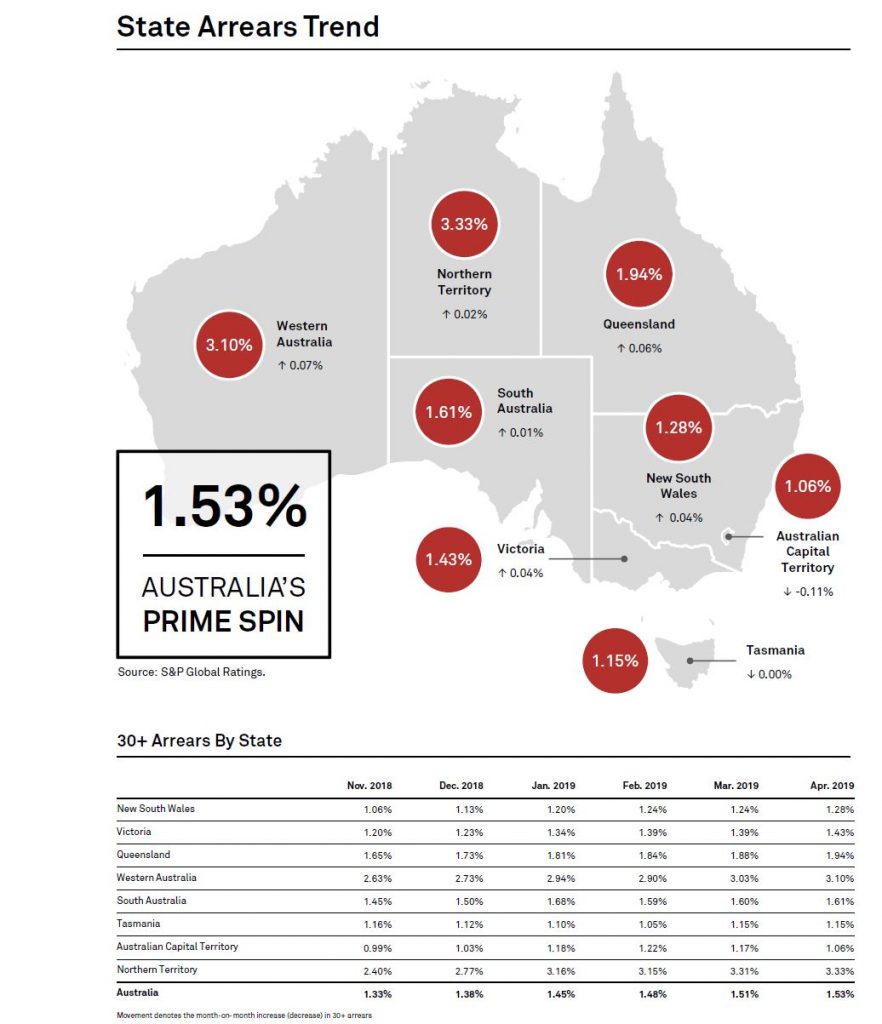

The S&P Spin Index for April shows a further rise in mortgage defaults, with WA and QLD leading the way. Only the ACT fell.

Now of course these are a myopic cross selection of loans, because they are those in the securitised pools. However, the rising trend continues.

