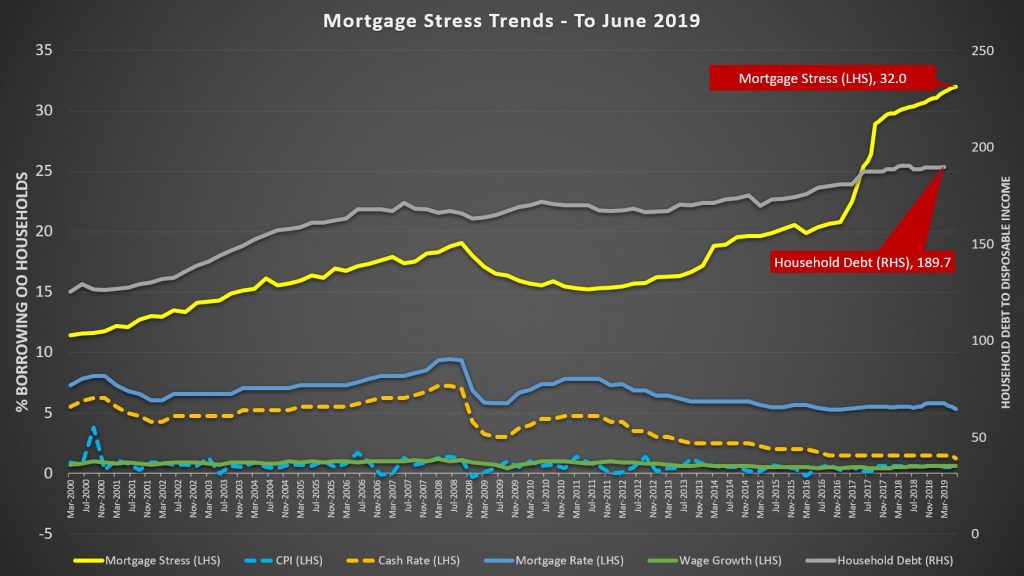

We have released the June 2019 mortgage stress results, based on our running 52,000 household surveys. We found that 32% of households are now dealing with mortgage stress, a record, meaning they are having cash flow issues managing their finances and mortgage repayments.

This translates into more than 1,063,000 households spread across the country, and nearly 71,000 risk default in the year ahead, even taking into account the fall in mortgage repayments represented by the recent rate cuts. Banks loses will rise.

This is because the costs of living continue to run ahead of incomes, while households have larger debts (and are being enticed to buy in the current complex risk environment).

The top post codes in stress are those in the outer suburban fringe areas, where many large estates are still being built, and households are super-highly leveraged.

