Wisr is Australia’s only ASX listed marketplace lender and a fintech pioneer in the rapidly growing Australian consumer finance market. The company is is increasing its personal loan limits following increased borrower demand, strong institutional lender support and continued improvement to loan evaluation.

As of this week, Wisr will increase its personal loan limit from $35,000 up to $50,000, with a comparative interest rate up to 5% p.a. lower than the four major banks.

Loans will be available for any worthwhile purpose over three or five years, with a comparison rate of 9.36% p.a. for borrowers with a strong credit rating. The neo-lender also offers no early repayment or exit fees.

Chief executive officer Anthony Nantes said, “We have never been in a stronger position to help more Australians achieve a fairer financial future. During the past six months we’ve seen increasing borrower demand, continued strong support from institutional lenders and improvements to our lending platform.

“[The] announcement means creditworthy Australian borrowers now have more choice, to do bigger, more exciting things, and the opportunity to potentially make significant savings through lower interest rates and lower fees when compared to a personal loan from a traditional big bank.”

The move follows a period of strong personal lending growth for the company. Wisr announced record loan growth earlier this year, with originated loans growing by 42% in FY18 Q3 when compared with the previous quarter. It was the company’s largest quarter in loan originations since it began in 2014.

During the same period the company also announced ongoing improvement to its automated loan evaluation platform. The gross annualised loss rate for the loan book up to the quarter ending 31 March 2018 had also been below 2%.

A joint venture backed by three of Australia’s big four banks has released its first app, with Beem It now available for iOS and Android devices according to a report in Computerworld.

The Commonwealth Bank of Australia, National Australia Bank and Westpac in October revealed that they would back Beem It, which the trio said would operate independently and seek to sign up additional partners as it developed cross-platform mobile payment services.

The launch of the joint venture came in the wake of the failure of the three banks, along with Bendigo and Adelaide Bank, to receive Australian Competition and Consumer Commission (ACCC) blessing to act as a cartel when negotiating with Apple over its Apple Pay platform.

More than 50 Australian financial institutions support Apple Pay. However, of the big four, only ANZ supports Apple’s digital wallet for iOS devices.

CBA, NAB, Westpac and Bendigo and Adelaide Bank lodged an application with the ACCC that would have allowed them to band together and negotiate with Apple over a number of issues relating to mobile payments.

A key goal of the banks was to force Apple to open up access to the iPhone’s Near Field Communications (NFC) antenna — which would allow the banks’ own iOS applications to support tap-and-go style payments over NFC.

Apple said in response that it would never open up NFC access.

Beem It allows instant payments between individuals signed up to the service. It can also be used to pay businesses that support Beem It and to split bills.

“We’re excited to bring instant payment technology to all Australians, ensuring that everyone can pay, request and split money via their smartphones, regardless of who they bank with,” Beem It CEO Mark Wood said in a statement.

“Beem It uses real-time banking technology to transfer funds between banks and ensure money doesn’t get in the way of great life moments.”

The service is offering $5 credit as a launch promotion. Beem It has a daily limit of $200 a day for sending money, and $10,000 for receiving money.

Earlier this year Australia’s New Payments Platform has its public launch.

The NPP facilitates real-time payments between banks, as well as additional services such as “data enriched” transactions and PayID, which allows payments to be sent using alternative identifiers instead of BSBs and account numbers.

In Australia, our household surveys also show significant appetite for digital payments, especially via mobile devices, and more than half of households here have not used cash for any transaction in the past month. And its rising. The drive to cashless seems unstoppable.

Yet I got caught out yesterday by the NAB systems failure, which saw their payments and internet banking services wiped out thanks to a power failure in Melbourne. My local garage has a NAB terminal and was unable to process EFTPOS payments. Luckily they had the paper based backup, which took credit cards, for later processing. Then at the local café I could not use person to person digital payments from my mobile – they were only taking cash, so I went to an ATM to find that was not working. Luckily I scraped up the spare cash I had pay for my coffee. An object lesson in frustration, and for some businesses, a loss of business, which granted NAB said they would consider compensating.

And this in the week where Telstra’s whole internet and phone system went down (without an explanation this time – at least they did not blame a lightning strike like the previous episode). And of course CBA’s payment systems had gone down previously.

Reflecting on all this, I am pulled in two directions. I am a fan of a digital migration towards a cashless society, yet it also shows there are potential risks which need to be explored further. In fact, consumers, who prefer digital, might be sleepwalking into future disaster. Time to think harder about the risks of going cashless.

