Something happened late last week, which superficially might

be attributed to positive news on the US China trade talks (later downplayed by

Trump) but it was wider and more significant than that.

In recent months many traders have been positioning for a

significant market correction, and potentially a US or global recession. Thus, risk

stocks were downplayed, while bonds and gold were all the rage.

This drove the yields on bonds down, to the point where in several

countries, like Germany they went negative, and at its peak, it was estimated

that around $17 trillion of bonds were effectively underwater. A couple of

weeks back, we pointed out that Gold had shot ahead of itself, and that the

Gold futures meant it would slide. It did, falling by more than $30 an ounce.

The 10-year US Treasury yield rose on Friday to 1.94%. up nearly 50 basis points from the lows at the end of August. Remember that the Fed cut its interest rate target twice, by a total of 50 basis points, and short-term Treasury yields have fallen by about that much. With the one-month yield now down to 1.56% and the 10-year yield up at 1.94%, the yield curve has un-inverted and steepened. Recession has been postponed, for now.

Germany’s 30-year bonds are interesting in that they tried

to sell them at a negative yield of -0.11% on August 21, with a 0% coupon – so

no interest payments for 30 years – and at a premium, in order to achieve the

negative yield of -0.11%. While €2 billion of these bonds were offered, only

€824 million were sold. And those investors may rue the day they bought.

This suggests the bank still thinks monetary policy – in this case

lowering interest rates to stimulate the economy – could help “support

sustainable growth in the economy, full employment and the achievement

of the medium-term inflation target”.

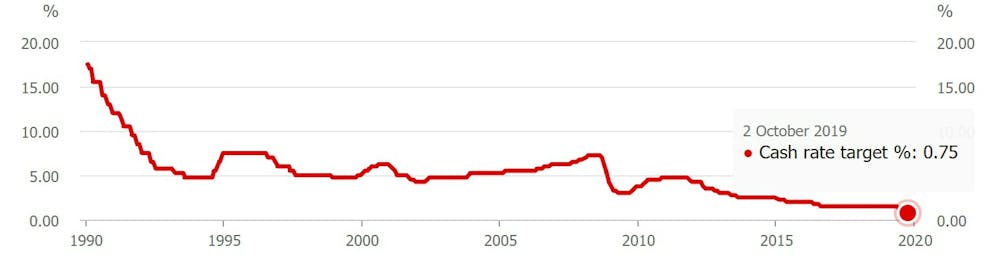

But in the wake of the bank last month lowering the official interest

rate to a record low and the current somewhat sad state of the

Australian economy, many commentators have speculated that monetary policy doesn’t work any more.

There are a number of variants of the “monetary policy doesn’t work”

argument. The most basic is that the Reserve Bank has this year cut

rates from 1.50% to 0.75% without any improvement to the Australian

economy.

This is a textbook example of one of the classic logic fallacies known as “post hoc ergo propter hoc” (from the Latin, meaning “after this, therefore because of this”).

Put simply, it assumes the rate cuts have had no effect and doesn’t

account for the possibility things might have been worse had there been

no cuts.

Things might have been even worse. We’ll never know.

It also ignores what might have happened if the RBA had cut sooner.

Again, we can’t know for sure. It is possible, though, to make an

educated guess.

When to cut rates

Had Reserve Bank governor Philip Lowe acted, say, 18 months earlier

to cut rates, he would have signalled that Gross Domestic Product growth

was indeed lower than desired, that the sustainable rate of

unemployment was more like 4.5% than 5%, and, most importantly, that he

understood the need to act decisively.

That would have sent a powerful signal.

It would also have ameliorated the huge decline in housing credit

that pushed down housing prices in Sydney and Melbourne by double

digits.

That, in turn, would have prevented some of the weakening in the

balance sheets of the big four banks that has occurred (witness this

annual general meeting season).

All of this would have pumped more liquidity into the economy and put

households in a much stronger position, likely leading to stronger

consumer spending than we have seen.

It is true there is a problem

with banks not being able to cut deposit rates below zero, and as a

result having less scope to cut mortgage rates, which are majority

funded from deposits.

But there are, of course, other ways monetary policy can work. The leading example is quantitative easing (QE).

This is where the central bank pushes down long-term interest rates

by buying government and corporate bonds. At the same time this expands

the money supply, thereby adding some upward inflationary pressure.

There is little reason to think such measures wouldn’t work.

The power of free money

Perhaps paradoxically, the closer interest rates get to zero the more powerful those rates may end up being.

To put it bluntly, if someone shoves a pile of money into your hand

and asks almost nothing in return, you’re likely to use it. In fact, you

would be pretty silly not to.

You might decide to redraw that and spend the money on a home

renovation or some other productive purpose. Or you might decide to buy a

more expensive house.

Such spending provides an economic boost.

The effect is all the more pronounced if people expect interest rates

to be low for a long period of time. Aggressive cutting coupled with

quantitative easing – which lowers long-term rates – signal just that.

But not only monetary policy

Just because monetary policy still has some effect at near-zero rates

doesn’t mean we should pin all of our economic hopes to it.

A near consensus of economists have argued repeatedly for the use of

more aggressive fiscal policy – including more infrastructure spending

and more tax cuts.

Indeed, Philip Lowe has raised eyebrows by speaking so forthrightly on this issue. That doesn’t make him wrong, though.

There is little doubt the Reserve Bank should have acted much earlier

to cut official interest rates. There is also a very good chance it

will need to begin to use other measures such as quantitative easing in

the relatively near future.

All of that says the Australian economy, like most advanced economies around the world, is in bad shape.

But it doesn’t mean monetary policy has completely run out of puff.

Author: Richard Holden, Professor of Economics, UNSW

The latest edition of our weekly finance and property news digest with a distinctively Australian flavour.

Contents:

00:24 Introduction

1:23 US China Trade Talks

3:04 US Markets

6:15 China

7:50 Australian Section

7:55 RBA on Monetary Policy

10:50 Household Confidence

11:10 Lending

11:40 REA

14:50 High Rise Construction

15:30 Property Market

16:20 Auctions

16:50 Bank Profit Results

17:50 Australian Markets

Nab reported a 13.6% fall in statutory net profit for 2019, at $4,798 million, compared with $5,702 million last year. Along with ANZ and Westpac, it is the same story of a massive hit from customer remediation (past results inflated by milking customers, and many customers still require remediation), margin compression, not helped by lower cash rates, weak loan growth, and higher mortgage delinquency and provisions. And again they expect 2020 to be a weak year economically speaking. So no growth story here.

Revenue was down 4.2%, although they at pains to point out that excluding customer-related remediation, revenue rose 1.1% mainly reflecting growth in business lending partly offset by lower margins. Of course they dismiss many of the writes-downs as a one-off, and there will be some “putting the trash out” as the new CEO takes up the reigns. $2,092 million for customer remediation all up, is a big number, and not yet final. But do not be misled, the underlying business is under extreme pressure, and competition for the meager loan volumes is intense.

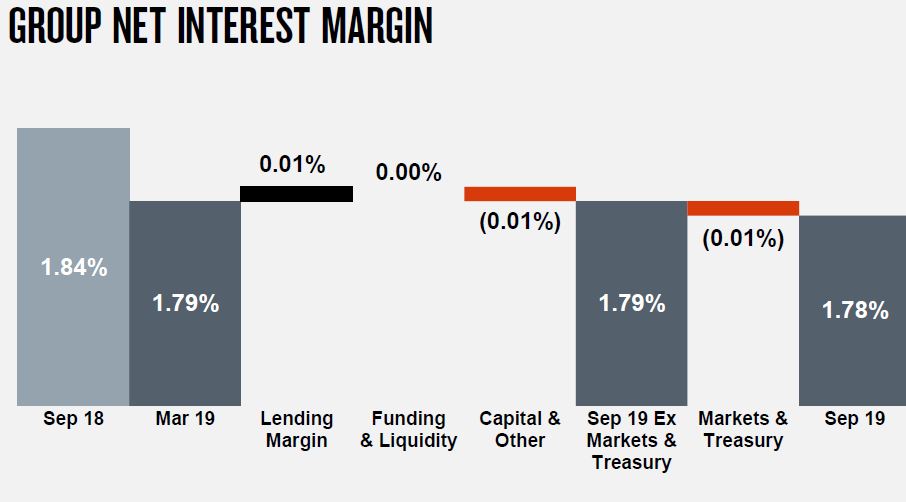

Net Interest Margin (NIM) declined 7 basis points (bps) to 1.78%. Excluding Markets and Treasury and customer-related remediation, NIM declined 4bps with home lending competition an important driver.

Expenses rose 0.2%. Excluding large notable items, expenses were up 0.4% with productivity benefits and lower performance based compensation largely offsetting higher investment and increased spend to strengthen the compliance and control environment.

But the revenue excludes customer-related remediation $1,207m in FY19, $249m in FY18. Expenses excludes: customer-related remediation $364m in FY19, $111m in FY18; capitalised software policy change $494m in FY19; restructuring-related costs $755m in FY18.