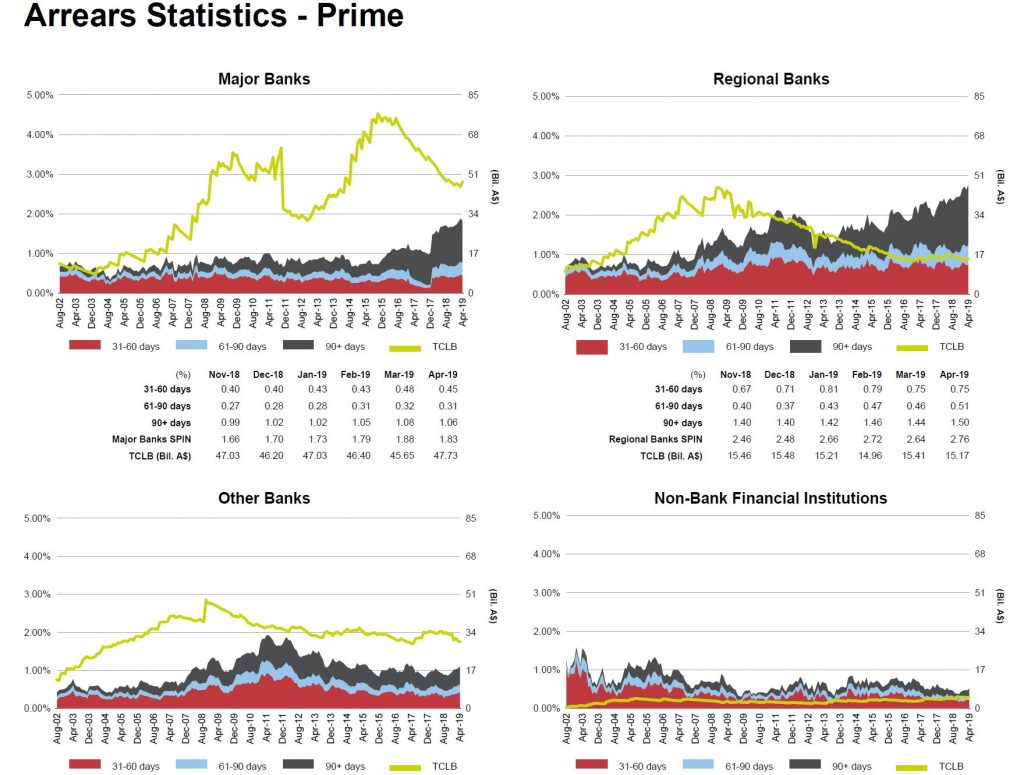

Within the mix, 90+ days arrears continue to climb especially among Regionals. It is worth reflecting that any upturn in the property market, to the extent it emerges, will have precisely NO effect on existing cash-strapped households, as the flat incomes, rising costs pincer movements continue to grip.

This was predictable, given the rising mortgage stress we have been detecting for some time. Of course the question becomes, will this lead to higher bank losses down the track?

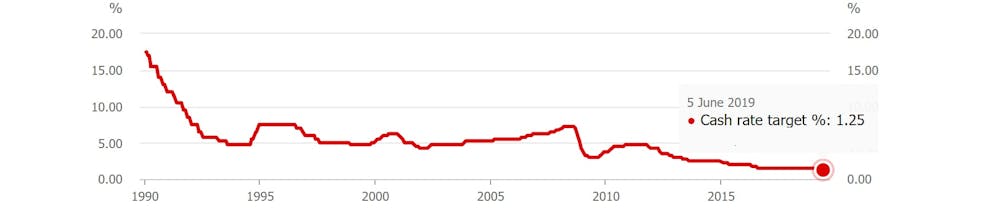

With its official cash rate now expected to fall below 1% to a

new extraordinarily low close to zero, all sorts of people are saying

that the Reserve Bank is in danger of “running out of ammunition.” Ammunition might be needed if, as during the last financial crisis, it needs to cut rates by several percentage points.

This view assumes that when the cash rate hits zero there is nothing more the Reserve Bank can do.

The view is not only wrong, it is also dangerous, because if taken

seriously it would mean that all of the next rounds of stimulus would

have to be come from fiscal (spending and tax) policy, even though

fiscal policy is probably ineffective long-term, its effects being neutralised by a floating exchange rate.

The experience of the United States shows that Australia’s Reserve

Bank could quite easily take measures that would have the same effect as

cutting its cash rate a further 2.5 percentage points – that is: 2.5

percentage points below zero.

In a report released on Tuesday

by the University of Sydney’s United States Studies Centre, I document

the successes and failures of the US approach to so-called “quantitative

easing” (QE) between 2009 and 2014.

It demonstrates that it is always possible to change the instrument

of monetary policy from changes in the official interest rate to changes

in other interest rates by buying and holding other financial

instruments such as long-term government and corporate bonds.

The more aggressively the Reserve Bank buys those bonds from private

sector owners, the lower the long-term interest rates that are needed to

place bonds and the more former owners whose hands are filled with cash

that they have to make use of.

In the US the Federal Reserve also used “forward guidance”

about the likely future path of the US Federal funds rate to convince

markets the rate would be kept low for an extended period.

It is unclear which mechanism was the most powerful, or whether the

Fed even needed to buy bonds in order to make forward guidance work.

However in a stressed economic environment, it is worth trying both.

As it comes to be believed that interest rates will stay low for an

extended period, the exchange rate will fall, making it easier for

Australian corporates to borrow from overseas and to export and compete

with imports.

The consensus of the academic literature is that QE cut long-term

interest rates by around one percentage point and had economic effects

equivalent to cutting the US Federal fund rate by a further 2.5 percentage points after it approached zero.

QE need not have limits…

Based on US estimates, Australia’s Reserve Bank would need to

purchase assets equal to around 1.5% of Australia’s Gross Domestic

Product to achieve the equivalent of a 0.25 percentage point reduction

in the official cash rate. That’s around A$30 billion.