And we are not alone. In some Scandinavian countries, the rush towards a cashless society is also hitting some turbulence. Take Sweden for example. It is one of the most cash-free societies in the world. The proportion of cash payments in the retail sector fell from about 40% in 2010 to about 15% in 2016. Two-thirds of consumers say they completely manage without cash; just as many say they mostly use cards even for payments under $20. More than half the nation’s bank branches no longer take or issue cash. Many stores greet the shopper with notices that they no longer accept hard currency. As a result, the total value of cash payments in the economy has fallen to less than 2% of GDP.

“In the not-too-distant future, Sweden may become a society in which cash is no longer generally accepted,” the Swedish central bank said recently. And in February, the bank warned that Sweden could soon face a situation where all payments were controlled by private sector banks. The Riksbank governor called for new legislation to secure public control over the payments system, arguing that being able to make and receive payments is a “collective good” like defence, the courts, or public statistics.

These comments have brought other concerns about a cash-free society into the mainstream. To put it bluntly, when you have a fully digital system you have no weapon to defend yourself if someone turns it off.

And in addition, no system based on technology is invulnerable to glitches and fraud. In the past year two Swedish banks had problems with card payments and by Bank ID, the digital authorisation system that allows people to identify themselves for payment purposes using their phones. And in addition every transaction can be tracked and recorded, remember Facebook?

Now, the banks recognise that digital payments can be vulnerable, just like cash but argues that they are no more vulnerable than any other method of payment. And they say, it is being driven by the customer preference for convenient payment alternatives.

A recent opinion poll said almost seven out of 10 Swedes wanted to keep the option to use cash, while just 25% wanted a completely cashless society.

So I think it’s time to reconsider the implications of digital payments, not least because payments can be tracked, digital networks appear vulnerable and with ATMs disappearing, it will be harder to get cash when needed.

The government is reportedly considering a new tax on the digital economy. While no details of the tax are available yet, the digital services tax recently proposed by the European Commission may give us an idea what the tax might look like.

In essence, the proposal will impose a 3% tax on the turnover of large digital economy companies in the European Union. Similar ideas have been suggested in the UK and France.

The current international tax system was designed before internet was invented, so this new tax is a response to this problem. Under the current system, a foreign company will not be subject to income tax in Australia unless it has a significant physical presence in the country. The key word here is “physical”.

It is well known that modern multinationals such as Google can derive substantial revenue and profits from Australia without significant physical presence here. It is no surprise that this 20th-century tax principle struggles to deal with the 21st-century economy.

This problem is well known but the solution is far more elusive.

Attempts to tax digital companies

The best solution in response to the rise of the digital economy is to reword the laws to take more into account than the “physical” presence of a company in the international tax regime. However, this reform would require international consensus on a new set of rules to allocate the taxing rights on the profits of multinationals among different countries.

In particular, it would mean more taxing rights for source countries where the revenue is generated. The formidable political resistance is not difficult to imagine.

The OECD has attempted to address this fundamental issue, but in vain so far. Its report on the taxation of digital economy in the Base Erosion Profit Shifting project did not provide any recommendation to improve the system at all. The recent report on its continuing work on the digital economy again shows little progress.

While the EU also recognises that the long-term solution should be a major reform of the international tax regime, the slow progress of the OECD’s effort is seriously testing the patience of many countries. Therefore, the EU has proposed the digital services tax as an “interim” measure.

Google as an example

The Senate enquiry into corporate tax avoidance revealed that Google is deriving billions of dollars of revenue every year from Australia but has been paying very little tax. In particular, the revenue reported to the Australian Securities and Investments Commission in Australia in 2015 was less than A$500 million, with net profits of A$47 million.

The government responded by introducing the Multinational Anti-Avoidance Law in 2016, targeting the particular tax structures used by multinational enterprises such as Google.

Google Australia’s 2016 annual report states that the company has restructured its business. Though not stated explicitly, the restructure was most likely undertaken in response to the introduction of this law.

As a result of the restructure, both revenue and net profits of Google Australia increased by 2.2 times.

However, here is the bad news. Though Google has reported significantly more profits in Australia, the profit margins of the local company remain very low compared to its worldwide group. For example, the net profit margin of Google Australia was 9% while that of the group was 22%.

Of course, a business may have different profit margins in different countries for genuine commercial reasons. However, based on our understanding of the tax structures of these multinationals, it’s likely that significant amounts of profits are booked in low-tax or even zero-tax jurisdictions.

This example suggests that while the Multinational Anti-Avoidance Law is achieving its objectives, it alone is unlikely to be enough.

A digital services tax in Australia

The digital services tax is a turnover tax, not an income tax. This circumvents the restrictions imposed by the current international income tax regime.