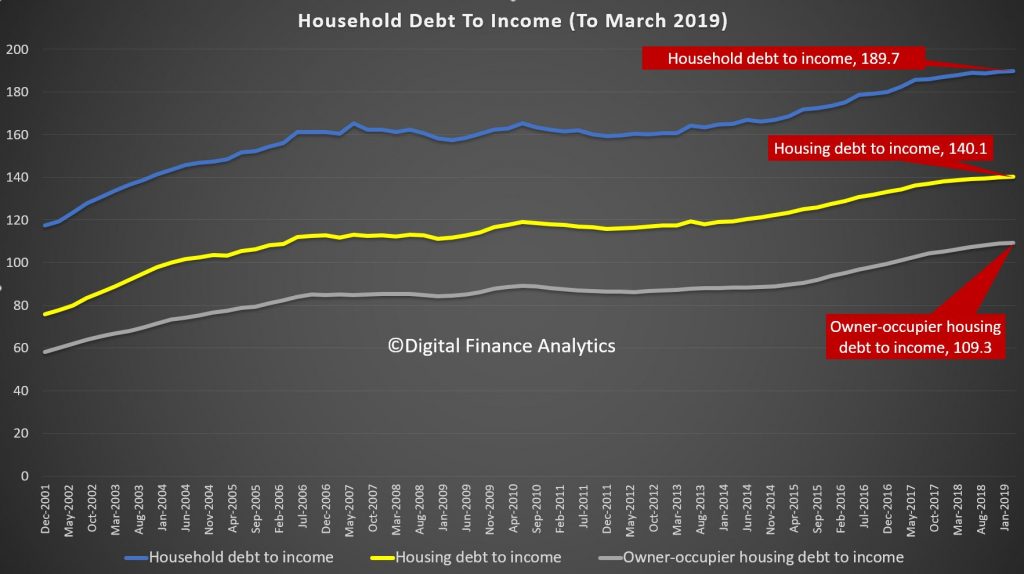

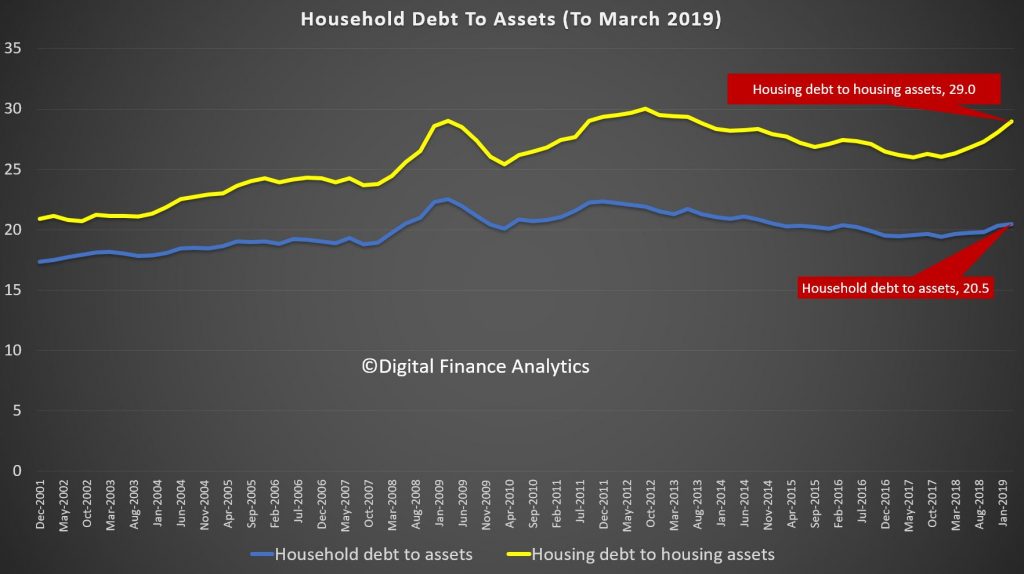

The RBA released their March 2019 data on household ratios. Whilst these series include small business finance, and include households not borrowing, the trends continue to tell the story of debt, and more debt.

The household debt to income ratio is at a record 189.7, while the housing debt to income ratio was 140.1, again a record and the owner occupied housing debt to income ratio was also up, to 109.3. These are high numbers, on a trend and international comparable basis. Households are drowning in debt.

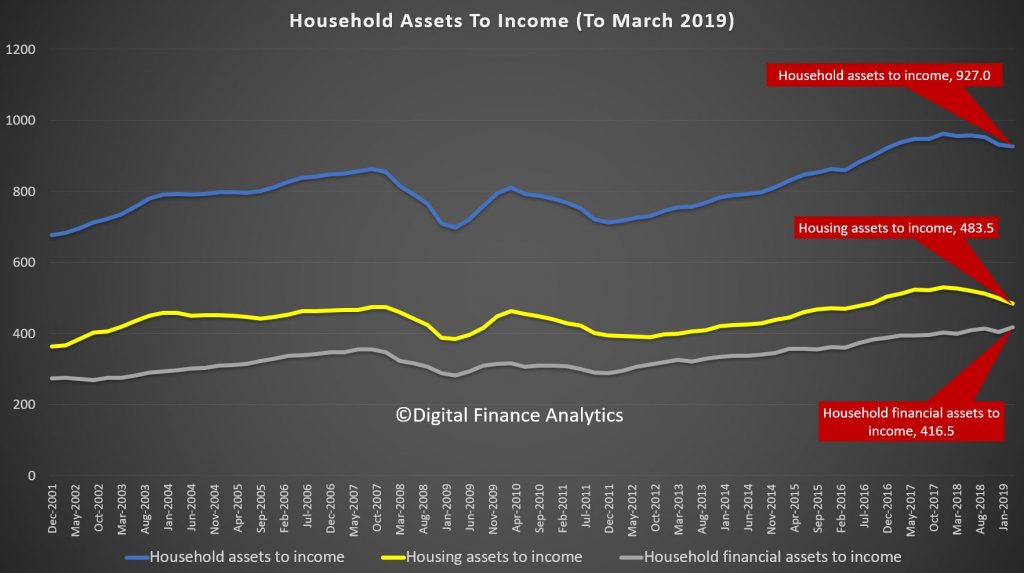

However the asset to income ratios tell another story. As home prices have fallen, so the ratio has decreased, assets are down relative to income. The exception are financial assets, which benefited from the rise in stock prices this year.