In cash earnings terms, they fell by 10.6%, from $5,702 million in 2018 to $5,097 in 2019.

FY19 cash earnings includes charges of $1,100 million after tax for additional customer-related remediation. During FY19 they uplifted customer remediation practices with more than 950 people (including NAB employees and external resources) solely dedicated to remediating customers.

In combination with provisions raised in 2H18 which have not yet been utilised, provisions for customer-related remediation as at 30 September 2019 total $2,092 million. They warn that the final cost of such remediation matters remains uncertain.

Cost savings of $480 million were achieved in FY19 bringing total savings since September 2017 to $800 million.

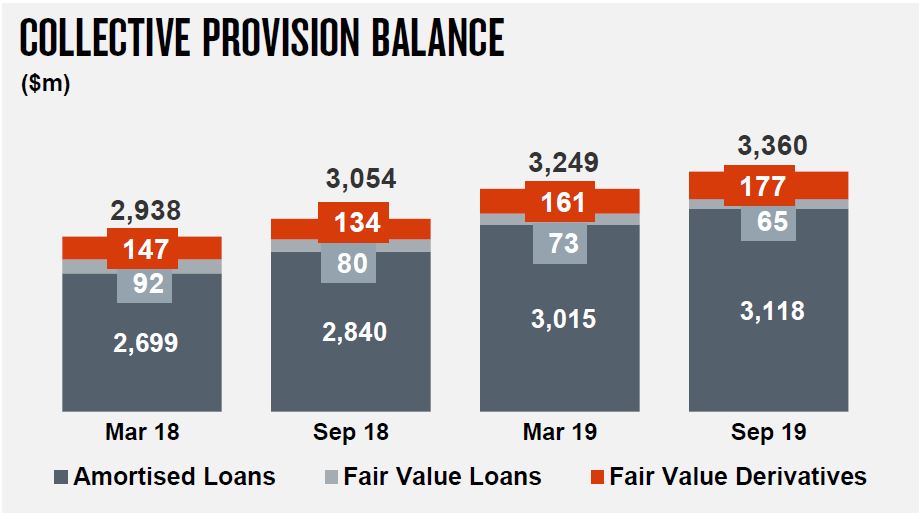

Collective provisions rose to 0.96% of CRWA’s, which equates to $3,360 million.

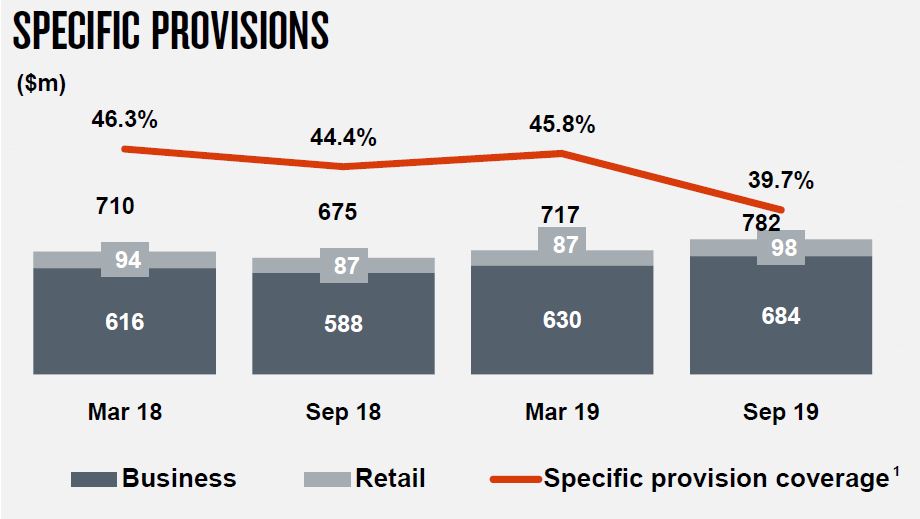

Whereas specific provisions fell to 39.7%, but were also higher.

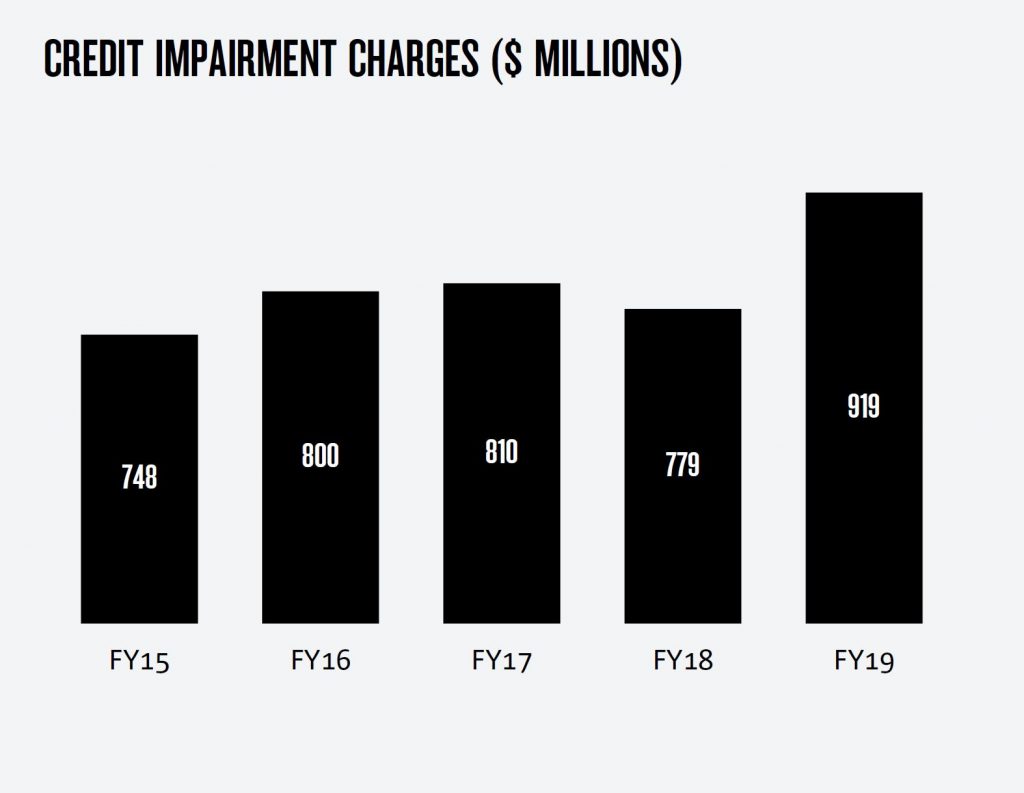

Credit impairment charges increased 18% to $919 million, and as a percentage of gross loans and acceptances rose 2bps to 15bps. FY19 charges include $60 million of additional collective provision forward looking adjustments for targeted sectors experiencing elevated levels of risk.