With over A$780 billion in long-term government (Commonwealth and

state) securities on issue, there’s enough to accommodate a very large

program of Reserve Bank buying, and the bank could also follow the

example of the Fed and expand the scope of purchases to include

non-government securities, including residential mortgage-backed

securities.

It could also learn from US mistakes. The Fed was slow to cut its

official interest rate to near zero and slow to embark on QE in the wake

of the 2008 financial crisis. Its first attempt was limited in size and

duration. Its success in using QE to stimulate the economy should be

viewed as the lower bound of what’s possible.

…even if it becomes less effective as it grows

It often suggested (although it is by no means certain)

that monetary policy becomes less effective when interest rates get

very low, but this isn’t necessarily an argument to use monetary policy

less. It could just as easily be an argument to use it more.

Because there is no in-principle limit to how much QE a central bank

can do, it is always possible to do more and succeed in lifting

inflation rate and spending.

Fiscal policy may well be even less effective. To the extent that it

succeeds, it is likely to push up the Australian dollar, making

Australian businesses less competitive.

US economist Scott Sumner believes the extra bang for the buck from government spending or tax cuts (known as the multiplier) is close to zero.

Reserve Bank Governor Philip Lowe this month appealed for help from the government itself, asking in particular for extra spending on infrastructure and measures to raise productivity growth.

He is correct in identifying the contribution other policies can make

to driving economic growth. No one seriously thinks Reserve Bank

monetary policy can or should substitute for productivity growth.

But it is a good, perhaps a very good, substitute for government spending that does not contribute to productivity growth.

Three myths about quantitative easing

In the paper I address several myths about QE. One is that it is

“printing money”. It no more prints money than does conventional

monetary policy. It pushes money into private sector hands by adjusting

interest rates, albeit a different set of rates.

Another myth is that it promotes inequality by helping the rich to get richer.

It is a widely believed myth. Former Coalition treasurer Joe Hockey told the British Institute of Economic Affairs in 2014 that:

Loose monetary policy actually helps the rich to get richer. Why?

Because we’ve seen rising asset values. Wealthier people hold the

assets.

But it widens inequality no more than conventional monetary policy,

and may not widen it at all if it is successful in maintaining

sustainable economic growth.

A third myth is that it leads to excessive inflation or socialism.

In the US it has in fact been associated with some of the lowest

inflation since the second world war. These days central banks are more

likely to err on the side of creating too little inflation than too

much.

Some have argued that QE in the US is to blame for the rise of left-wing populists

like Alexandria Ocasio-Cortez and “millennial socialism”. But it is probably truer to say that their grievances grew out of too tight rather than too lose monetary policy.

QE has been road tested. We’ve little to fear from it, just as we have had little to fear from conventional monetary policy.

Author: Stephen Kirchner, Program Director, Trade and Investment, United States Studies Centre, University of Sydney

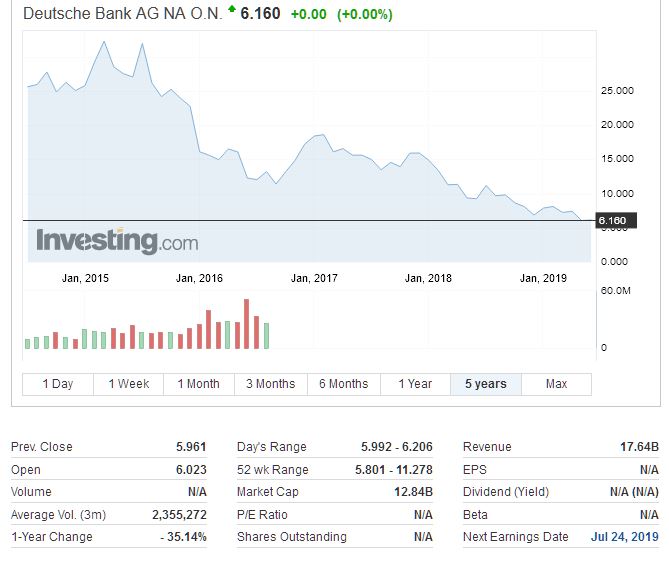

According to a report in the Financial Times, Deutsche Bank is going to overhaul its trading operations and create “bad bank” which will house or sell assets valued at up to €50B (risk adjusted). This would lead to the closure or reduction in its U.S. equity and trading businesses.

While this will likely de-risk the business, it will also reduce profitability (as the US trading division contributed higher returns, and the remaining bank will rely more on deposits for funding. This helps to explain the falls in its share price.

The Australian Prudential Regulation Authority (APRA) has released its response to the first round of consultation on proposed changes to the capital framework for authorised deposit-taking institutions (ADIs).