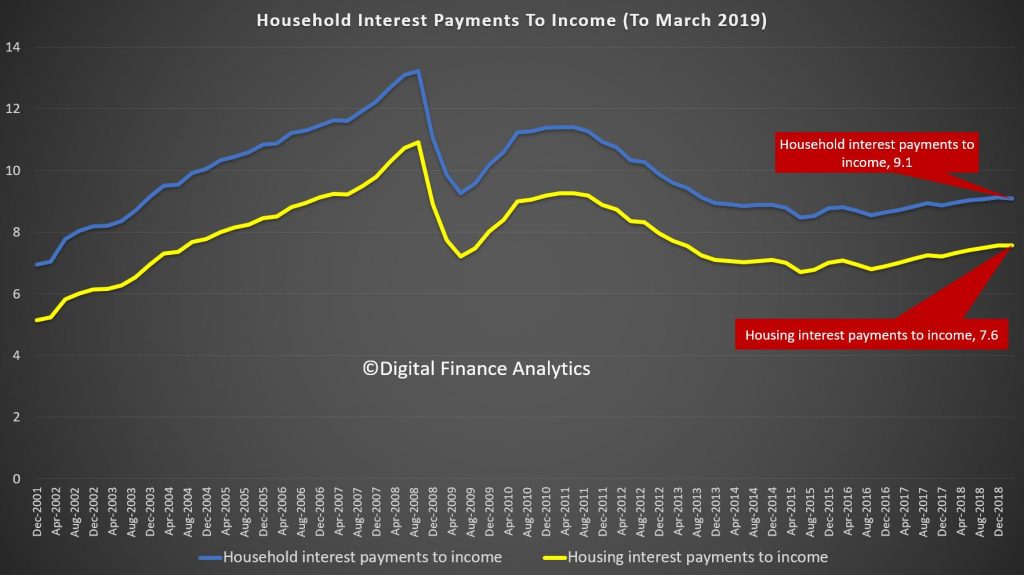

The ratio of interest to income continues to rise because households are borrowing at a faster rate than their incomes are growing, helped of course by lower interest rates. This ratio is below that before the GFC because rates have dropped. And this is the one ratio spruikers turn to to defend the high debt levels – but it is myopic, and going in the wrong direction.

Finally, the RBA data debt to assets shows the pincer movement as home prices fall, and debt rises. This is now heading towards the highest we have seen.

The obvious conclusion is that the debt burden is too great, mortgage stress will go on rising, until the balance between debt and income is restored.

The recent loosening of lending standards simply pours more fuel on the fire. Households are being used a canon fodder in the vein attempt to keep the faltering economy afloat.

At the time of writing, cuts of 25bps had been announced by Resimac, State Custodians and Athena Home Loans. Reduce Home Loans cut its rates by 22bps, taking its lowest advertised rate to 2.89% and putting the lender in the sub 3% category with Greater Bank, HomeStar Finance and BOQ.

Unlike last month’s cut, all the majors responded to the RBA’s announcement before the day’s end.

As with last month, ANZ was the first

to react, announcing a full 25bps decrease across all variable interest

rates for Australian home and residential investment loans.

In June, ANZ elected to pass through just 18bps of the RBA’s 25bps

cut, defying Treasurer Josh Frydenberg’s public demand for a full

transference of the reduction.

CBA was next to go public, opting for a 0.19% reduction across both

its owner occupied and investor P&I standard variable rate home

loans.

The interest only home loans, both owner occupied and investment, received the full 25bps cut.

Last month, CBA passed through the 0.25% cut in full.

The bank also announced a special five-month term deposit rate for

savers, introduced at 2.20% per year, which is a 0.20% increase.

“With official interest rate settings already at record lows, we are

focused on balancing the benefits and the costs of further interest rate

reductions between our 1.6 million home loan and over 6 million savings

customers,” said Angus Sullivan, group executive of retail banking

services.

“It is not possible to pass on the full rate reduction to over $160

billion of our deposits, including deposits where interest rates are at

or already near zero,” he added.

In June, NAB also passed through the full 25bps. However, this month

they elected to reduce variable home loan interest rates by 19bps, but

also provided more commentary along with the decision than the other

majors.

“Decisions like these are difficult and reflect the current unique

circumstances, with home loan rates at record lows at the same time as

deposit and savings rates also being at record lows,” said chief

customer officer of consumer banking, Mike Baird.

“The difference between what we charge and how much it costs us to

fund a mortgage remains under pressure and while the circumstances of

each RBA cash rate decision will vary and has some influence on the cost

of borrowing money, it is not the only funding cost driver for NAB.”

“Getting the balance right is an ongoing challenge for banks and,

with 9 million customers, making the right decisions for our customers

matters for the Australian economy,” he explained.

Westpac rounded out the responses yesterday evening, announcing a

reduction of 20bps for variable rates including owner occupier paying

P&I, investment p&I, and owner occupier for interest only

customers.

The rate was reduced by 0.30% for residential investment property

loans for customers for customers with interest only repayments.

In June, Westpac reduced rates for owner occupiers paying P&I by

just 0.20%, and rates for investor customers with interest only payments

by 0.35%

Courtesy of Philip Lowe, speaking in Darwin tonight. Savers do not even warrant a mention… more the shame!

As I am sure you are aware, this morning the Board decided to reduce the cash rate by a quarter of a percentage point to 1 per cent. This follows a similar adjustment last month. This easing of monetary policy will support jobs growth across the country and provide greater confidence that inflation will be consistent with the medium-term target of 2 to 3 per cent.

