring regulated entities are well managed, soundly capitalised and able to withstand severe stresses is designed to protect the interests of their depositors, policyholders or members.

“But to be clear, it is not APRA’s role to protect incumbent players when better, safer and more efficient ways of doing business emerge.

“Ultimately, we seek to look at it with a sharp focus on what is in the longer-run interests of their depositors, policyholders or members — not the business itself, or its owners — and make sure that boards and management are doing likewise.

“If that means their time is up, so be it. Our role then becomes ensuring they make an orderly exit from the industry.”

FBAA hits out at comments

The executive director of the Finance Brokers Association of Australia (FBAA), Peter White, hit out at the comments made by Mr Byres yesterday, telling The Adviser: “As it is, I certainly and completely disagree with this as being a current or near-term situation.”

The head of the FBAA highlighted that its research had recently showed that nearly 95 per cent of broker clients were satisfied with their broker, adding that more than half of the borrowing population uses a broker.

“So, digital distribution is not supported by fact,” Mr White said.

While the head of the FBAA suggested that digital home loans without any human intervention may be commonplace in 20 years’ time, he added that “we are a long way from this” in the near future.

Mr White told The Adviser: “For now, most people want to transact their home loan with a person, not a screen, and this won’t change for some time. Let alone the technical and legal barriers that still exist, the human element is still far more desired.”

In a shot across the bow, Mr White concluded: “So, for now (and once again), APRA seems to be out of touch with reality and people. Possibly they should be more so focused on their governance of ADIs given what we’ve all witnessed in the [banking] royal commission rather than out-of-focus speculation.”

ASIC has taken action to stop several proposed initial coin offerings or token-generation events (together, ICOs), targeting retail investors.

As well, ASIC recently stopped the issue of a Product Disclosure Statement for a crypto-asset managed investment scheme.

Consistent problems identified by ASIC are:

the use of misleading or deceptive statements in sales and marketing materials;

operating an illegal unregistered managed investment scheme (MIS);

not holding an Australian financial services licence.

Such problematic offers involve significant risks for investors.

ASIC Commissioner John Price said, ‘If you raise money from the public, you have important legal obligations. It is the legal substance of your offer – not what it is called – that matters. You should not simply assume that using an ICO structure allows you to ignore key protections there for the investing public and you should always ensure disclosure about your offer is complete and accurate.’

Recent activity by ASIC

In five other separate matters since April 2018, ASIC successfully acted to prevent ICOs raising capital without the appropriate investor protections. These ICOs have been put on hold and some will be restructured to comply with the applicable legal requirements.

ASIC is taking further action in respect of one completed ICO.

On 13 September 2018, ASIC issued a final stop order on a Product Disclosure Statement issued by Investors Exchange Limited (IEL) for units in the New Dawn Fund (Fund). The Fund was proposing to invest in a range of cryptocurrency assets. Following ASIC raising concerns about the PDS, IEL consented to a final stop order so that no units could be obtained under the PDS. ASIC acknowledges the co-operative approach taken by IEL in responding to ASIC’s concerns.

Investor warning

As outlined on MoneySmart, ICOs are highly speculative investments that are mostly unregulated, and while there are genuine businesses using this structure many have turned out to be scams. ASIC suggests that investors consult the information on Moneysmart before deciding to invest.