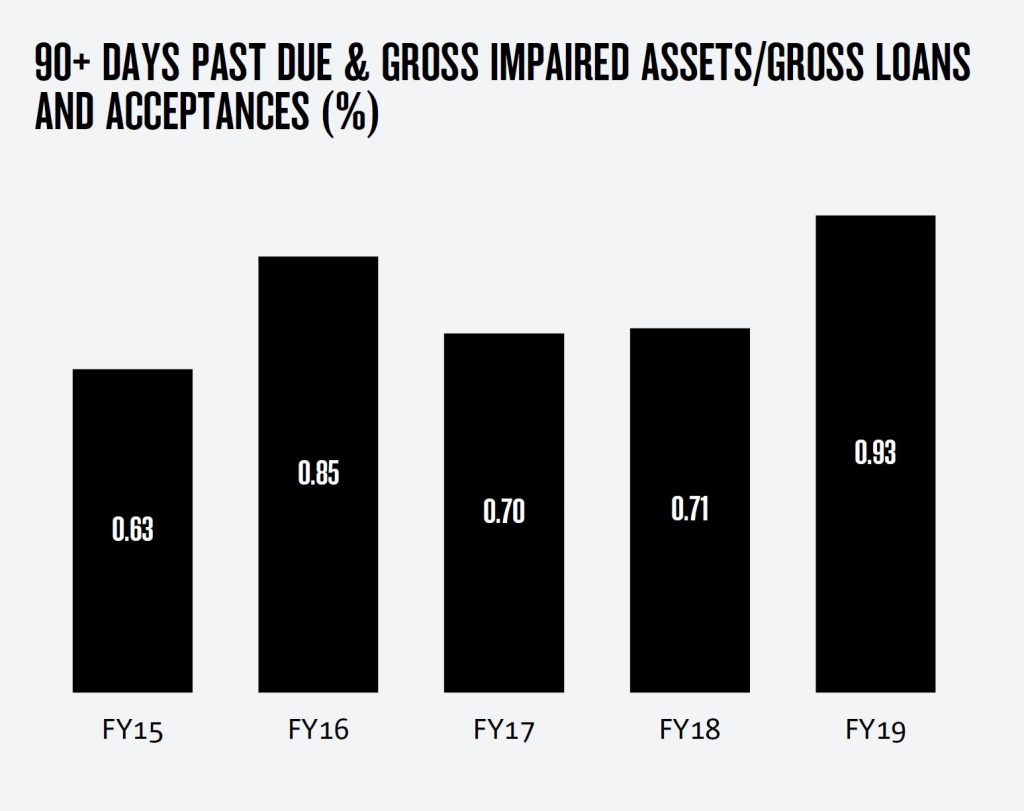

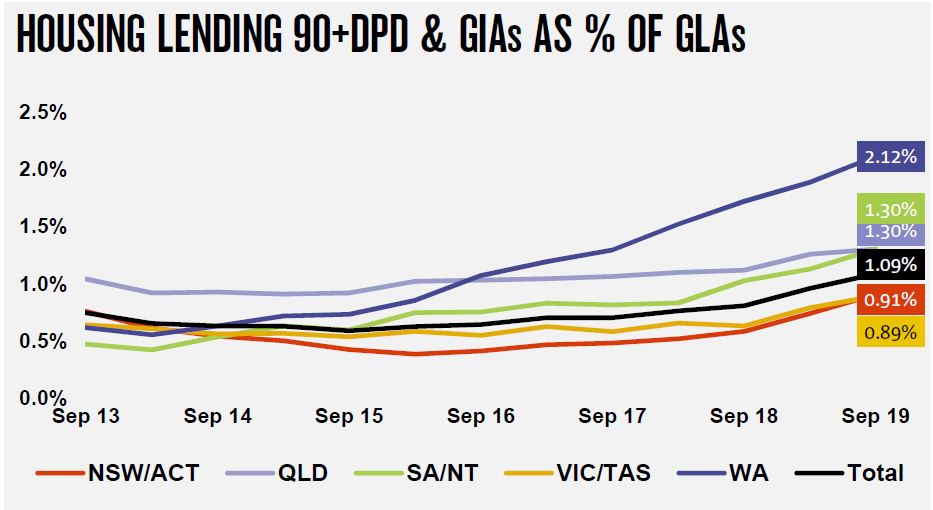

The ratio of 90+ days past due and gross impaired assets to gross loans and acceptances increased 22bps to 0.93%, largely due to rising Australian mortgage delinquencies.

While Australian housing arrears increased further, loss rates for this portfolio is 2bps. Collective provision forward looking adjustments for targeted sectors increased over FY19 and now stand at $641 million. In their scenario testing, they estimate a Peak Net Credit Impairment of $1.8bn in year 2, which equates to 57 basis points, based on an average home price fall of 25.2%

2.4% of mortgages in Australia are above 100% LVR (based on SA3 level CoreLogic data, so not very specific).

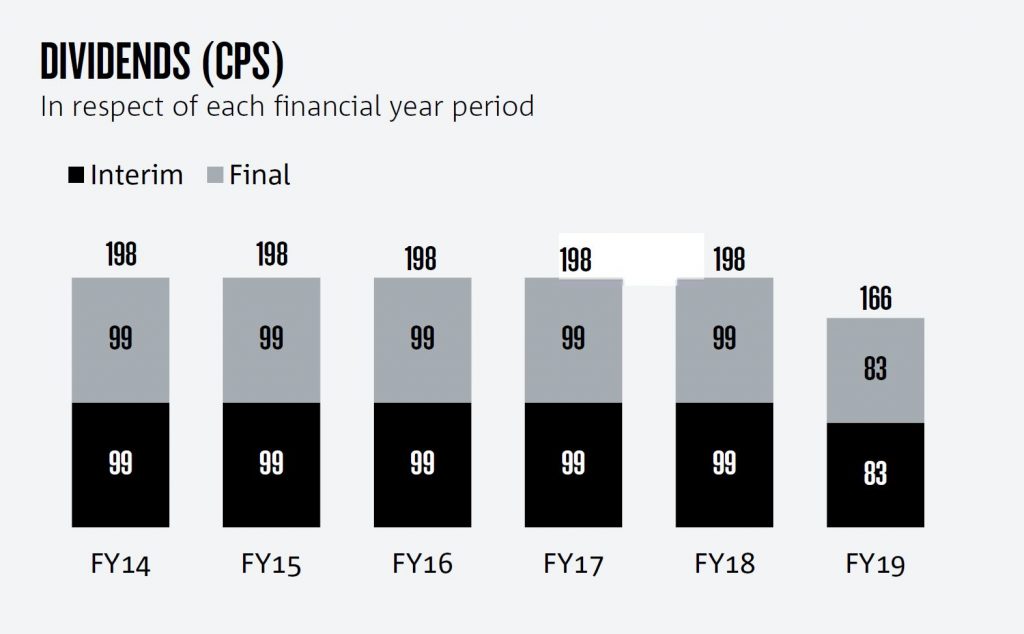

The final fully franked dividend of 83 cents per share (cps) has been held stable with the 2019 interim dividend, bringing the total for FY19 to 166 cps. This represents a 16% reduction compared with FY18.

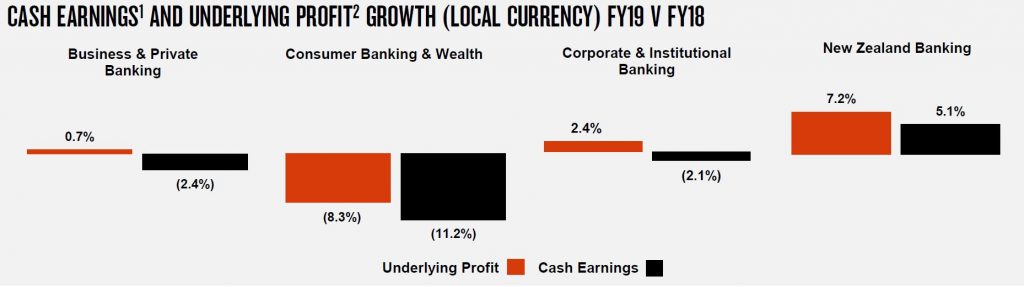

Across the divisions in cash earning terms:

Business & Private Banking $2,840 were down 2.4% on last years, reflecting higher credit impairment, charges and higher investment spend. Revenue increased 1% reflecting good SME business lending growth.

Consumer Banking & Wealth $1,366 were down 11.2% where banking earnings decreased given lower margins with competitive pressures in housing a key driver, combined with increased credit impairment charges.

Wealth earnings also declined reflecting the impact of customer preferences and repricing on margins, and lower average funds under management and administration.

Corporate & Institutional Banking $1,508 down 2.1% reflecting higher credit impairment charges relating to impairment of a small number of larger exposures. Revenue increased 1% despite lower Markets income, with higher lending volumes benefitting from continued focus on growth segments.

New Zealand Banking NZ$1,055m up 5.1% benefitting from growth in lending, partly offset by increased investment spend and higher credit impairment charges.