Our assessment is that despite the Australian economy having performed reasonably well over recent years, there is still a fair degree of spare capacity in the economy. It is both possible and desirable to reduce that spare capacity. We should be able to achieve a lower rate of unemployment than we currently have and we should also be able to reduce underemployment. If, as a country, we can do this, we could expect a further lift in wages growth and stronger growth in household incomes. These would be good outcomes. As I hope you are aware, the Reserve Bank’s monetary policy framework is centred on the inflation target, but the ultimate objective of our policies is to promote the collective economic prosperity of the people of Australia.

In the Board’s judgement, the easing of monetary policy last month and this month will help promote our collective welfare. At the same time, though, we recognise that the benefits are not evenly distributed across the community and that there are some downsides to monetary easing. Partly for these reasons, over recent times I have been drawing attention to the fact that, as a nation, there are options other than monetary easing for putting us on a better path.

One option is fiscal support, including through spending on infrastructure. This spending adds to demand in the economy and – provided the right projects are selected – it also adds to the country’s productive capacity. It is appropriate to be thinking about further investments in this area, especially with interest rates at a record low, the economy having spare capacity and some of our existing infrastructure struggling to cope with ongoing population growth.

Another option is structural policies that support firms expanding, investing, innovating and employing people. A strong, dynamic, competitive business sector generates jobs. It can help deliver the productivity growth that is the main source of sustainable increases in our wages and incomes. So, as a country, we need to keep focused on this.

To repeat the point, it is important that we think about the task ahead holistically. Monetary policy does have a significant role to play and our decisions are helping support the Australian economy. But, we should not rely on monetary policy alone. We will achieve better outcomes for society as a whole if the various arms of public policy are all pointing in the same direction.

The two cuts in interest rates the Board has delivered recently will make an important contribution to putting us on a better path and winding back spare capacity. It is also worth drawing your attention to a few other developments.

First, borrowing costs for almost all borrowers are now the lowest they have ever been. As an illustration, the Australian Government can borrow for 10 years at around 1.3 per cent, the lowest rate it has faced since Federation in 1901. It is also able to borrow for 30 years at an interest rate of less than 2 per cent. Private businesses and households also face low borrowing rates. This is not only because official interest rates are low, but because credit spreads are low too.

Second, Australia’s terms of trade have risen again, largely due to higher iron ore prices. Investment in the resources sector is also expected to increase over the next few years, after having declined steadily for almost seven years. To be clear, we are not expecting another major mining boom, but we are expecting a solid upswing in the resources sector, which will help the overall economy. I hope that, in time, the effects of this upswing will be felt here in the Northern Territory too.

Third, the exchange rate has depreciated over the past couple of years and, on a trade-weighted basis, is at the bottom end of its range of recent times. This is helping support important parts of the economy.

And fourth, we are expecting stronger growth in household disposable income over the next couple of years, partly due to the expected implementation of the low and middle income tax offset. Stronger growth in incomes should support household spending.

Together, these various developments will help the Australian economy.

At the same time, though, we need to watch global developments very closely. Over recent times, the uncertainty generated by the trade and technology disputes between the United States and China has made businesses in many countries nervous about investing. Many are preferring to sit on their hands, rather than commit to capital spending that is difficult and costly to reverse. The result is less international trade and a weakening trend in investment globally. If this continues for too much longer, the effects on economic growth are likely to be significant. For this reason, the risks to the global economy remain tilted to the downside.

The combination of these persistent downside risks and continuing low rates of inflation has led investors around the world to expect interest rate reductions by all the world’s major central banks. In Europe and Japan, official interest rates are already negative but investors are expecting the central banks to go further into negative territory. And in the United States, investors are expecting a substantial reduction in interest rates over the period ahead. This is quite a different world from the one we were facing earlier in the year.

What all this means for us here in Australia is yet to be determined.

We need to remember that the central scenario for both the global and Australian economies is still for reasonable growth, low unemployment and low and stable inflation. As I discussed a few moments ago, there are a number of developments that are providing support to the Australian economy. So we will be closely monitoring how things evolve over coming months. Given the circumstances, the Board is prepared to adjust interest rates again if needed to get us closer to full employment and achieve the inflation target in a way that supports the collective welfare of all Australians, including those who call the Northern Territory home

At its meeting today, the Board decided to lower the cash rate by 25 basis points to

1.00 per cent. This follows a similar reduction at the Board’s June meeting. This

easing of monetary policy will support employment growth and provide greater confidence that inflation

will be consistent with the medium-term target.

The outlook for the global economy remains reasonable. However, the uncertainty generated by the trade

and technology disputes is affecting investment and means that the risks to the global economy are

tilted to the downside. In most advanced economies, inflation remains subdued, unemployment rates are

low and wages growth has picked up. The slowdown in global trade has contributed to slower growth in

Asia. In China, the authorities have taken steps to support the economy, while continuing to address

risks in the financial system.