The package of proposed changes, first released in February last year, flows from the finalised Basel III reforms, as well as the Financial System Inquiry recommendation for the capital ratios of Australian ADIs to be ’unquestionably strong’.

ADIs that already meet the ‘unquestionably strong’ capital targets that APRA announced in July 2017 should not need to raise additional capital to meet these new measures. Rather, the measures aim to reinforce the safety and stability of the ADI sector by better aligning capital requirements with underlying risk, especially with regards to residential mortgage lending.

APRA received 18 industry submissions to the proposed revisions, and today released a Response Paper, as well as drafts of three updated prudential standards: APS 112 Capital Adequacy: Standardised Approach to Credit Risk; the residential mortgages extract of APS 113 Capital Adequacy: Internal Ratings-based Approach to Credit Risk; and APS 115 Capital Adequacy: Standardised Measurement Approach to Operational Risk.

The Response Paper details revised capital requirements for residential mortgages, credit risk and operational risk requirements under the standardised approaches, as well as a simplified capital framework for small, less complex ADIs. Other measures proposed in the February 2018 Discussion Paper, as well as improvements to the transparency, comparability and flexibility of the ADI capital framework, will be consulted on in a subsequent response paper due to be released in the second half of 2019.

After taking into account both industry feedback and the findings of a quantitative impact study, APRA is proposing to revise some of its initial proposals, including:

for residential mortgages, some narrowing in the capital difference that applies to lower risk owner-occupied, principal-and-interest mortgages and all other mortgages;

more granular risk weight buckets and the recognition of additional types of collateral for SME lending, as recommended by the Productivity Commission in its report on Competition in the Financial System; and

lower risk weights for credit cards and personal loans secured by vehicles.

The latest proposals do not, at this stage, make

any change to the Level 1 risk weight for ADIs’ equity investments in

subsidiary ADIs. This issue has been raised by stakeholders in response to

proposed changes to the capital adequacy framework in New Zealand. APRA has

been actively engaging with the Reserve Bank of New Zealand on this issue, and

any change to the current approach will be consulted on as part of APRA’s

review of Prudential Standard

APS 111 Capital Adequacy: Measurement of Capital later this year.

APRA’s consultation on the revisions to the ADI capital framework is a

multi-year project. APRA expects to conduct one further round of consultation

on the draft prudential standards for credit risk prior to their finalisation.

It is intended that they will come into effect from 1 January 2022, in line

with the Basel Committee on Banking Supervision’s internationally agreed

implementation date. An exception is the operational risk capital proposals for

ADIs that currently use advanced models: APRA is proposing these new

requirements be implemented from the earlier date of 1 January 2021.

APRA Chair Wayne Byres said: “In setting out these latest proposals, APRA has

sought to balance its primary objectives of implementing the Basel III

reforms and ‘unquestionably strong’ capital ratios with a range of important

secondary objectives. These objectives include targeting the structural

concentration in residential mortgages in the Australian banking system, and

ensuring an appropriate competitive outcome between different approaches to

measuring capital adequacy.

“With regard to the impact of risk weights on competition in the mortgage

market, APRA has previously made changes that mean any differential in overall

capital requirements is already fairly minimal. APRA does not intend that the

changes in this package of proposals should materially change that calibration,

and will use the consultation process and quantitative impact study to ensure

that is achieved.

“It is also important to note that the proposals announced today will not

require ADIs to hold any capital additional beyond the targets already

announced in relation to the unquestionably strong benchmarks, nor do we expect

to see any material impact on the availability of credit for borrowers,” Mr

Byres said

The Swiss bank has revealed plans to launch a comprehensive strategic wealth management partnership in Japan, via InvestorDaily.

UBS

and Sumitomo Mitsui Trust Holdings Inc. (SuMi Trust Holdings) have

agreed to establish a joint venture, 51 percent owned by UBS, that will

offer products, investment advice and services beyond what either UBS

Global Wealth Management or SuMi Trust Holdings is currently able to

deliver on its own.

The JV will open UBS’s current wealth

management customer base to a full range of Japanese real estate and

trust services, while SuMi Trust Holdings’ clients – one of the largest

pools of high-net-worth (HNW) and ultra-high-net-worth (UHNW)

individuals in Japan – will be able to access UBS’s wealth management

services, including securities trading, research and advisory

capabilities.

“No wealth management firm today provides this range

of offerings to Japanese clients under a single roof. UBS expects the

new joint venture to fill this gap by offering expanded products and

services to clients from both franchises,” UBS said in a statement.

“This

is the Japanese market’s first-ever wealth management partnership

developed between an international financial group and a Japanese trust

bank. Subject to receiving all necessary regulatory approvals, the two

companies plan to begin offering each other’s products and services to

their respective current and future clients from the end of 2019. Also

subject to approvals, these activities will ultimately be incorporated

into a new co-branded joint venture company by early 2021.”