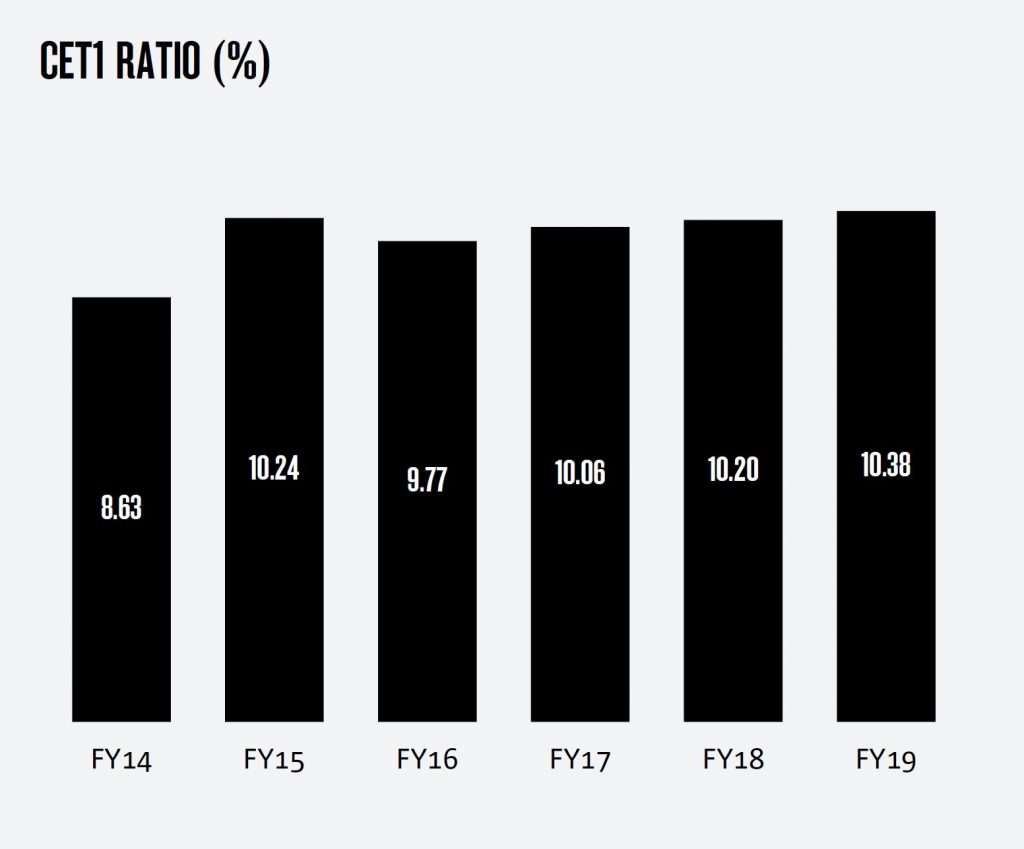

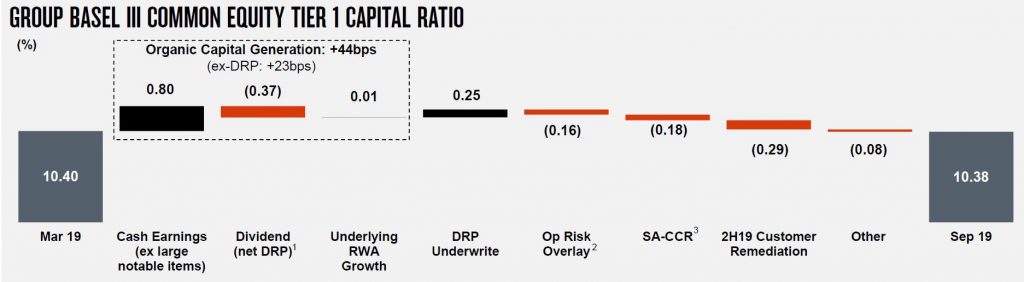

The Group Common Equity Tier 1 (CET1) ratio is 10.38%, up 18bps from September 2018, and includes $1 billion (25bps) of proceeds received in July from the 1H19 underwritten Dividend Reinvestment Plan and 34bps adverse impact from regulatory changes relating to operating risk and derivative counter party credit risk measurement.

Leverage ratio (APRA basis) of 5.5%

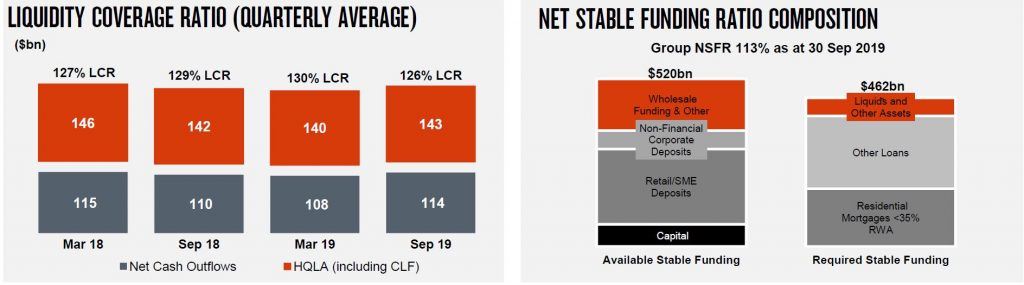

Liquidity coverage ratio (LCR) quarterly average of 126% and Net Stable Funding Ratio (NSFR) of 113%

NAB expects weak credit growth ahead, a GDP result in 202 of around 2% and business confidence also weakened which may dampen business credit growth.

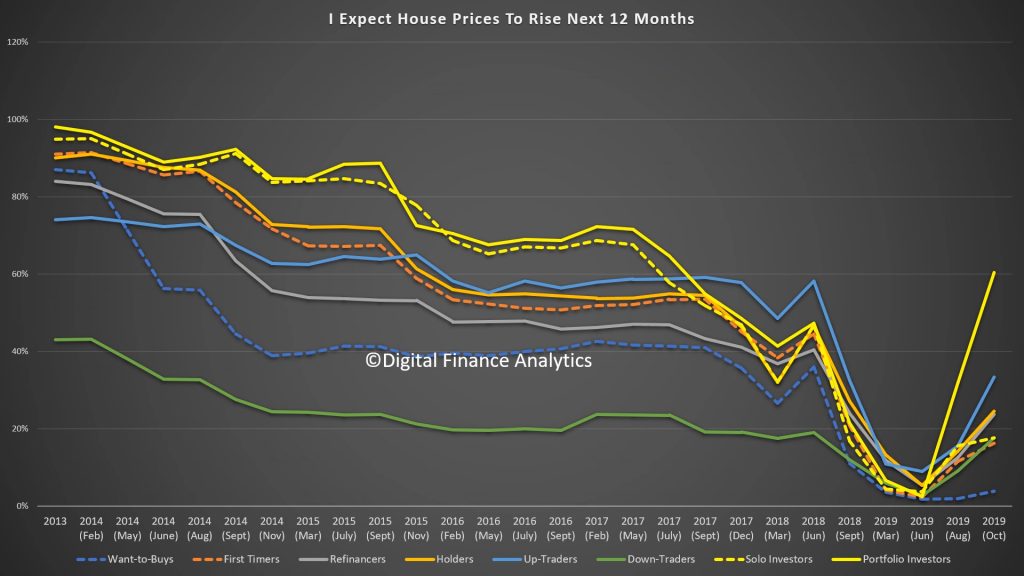

In the final part of our October 2019 Household Survey we look at the results through the lens of our segmentation models. What is clear is there is a disconnect between future home price expectations (much more positive) and proposed activity (lower demand for credit, and intentions to transact). This is at the heart of the weirdness in the market at the moment, and it helps to explain the low levels of listings and transactions (and hence the high auction clearance rates on those low volumes). There is nothing in the latest results however which flags significant momentum increases ahead.

We start with the cross-segment trends. First there is a significant hike in those expecting home prices to be higher in the next 12 months. It reached a low around the election, and has been rising since the cash rate cuts. Portfolio Investors (those with multiple investor properties are the most bullish). But the expectations are there across the board.

However, this does not necessarily translate into intention to transact. First Time Buyers and Down Traders (around 900k) are most likely to be in the market, the former aided by the extra incentives available and the latter by the need to pull equity from existing properties. Property investors remain largely on the sidelines. There is also a slight downward inflection in the past quarter.

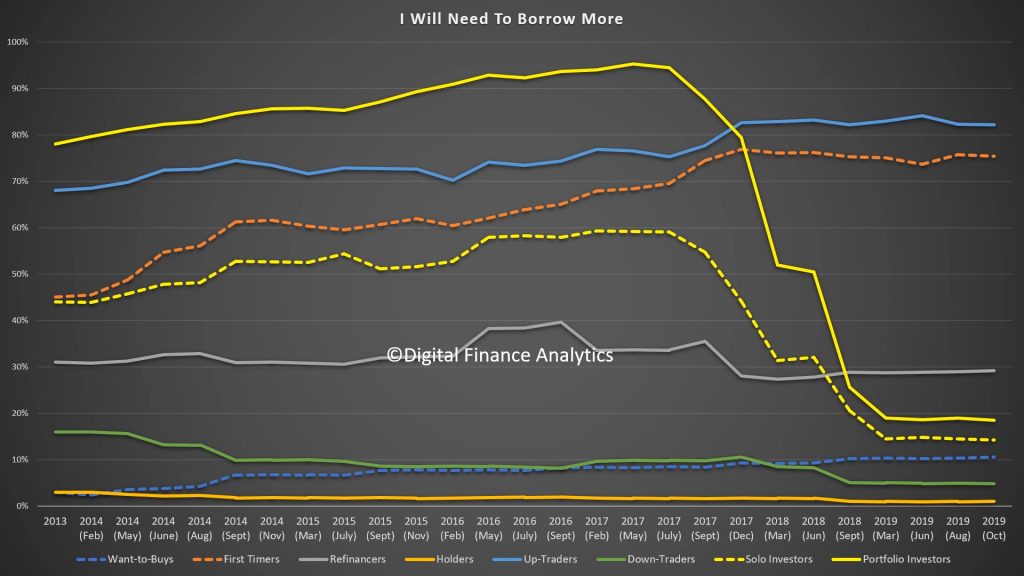

Another lens is demand for credit which shows stubborn resistance other than from First Time Buyers ~around 150k actively looking) and Up Traders (around 550k actively looking). Refinancing is tracking at levels we have seen for some time. This suggests that banks will have to compete hard for meager pickings, and refinancing and first time buyers will be the targets for special deals.