Global financial conditions remain accommodative. The persistent downside risks to the global economy

combined with subdued inflation have led to expectations of easing of monetary policy by the major

central banks. Long-term government bond yields have declined further and are at record lows in a number

of countries, including Australia. Bank funding costs in Australia have also declined, with money-market

spreads having fully reversed the increases that took place last year. Borrowing rates for both

businesses and households are at historically low levels. The Australian dollar is at the low end of its

narrow range of recent times.

Over the year to the March quarter, the Australian economy grew at a below-trend

1.8 per cent. Consumption growth has been subdued, weighed down by a protracted period of low

income growth and declining housing prices. Increased investment in infrastructure is providing an

offset and a pick-up in activity in the resources sector is expected, partly in response to an increase

in the prices of Australia’s exports. The central scenario for the Australian economy remains

reasonable, with growth around trend expected. The main domestic uncertainty continues to be the outlook

for consumption, although a pick-up in growth in household disposable income is expected to support

spending.

Employment growth has continued to be strong. Labour force participation is at a record level, the

vacancy rate remains high and there are reports of skills shortages in some areas. There has, however,

been little inroad into the spare capacity in the labour market recently, with the unemployment rate

having risen slightly to 5.2 per cent. The strong employment growth over the past year or so

has led to a pick-up in wages growth in the private sector, although overall wages growth remains low. A

further gradual lift in wages growth is still expected and this would be a welcome development. Taken

together, these labour market outcomes suggest that the Australian economy can sustain lower rates of

unemployment and underemployment.

Inflation pressures remain subdued across much of the economy. Inflation is still, however, anticipated

to pick up, and will be boosted in the June quarter by increases in petrol prices. The central scenario

remains for underlying inflation to be around 2 per cent in 2020 and a little higher after

that.

Conditions in most housing markets remain soft, although there are some tentative signs that prices are

now stabilising in Sydney and Melbourne. Growth in housing credit has also stabilised recently. Demand

for credit by investors continues to be subdued and credit conditions, especially for small and

medium-sized businesses, remain tight. Mortgage rates are at record lows and there is strong competition

for borrowers of high credit quality.

Today’s decision to lower the cash rate will help make further inroads into the spare capacity in

the economy. It will assist with faster progress in reducing unemployment and achieve more assured

progress towards the inflation target. The Board will continue to monitor developments in the labour

market closely and adjust monetary policy if needed to support sustainable growth in the economy and the

achievement of the inflation target over time.

Research from credit information website, CreditSmart.org.au, has

revealed that one year on from the adoption of Comprehensive Credit Reporting

(CCR), most Australian consumers are still unaware of the changes that are

impacting their credit health, and may not know how it can impact their future

credit applications.

The research found that in the last 12 months, only one in

four consumers checked their credit report. More worryingly, consumers who are

struggling with their credit health said they were just as likely to seek

advice from credit repair or debt management services as they would from their

lender or free financial counsellor.

“Consumers are still largely unaware of credit reporting,

what information is contained in their credit report, and what that means about

their borrowing behaviour and overall credit health,” said Mike Laing, CEO of

the Australian Retail Credit Association (ARCA), which founded CreditSmart.

“Our research has found that while awareness has actually

increased 11% from last year, less than 1 in 3 consumers are aware that credit

reporting has changed. Importantly however, awareness is higher among those

with a real need to know – with one in two consumers who are planning to make a

significant purchase in the next 12 months being aware of the changes,” added

Mr Laing.

The rollout of comprehensive credit reporting has

accelerated rapidly in Australia since last year, with more data shared than

ever before. By September this year, comprehensive credit information for 80%

of consumer loan accounts will be available.

“CCR allows lenders to share and view more detailed credit

information about consumers to provide a clearer view of a consumers’ credit

history. This is a positive move for consumers who have a strong history of

making payments on time.” added Mr Laing.

Consumer awareness highest for users of riskier

credit products

According to CreditSmart, credit cards make up the majority of

accounts currently in the CCR system at around 87%, followed by mortgages at

9%.

Yet, people who hold these mainstream types of accounts are

the least aware of the changes to credit reporting and may not be aware of the

value it adds to their credit history, if they have a strong record of making

payments on time.

It was also found that those consumers with products that

are sometimes seen as riskier, such as leases for household goods (61%), cash

loans (54%) and payday loans (79%), plus personal loans (55%), are all far more

aware of the changes to credit reporting[1] This could indicate the users of

those products have been given more information about the changes, or that they

have taken more time to understand the changes.

Consumers using these riskier products also rated their

credit health as significantly worse than users of home loans and credit cards.

Interestingly, Buy Now Pay Later (BNPL) users have

relatively low awareness of credit reporting changes despite significant

numbers rating their credit health as poor.[2]

Consumer awareness a work in progress

Awareness of credit reporting changes is not the same as

understanding the detail behind their credit report, according to Mr Laing.