UBS Group CEO Sergio P. Ermotti said the Swiss banking giant has over 50 years of history in Japan.

“This

landmark transaction with a top-level local partner will ideally

complement our service and product offering to the benefit of clients,”

he said. “The joint venture is a blueprint for how complementary

partnerships can unlock value for clients as well as shareholders.”

Zenji

Nakamura, UBS’s Japan country head, said the transaction is a boost for

the group’s overall business in Japan, bringing reputational benefits

to its investment banking and asset management units, which fall outside

the alliance.

“It is a new milestone that sends a clear message of long-term commitment to the Japanese market.”

UBS

will contribute all of its current wealth management business in Japan

to the new company, while SuMi Trust Holdings will extend its trust

banking expertise and refer relevant clients to the new joint venture.

Sumitomo

Mitsui Trust Holdings is Japan’s largest trust banking group, with

Sumitomo Mitsui Trust Bank Limited serving as its core business. It

offers a range of services, including banking, real estate, asset and

wealth advisory to individuals and corporate clients. As of end March

2018, it held 285 trillion yen in assets under custody – Japan’s largest

such pool – and a significant portion of those assets come from HNW and

UHNW clients.

UBS boasts over US$2.4 trillion in assets under management. It operates from locations in Tokyo, Osaka and Nagoya.

The two companies have agreed not to disclose the financial details of the transaction.