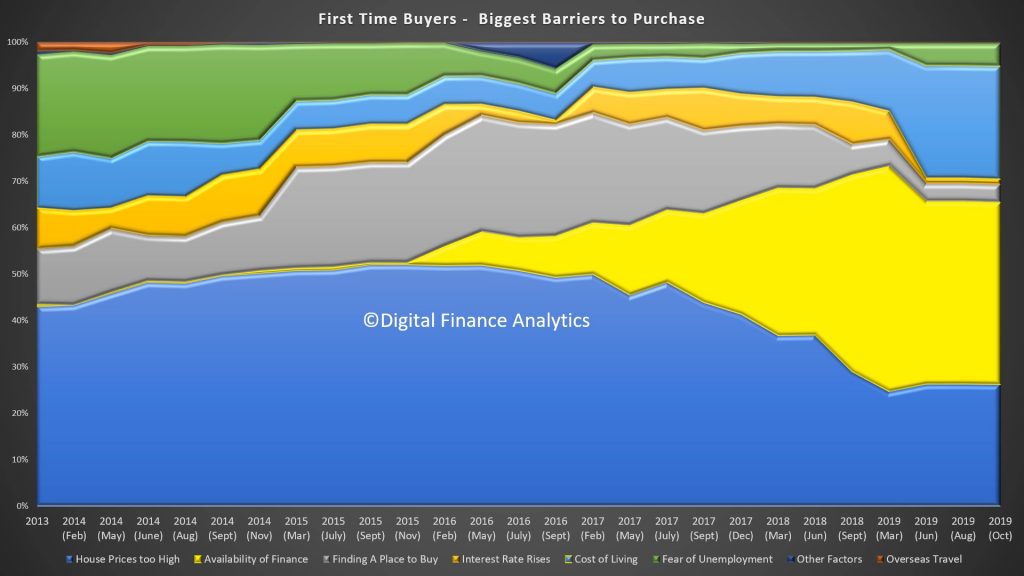

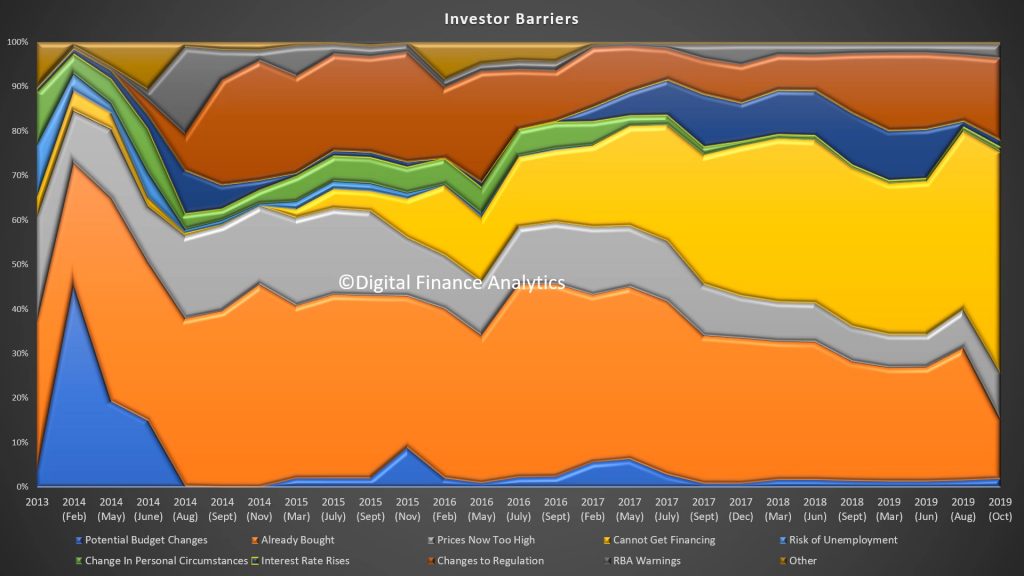

Those Wanting to Buy say that availability of finance (40%) and costs of living (30%) are the main barriers, although high home prices at 16% still registers. Interest rates and fear of unemployment are low relatively speaking.

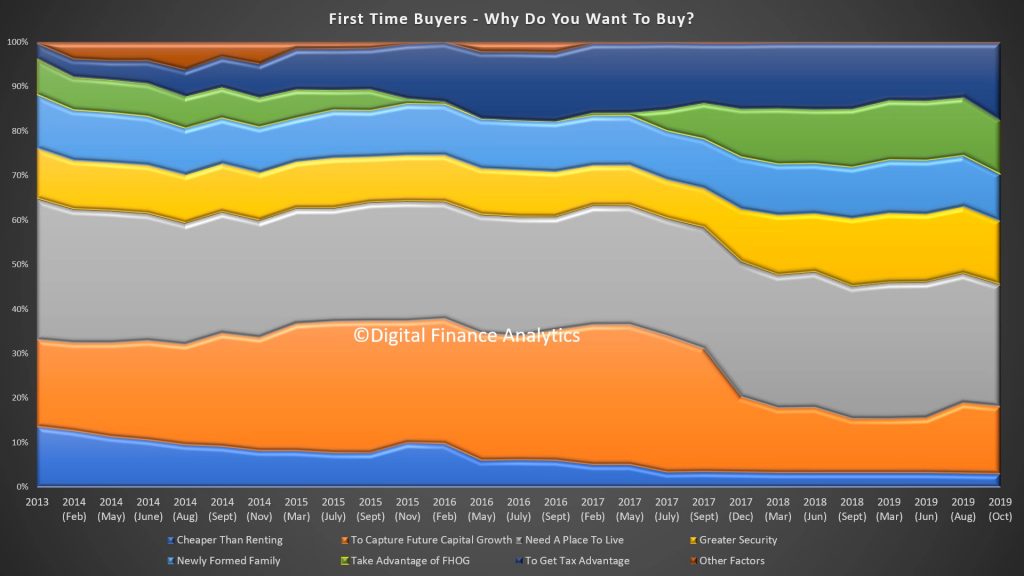

First time buyers are being driven by a range of factors including the need for shelter and a place to live (28%), greater security (14%), tax advantage (17%) and to take advantage of the FHOG (12%). But that said there are significant barriers as well.

Barriers include home prices too high (26%), availability of finance (39%) and costs of living (24%). On the other hand finding a place to buy and rising interest rates hardly registered.

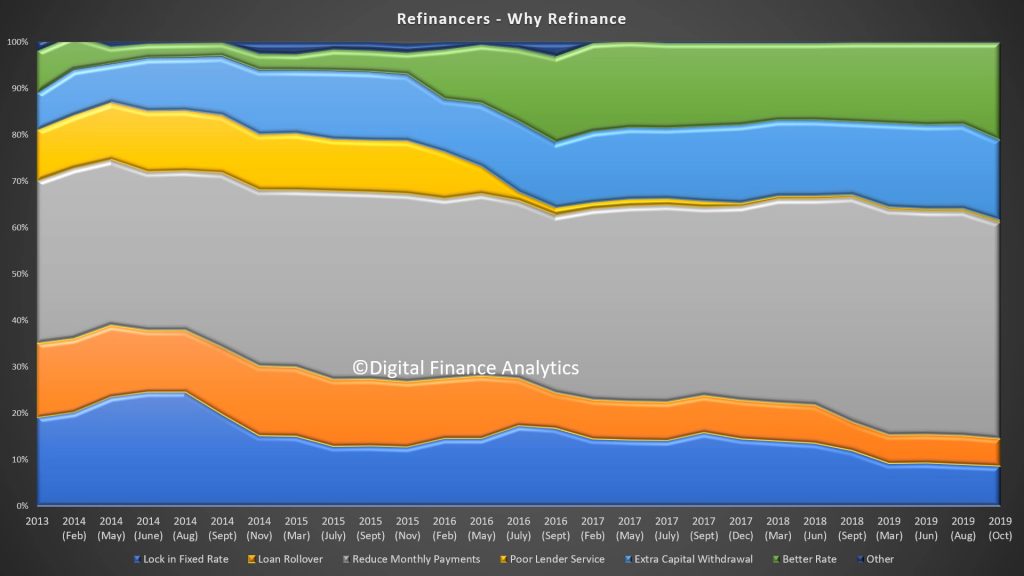

Household seeking to refinance are being driven by reducing monthly repayments (50%), for a better rate (22%) and extra capital withdrawal 20%.