“It is easy to understand how consumers may become confused

about what’s important when it comes to credit reporting and their credit

health. There’s a lot of information out there and it’s important to bring it

back to a simple, straightforward message.

“We want consumers to be aware of the importance of their

credit history to their credit health – and how that history may impact their

financial future. The steps are to understand how the credit reporting system

has changed, to get your credit report to see your credit history and to manage

the credit that you have responsibly” added Mr Laing.

For more information on the changes to credit

reporting and where to get your free credit reports you should go to www.creditsmart.org.au, which provides clear information on the credit

reporting system to assist consumers to optimise their credit health.

The New Zealand Central Bank is steering a path quite different from the RBA with a move to lift bank capital to much higher levels, in the interests of protecting households and businesses in New Zealand.

The costs, they say, are worth the benefits! Indeed the recent IMF report on NZ endorsed their approach.

Australian Banks operating in New Zealand are resisting according to the AFR – “Australia’s banks would have to raise at least $NZ20 billion ($19.1 billion) to satisfy New Zealand capital requirements, leading the big four to threaten a rethink of their business models if the proposals get the green light”.

But of course banks in Australia need higher capital buffers despite what the local regulators may say. NZ is on the better path.

As part of this journey, the New Zealand Reserve Bank released submissions along with a Summary of Submissions (PDF 399 KB) on the latest consultation paper in its Capital Review, which proposes several measures to ensure a safer banking system for New Zealanders.

There was significant and wide-ranging media and public interest in the How much capital is enough? (PDF 545 KB)paper, with written feedback from 161 submitters. Feedback has also been received from analysts and other interested parties who did not make a formal submission.

“The Reserve Bank welcomes the large number of submissions on this consultation, as well as the effort and consideration that has gone into them,” Deputy Governor Geoff Bascand says. “We believe this shows how important this issue is for everyone, and we are pleased that a broader set of stakeholders has taken an interest in the Capital Review.”

In general, submitters support the Reserve Bank’s objective to ensure that New Zealand’s financial system is safe, acknowledging the economic and well-being impacts of banking crises. Many submitters, particularly from the general public, support the proposed higher capital requirements for banks. A number of submitters observe that higher capital requirements could lead to higher borrowing costs for New Zealanders. Some submitters, in particular banks and business groups, question whether the proposed increases are too large and too costly.

Central to the measures proposed in the consultation paper are increases in regulatory capital buffers for locally incorporated banks. The changes include requiring bank shareholders to increase their stake so that they absorb a greater share of losses should their bank fail, improving the quality of capital, and ensuring banks more accurately measure their risk.

Increasing the amount and quality of capital can be reasonably expected to mean that banks can survive all but the most exceptional shocks, Mr Bascand says. “We think the costs of doing so are outweighed by the benefits – someone’s cost is for society’s broader benefit.”

The Reserve Bank is also consulting on changes to the quality of capital, constraints on modelling capital requirements, and the implementation timeline.

It is continuing its stakeholder outreach programme, which includes conducting focus groups to understand the public’s risk appetite, and engagement with iwi, social sector and industry groups, financial institutions and investors. It has also engaged three external experts for an independent review of its proposals.

“The submissions on the proposals are just one part of the review,” Mr Bascand says. “All these inputs will help us to make robust and well-calibrated policies and decisions that best represent society’s interests.”

In this context, Mr Bascand welcomed reports by two key international financial institutions and a major rating agency last week that support the proposals to increase bank capital ratios.

Following its recent mission to New Zealand, the International Monetary Fund has released a Concluding Statement that highlights the need for strengthening bank capital levels and that the proposals appear commensurate with the systemic financial risks facing New Zealand. The Organisation for Economic Co-operation and Development’s latest Economic Survey of New Zealand expects increases in capital will likely have net benefits for New Zealand. And Standard and Poor’s says that the proposals should not have material impacts on overall credit availability.

The Capital Review began more than two years ago, when the Reserve Bank published an issues paper and opened the first of four public consultations. It will publish its response to the submissions alongside final decisions, expected in November 2019.

Implementation of any new rules will start from April next year. There will be a transition period of a number of years before banks are required to meet the new requirements

The MFAA and the FBAA have called on ASIC to provide the mortgage industry with greater guidance surrounding expense verification, but have urged the regulator not to adopt a “prescriptive approach” to responsible lending, via The Adviser.

The

Australian Securities and Investments Commission (ASIC) has published

submissions from its first round of consultation regarding its proposal

to update its responsible lending guidelines (RG 209).

In February, ASIC stated that it considered it “timely”

to review and update its guidance (in place since 2010) in light of its

regulatory and enforcement work since 2011, changes in technology, and

the release of the banking royal commission’s final report.

