Journalism is in an existential crisis: revenue to news organisations has fallen off a cliff over the past two decades and no clear business model is emerging to sustain news in the digital era.

In the latest in our series on business models for the news media, journalist and academic Jane Singer looks at the use of micropayments.

Once upon a time, the gap between the relatively low supply of something in high demand – timely and trustworthy information – generated enormous profits for news publishers. But over the past 15 years or so, the digital, social and mobile revolutions have all but obliterated that gap.

In response, publishers have scrambled for new revenue streams, and much recent attention has turned to “micropayments” – the payment of a very small amount to access a comparably small bit of content, such as a single story.

The traditional media world is one of bundled information, with a lot of diverse content in one package that aims to provide something for everyone. The digital world, though, is an unbundled one. It enables each individual to select one item at a time from among the billions of things on offer. Are we willing to pay for this content? Sometimes yes – see iTunes.

But the question for news outlets is whether personalised news can follow the lead of personalised entertainment in generating interest and – in their fondest dreams – income.

Blendle is poised to take on the US market.Blendle

So far, news micropayment initiatives are – at best – a work in progress. The most buzz has been around a Dutch service called Blendle, which claims half a million registered users in Europe and is poised to tackle the US market. Most items on Blendle, which come from diverse outlets, cost between 10 cents and 90 cents and come with a money-back guarantee: you only pay for stories you actually read – and if you then don’t like them, you can ask for your pennies back.

The slick interface appeals to fans, as does the lack of advertising (and advertising’s attendant clickbait). But others have flatly predicted the concept is doomed to fail. News consumers want to pay nothing, they say, and even a very small amount of money is not nothing.

Who pays the piper?

But perhaps the model here is not an “iTunes for journalism”, if by journalism we mean big-name branded content. Perhaps a crowdfunding site such as Kickstarter offers a better template – the ability for users to stack their coins behind ideas they want to see developed rather than existing stories they want to read.

Experiments with crowdfunded journalism have proliferated. One flavour is essentially a low-cost membership model that allows its member – or donors – to steer journalists to topics of interest. MinnPost, a non-profit site in Minnesota, has made good use of this approach. For instance, a New Americans beat, which covers the state’s immigrant and refugee communities, was launched last October based on pledges from interested donors.

In Scotland, a new investigative journalism site called The Ferret also pursues topics that its users say they want; fracking was an early example. And in the Netherlands, de Correspondent drew donations of more than a million euros in just eight days simply on the promise of delivering high-quality stories about important topics rather than “the latest hype”.

The other approach reverses the process, in a way, and is closer to the familiar crowdfunding concept – journalists propose ideas they would like to pursue and users back the ones they like. Stories that meet their funding target get written; those that don’t, don’t. Perhaps the most innovative example came from a British site called Contributoria, backed by the Guardian Media Group. Over a period of 21 months in 2014 and 2015, Contributoria published nearly 800 articles on topics from urban regeneration in Beirut to a day in the life of a bookie; its writers earned a total of £260,000 over that time, most of it built up from quite small individual payments.

Sustainability

However, such experiments have proved hard to sustain. Contributoria closed in October 2015, with its co-founder declaring that crowdfunding was just one piece of the puzzle. What the initiative really showed, he told journalism.co.uk, was that people have a “voracious appetite … to be part of the journalism process, including the way it gets financed”.

Perhaps that is, for now, the takeaway point on micropayments. The desire being given voice is less about paying for journalism than for having a stake in it. News organisations fervently hope that stake will be financial, but for users, “ownership” of the news seems more important than the payment involved.

As information proliferates wildly, consumers are saying they want a sense of control over it. Digital media gives them the ability to be reporters, but mostly, they seem to want to be editors: the gatekeepers who decide what news they will see by commissioning a freelance article, or steering an investigative team toward a topic, or engaging with this niche news app but not that one.

Getting the mix right

For news organisations, then, micropayments are just one option among many in a fragile and fractured digital ecosystem – something to add to the revenue mix if doing so requires only small investments of time, effort or money.

While experimentation is all to the good, the pay-off from this option seems inherently small. The vast majority of online users do not pay now for digital news and have no plans to change their ways. There’s no evidence of a massive demand from users for the ability to pay upfront to read news content – and, even if there were, the small amount of revenue generated on any given day would fluctuate considerably depending on what was on offer. This is not the most desirable funding model for organisations that need a stable financial base to support staff, infrastructure and the ongoing ability to hold the powerful to account.

The reverse option – enabling news consumers to steer the direction of journalistic investigations – seems more plausible and the various non-profit enterprises I’ve mentioned are among those offering examples of ways this might work.

But news users aren’t the only ones who like to be in control. Journalists tend to be fiercely committed to the notion of editorial independence – which is another way of saying that they like to decide for themselves what is and isn’t news. Whether they will be willing to share that control – and, if so, what they might be able to extract from users in exchange – remains to be seen.

Author: Jane B. Singer, Professor of Journalism Innovation , City University London

Google had barely dipped a toe in the mortgage business, but it appears the tech giant is getting out.

Last November, Google launched Google Compare for mortgages, an online tool that allowed home buyers to find and compare home loans. The product was initially available only in California, and joined other Google Compare products that allowed consumers to find and compare credit cards and various types of insurance. There was talk that Google Compare could have eventually entered the Australian market as well.

Google didn’t actually fund mortgages, but it did register as a licensed mortgage broker, according to a CNN report. The company had hoped to use its global reach to provide consumers with niche products and financial services, according to a Wall Street Journal report.

But it appears the Compare product line hasn’t been as successful as the search engine titan had hoped. According to the Journal, Google struggled to sell ads on Compare – and the largest lenders and insurers simply declined to come on board.

In an email acquired by the website Search Engine Land, Google informed its partners that all Compare products – mortgage, insurance and credit card – would begin winding down immediately and shutter for good on March 23.

“Despite people turning to Google for financial services information, the Google Compare service itself hasn’t driven the success we hoped for,” the email stated. “We greatly appreciate your partnership and understand that this decision will be disappointing to some. But after a lot of careful consideration, we’ve decided that focusing more intently on AdWords and future innovations will enable us to provide fresh, comprehensive answers to Google users, and to provide our financial services partners with the best return on investment.”