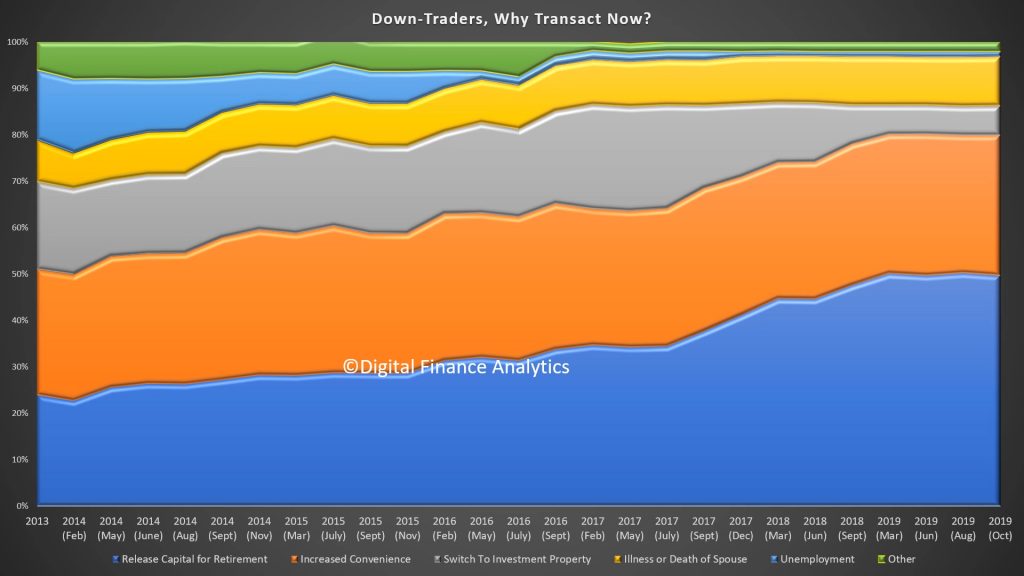

Down Traders are driven by the desire to release capital for retirement (50%), increased convenience (30%) and illness or death of spouse (11%). Interest in investment property has faded to 6%.

Up Traders are being driven by the desire for more space (41%), job change (16%), property investment (22%) and life-style changes 20%).

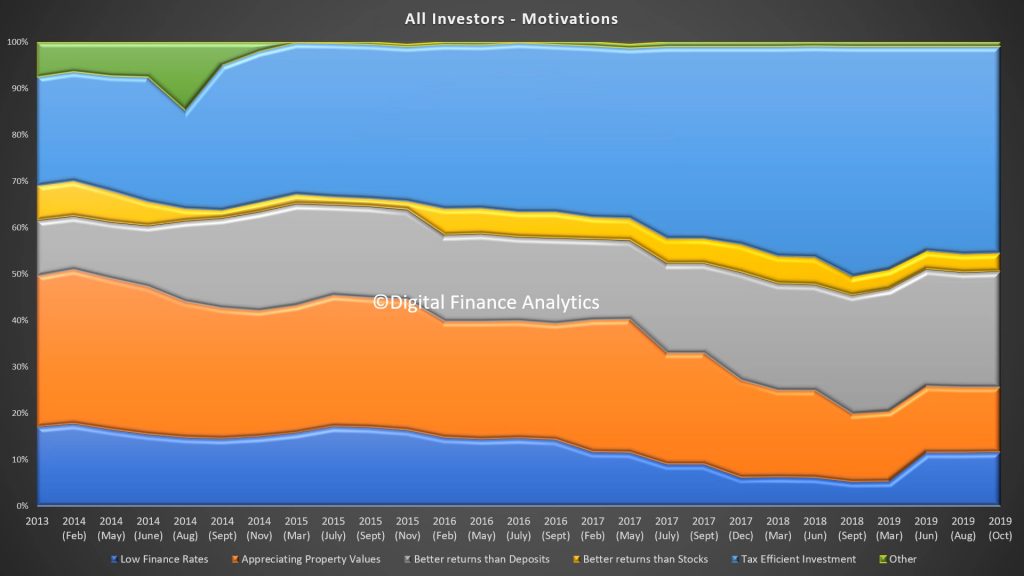

Turning to investors 45% are driven by tax benefits, better returns than deposits (25%) and appreciating property values (14%).

On the other hand, investors face a number of barriers including cannot getting finance (49%), and they have already bought (13%).

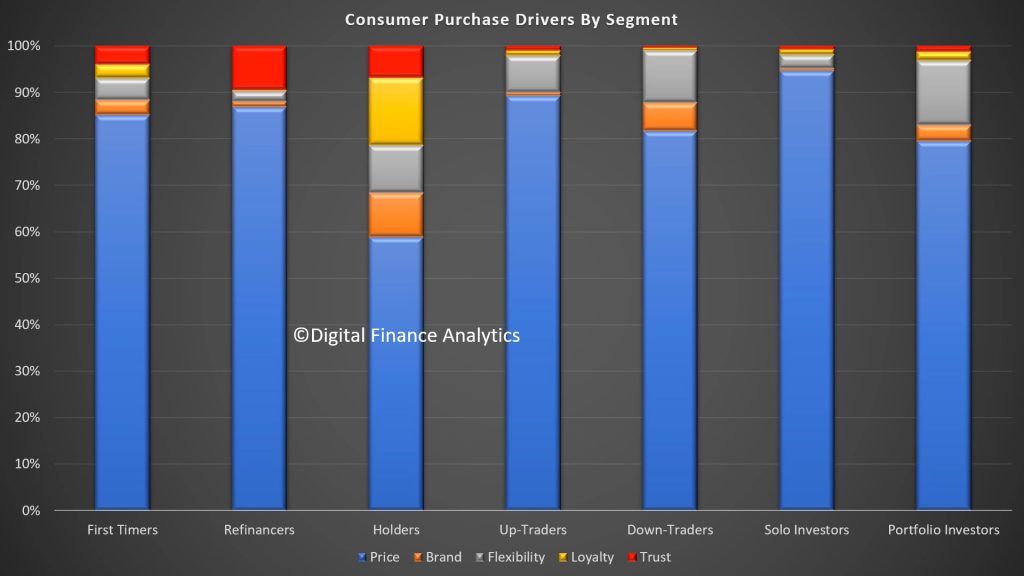

And finally across the segments the prime selection point is price, although it varies, and loyalty is not seen as significant or rewarded.

Standing back, it appears that property sector momentum is likely to remain patchy at best, with more action at the more expensive end of the value spectrum, and first time buyers remaining as the primary “canon fodder” with regards to new transactions. It will be interesting to see how the Government scheme due in January changes the picture.

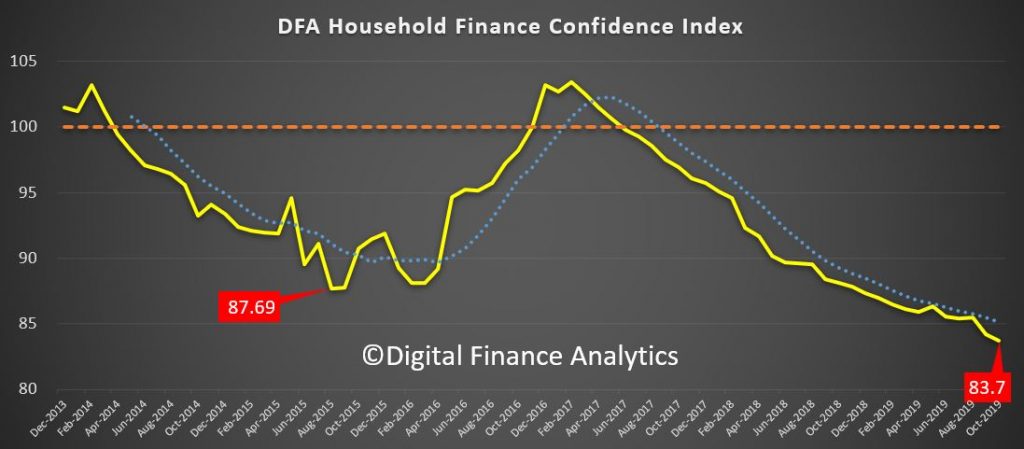

The bad news keeps coming, with the latest DFA Household Financial Confidence Index for October at the lowest ever of 83.7.

This continues the trends of recent months, since dropping through the neutral 100 score in June 2017.

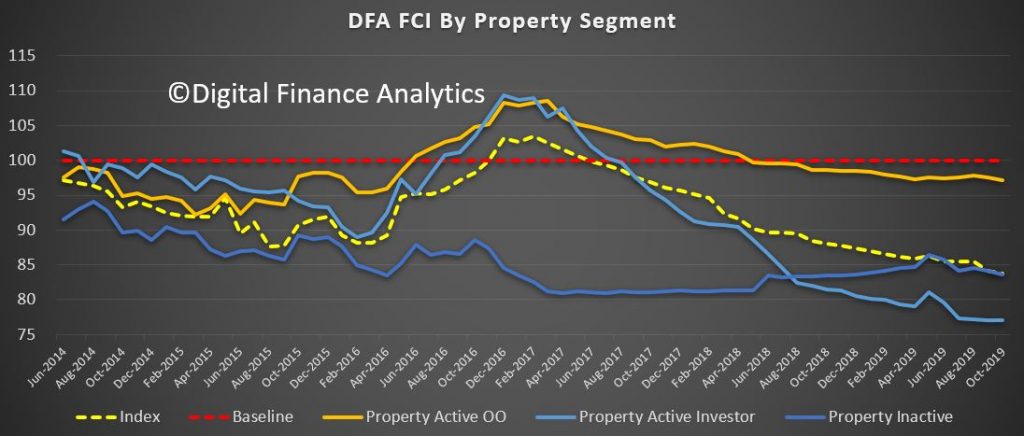

The falls were widespread across our property segments, with investors still way down, under the pressure from low net rental yields, the need to switch to principal and interest from interest only, and worries about construction defects. Owner occupied households were less negative, but those renting continue to struggle with higher levels of rental stress.