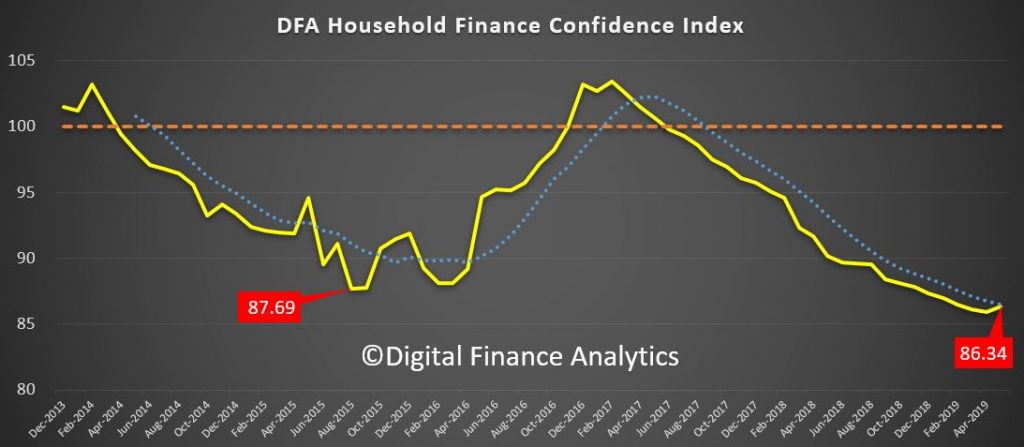

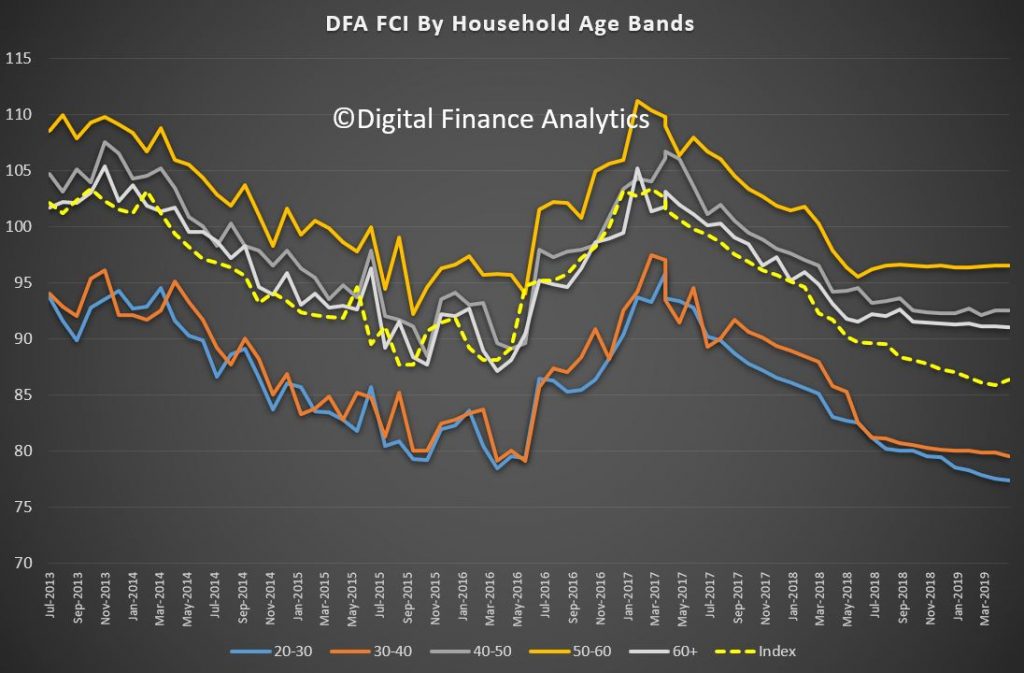

We have released our latest financial confidence index which is derived from our rolling 52,000 household surveys. The index moved a little higher since the election, reflecting some more positive vibes from property investors, at the margin, and from those holding property more generally.

It is all relative however, as the current read of 86.34 is up from April’s 85.9, but the overall measure is still in deeply negative territory.

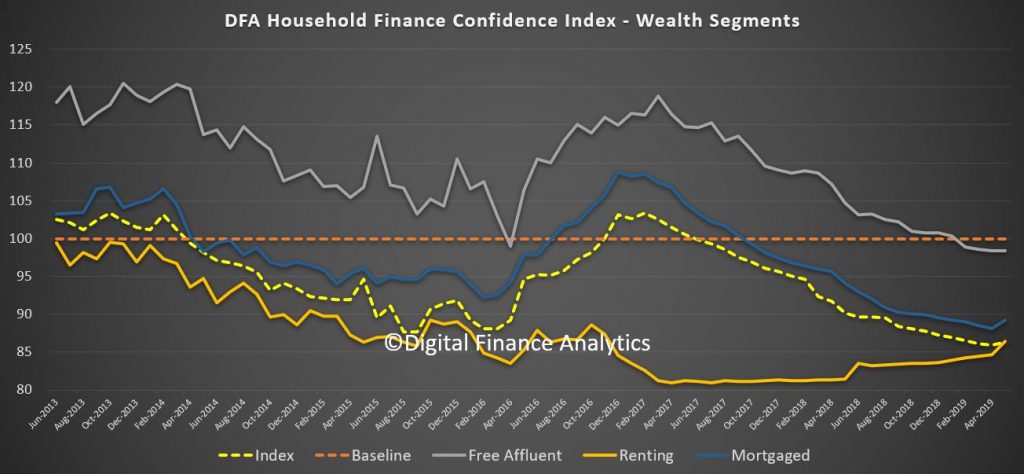

Looking at the segments by wealth, there was a bounce in those with mortgages, and also those renting or living with family or friends – but again still in negative territory. Those with property, and no mortgage hardly reacted at all.

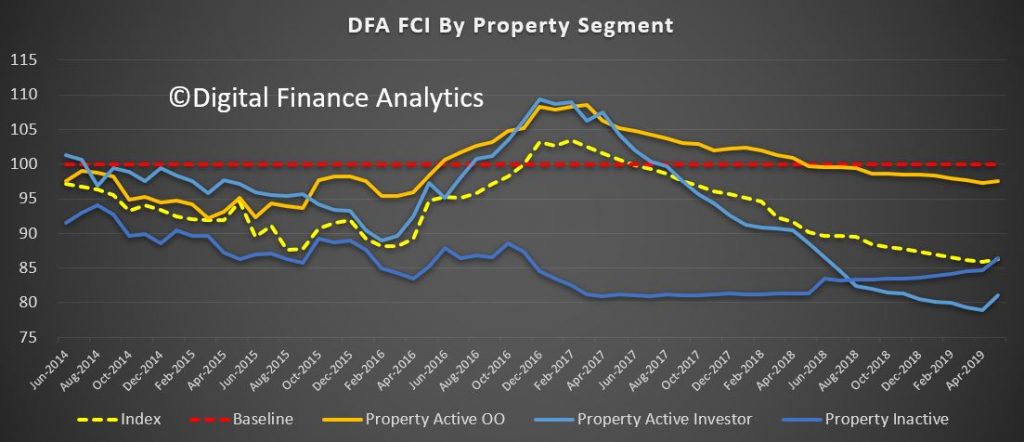

Analysis across our property segments shows a move up from property investors (now expecting no changes to capital gains and negative gearing), a slight improvement from owner occupied borrowers, and a kick up from those renting.