The Compare site was always a risk. According to a Fox Business report, analysts warned at the outset that the product, by allowing consumers to buy mortgages and insurance policies directly, had the potential to anger lenders and insurers who were major advertising clients of Google.

Google has not yet officially commented on the shutdown.

Google’s lead generation product known as Google Compare, will start sunsetting this week.

In an email sent to partners and acquired by Search Engine Land, the Google Compare Team told Compare partners on Monday night that the product will start to wind down on Tuesday, February 23, 2016. Google Compare will shut down completely in both the US and UK — the two markets where Compare is offered — one month later on March 23.

The email to Compare partners:

From: Google Compare Team Subject: An Update on Google Compare

Dear Partner,

Beginning on February 23, 2016, we will start ramping down the Google Compare product, which is currently live in both the US and UK. We plan to terminate the service as of March 23, 2016. As you know, Google Compare (formerly Google Advisor in the U.S.) has been a specialized, standalone service that enables consumers to get quotes from a number of providers for financial products such as car and travel insurance, credit cards and mortgages.

Despite people turning to Google for financial services information, the Google Compare service itself hasn’t driven the success we hoped for. We greatly appreciate your partnership and understand that this decision will be disappointing to some. But after a lot of careful consideration, we’ve decided that focusing more intently on AdWords and future innovations will enable us to provide fresh, comprehensive answers to Google users, and to provide our financial services partners with the best return on investment.

We’re grateful for all the feedback that you have provided over the course of this product’s development, and we are looking forward to partnering with you to achieve greater success in the future.

We will work with you during this transition and beyond. Please reach out to your Google representative if you have any questions and to discuss the next steps.

The Google Compare Team

Google has confirmed the email’s authenticity.

The company only recently began rebuilding the Compare product from the ashes of the Advisor program in the US. The single piece left standing from that initial effort was the credit card offering — savings accounts, CDs and mortgages had all discontinued. Compare for Auto Insurance launched just last March, starting in California. Then Google relaunched Compare for Mortgage quotes in November with Zillow and Lending Tree among the launch partners. Both of those relaunches had limited roll outs. In the UK, Google Compare has been running since 2012 for car insurance, mortgage rates, credit cards and travel insurance.

A Google spokesperson told Search Engine Land that while searches on these queries remained high, the product didn’t get the traction it hoped for and revenue was minimal. That’s in part due to the limited availability of the products in both the US and the UK.

In the UK, the Compare product also came under scrutiny in 2014 by the Financial Conduct Authority, the UK financial services industry regulator, when comparison sites complained Google was competing unfairly by placing its own product at the top of the search results. However, any legal concerns did not play a role in the decision to close Compare, we’re told.

What’s next? Google says the focus will primarily be on AdWords and transitioning partners to standard ad products. However, it may still focus on the space and look at new product avenues.

While the move will come as a surprise to many outside the company, apparently internally this decision to terminate Compare is not coming as a shock. The Google spokesperson said the company will help Googlers currently working on Compare find new roles within the company.

The Australian payments system is evolving, both in terms of some innovative new payment instruments that are on their way and the declining use of some of our older or legacy payment instruments. Tony Richards RBA Head of Payments Policy Department RBA, spoke at the Payments Innovation 2016 Conference on this evolution.

There is a lot happening in the payments industry at present, so my sense is that it would be premature to have a serious discussion about possibly phasing out cheques before the implementation of the New Payments Platform (NPP), which is scheduled to begin operations in late 2017. But if this conference was to revisit this issue in early 2018 with the NPP up and running, it should find significant new payments functionality in place. This will include the ability for end-users to make real-time transfers with immediate availability of funds, to make such transfers on a 24/7 basis, to attach data or documents with payments or payment requests, and to send funds without knowing the recipient’s BSB and account number. These are all aspects that match or exceed particular attributes of cheques.

In addition, by early 2018 another two years will have passed and there will no doubt have been a significant further decline – based on current trends, a further 30 per cent or so – in cheque usage.

By that point, more organisations and individuals will have further reduced their cheque usage. The Bank has recently been doing some liaison with payment system end-users in our Payments Consultation Group and has heard some impressive accounts about how some of the major Commonwealth government departments and some large corporates have largely moved away from the use of cheques. Cheque usage in the superannuation industry has also fallen very significantly as part of the SuperStream reforms.

A shift away from the use of bank cheques is also underway in property settlements. On average, there are around 40 000 property transactions in Australia each month, plus a significant number of refinancings, with most of these requiring at least a couple of cheques for settlement. However, starting in late 2014 and after much preparatory work, electronic conveyancing and settlement is now feasible. This is being arranged by Property Exchange Australia Ltd (an initiative that includes several state governments and a number of financial institutions), with interbank settlement occurring in RITS, the Reserve Bank’s real-time gross settlement system. Volumes have risen steadily and by late 2015 the number of property batches settled in RITS – each batch typically corresponds to a single transaction or refinancing – had reached nearly 4 000 per month. This trend is expected to continue.

In addition, the Bank’s Consumer Use Survey indicates that usage of cheques is falling rapidly for households of all ages. Our survey from late 2013 confirmed that older households continue to use cheques more than younger ones. However, older households are also reducing their use of cheques significantly. And with more and more older households now using the internet, their use of cheques is likely to continue falling. Indeed, I’m sure we all have a story about an older family member or friend who has recently bought or received a tablet or notebook and discovered the benefits of being online.

Graph 8

Graph 9

We will get a further reading on households’ use of cheques and other payment instruments in the Bank’s next Consumer Use Survey, which – if we follow the timetable of recent surveys – will be published in the first half of next year based on data collected late this year.

More broadly, as the industry starts to think about options for the cheque system, it will be important to make sure that those parts of the community that still use cheques are fully consulted so that we can be sure that their payment needs are met by other instruments. This is likely to involve consultations with organisations representing older age groups, the non-profit sector and those in rural Australia.