The targets of this tax include income of large multinationals from providing advertising space (for example, Google), trading platforms (for example, eBay) and the transmission of data collected about users (for example, Facebook).

If Australia follows the model of the digital services tax, the new tax may generate substantial amount of revenue. For example, Google Australia’s revenue reported in its 2016 annual report was A$1.1 billion. A 3% tax on that amount would be A$33 million.

Along with the digital services tax proposal, the EU proposed the concept of “significant digital presence” as the long-term solution for the international tax system. The exact details are subject to further consultation. However, the relevant factors may include a company’s annual revenue from digital services, the number of users of such services, and the number of online contracts concluded on the platform.

The destiny of this proposal is unclear, but it’s likely to be subject to fierce debate among countries. In any case, the proposals of the digital services tax and the digital presence concept suggest there may be a paradigm shift in the thinking of tax policymakers in response to the challenges imposed by the digital economy that would be difficult, if not impossible, to resist.

Author: Antony Ting, Associate Professor, University of Sydney

An interesting perspective on crypto-currencies from an op-ed by Mr Agustín Carstens, General Manager of the BIS. He says that the short experience of cryptocurrencies shows that technology, however sophisticated, is a poor substitute for hard-earned trust in sound institutions. Perhaps not an unsurprising stance from the central bankers’ banker! As we highlighted yesterday, some central banks are now exploring alternatives via CBDC’s.

How to preserve trust in financial transactions is a tricky business in our digital age. With new cryptocurrencies proliferating, it’s as important to educate the public about good money as it is to build defences against fake news, online identity theft and Twitter bots. Conjuring up new cryptocurrencies is the latest chapter in a long story of attempts to invent new money, as fortune seekers have tried to make a quick buck. It has become the alchemy of the age of innovation, with the promise of magically transforming everyday substances (electricity, in this case) into gold (or at least euros).

Many cryptocurrencies are ultimately get-rich-quick schemes. They should not be conflated with the sovereign currencies and established payment systems that have stood the test of time. What makes currencies credible is trust in the issuing institution, and successful central banks have a proven record of earning this public trust. The short experience of cryptocurrencies shows that technology, however sophisticated, is a poor substitute for hard-earned trust in sound institutions. We will explain this concept further in a special section of our annual report on 17 June.

Recent episodes show how private cryptocurrencies struggle to earn public trust. Cases of fraud and misappropriation abound. Above all, the technology behind cryptocurrencies makes them inefficient and certainly less effective than the digital payment systems already in place. Let me highlight three aspects.

First, the highly volatile valuations of cryptocurrencies conflict with the stable monetary values that must underpin any system of transactions which sustains economic activity. Over the last two decades, consumer price inflation in advanced economies averaged 1.8%. In contrast, over the last three months, the five largest cryptocurrencies have on average lost 21% of their value against the US dollar.

Second, the many cases of fraud and theft show that cryptocurrencies are prone to a trust deficit. Given the size and unwieldiness of the distributed ledgers that act as a register of crypto-holdings, consumers and retail investors in fact access their “money” via third parties (crypto-wallet providers or crypto-exchanges.) Ironically, investors who opted for cryptocurrencies because they distrusted banks have thus wound up dealing with entirely unregulated intermediaries that have in many cases turned out to be fraudulent or have themselves fallen victim to hackers.

Third, there are fundamental conceptual problems with cryptocurrencies. Making each and every user download and verify the history of each and every transaction ever made is just not an efficient way to conduct transactions. This cumbersome operational setup means there are hard limits on how many, and how quickly, transactions are processed. Cryptocurrencies therefore cannot compete with mainstream payment systems, especially during peak times. This leads to congestion, transaction fees soar, and very long delays result.

In the end, one has to ask if cryptocurrencies are an improvement compared with current means of payment. Technological advances can mitigate some of the shortcomings of existing cryptocurrencies, but institution-free technology is unlikely ever to remedy the fundamental problem of recreating trust from a fragmented system of unregulated, self-interested actors. In particular, in a decentralised network of users, nobody has the incentive to stabilise the currency in times of crisis. This can make the whole system unstable at any given point in time.

Admittedly, there are also sobering examples of sovereign monies failing, mostly when public trust broke down – even in recent times. But on the whole, recent decades can be seen as a historically rare period of monetary stability, underpinned by independent central banks.

The technology behind cryptocurrencies could be used in other interesting ways, however. Central banks have long championed the use of new payment technologies – as long as they prove socially useful – in the interests of increased efficiency. One should also note that digital central bank money is not new: it has been quietly enabling some of the most significant innovations in financial plumbing for the last 20 years.