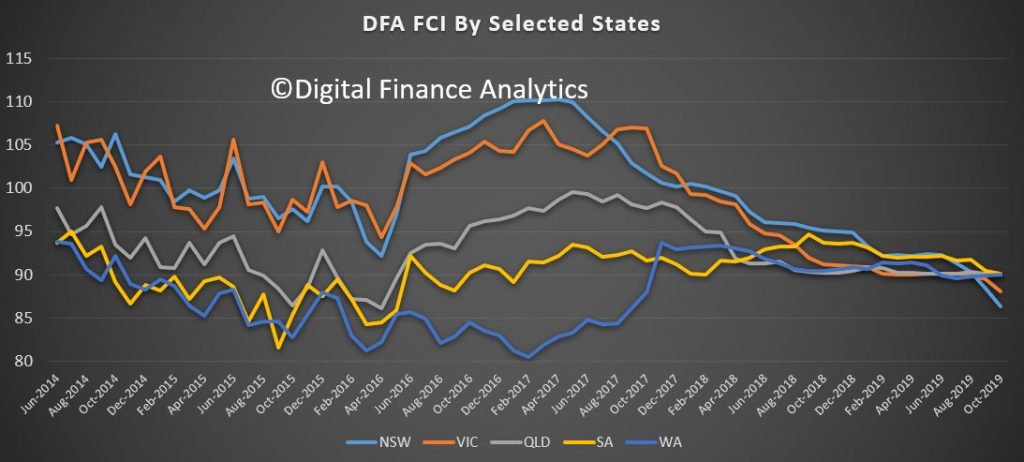

Across the states there were significant falls in NSW and VIC, whilst other states continued to track as in recent months. The main eastern states are now lower than WA and SA, which is a surprising new development.

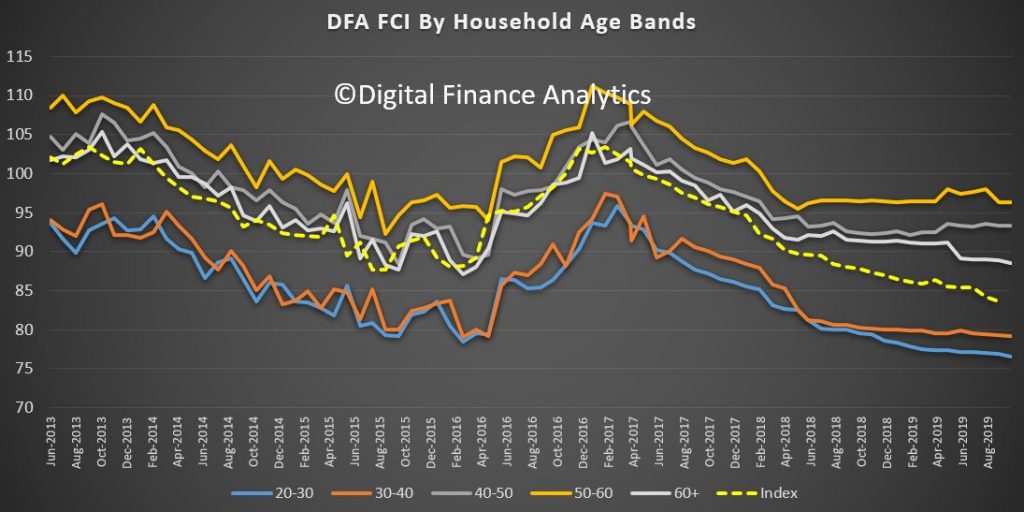

Across the age bands, the falls are mainly among lower aged groups, while those aged 50-60 are feeling more positive thanks to recent stock market rises.

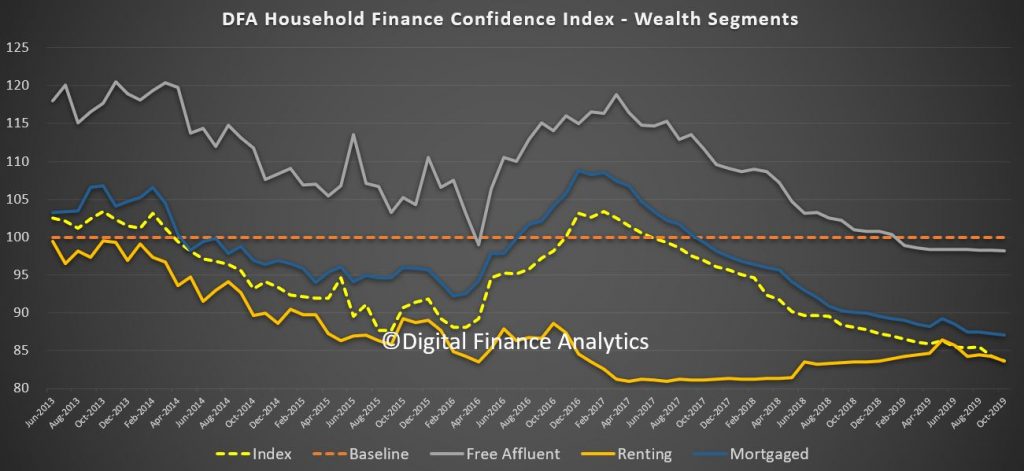

This is also reflected across our wealth segments, with those holding property mortgage free and other financial assets more positive (though still below neutral) compared with mortgage holders and those not holding property at all.

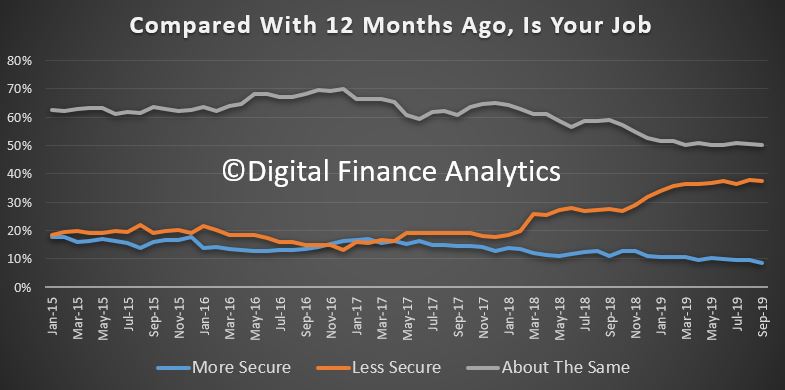

We can then turn to the moving parts within the index, based on our rolling 52,000 household surveys. Employment prospects continue to look shaky, both in terms of under-employment and job security. Jobs in retail and construction and also finance are under-pressure, and the impact of the drought is also hitting some areas. 8% of household felt more secure than a year ago, the lowest read ever in this part of the survey. More households have multiple part-time jobs.

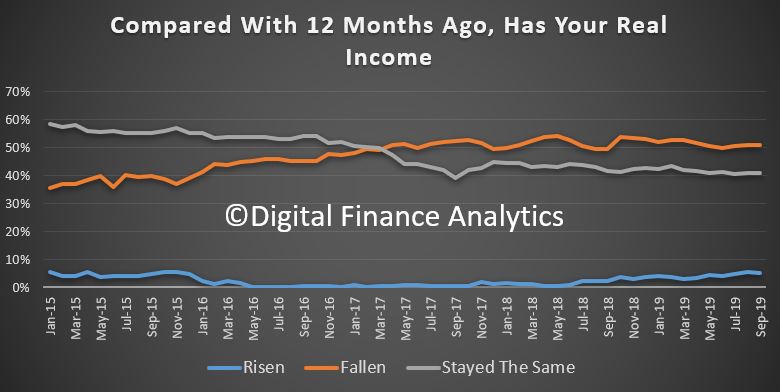

Income remains under pressure, with 51% saying their real incomes have fallen in the past year, while 5% reported an increase, often thanks to switching jobs or employers.