Cash

Discussions about the declining use of cheques sometimes also touch upon the declining use of cash.

Because transactions involving cash typically do not involve a financial institution, data for the use of cash are actually quite limited. However, one good source of data on the use of cash by individuals is the Bank’s Consumer Use Study. Our most recent study, in late 2013, showed that cash remained the most important payment method for low-value transactions (around 70 per cent of payments under $20). However, it confirmed that the use of cash had declined significantly, with the proportion of all transactions involving cash falling from 70 per cent in the 2007 survey to 47 per cent in 2013.

More recent data on the transactions use of cash are not available, though the ongoing fall in cash withdrawals from ATMs and at the point of sale suggest that it has continued. In addition, the continuing strong growth of contactless transactions and the growing acceptance of cards for low-value transactions are also suggestive of a further decline in the use of cash.

Graph 10

Graph 11

However, that is where the parallels with cheque usage end. While the use of cash in transactions has been declining, the demand to hold cash has continued to grow. This is the case for low denomination banknotes as well as high denomination ones. Indeed, in recent years there has been a modest increase in the rate of growth of banknotes on issue, to an annual rate of around 7 per cent over the past couple of years. More broadly, over the longer term, growth in banknote holdings has been largely in line with nominal growth in the overall economy.

Graph 12

Graph 13

The growing demand for holdings of cash suggest that it continues to have an important role as a store of value and there is some evidence – from demand for larger denomination notes – that this increased following the global financial crisis. So, despite the decline in use in transactions, cash is likely to remain an important part of both the payments system and the economy more broadly for the foreseeable future. In particular, significant parts of the population appear to remain more comfortable with cash than with other payment methods in terms of ease of use for transactions or transfers, as a backup when electronic payment methods may not be available, or as an aide for household budgeting.

Given the important ongoing role of cash in the payments system, the Bank is currently undertaking a major project to upgrade the existing stock of notes. Counterfeiting rates of the current series of banknotes remain low by international standards but have been rising and there are some signs that the counterfeiters are getting a bit better with new and cheaper scanning, printing and image manipulation technology. Accordingly, the program for the next generation of banknotes includes major security upgrades that should ensure that Australia’s banknotes remain some of the world’s most secure. The first release of the new banknotes will occur in September this year, with the release of the new five dollar note.

Australia is not alone in continuing to invest to ensure that the public can continue to have confidence in its banknotes. The United States has also done so recently, and Sweden – which is often cited as being furthest along the path to a cashless or less-cash society – is also in midst of introducing a new series of notes.

Digital currencies and distributed ledgers

As the use of cash and cheques continues to fall, the Bank will – subject to there not being any overriding concerns about risk – be agnostic as to what payment methods replace the legacy systems, consistent with its mandate to promote competition and efficiency.

In the short run, it is likely that we will see further growth in the existing electronic payment methods, including payment cards in their various form factors. In the medium term, it is likely that we will see growth in new payment methods and systems, including those that will be enabled by the NPP.

Let me stress that the Bank has not reached a stage where it is actively considering this, but in the more distant future it is even possible that we may we see a digital version of the Australian dollar. As the Bank has noted in the past, it seems improbable that privately-established virtual currencies like Bitcoin, with its significant price volatility, could ever displace well-established, low-inflation national currencies in terms of usage within individual economies. Bitcoin has, however, served to stimulate interest in the potential offered by distributed ledgers, extending to the possibility of central-bank-issued digital currencies. A plausible model would be that issuance would be by the central bank, with distribution and transaction verification by authorised entities (which might or might not include existing financial institutions). The digital currency would presumably circulate in parallel (and at par) with banknotes and other existing forms of the national currency.

A few countries have explicitly discussed the possibility of digital versions of their existing currency. Both the Bank of England and Bank of Canada have indicated that they are undertaking research in this area. And a recent announcement from the People’s Bank of China indicated that it has plans for digital currency issuance, though few specifics were provided.

The Bank will be interested to see what proves to be possible and what proves to be problematic, as countries consider going down the path of digital currency issuance. Given the various cybersecurity and cryptography risks involved, my personal expectation is that full-scale issuance of digital currency in any country, as opposed to limited trials, is still some time away. And I think it remains to be seen if there is real demand for a digital equivalent of cash and what it might offer end-users relative to what will be offered by the various forms of real-time payments that are being developed in many countries through projects like the NPP.

I should also touch briefly on another potential application of blockchain or distributed ledger technologies, namely in the settlement of equity market transactions. As the overseer of clearing and settlement facilities licensed to operate in Australia, the Bank obviously has a keen interest in the plans of the ASX Group to explore the use of distributed ledgers. Along with the Australian Securities and Investments Commission and other relevant public sector organisations, we will be working closely with ASX as it considers whether a distributed ledger solution might be the best way to replace its existing CHESS infrastructure.

Review of Card Payments Regulation

I will conclude with a few comments on the ongoing Review of Card Payments Regulation.

The Bank issued a consultation paper containing some draft changes to standards in late 2015. It has received substantive submissions from 43 different stakeholders, with a number of parties providing both a public submission and additional confidential information. 33 non-confidential submissions have been published on the Bank’s website.

The submissions indicate that most end-users of the payments system are broadly supportive of the Bank’s reforms over the past decade or more. Some submissions have indeed suggested that the Bank could have gone further in its proposed regulatory changes. Financial institutions and payment schemes have expressed a range of views. For the most part they have recognised the policy concerns that the Bank is responding to. In some cases there is a fair bit of common ground in areas where they have made suggestions for changes to the draft standards, but in others there are conflicting positions that correspond to the different business models of the entities that have responded to consultation.

The Payments System Board discussed the Review at its meeting last Friday, focusing on issues that stakeholders have highlighted in submissions. As we always do when regulatory changes are proposed, Bank staff will be meeting with a wide range of stakeholders to discuss submissions. Indeed, we have already had a significant number of meetings, sometimes multiple meetings with particular firms as they were preparing their submissions.