Currently, central banks around the world are working on systems for retail payments that will allow instant transfers, anytime and anywhere. They are also actively testing the distributed ledger technology underlying cryptocurrencies – not as a substitute for the current system, but to build on it. Even in this digital age, trust in the issuing institution matters and will continue to underpin currencies. Central banks, for their part, will have to continue earning that public trust by closely guarding their currency’s value.

There is growing interest in central bank digital currencies or CBDCs.

A central bank digital currency is a digital form of central bank money denominated in the official unit of account for general purpose users. Rather than a full decentralised version of a digital currency, like Bitcoin, a CBDC falls within the control of a countries central bank, and so is caught within their overall supervision and control. There are many variants of a CBDC, which can take several forms with different properties, depending on its purpose.

Central Banks will we suspect use their “normal” financial stability tests when assessing the merits of a CBDC. Is a CBDC is necessary and desirable for ensuring an efficient and robust payment system and confidence in the monetary system. Confidence in the monetary system means that we trust that the value of money will remain stable over time. This confidence is supported by low and stable inflation, the ability to make payments safely and efficiently and the certainty that money is genuine and its issuers are solvent and will honour their commitments.

Last week, Norway’s central bank issued a working paper on CBDCs. The report, prepared by a Norges Bank, investigated aspects they believe should be considered when assessing the issuance of a CBDC. They said that a decline in cash usage has prompted the bank to think about whether at some future date a number of new attributes that are important for ensuring an efficient and robust payment system and confidence in the monetary system will be needed.

The report states that a CBDC could provide customers with an alternative means to store assets. According to Norges bank, the foundation of a CBDC must also not interfere with the ability of the bank and other financial institutions to provide credit. Norges Bank will reportedly continue to issue cash as long as there is demand for it. The working group has only completed the initial phase of studying a potential CBDC, stating: “It is too early to conclude whether Norges Bank should take the initiative in introducing a CBDC. The impacts of a CBDC – and the socio-economic cost-benefit analysis – will depend on the specific design. The design, in turn, will depend on the purpose of introducing a CBDC.”

Sweden is considering the development of an e-Krona saying the use of banknotes and coins is declining in society. At the same time, technological advances with regard to electronic money and payment methods are moving rapidly. The Riksbank has therefore started a project aimed at examining whether the krona needs to be issued in an electronic form, an “e-krona”. No decision has yet been taking on issuing an “e-krona” or on what technical solution would be used.

The Federal Council of the Government of Switzerland requested a report on the risks and opportunities of introducing its own state-backed digital currency, or so called “e-franc.” The proposal also intends to examine and clarify legal, economic, and financial aspects of the e-franc.

The report lays out various scenarios of possible risks and financial stability issues of central bank digital currencies (CBDCs) and describes three potential models of CBDC depending on the sectors that have access to CBDC, from a narrow CBDC where access is limited to banks and non-bank financial institutions (NBFIs), to direct and indirect access extended to households and non-financial firms.

The Financial Institutions Access model is limited to banks and NBFIs, where financial institutions can interact directly with the central bank to purchase and sell CBDC in exchange for eligible securities. Financial institutions are not supposed to provide an asset to households and firms, which are entirely backed by central bank money.

The Economy-wide Access model assumes that access to CBDCs is granted to banks and NBFIs, households and firms. In this way, a CBDC can serve as money for all agents in the economy. While only banks and NBFIs can interact directly with the central bank to buy and sell CBDCs, the report says that “households and firms must use a CBDC Exchange to buy and sell CBDC in exchange for deposits.”

Within the Financial Institutions Plus CBDC-Backed Narrow Bank Access model access is again limited to banks and NBFIs. There is at least one financial institution that acts as a ‘narrow bank,’ which provides financial assets to households and firms that are fully backed by a CBDC but that does not extend credit.

Note also that they are agnostic to the technology that underlies CBDC and the use of distributed ledger technology (DLT) is not assumed.

So the three models of CBDC vary in the sectors that have access to CBDC, from a narrow CBDC where access is limited to commercial banks and NBFIs, a moderate step beyond access allowed to the UK’s current RTGS system, to a system where access is also extended to households and non-financial firms. The latter is an economy-wide system. Second, they vary in whether there exist entities that provide deposit facilities that are fully backed by CBDC (as distinct from deposit facilities fully backed by reserves). Economically these entities are narrow banks. The three models together cover a range of plausible CBDC systems.