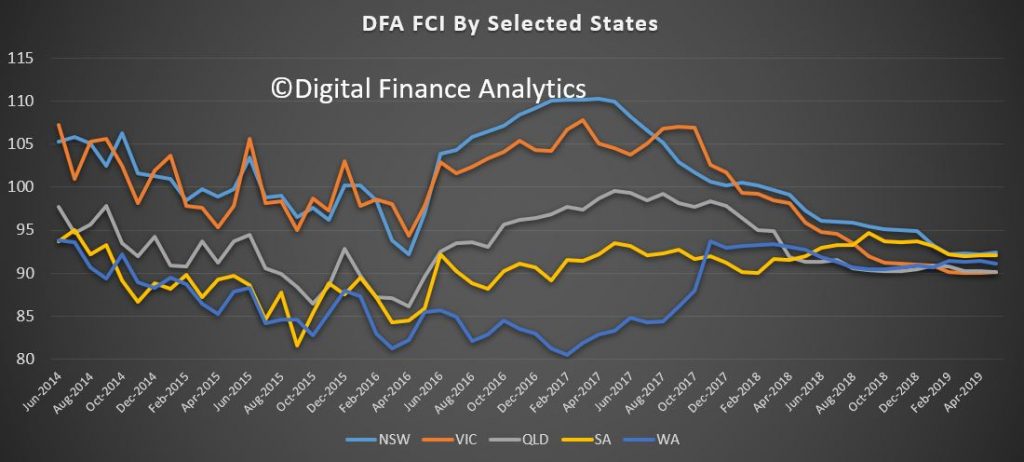

By states, the convergence of recent times continues, although NSW and VIC saw a slight improvement, while WA and QLD saw a deterioration (linked to higher default rates in these states).

Younger household scores fell again, but there was a bounce in those aged 40-50 and 50-60, directly linked to the slight change in property investment sentiment.

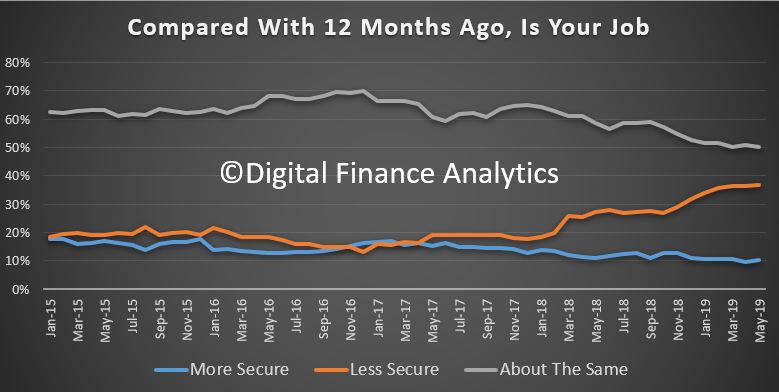

Within the moving parts, there was little movement in job security, with 36% still feeling less secure than a year ago. Public sector jobs look less secure now.

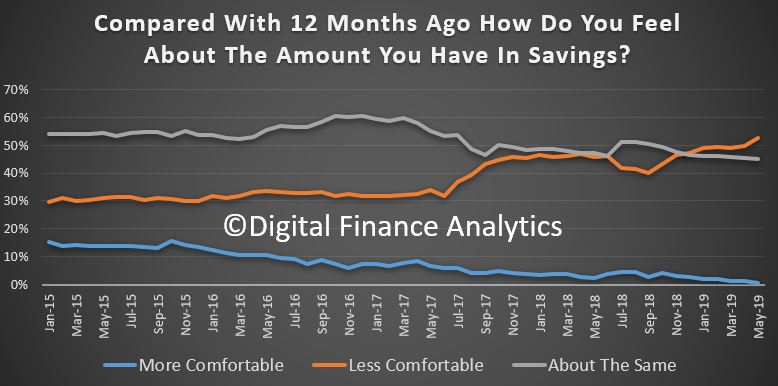

Savings remain under pressure, with lower rates on bank deposits, though higher returns from shares. The prospect of lower deposit rates took the “less comfortable” rating down 2.88% compared with the previous month.

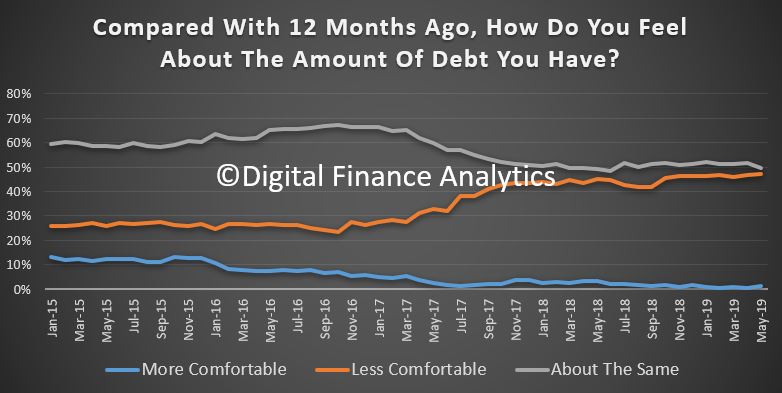

Debt remains a concern, with 47% worried by the amount of credit they hold, while 49% are feeling about the same as a year ago, down 2.16% on the month before.