Some of the issues to be explored in consultation meetings include: the treatment of commercial cards and domestic transactions on foreign-issued cards in the interchange benchmarks; the proposed shift to more frequent compliance to ensure that average interchange rates remain consistent with benchmarks; and the calculation of permissible surcharges for merchants (such as travel agents or ticketing agencies) that are subject to significant chargeback risk when they accept credit or debit cards.

One other issue that I would like to flag ahead of our consultation meetings relates to the proposed reforms to surcharging arrangements. The Bank’s proposed new surcharging standard has been drafted to be consistent with amendments to the Competition and Consumer Act 2010 which were passed by the House of Representatives on 3 February and by the Senate yesterday.

The proposed framework envisages that merchants will retain the right to surcharge for expensive payment methods. However, the permitted surcharge will be defined more narrowly as covering only the merchant service fee and other fees paid to the merchant’s bank or other payments service provider. Acquirers would be required to provide merchants with easy-to-understand information on their cost of acceptance for each payment method, with debit/prepaid and credit cards separately identified. The draft standard would require that merchants would receive an annual statement on their payment costs which they could use in setting any surcharge for the following year. The information in these statements should allow the Australian Competition and Consumer Commission (ACCC) to easily investigate whether a merchant is surcharging excessively.

The objectives of the proposed changes to the regulation of surcharging received widespread support in submissions. However, a number of financial institutions have argued that it would be difficult to provide statements to merchants on their average acceptance costs for each payment system. Some have said that their billing process draws on multiple systems within their organisations (and sometimes from third parties), so that it is not straightforward to provide the average cost information proposed by the Bank. Some have indicated that they do not currently provide annual statements to merchants, so this would be a significant change. Accordingly, a number have suggested that they would prefer a significant implementation delay before they are required to provide merchants with the desired transparency of payment costs. Bank staff will be testing these points in our consultation meetings with acquirers. In doing so, we will be looking to see what might be done to ensure that the standards can take effect as soon as possible, in order to meet community expectations about the elimination of instances of excessive surcharging.

More broadly, the Board also discussed a possible timeline for concluding the Review. The Bank’s expectation is that a final decision on any regulatory changes should be possible at the May meeting. It is too soon to give much guidance on the date when any changes to the Bank’s standards might take effect, but the Board recognises that an implementation period will be necessary for the industry.

As part of its innovation agenda the Coalition government is offering a tax offset of 20 cents for every dollar invested into a startup, as well as an exemption from capital gains tax for up to 10 years. However, it has emerged that this incentive could be limited to only ‘sophisticated’ investors, defined as those earning more than $250,000 per annum or having a net worth of more than $2.5 million.

Placing this restriction on startup investment could potentially disadvantage a key group of seed capital providers namely family and friends or informal investors. Family and friends provided $66 billion of startup capital to emerging ventures in the United States This is about three times more than either venture capitalists or professional angel investors.

Many of today’s largest listed US companies took seed capital from informal investors. For example Whole Foods Market, a $10 billion American organic food company, was started with founder savings and capital provided by family and friends.

These investors each provide anywhere between $1,000 to $30,000 in seed funding, yet many of them would not qualify as sophisticated investors under the Australian government’s definition.

Australian startups face serious challenges in accessing capital at almost every stage in their growth cycle. In particular, difficulties in accessing seed capital, needed to help turn an idea into an operating business, appears to be a critical road block for many aspiring Australian entrepreneurs.

For example, one in five startups cite restricted access to capital as a major barrier to innovation.

So where can startups access very early stage capital? It appears the sources are limited. The latest data from the Australian Venture Capital Association shows that very few seed investments are made in Australia by venture capitalists.

Further, the angel and incubator community is only just emerging, with only about 12 active groups across the country. This further points to the important role that informal investors can play in filling the capital cap that occurs at a venture’s seed stage.

It is true that informal investors stand to lose a greater proportion of their wealth in comparison to high net worth individuals when investing in startups. However another important innovation agenda reform, equity crowdfunding whereby ordinary mum and dad investors can take an equity stake in a startup through an online portal, would allow them to diversify their risks across many ventures, beyond those in which they have personal connections.

With this in mind, there are several reasons to believe that encouraging, rather than penalising small unsophisticated investors, is an important step to help young Australian startups to grow.

Family and friend investors have a personal connection with the founder, and typically will invest out of loyalty, trust and a belief in the founder’s ability. Such relationship characteristics are difficult to replicate with professional investors, who will often price down a company’s value to account for the possibility of moral hazard or unscrupulous founder motives.

In fact, if a start-up can grow through family and friend investments, often venture capitalist and angels become more inclined to offer follow-on funding, because the fact that informal investors have put their trust (and money) in the founder is a strong signal of the entrepreneur’s integrity and ability.

Bringing on formal or sophisticated investors too early can also stifle innovation. Venture capitalists are certainly not patient. They look for an exit in five years. Angel investors are a little more patient, but still look at a 10 year time frame. Often developing an innovative business can take much longer. For example, Glenn Martin the founder of Martin Jetpack, a Kiwi startup that listed on the ASX last year, first started work on the jet pack in 1981.

Further, a slower start to a venture is often a safer start, where the entrepreneur can take a “try it, fix it” approach and has ample opportunity to correct errors from poor decisions. Informal investors are more likely to be hands-off in their investment approach and thus far more likely to tolerate such an uncertain environment.

On the other hand, professional investors are much more hands-on and may prefer the safe proven routes learnt from previous investments, when in fact an experimental try-it, fix-it approach may be more conducive to innovation.

In order to ensure that our taxation system creates incentives that promote a successful startup ecosystem, careful consideration should be given to how early stage ventures are developed in other successful startup environments.

The Australian government’s efforts to recently secure a “landing-pad” in San Francisco’s highly successful RocketSpace hub, is exactly the kind of initiative that will help Australians learn how to foster a more vibrant domestic startup ecosystem.

While this will not directly address the seed capital gap, helping founders to access valuable networks and to develop their ideas through co-working with others, will certainly enhance their future capital raising capabilities.