ASIC

added that its review of RG 209 will consider whether the guidance

“remains effective” and will seek to identify changes and additions to

the guidance that “may help holders of an Australian credit licence to

understand ASIC’s expectations for complying with the responsible

lending obligations”.

In submissions to ASIC, the Mortgage &

Finance Association of Australia (MFAA) and the Finance Brokers

Association of Australia (FBAA) called for greater clarification

surrounding guidelines that relate to the verification of a borrower’s

expenses (which was a key point of scrutiny during the royal commission).

The

MFAA encouraged ASIC to provide “as much guidance as possible”, and

lamented the lack of uniformity in the application of current

guidelines.

“An unfortunate side effect of these changes is that

the requirements of individual lenders have changed from being

reasonably consistent to being quite diverse,” the MFAA noted.

“This is causing significant cost, confusion and delay for consumers as well as for brokers.

“This

is not a good consumer outcome because it has become very difficult for

brokers to be familiar with the requirements of multiple lenders whose

credit policies vary considerably.”

The industry association

claimed that a disparity in the credit policies imposed by lenders may

limit borrower choice by “resulting in brokers dealing with a smaller

panel of lenders”.

“It is important that RG 209 provides as much

guidance as possible, specifically dealing with the five most common

finance types (home loans, residential investment loans, car loans,

credit cards and personal loans – excluding small amount credit

contracts) to assist consistency in consumer accessibility to these

products while supporting the spread of credit access across the market

through the enhanced clarity of regulatory expectation,” the MFAA added.

“We

envisage that within each of these five loan types, RG 209 should

specify ‘base’ inquiries and verifications because current industry

standards are often quite similar across the product range.”

The

FBAA agreed, calling for “some additional guidance to be provided around

expense verification”, but has warned against a move to a more

prescriptive approach to responsible lending.

“Responsible lending is principles-based and intended to be flexible, adaptable and technology neutral,” the FBAA stated.

“There

are genuine risks associated with guidance becoming too prescriptive.

It would undermine the intentions of the responsible lending framework,

stifle productivity and innovation and impede consumer access to

regulated finance.”

Public hearing to be held in August

Last week, ASIC confirmed that it will host a new set of public hearings to further discuss its proposed changes to its responsible lending guidelines.

The

corporate regulator has now confirmed that the hearings will take place

in August and will be held in both Sydney and Melbourne.

ASIC

stated that the hearings, which will be live streamed online, are aimed

at “testing the views of stakeholders and providing greater

understanding of business operations”.

“The responsible provision of credit is critical to the Australian economy,” ASIC commissioner Sean Hughes said.

“We are taking this opportunity to test views to make sure our guidance remains relevant, clear and timely.

“Public hearings will provide a robust and transparent way to air issues and views raised in written submissions.”

The

stakeholders invited to participate in the hearings will be drawn from

the groups or individuals who provided a written submission to ASIC on

the responsible lending guidance.

The open banking regime officially began yesterday with the four major banks offering data on a variety of products as part of the regime’s roll-out, via InvestorDaily.

The

four major banks had a deadline of 1 July to make product data

available on all credit and debit card, deposit and transaction accounts

with more products to follow.

By February, first mortgage data

will have to be available, with eventually all products being available

for the major banks by 2020. 1 July 2020 is the start date for all other

banks to begin offering their credit and debit card product data with

an end date of 2021.

Customer data will be included in the regime

by 1 February 2020, which will allow consumers to more fully control

their data and enable greater transparency and competition throughout

the industry.

Open banking has been sweeping across the world, with the most relatable example for Australia being the UK open banking regime.

The

UK introduced theirs following an exposure of poor practice, not

dissimilar to Australia. Where it differs though is that the UK regime

applies to only nine banks, whereas Australia’s will apply to all ADIs.

The

Australian regime only grants read-only access to data with reciprocal

obligations and an eventual plan to open to other industries, such as

utilities.

What it will eventually mean is that customers of a

bank can request or give consent for their data to be shared with an

accredited third party, such as a bank, financial services provider,

utility provider or a telecommunications provider.

The regime will

break down the barriers consumers have faced in finding the best

banking products and eventually switching to that provider.

Commonwealth

Bank’s general manager of digital banking, Kate Crous, told Investor

Daily that the bank was supportive of the model that puts customers in

control and had worked hard to ensure they were ready.

“We have

worked hard with regulators and other industry participants to ensure

the Consumer Data Right regime will be successful, particularly in

building consumer trust and confidence around the use and exchange of

their data.

“The first milestone is publishing product information

via an application programming interface (API) from 1 July 2019. This

will enable an easier comparison of banking products from financial

institutions and allow the industry to test the APIs before sharing

consumer data next year,” she said.

Ms Crous said developers are now able to access information on how to integrate with the CBA APIs.

Westpac’s chief data and strategy officer, Jamie Twiss, said keeping data safe was crucial and the pilot was an important step.