They show that for the scenarios of initial CBDC introduction for all models, if the introduction of CBDC follows a set of reasonable core principles, then the banking sector’s two key functions, the provision of credit to borrowers and the provision of liquidity to depositors, are not necessarily curtailed. Some bank deposits may disappear, but, to a first approximation, this can occur without affecting the quantity of aggregate credit or aggregate liquidity. Banks and their customers, through their respective portfolio decisions, control the extent to which depositor switching to CBDC affects the size and composition of bank balance sheets. Banks can continue to play their traditional intermediation role.

Next they turn to the question of confidence loss and layout some core principles

The first core principle is that the interest rate paid on CBDC should be adjustable. This allows the market for CBDC to clear without a need for either large balance sheet adjustments or movements in the general price level.

The second core principle is that CBDC should be distinct from reserves, with the central bank not exchanging reserves for CBDC. This addresses the risk of a ‘run by the back door’, whereby a single bank’s commitment to issue CBDC in exchange for bank deposits, together with its commitment to settle interbank payment in reserves, could in the absence of this condition facilitate a rundown in aggregate reserves and deposits when bank customers seek to switch into CBDC. This core principle also enables the central bank to retain control over the quantity of reserves in the financial system, which has traditionally been a key mechanism through which central banks control policy rates.

The third core principle is that commercial banks should never have an obligation to convert deposits into CBDC on demand. Requiring banks to convert deposits to CBDC on demand opens the door to runs on the aggregate banking system. These runs could be much faster and at larger scale than in the current system, where cash is the only central bank money available to depositors. In such a scenario, there could be substantial operational and political economy barriers to the central bank providing sufficient market-stabilising liquidity support. Such an obligation on banks to guarantee convertibility is therefore highly dangerous. It is also unnecessary. One frequently cited rationale for this obligation is that it is necessary to ensure parity between bank deposits and other forms of central bank money. However, that parity can be achieved in several other ways.

They challenge the assumption that banks should guarantee conversion, noting first that greater vulnerability to aggregate bank runs is unlikely to increase confidence in the banking system, and second that the key pillars supporting confidence in banks are strong prudential oversight, maintenance of adequate capital and liquidity buffers, deposit insurance, and commitment to clear interbank payments in reserves at parity (and thereby facilitate payments), rather than the promise to always pay out central bank money to depositors. To see the latter, consider the hypothetical case where banks commit to exchange deposits for CBDC on demand but have little capital or liquid assets, and are not supported by a deposit guarantee. In this case the commitment is not credible and hence cannot be a source of much confidence.

The fourth core principle, which complements the second and third principle, is that the central bank only issues CBDC against eligible assets, principally government securities but with the definition of eligible assets at the central bank’s discretion. This conforms to current practice for the issuance of central bank money, and is therefore conservative rather than radical. What would truly be radical, and highly undesirable, is guaranteed issuance against bank deposits, which would amount to a guarantee of automatic unsecured lending to banks.

So in conclusion, the report found that, after a first approximation, there is no reason to believe that introducing a CBDC would have an adverse effect on private credit or on total liquidity provision to the economy. Although the report does stipulate that further models and research are necessary to make a more concrete determination.

The Bank of England Paper only studies the balance sheet and financial stability aspects of CBDC. It does not attempt to evaluate whether the introduction of CBDC presents a net benefit to the financial system and society. This is still an open question for many central banks, with the answer likely to vary across countries (due to differences in, for example, the service offering of existing payment systems and the prevalence of cash use).

Finally, it’s worth noting that a few central banks have taken a decision. In 2015, Ecuador issued a US-dollar denominated national digital currency, while more recently the National Bank of Demark and the Reserve Bank of Australia concluded that in their respective economies the potential benefits of introducing a CBDC to households and businesses do not currently outweigh the risks, and therefore they have no plans to introduce one.

An online business lender is aiming to raise around $146million through an initial public offering (IPO).

Prospa is expected to list the ASX on 6 June, offering shares at an offer price of $3.64 per share. The IPO was lodged with the Australian Securities and Investments Commission (ASIC).

The majority of funds raised in the IPO will be used to fund growth in Prospa’s existing business model and for investing in new product categories and expansion into New Zealand.

While there will be no general public offering of shares, offers will include:

An institutional offer, which consists of an offer to Institutional Investors in Australia and certain other geographies

A Retail Offer, consisting of the:

Broker Firm Offer, which is open to Australian retail clients and sophisticated New Zealand retail clients of Macquarie Equities, Crestone and JBWere; and

Priority Offer, which is open to investors chosen by the Company; and

An Employee Offer, which is open to eligible Prospa employees.

The IPO will see long-term, London based venture capital investor Entrée Capital support the offer to maintain its 34% stake in the company.

In addition, Australian based venture capital investors Airtree has invested an additional $3m giving it a stake in the company of 8.4%, whilst SquarePeg has invested an additional $10m, increasing their holding from 3.2% to 4.4%.