Author: Jason Zein, Associate Professor, UNSW Australia

In the United Kingdom, Transport for London (TfL) enables people to pay for their tube, train or tram journeys with a tap of their bank cards and this contactless payment now represents 25% of all (TfL) pay-as-you-go transactions. From 2018 New York subway and bus travellers are expected to be able to pay with their contactless bank cards or mobile phones.

And in Australia both the volume and value of cash withdrawals from the ATM network continue to fall from their peak in 2008, despite an ever-increasing number (now over 31,000) of available ATMs. Indeed figures released in February 2016 by the Reserve Bank of Australia (RBA) show consumers withdrew an average of A$11.7 billion a month from ATMs in 2015, down 1.7% from 2014.

Cash not done yet

And yet in other countries, cash is still king. Japan is still heavily reliant on cash for everyday purchases in retail outlets and restaurants. According to the Bank for International Settlements’ statistics on payments for 2014, there is US$6,429 of banknotes and coins in circulation per person in Japan, compared to US$2,459 for Australians and US$1,588 for the British.

Of further interest is that in Australia by 2014, the total volume of notes on issue was A$60.8 billion, with 92% of this total being in the high denomination A$50 and A$100 notes. According to data from Retail Banking Research, global ATM cash withdrawal volumes grew by 7% in 2014 and the upsurge in usage was most evident in the Asia-Pacific, Middle East and Africa regions.

So how to explain this seeming dichotomy between the holding and use of cash and the use of cards or mobile phones to make payments? Well as human beings we seem to have a psychological relationship with cash, that gives it an enduring appeal.

Cash is widely accepted; it is easy to carry; it is untraceable and it is reliable in times of crisis. People may be particularly attracted to notes because of the way they look and feel and because they want to store their wealth in physical objects, as the world around them becomes more unstable. This trust in “real currency” could explain the large increase in demand for cash during the global financial crisis, as people sought the “comfort” of a wad of banknotes.

Cash can also be used to avoid paying taxes; who amongst us has never used the words “Would that be cheaper for cash?”. The use of cash supports the “black” or “grey” economy, where tax evasion requires untraceable transactions. It is also more than useful where illegal activities produce wealth that needs to be kept secret from the authorities. Perhaps this helps to explain the proliferation of A$100 notes in circulation, but often rarely actually seen in circulation?

Despite the growth of card payments; the arrival of Android Pay, Apple Pay and Samsung Pay and the cryptocurrencies such as Bitcoin, cash is still here and here to stay.

Author: Steve Worthington, Adjunct Professor, Swinburne University of Technology

ANZ today launched its own mobile payments app giving customers the freedom to tap their phone for purchases and cash withdrawals in a quick and secure format. Customers with an Android smartphone can download ANZ Mobile Pay from today and turn their phone into a virtual credit or debit card with the broadest range of cards on offer.

ANZ Managing Director Products and Marketing Matt Boss said: “This new app is another demonstration of ANZ’s commitment to providing customers with innovative solutions to make their lives easier.

“ANZ Mobile Pay delivers a payments solution for our customers to help them take full advantage of the rapidly changing digital environment we live in, including the ability to withdraw cash from contactless-enabled ANZ ATMs with a tap of their phone.

“Customers using ANZ Mobile Pay will be able to add their existing credit or debit card, and then simply tap their mobile phone for purchases at contactless retail locations anywhere in the world with the security we provide for all online and digital transactions,” he said.

“Given Australians are already the most prolific users of contactless payments in the world and the fact that Android is a major player in the local smartphone market, we believe ANZ Mobile Pay will be a popular addition for many of our customers.”

ANZ Mobile Pay allows customers to:

Add a range of ANZ Visa and American Express® credit cards, as well as ANZ Visa Debit cards

Choose the way you pay with three payment options: Wake to Pay, Launch to Pay and Passcode to Pay

Enter your PIN for all payments over $100

Withdraw money at supported contactless-enabled ANZ ATMs

ANZ Mobile Pay is available for download from the Google Play store from today. Once installed, customers just need to tap their card against the phone, then enter their date of birth and mobile number, and finally choose their preferred payment option

Optus have announce you can Visa payWave with your mobile. If you have an Optus mobile service, a compatible mobile and the app, you can get Cash by Optus. Use the Cash by Optus™ app with one of our payment accessories or specially designed SIMs to pay for purchases with just the wave of your hand. Just link the app to your bank account, and you can make payments up to $100 at a time wherever you see Visa payWave.

They are offering a range of payment accessories. A payment accessory is an Optus issued NFC-enabled device which can be used to enable you to make contactless payments. Payment accessories can be in the form of a sticker, band or other device that Optus may issue. You can use it to make contactless payments just as usual. Simply tap the payment accessory to complete the transaction. Cash by Optus NFC SIM and Payment Accessories remain property of Optus.

Once you have download the Cash by Optus™ app and complete the registration process; you can then load up to $500, get access to real-time information and manage payment settings. As it doesn’t come with a PIN Cash by Optus™ can’t be used for contactless transactions $100 and over or for transactions that require a PIN.

It can take 1 to 2 business days for the link deposit, “CashByOptus LINK” to arrive in your bank account. You can only link to Australian banks and most other Australian non-bank financial institutions. It will not work with foreign banks and accounts that don’t allow direct debit payments.

You can access your transaction history electronically via the Cash by Optus app. Your transaction history will be available via the app until the facility is closed

But there is no print feature within the app. They suggest But you could take a screenshot and email it to yourself and print it. As the Cash by Optus™ facility is designed for electronic use, you have agreed that notices, transaction information and communications related to the facility will be available electronically.

Robo-Advice, the concept of using computer automation to provide tailored financial advice has been hitting the headlines recently. DFA has researched household demand for these digitally delivered services, and today we share some of the results.

By way of background, a robo-advisor is an online wealth management service that provides automated, algorithm-based portfolio management advice without the use human financial planners. Robo-advisors (or robo-advisers) use the same software as traditional advisors, but usually only offer portfolio management and do not get involved in more personal aspects of wealth management, such as taxes and retirement or estate planning. Robo-advisors are typically low-cost, have low account minimums, and attract younger investors who are more comfortable doing things online. The biggest difference is the distribution channel: previously, investors would have to go through a human financial advisor to get the kind of portfolio management services robo-advisors now offer, and those services would be bundled with additional services.