“Westpac

is focusing on creating a trusted open banking regime that is secure,

flexible and easy to use for all Australians. The pilot program will lay

initial foundations to test the performance, reliability and security

of the system before any personal consumer data is shared. It will also

give software developers and fintechs a network of financial

institution’s data to build and improve financial services.”

Westpac

will provide generic information on product data as of today, which

will include interest rates, discounts, eligibility criteria, product

features and descriptions plus fees and charges.

A NAB

spokesperson told Investor Daily that their focus was on ensuring that,

as an industry, open banking worked for the consumer.

“This is a

complex change to the industry and the timelines are challenging, but we

firmly believe that speed shouldn’t compromise safety and customer

experience; getting it right is paramount to consumer trust and

confidence in the system,” NAB said.

The spokesperson

said NAB had actively started to develop processes since back in 2017 to

be ready for open banking and would continue to work with Data 61 and

ACCC.

Fintech response

Deputy chief

executive of neobanks Volt Luke Bunbury said it will mean that the

incumbent banks will need to innovate to compete with newer entrants.

“This

means the incumbent banks will have to innovate to compete, as there

will be a long line of fintechs and neobanks like Volt wanting to

harness this data to offer customers a superior banking experience.

“Customers

will be the masters of their data, and third parties will have to earn

it by being innovative and trustworthy,” he said.

Part of this was changing the narrative by offering an improvement to lives and not just the sale of products, said Mr Bunbury.

“Volt

and other innovative banks will be able to help Australians find and

secure better deals on a range of banking and even non-banking services,

like utilities and travel.

“By enabling data to be shareable

across financial institutions, it will be also possible for customers to

manage multiple bank accounts from one mobile app, regardless of

whether the accounts are held with rival banks,” he said.

Chief executive of Verrency David Link said the regime was going to eventually drive greater innovation.

“While

1 July 2019 will not drastically change the way Australians bank – as

only product, rather than customer, data will be available until 1

February 2020 – this is a huge step towards that much more

transformative change,” Mr Link said.

Banks would have to start to

offer a personalised consumer offering, said Mr Link, and those that

are agile were going to thrive.

“The effective use of data and

access to new value-added services will slowly become a major

decision-driver for consumers when it comes to choosing or changing who

‘owns their relationship’.

“Banks which don’t take this extremely

seriously are going to slowly struggle to remain competitive. On the

other hand, those which take steps to become more agile – especially in

their ability to deliver value around the consumer relationship – are

going to thrive in the post-open banking landscape,” he said.

Monetary policy can no longer be the main engine of economic growth,

and other policy drivers need to kick in to ensure the global economy

achieves sustainable momentum, the Bank for International Settlements

(BIS) writes in its Annual Economic Report.

In its flagship economic report, the BIS calls for a better balance

between monetary policy, structural reforms, fiscal policy and

macroprudential measures. This would allow the global economy to move

away from the debt-fuelled growth model that risks turbulence ahead.

“Navigating the way to clearer skies means balancing speed with

stability and conserving some fuel to cope with possible headwinds,”

says BIS General Manager Agustín Carstens.

“A sustainable flight path requires the long-overdue full engagement of

all four engines of policy, rather than short-term turbo charges.”

In the report, the BIS says that although global expansion hit a soft

patch last year, the resilience of service industries and strong labour

markets can support growth in the near term. Employment increases and

solid wage rises have sustained consumption. Still, significant risks

remain, including trade tensions and rising debt, particularly in the

corporate sector in some economies.

“As well as clouding future demand and investment prospects, the

trade tensions raise questions about the viability of existing supply

chain structures and about the very future of the global trading

system,” says Carstens. “Trade wars have no winners.”

Other risks to the outlook include weak bank profits in several

advanced economies and deleveraging in some major emerging market

economies (EMEs), particularly China. Necessary moves to curb credit

growth there act as a drag on activity.

EMEs’ greater sensitivity to global financial conditions and

resulting capital flows has meant that, since the financial crisis, they

have had to cope with strong spillovers from accommodative monetary

policy in advanced economies. One chapter of the report analyses how EME

monetary policy frameworks have sought to tackle the resulting trade-offs.

The frameworks typically combine inflation targeting with currency

intervention, and are complemented with macroprudential measures to

address the build-up of financial vulnerabilities.

“This kind of multiple-tool policymaking is not yet very well

anchored conceptually. EME monetary policy practice has moved ahead of

theory. Theory has to catch up,” says Claudio Borio, Head of the

Monetary and Economic Department.

The BIS’s financial results, published at the same time in the Annual Report 2018/19,

include a balance sheet total of SDR 291.1 billion (USD 403.7 billion)

at end-March 2019 and a net profit of SDR 461.1 million (USD 639.5

million).

Property expert Joe Wilkes and I discuss the latest housing sales and lending data from New Zealand, plus deposit insurance and first time buyers. Things are turning a bit sour!