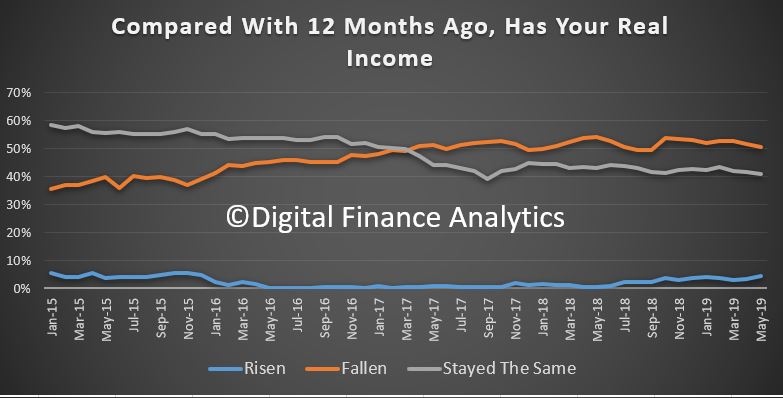

Income remains under pressure. Given the lack of real wages growth this should be of no surprise. 40% said they had seen no change in the past year, and 50.5% said, in real terms their income had fallen.

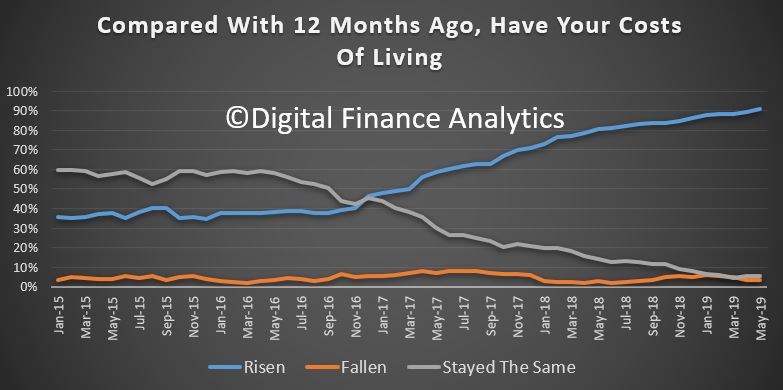

On the other hand, costs of living remain a challenge, with 91% saying costs have risen over the part year. Electricity, child care, health costs, rates, and food all registered, suggesting the CPI continues to understate the real experience of many households.

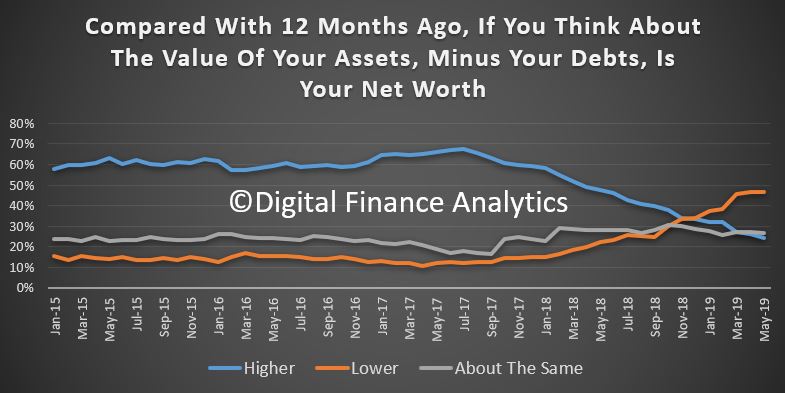

And finally, net wealth deteriorated for 46% of households compared with a year ago, thanks to falling property prices. 26% said there was no change and 24% higher ( down 1.63% on last month). Stock market performance helped to offset the property falls.

So the question becomes, will the slight tick-up in property related sentiment stick, or is the overall index set to fall further, as reality dawns – low income, rising costs, big mortgages, compressed returns on bank deposits, and weaker job prospects?

Put like that, the small falls in mortgage monthly repayments, and income uplifts for some may not be sufficient to support the index ahead. We will see.

Here is an extended discussion between Ex APRA/ASIC Executive Wilson N. Sy, Economist John Adams and Analyst Martin North. We look at how banking is regulated and who is really pulling the strings.