Chairman Greg Ruddock said on behalf of the Prospa Board that he was pleased to offer the opportunity to become a shareholder in the company.

He added, “Prospa has flourished by offering fast, flexible loans to Australian small businesses that have historically been underserved by traditional banks. Since inception, Prospa has strategically invested in the two most important parts of our business, people and technology. This offer marks another stage of growth for the company, as we look to expand into new geographies and products.”

Co-CEO Greg Moshal said, “From the very beginning, Prospa has set out to be the market leader at what we do, lending to small businesses. And we have done this by obsessing about our customers and finding new ways to improve their chance of success by designing outstanding new customer solutions. Prospa’s success has been the result of a group of smart, talented and passionate people uniting around a common mission to change the way small businesses experience finance.”

Co-CEO Beau Bertoli added, “We started Prospa in 2012 because it was clear to us there had to be a better way. As first mover in a nascent market, Prospa has led the way in enabling small businesses to succeed. Listed life marks another milestone in our growth, however our approach to business won’t change. We are relentlessly looking for a better way to operate, continuously innovating our products and business model and using data to make great decisions and better manage risk.”

Post-IPO, Airtree and SquarePeg will be escrowed to the end of the forecast period.

Entrée Capital and Prospa’s co-founders Greg Moshal and Beau Bertoli, chairman Greg Ruddock and non-executive director, Avi Eyal (co-founder and Managing Partner of Entrée Capital) will be escrowed until the release of Prospa’s FY19 full year audited results.

Earlier this year Prospa confirmed the appointment of Greg Ruddock to the role of chairman of the board, and Gail Pemberton AO and Fiona Trafford-Walker as independent non-executive directors.

