Australia’s market for small- and medium-sized enterprises (SME) is by no means easy. The nation is grappling with a late supplier payments problem and with regulators looking to accelerate corporate payments to SMEs, though with limited expectation for the efforts to work.

But that presents an opportunity for alt lending, analysts say, as do tighter restrictions on traditional banks that may guide SMEs toward alt-fin, as they look to ease their cash crunches.

It seems an ideal climate for the alternative lending industry, but news of an analysis from Moula and Digital Finance Analytics this week finds awareness of these options is lacking among small business owners.

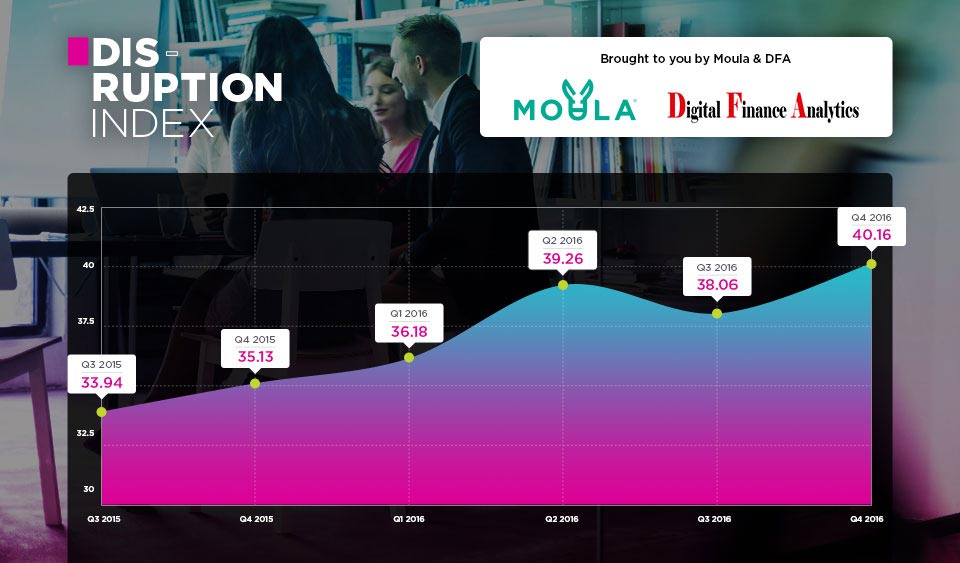

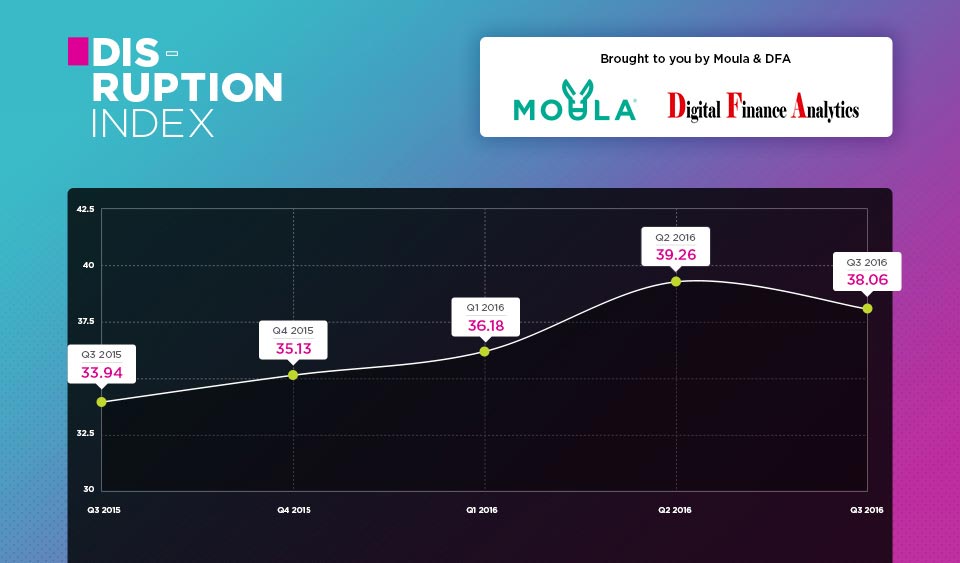

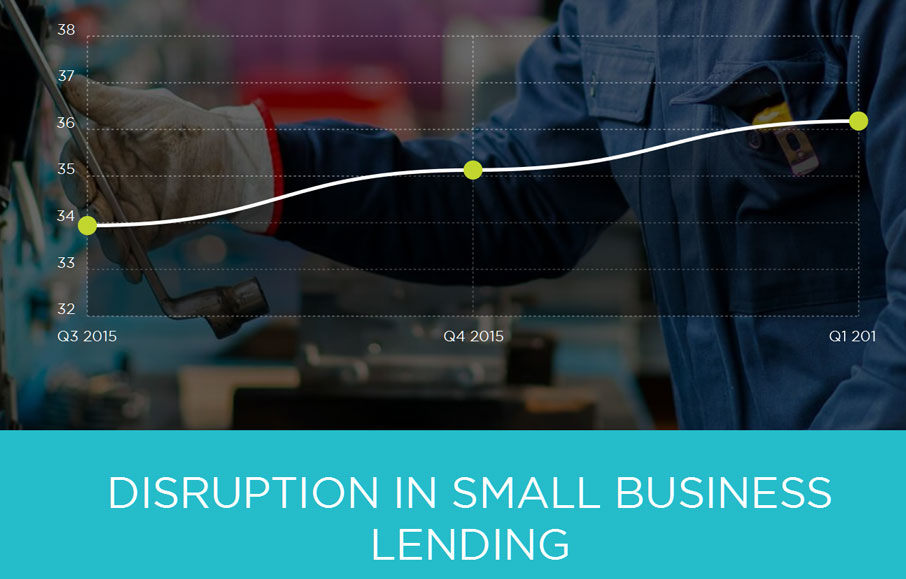

In their Disruption Index report, released quarterly, Moula and Digital Finance Analytics (DFA) scored Q1 2017 at 38.39, a 6.1 percent increase from Q1 2016. But the report said this represents only “gradual change” among small businesses in terms of their awareness of alternative lending options.

“There is still a certain air of skepticism about non-traditional forms of lending,” said DFA Principal Martin North in an interview with Australian Broker. “So SMEs who need to borrow tend to still go to the normal suspects. They’ll look to the banks or put it on their credit cards.”

He added that this means the alternative finance industry has to work harder to boost awareness and promote education.

“I think the FinTech sector has a terrific opportunity to lend to the SME sector, but they haven’t yet cracked the right level of brand awareness,” North continued. “Perhaps they need to think about how they use online tools, particularly advertising to re-energize the message that’s out there.”

There certainly is a market for alternative lenders to fill in the funding gap for small businesses.

Earlier this year, Australia’s Small Business and Family Enterprise Ombudsman Kate Carnell began naming some of the worse offenders of late supplier payments, including Kellogg’s and Mars, likening their delayed invoice payment practices to “extortion.” With the Council of Small Business Australia, regulators began to take a harsher stance on late payments, and in May, the voluntary Supplier Payment Code, which sees companies vowing to pay suppliers on time, came into effect.