ASIC’s chairman Greg Medcraft says computer-generated financial advice, or “robo advice” could slash investment costs and eliminate conflicts of interest in the maligned financial planning industry. They have established a “robo-advice taskforce”, which is investigating the suitability of potential entrants, who use computer algorithms to match investors with suitable assets at a lower cost than human advisers.

A number of Australian players are experimenting with different offers and solutions. For example, according to the AFR, Macquarie is creating a robo-advice platform that puts in one place more than 30,000 local and international investment choices. Unlike other robo-advice platforms, which are really vehicles for gaining funds under management and charging an asset management fee, Macquarie has opted for genuine portfolio advice that does not discriminate between particular fund managers or show any bias towards particular stocks or sectors.

Midwinter’s “Robo-Advice Survey” from 2015, which comprised of responses from over 288 advice professionals, representing over 65 licensees showed the majority of advisers (55%) surveyed were aware of Robo-Advice and not concerned about its potential to disrupt the advice industry, with 12% of these advisers actually excited about its arrival. Around a quarter of advisers were aware and concerned of the impact of Robo-Advice on their business. Only a small amount of advisers (5%) considered themselves apathetic towards the rise of Robo-Advice.

Fintech’s such as Decimal which was founded in 2006 by former Asgard senior executive Jan Kolbusz, provides new capability to the financial advice industry utilising the power and affordability of the cloud. Decimal has subsequently entered into an agreement with Aviva Corporation that saw the company listed on the ASX in April 2014 as Decimal Software Limited (DSX).

So turning to our analysis, DFA has been examining the prospective impact of Robo-Advice, from a household perspective using data from our household surveys. We have found that currently those who have received financial advice already, and who are most digitally aware would readily consider Robo-Advice services. Our conclusion is that rather than growing and extending advice to more Australian households, the first impact of Robo-Advice will be to cannibalise existing advisor relationships.

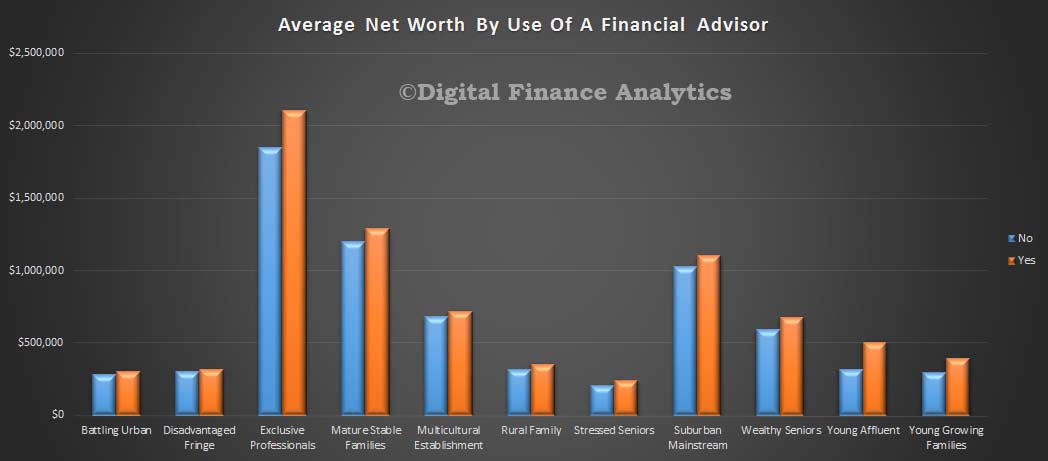

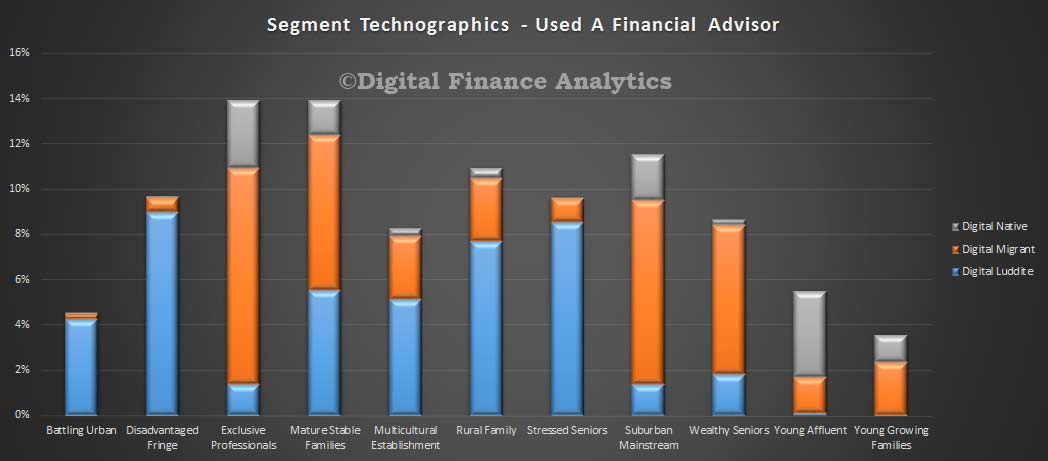

To start the analysis,we looked at overall estimated net worth by household segment. Those households with higher balances are more likely to have sought, or are seeking financial advice. On average a quarter of households have at some time sought advice.