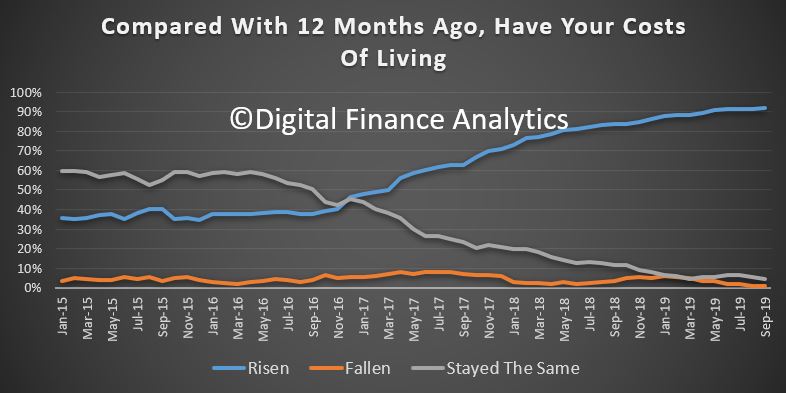

Household budgets are under pressure as costs of living rise, with 91% reporting higher real costs that a year ago, this is a record in our survey. Expenses rose across the board, from child care, health care, school fees and rates. Food costs were higher partly thanks to the drought. There was a small fall in the costs of power, and fuel, but not enough to offset rises elsewhere. Mortgage interest rate falls were blotted up quickly, and the tax refunds where they were received were much lower than people had been expecting.

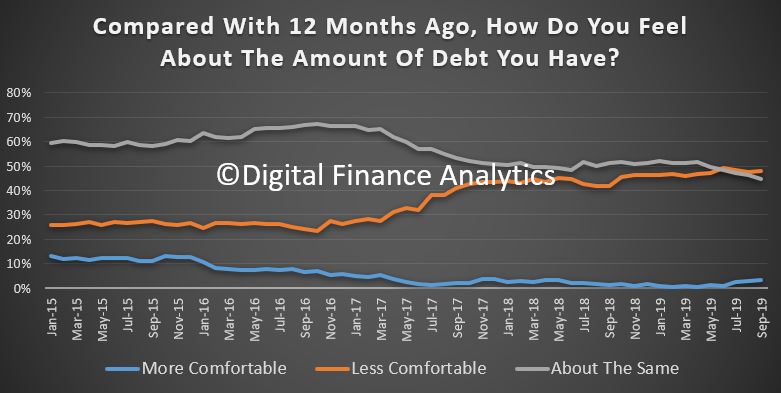

Some households are deleveraging (paying down debt) , while others are more concerned about the amount they owe from mortgages to credit cards and on other forms of credit. 48% of households are less comfortable than a year ago. Lower interest rates are only helping at the margin.

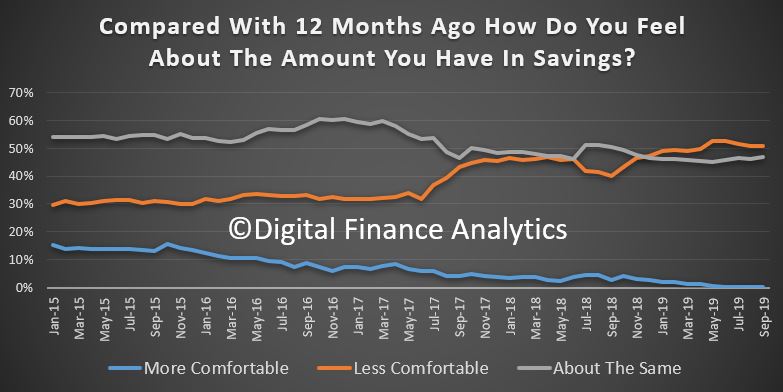

Savings are under pressure from several fronts. Some households are tapping into savings to keep the household budget in check – but that will not be sustainable. Others are seeing returns on term deposits falling away, yet are unwilling to move into higher-risk investment assets. Those in the share markets are enjoying the current bounce, but many expressed concerns about its sustainability. 49% of households are less comfortable than a year ago, while 47% are about the same. Significantly around 27% of households have no savings at all and would have difficulty in pulling $500 together in an emergency. Around half of these households also hold a mortgage. Worth reflecting on this with 32.2% of households in mortgage stress as we also reported today!

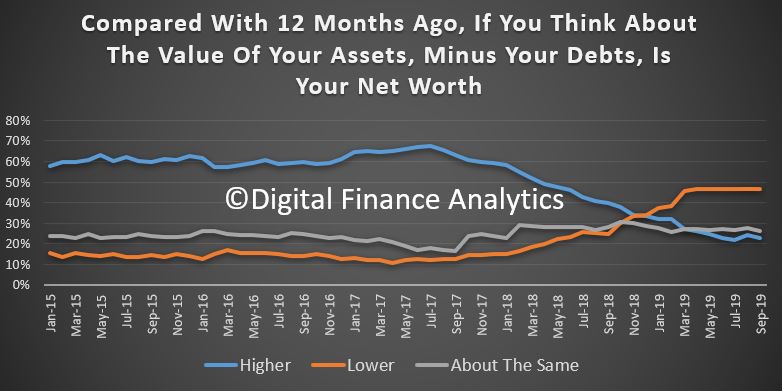

And finally, we consider net worth (assets less liabilities). Here the news is mixed as some households are now convinced their property is worth more citing the recently if narrowly sourced data on rises in Sydney and Melbourne. However other households reported net falls. 24% of households said their net financial position was better than a year ago (up 1.3%), while 45% said they were worse off (down 1.6%). There are also significant regional differences with households in Western Australia and Queensland significantly worse off, while some in inner city areas of Sydney and Melbourne claimed significant advances.

So, overall the status of household confidence continues to weaken, which is consistent with reduced retail activity, and a focus on repaying debt. Unemployment is lurking, but underemployment is real. We also see weaker demand for mortgages ahead, and we will discuss this in more detail in our upcoming household survey release. Without significant economic change, these trends are likely to continue for some time. If the RBA and Government is relying on households to start spending, they will need a very different strategy – including a significant fiscal element. Lower interest rates alone will not cut the mustard.

The RBA held rates today, as expected, but their explanation is turning pretty sour as reality bites. Expect more downgrades and rate cuts ahead, just a matter of time.

I also find it amazing that unlike UK, USA, and NZ there is no streamed press conference nor questions from the media after the announcement. The RBA continues to be more covert than its peers and less exposed to questions about its policy.

At its meeting today, the Board decided to leave the cash rate unchanged at 0.75 per cent.

While the outlook for the global economy remains reasonable, the risks are tilted to the downside. The

US–China trade and technology disputes continue to affect international trade flows and

investment as businesses scale back spending plans because of the uncertainty. At the same time, in most

advanced economies, unemployment rates are low and wages growth has picked up, although inflation

remains low. In China, the authorities have taken steps to support the economy while continuing to

address risks in the financial system.

Interest rates are very low around the world and a number of central banks have eased monetary policy

in response to the persistent downside risks and subdued inflation. Expectations of further monetary

easing have generally been scaled back over the past month and financial market sentiment has improved a

little. Even so, long-term government bond yields are around record lows in many countries, including

Australia. Borrowing rates for both businesses and households are also at historically low levels. The

Australian dollar is at the lower end of its range over recent times.

The outlook for the Australian economy is little changed from three months ago. After a soft patch in

the second half of last year, a gentle turning point appears to have been reached. The central scenario

is for the Australian economy to grow by around 2¼ per cent this year and then for growth

gradually to pick up to around 3 per cent in 2021. The low level of interest rates, recent tax

cuts, ongoing spending on infrastructure, the upswing in housing prices in some markets and a brighter

outlook for the resources sector should all support growth. The main domestic uncertainty continues to

be the outlook for consumption, with the sustained period of only modest increases in household

disposable income continuing to weigh on consumer spending. Other sources of uncertainty include the

effects of the drought and the evolution of the housing construction cycle.

Employment has continued to grow strongly and has been matched by strong growth in labour supply, with

labour force participation at a record high. The unemployment rate has remained steady at around

5¼ per cent over recent months. It is expected to remain around this level for some time,

before gradually declining to a little below 5 per cent in 2021. Wages growth remains subdued

and is expected to remain at around its current rate for some time yet. A further gradual lift in wages

growth would be a welcome development and is needed for inflation to be sustainably within the

2–3 per cent target range. Taken together, recent outcomes suggest that the Australian

economy can sustain lower rates of unemployment and underemployment.

The recent inflation data were broadly as expected, with headline inflation at 1.7 per cent

over the year to the September quarter. The central scenario remains for inflation to pick up, but to do

so only gradually. In both headline and underlying terms, inflation is expected to be close to

2 per cent in 2020 and 2021.

There are further signs of a turnaround in established housing markets, especially in Sydney and

Melbourne. In contrast, new dwelling activity is still declining and growth in housing credit remains

low. Demand for credit by investors is subdued and credit conditions, especially for small and

medium-sized businesses, remain tight. Mortgage rates are at record lows and there is strong competition

for borrowers of high credit quality.

The easing of monetary policy since June is supporting employment and income growth in Australia and a

return of inflation to the medium-term target range. Given global developments and the evidence of the

spare capacity in the Australian economy, it is reasonable to expect that an extended period of low

interest rates will be required in Australia to reach full employment and achieve the inflation target.

The Board will continue to monitor developments, including in the labour market, and is prepared to ease

monetary policy further if needed to support sustainable growth in the economy, full employment and the

achievement of the inflation target over time.