As regulators consider whether to create fair supplier payment practice legislation, small businesses in the country continue to struggle: Research from American Express Australia and Xero released in April found nearly a third of the invoices in the cloud accounting platform can’t be reconciled every month because they’re waiting to be paid.

Meanwhile, Australian Broker reported, regulators are imposing stricter rules on traditional banks that may see them back even further away from small business borrowers. Plus, Moula and DFA’s report found, small business demands on their financial service providers are on the rise. According to their report, SMEs say a loan application should take, on average, less than five days to see final approval. Alternative lenders take an average of 36 hours, the report found.

The data suggests alt lending can meet some of the demands among SMEs for working capital and faster lending services.

“FinTechs like Moula are at the quick end, but a lot of the traditional lenders such as the major banks take a lot longer,” North continued. “What this is saying is that if the expectations of SMEs point to quick approval times and if the major players aren’t able to do that because of their internal systems and processes, then there is an interesting opportunity for the FinTechs who can do it quicker. They can actually disrupt [the industry].”

According to North in a statement found within the report itself, awareness levels among SMEs are gradually rising.

“In the last three months, we have seen a significant shift in attitudes among SMEs as they become more familiar with alternative credit options and migrate to digital channels,” he said. “The attraction of online application, swift assessment and credit availability for suitable businesses highlights the disruption which is underway. There is demand for new services and supply from new and emerging players to the SME sector.”

Indeed, while awareness is on the rise, it’s still relatively low. In Q4 of 2016, Moula found that just 14.1 percent of SMEs surveyed said they are familiar with their alternative finance options.

“So, what’s the barrier to growth?” North reflected to Australian Broker. “It’s not technology or demand from the SME sector. The barrier to growth is awareness and the willingness of SMEs to commit to this particular new business model.”