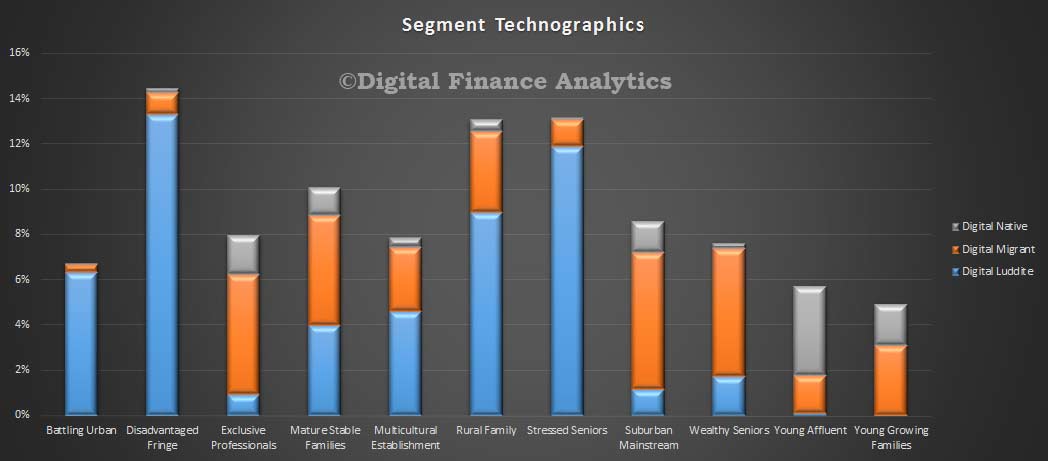

Next we looked at the technographic trends across our household segments using our digital segmentation, between those who are digital natives (always used digital), migrants (learning to use digital) and luddites (not willing or able to use digital). The chart below shows the relative distribution by segment across these three. The more affluent, and younger are most digitally aligned, and so are more likely to embrace Robo-Advice.

Next, we combine the data about getting financial advice and technographics. We find a greater proportion of households who are digitally aware have sought advice.

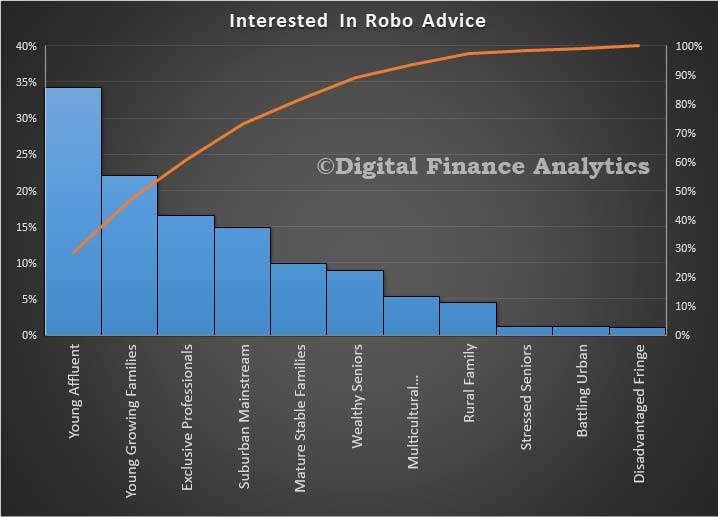

Finally, we asked in our surveys about households awareness and intention to consider Robo-Advice solutions if they were available. The results are shown below, with young affluent households, young growing families and exclusive professionals most likely to consider such a service. The proportions for each segment are those who would consider Robo-Advice, across all the digital segments.

However, the analysis showed that those with existing advice relationships AND high digital alignment were most likely to consider Robo-Advice. Those who are digitally aligned, but not seeking advice showed no propensity to use such a service – at this point in time.

So two observations, first there are many different potential offerings which should be constructed on a Robo-Advice basis, as the needs, of young affluent, and very different from say exclusive professionals. So effective segmentation of the offers will be essential, and different personas will need to be incorporated into the systems being developed.

Second, the bulk of the interest lays with those who have had advice, so it may not, in the short term grow the advice pie. Indeed there appears to be strong evidence that existing advisors may find their business being cannabalised as existing clients switch to Robo-Advice. This is especially true if the range of options are greater, and the price point lower.

We therefore question the assumption expressed within the industry that Robo-Advice is not a threat, as it will simply expand the pie to segments which today do not seek advice. In fact, we suggest the clever play is to make it a tool, and aligned to Advisors, rather than a substitute for them. In addition, the marketing/education strategies need to be developed carefully. There is a lot in play here.

Recently the Australian Securities Exchange (ASX) bought a $15 million stake in Digital Asset Holdings, a developer of blockchain technology. One of the main reasons is to upgrade its share registry system by using blockchain or distributed ledger technology.

Put simply, blockchain technology is a method of recording and confirming transactions where instead of a centralised platform, participants each hold a complete record of transactions through peer to peer verification of transactions. This means there is no central recording system, rather each participant keeps a record of all transactions ever made. This is the same system which allows Bitcoin to operate with no central body.

How would blockchain technology be adopted at the ASX?

Instead of the ASX clearing house settling trades, trades will be settled by participants confirming transactions through the peer to peer network. The network (likely made up of brokers) will record the buyer and selling participants, the number of shares traded, price of shares, time of exchange and the exchange of funds. The ASX will still provide a centralised electronic exchange for participants to place orders, only the settlement or back office function will be sourced to the network.

The benefits?

Blockchain has great potential to cut inefficiencies in the share settlement function. As trades are settled by peer confirmation, there is no need for a clearing house, auditors to verify trades and custodians to ensure a fund has the shares they say they hold. Essentially this is cutting out the middleman in the back office which means less costs in record keeping and in turn less costs to trading on the ASX. Given the high costs in getting a third party to audit, record keep and/or verify trades these costs are substantial.

The peer confirmation of trades also means settlement can be almost instantaneous. Compare this to the current settlement period of three working days (‘T+3’) as the ASX needs to make sure the participants have the money and shares on hand to exchange. This would make shares a far more liquid investment – almost as good as having cash on hand. Higher liquidity means more investment into ASX shares.

As all participants have the full record of transactions and therefore holdings of investors there is complete transparency in the equity market. This makes it almost impossible to falsify transactions or to alter prior transactions. If a false trade occurs, participants will find inconsistencies in their full ledger and reject the trade. For example an investor would be unable to sell stock that they did not own as all participants would know exactly how much stock the investor owns now.

The challenges?

First, implementing a clearing system using blockchain will introduce a new type of fee. In the Bitcoin blockchain, miners process Bitcoin transactions by solving optimisation problems and get rewarded by newly created Bitcoins and settlement fees offered by Bitcoin users who wish to have their transactions processed.