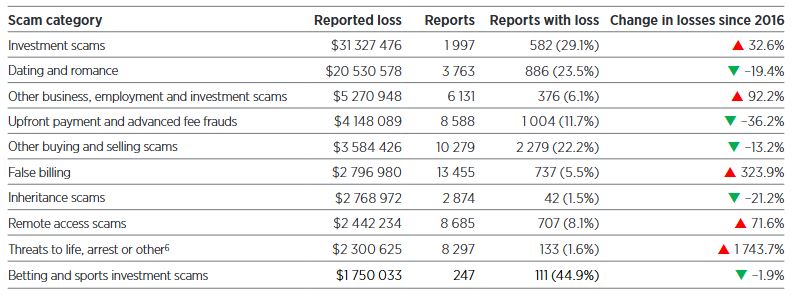

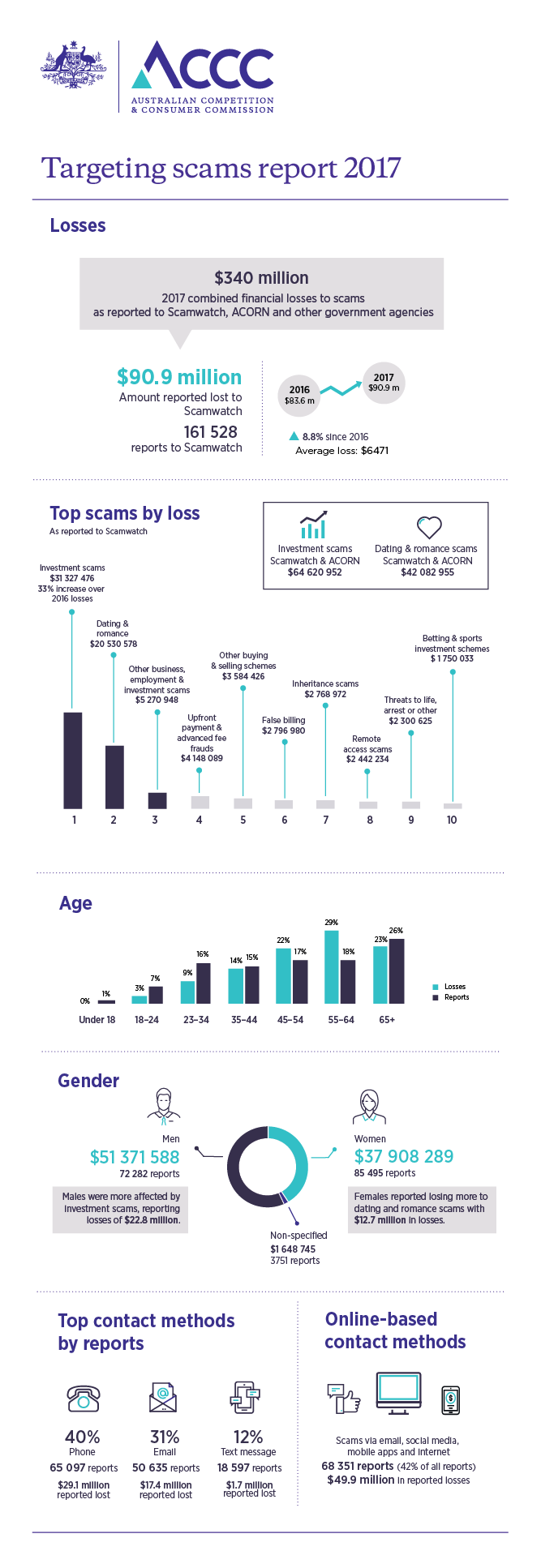

The ACCC says that Australians lost more money to scammers in 2017 than in any other year since the ACCC began reporting on scam activity. According to the ACCC’s ninth annual Targeting scams report more than 200,000 scam reports were submitted to the ACCC, Australian Cybercrime Online Reporting Network (ACORN) and other federal and state-based government agencies in 2017. Total losses reported were $340 million – a $40 million increase compared to 2016.

The top three most reported scam categories of 2017 were phishing, identity theft and false billing scams. Losses to investment scams reported to Scamwatch increased by 33 per cent which translates to an increase in losses of $7.6 million. Combined losses with ACORN reports brings investment scam losses to $64.6 million in 2017, an increase over the $59 million in combined losses reported in 2016. False billing scams reported to Scamwatch increased by 324 per cent, from $659 835 in 2016 to

$2.7 million in 2017. Remote access scams reported to Scamwatch increased by 72 per cent representing an increase in losses of $1 million.

This is the first time reported losses to scams have totalled more than $300 million and demonstrates the increasing impact of scams on Australians. Investment scams topped the losses at $64 million, an increase of more than 8 per cent. Dating and romance scams caused the second greatest losses at $42 million.

“It’s very worrying that Australians are losing such extraordinary amounts to scammers. Based on just the reports provided to the ACCC, victims are losing an average of $6500. In some cases people have lost more than $1 million,” ACCC Deputy Chair Delia Rickard said.

“Some scams are becoming very sophisticated and hard to spot. Scammers use modern technology like social media to contact and deceive their victims. In the past few years, reports indicate scammers are using aggressive techniques both over the phone and online.”

Today marks the beginning of Scams Awareness Week 2018 and this year Scamwatch is asking people to “Stop and check: is this for real?” when they’re contacted by scammers who are pretending to be from well-known government organisations or businesses.

Scamwatch received almost 33,000 reports of these threat-based impersonation scams in 2017. Over $4.7 million was reported lost and more than 2800 people gave their personal information to these scammers.

“These scams can be very frightening. For example, scammers will impersonate the Australian Taxation Office and threaten people with immediate arrest unless they pay an outstanding tax bill. They may pretend to be from Telstra to try to hack into your computer or from Centrelink promising extra payments in return for a ‘fee’,” Ms Rickard said.

“Scammers scare us or butter us up with promises of cash because they know it clouds our judgement. People get so worried about being arrested they don’t question if the person threatening them is genuine.”

“If you’re being threatened, take a deep breath, and ask yourself if the call makes sense. The ATO will never threaten you with immediate arrest; Telstra will never need to access your computer to ‘fix’ a problem; and Centrelink will never require a fee to pay money it owes you. Finally, none of these organisations will ask you to pay using iTunes gift cards,” Ms Rickard said.

“If something doesn’t feel right, hang up the phone or hit delete. If the person said they were, for example, from Telstra or the ATO, find the phone number for that organisation online or in the phone book, call them and let them know about the call you received. They’ll let you know if it’s genuine or a scam.”

The ACCC encourages people to visit www.scamwatch.gov.au (link is external) to report scams so we can warn others about them and learn more about what to do if they’re targeted by scams.

Centrally cleared cryptocurrency derivatives could be a real-world test of clearinghouses’ margining and default procedures, particularly if derivative notional volumes increase and cryptocurrencies exhibit heightened price volatility, says Fitch Ratings.

Although they have largely avoided direct exposure to cryptocurrencies, banks’ role as clearing members creates a secondary channel for cryptocurrency risk. This could indirectly affect banks under more extreme stress scenarios, such as if margining and clearinghouse capital contributions prove insufficient to absorb counterparty defaults.