Miners prioritise the order of transactions to be cleared based on the fees offered and the difficulty of the problems to record the transaction in a block. This is what allows a blockchain to have no centralised clearing house.

If the ASX blockchain requires investors to include transaction fees in order for their transactions to be cleared, then the ASX is transferring the cost of maintaining the back office to the investors. If this is to happen, investors will have to compete against each other to have their transactions cleared faster than those of others. Alternatively, if the new system doesn’t allow such fees and relies on brokers or other entities to clear the transactions, then the ASX is again transferring the cost of maintaining back office to those entities.

The second concern is increased transparency. Under the proposed trading system, most of positions of the market participants could be exposed to the public as the trading ID can be identified. This could disadvantage many investors such as super, managed and hedge funds. For example, a super fund typically sells a large position on a gradual basis for a prolonged time period.

In this process, it is critical not to be noticed by other traders who may take advantage of such large-scale sales. With complete transparency such as in blockchain, such a sell-off could not be applied effectively. Potentially this may make investors leave the ASX and seek more opaque venues to trade such as dark pools.

Will it work?

Clearly a direct adoption of blockchain from Bitcoin technology would not be viable for the ASX. If the ASX is able to adopt blockchain technology and address privacy, security and trade transparency concerns then this would yield great cost savings to investors.

Authors: Adrian Les, Senior Lecturer in Finance, University of Technology Sydney; KIHoon Hon, Assistant Professor, University of Technology Sydney

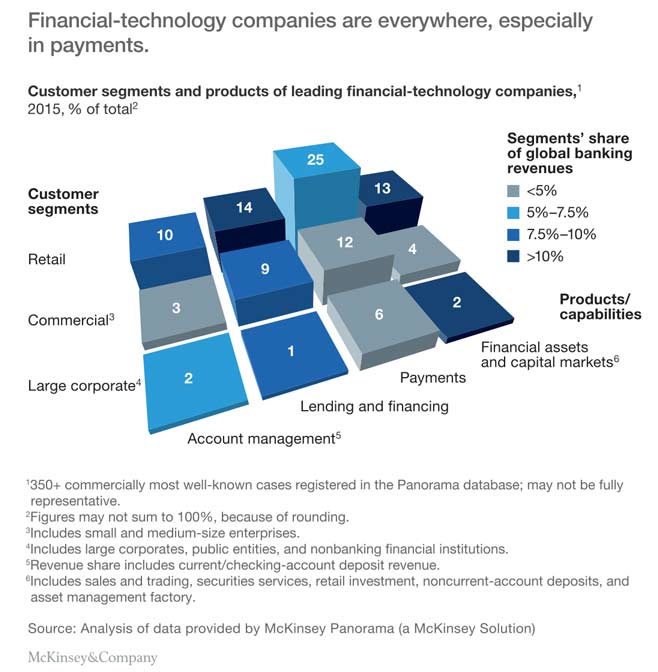

McKinsey has published an article about the rise of Fintechs “Cutting through the noise around financial technology”, and suggests that this time, unlike the dotcom bubble, more is at stake for existing financial services companies. Here is an extract, but we recommend the entire article.

Banking has historically been one of the business sectors most resistant to disruption by technology. Since the first mortgage was issued in England in the 11th century, banks have built robust businesses with multiple moats: ubiquitous distribution through branches; unique expertise such as credit underwriting underpinned by both data and judgment; even the special status of being regulated institutions that supply credit, the lifeblood of economic growth, and have sovereign insurance for their liabilities (deposits). Moreover, consumer inertia in financial services is high. Consumers have generally been slow to change financial-services providers. Particularly in developed markets, consumers have historically gravitated toward the established and enduring brands in banking and insurance that were seen as bulwarks of stability even in times of turbulence.

The result has been a banking industry with defensible economics and a resilient business model. This may now be changing. Our research into financial-technology (fintech) companies has found the number of start-ups is today greater than 2,000, compared with 800 in April 2015. Globally, nearly $23 billion of venture capital and growth equity has been deployed to fintechs over the past five years, and this number is growing quickly: $12.2 billion was deployed in 2014 alone.

So we now ask the same question we asked during the height of the dot-com boom: is this time different? In many ways, the answer is no. But in some fundamental ways, the answer is yes. History is not repeating itself, but it is rhyming.

The moats historically surrounding banks are not different. Banks remain uniquely and systemically important to the economy; they are highly regulated institutions; they largely hold a monopoly on credit issuance and risk taking; they are the major repository for deposits, which customers largely identify with their primary financial relationship; they continue to be the gateways to the world’s largest payment systems; and they still attract the bulk of requests for credit.

Some things have changed, however. First, the financial crisis had a negative impact on trust in the banking system. Second, the ubiquity of mobile devices has begun to undercut the advantages of physical distribution that banks previously enjoyed. Smartphones enable a new payment paradigm as well as fully personalized customer services. In addition, there has been a massive increase in the availability of widely accessible, globally transparent data, coupled with a significant decrease in the cost of computing power. Two iPhone 6s handsets have more memory capacity than the International Space Station. As one fintech entrepreneur said, “In 1998, the first thing I did when I started up a fintech business was to buy servers. I don’t need to do that today—I can scale a business on the public cloud.” There has also been a significant demographic shift. Today, in the United States alone, 85 million millennials, all digital natives, are coming of age, and they are considerably more open than the 40 million Gen Xers who came of age during the dot-com boom were to considering a new financial-services provider that is not their parents’ bank. But perhaps most significantly for banks, consumers are more open to relationships that are focused on origination and sales (for example, Airbnb, Booking.com, and Uber), are personalized, and emphasize seamless or on-demand access to an added layer of service separate from the underlying provision of the service or product. Fintech players have an opportunity for customer disintermediation that could be significant: McKinsey’s 2015 Global Banking Annual Review estimates that banks earn an attractive 22 percent ROE from origination and sales, much higher than the bare-bones provision of credit, which generates only a 6 percent ROE.