A dramatic increase in financial institutions’ exposure to cryptocurrency derivatives could challenge clearinghouses and large financial institution clearing members in ways beyond those typically associated with the introduction of new market products. Cryptocurrencies are prone to extreme price volatility, which has been exacerbated by a nascent, unregulated underlying market with a limited price history and without generally accepted fundamental valuation principles. These factors complicate margin calculations, particularly related to short positions, for which losses cannot be capped. Inadequate margins may lead to use of clearinghouses’ collective funds to mitigate losses, thus calling upon the resources of non-defaulting clearing members, including many of the world’s largest banks and other financial institutions.

Bitcoin futures are cash-settled derivatives (i.e. without delivery of the base asset) that allow investors to assume long and short exposures to bitcoin prices without directly facing the cryptocurrency itself. In December 2017, CME Group and CBOE introduced the trading of bitcoin futures under the tickers BTC and XBT, respectively. BTC contracts are cleared through CME Clearing, while XBT contracts are cleared through Options Clearing Corporation (OCC).

As of May 9, 2018, open interests in XBT and BTC were modest at 6,287 and 2,479 contracts, respectively, worth approximately $59 million and $116 million, respectively. However, if challenges associated with trading the cryptocurrency are addressed, including uncertainty over regulatory, tax and legal frameworks, cryptocurrency derivative volumes could grow.

Clearinghouses have imposed high initial margin requirements, as well as price and position size limitations, suggesting a cautious approach thus far to trading cryptocurrency derivatives. As of May 9, 2018, initial (maintenance) margin requirements at CME were 43% of the associated notional amount, while at OCC the percentage was 44%, up from around 30% at the derivatives’ introduction in December 2017. Position limits at both exchanges are limited to 5,000 contracts in total or 1,000 in spot/expiring contracts. Consistent with price limitations for equity indexes, the maximum price limits at CME and CBOE are set at 20% above or below the previous day’s closing price, and trading is not permitted outside this band. There are also special price fluctuation limits set at 7% and 13%, which lead to temporary trading suspension.

The CME and OCC have not yet established separate legal entities or default funds for cryptocurrency derivatives, instead allocating exposure to the same default funds as equity indexes. This is understandable given the cost inefficiencies of establishing entities and default funds for what is currently a relatively low volume business. Nevertheless, a member default from losses on cryptocurrency derivatives may cause disruptions in other cleared products. Should centrally-cleared cryptocurrency derivatives materially grow, Fitch would expect clearinghouses at a minimum to establish separate default funds in an effort to isolate and mitigate associated risks.

Now, today I am not going to discuss the mechanics of the digital currency, there are plenty of others who have done that; nor am I going to discuss the limited supply, which is mirroring gold, other than to note this one of the fundamental design criteria of the crypto currency.

But institutional investors are getting more interested.

For example, Goldman Sachs announced it will be opening a crypto derivatives trading desk “within weeks,” as well as recently hiring a cryptocurrency trader as vice president of their digital asset markets. It will trade Bitcoin futures in a principal, market-making capacity and will also create non-deliverable forward products.

Then last week there was some more potentially important news out of the USA. There are rumours that the New York Stock Exchange may be planning to offer ‘Physical Delivery’ of Bitcoin. If this is true, it could mark a significant transformation in the role of digital currencies like Bitcoin.

The suggestion from unnamed “multiple sources” is that NYSE’s parent company Intercontinental Exchange or ICE is planning to offer Bitcoin (BTC) swap contracts but these contracts would be settled with the delivery of Bitcoin itself. Think about that, a mechanism to allow the physical delivery of a digital currency. If this IS true, this would have significant consequence for the future of crypto.

While there are Bitcoin futures contracts currently being offered on Chicago based CME Group derivatives marketplace or CME (since December 2017) and Chicago Board Options Exchange CBOE, these are ultimately settled in dollars.

The suggested crypto swap contracts would be settled in Bitcoin, and this would be a significant milestone which may signal a major Wall Street adoption of crypto.

Significantly it could mean that the ICE has a custody solution. As Bitcoin are generally bearer instruments it means you have to have a third-party custody option if institutional investors are going to get seriously involved.

There are so called “Cold storage custodian solutions” offered by small operators.

It’s not clear whether ICE is likely to build an in-house cold storage solution or to outsource it. In fact, ICE has made no comment at all on this, so it might be just speculation.

But here’s the thing, if ICE can offer a custodian solution that meets SEC rules and compliance requirements, this could “open the floodgates” to institutional capital, resulting in some “big price moves” in the crypto markets.

A custody solution would also open the door for pensions and endowments and so become an emergent asset class…most obviously at the expense of gold.

The Bitcoin price is still sitting well below the previous highs and the markets did not really respond to the rumours. But if this is true, then it may mark a significant inflection point in evolution of crypto. It might go mainstream.