Drawing from his direct experience in the market, mortgage broker and financial adviser Chris Bates and I discuss the latest issues and look forward to what 2019 may bring.

Chris can be found at www.wealthful.com.au & www.theelephantintheroom.com.au plus via LinkedIn: https://www.linkedin.com/in/christopherbates

I discuss the recent reports on cracks appearing in an Olympic Park High Rise with Property Insider Edwin Almeida who has been sounding the alarm on this issue for some time.

What are the potential implications, and how wide should the investigations go? How worried should we be?

Caveat Emptor! Note: this is NOT financial or property advice!!

Could new innovators create a wave of disruption in the banking sector? APRA’s new rules provides an on-ramp and players are already appearing. The high penetration of mobile devices offers potential, perhaps. This from Investor Daily.

On Tuesday (18 December), the prudential regulator announced that

Xinja Bank Limited has been officially authorised as a restricted

deposit-taking institution (RADI).

Xinja is only the second Australian neobank to receive this status.

Volt Bank was granted a RADI in May, literally days after APRA finalised

the framework, which was created in response to the government’s push

for greater innovation and new entrants to the banking industry.

However, as its name suggests, a restricted ADI licence has

significant limitations. A RADI is really a stepping stone on the

journey to acquiring a full banking licence. It allows neobanks like

Xinja and Volt to conduct limited banking capabilities for a maximum

period of two years while they develop their capabilities and resources.

It also gives them time to raise the significant levels of capital

required to meet APRA’s demands for a full banking licence.

RADI’s must hold a minimum $3 million in capital, or 20 per cent of

adjusted assets, and can only hold $2 million worth of customer

deposits. When you consider that Australia’s largest bank, CBA, holds

more than $150 billion in customer deposits, you get an idea of the

competitive dynamics at play here.

However, the royal commission has severely damaged the reputations of

the incumbent banks like CBA and customers are arguably more open to

alternative offerings. Neobanks like Volt and Xinja could be poised to

capture a decent share of the banking sector – provided they have their

ducks in a row.

Volt, led by former NAB and Barclays executive Steve Weston, is

arguably the frontrunner in the race to obtain the much-coveted full

banking licence. The speed at which Volt was able to secure a RADI is

worth noting. Investor Daily understands that the group has been working

tirelessly to secure a banking licence as soon as possible.

The word on the street is that Volt could be given full ADI status by

the end of the year after it brought in KPMG’s corporate finance team

to facilitate a capital raise of around $40 million.

Anyone looking to make a bet on whether or not a brand-new challenger

bank can succeed in a market as oligopolistic at Australia’s needs to

consider two things: how willing customers are to try them out and if

they have succeeded in other markets.

The customer demand is clearly there. The royal commission has

provided the perfect platform for neo-banks tell their story, which is

the antithesis of what we heard from the banks during the Hayne inquiry.

A quick look at Volt’s website shows the bank is tapping directly

into the complaints of Australian banking customers and addressing them

head-on.

“We’ll always give you honest recommendations to protect your money and your data,” the company promises.

“We’ll remove speed bumps and will use the best available tech to make things easy and simple.

“We’ll suggest ways to save you time and money, both when you borrow and when you spend.”

Where incumbents have been slammed for predatory lending tactics and

high credit card fees, neobanks are looking at ways to harness

technology to provide a disciplined approach to lending, saving,

spending and investing money. Responsibility is high on their agenda.

I’ve heard that one potential Volt Bank feature will allow customers to

set parameters that lock them out of their account for a 24-hour period

if they know they’ll be in a situation where spending could get out of

control, like a pub or casino.

Challenger banks have made significant inroads in the UK, which is

always a good market to follow for clues about what will happen in

Australia. Our British cousins were a few years ahead of us on mortgage

reform, macro prudential measures and the rise of the neobank.

Groups like Aldermore, Atom Bank, Metro Bank and Monzo have cropped

up since the GFC. Metro Bank launched in 2010, when the shocks of the

financial crisis were still being felt by many, and became the first new

‘high street’ bank to launch in Great Britain in over 100 years.

From a standing start less than a decade ago, the bank has grown

customer deposits to over £11.7 billion ($20.6 billion) and recorded

£16.4 billion ($28.8 billion) in asset in FY17.

While Metro Bank competes directly with the UK’s high street

incumbents like HSBC and Santander, Australia’s neo-banks will offer a

completely digital service.

With more and more Australians using their smartphone for everyday

banking, a simplified customer-friendly approach to financial services

could be the winning ticket for groups like Volt and Xinja. Particularly

as the majors face the challenging task of transforming from large,

slow-moving machines to nimble, more efficient operators.

In another in our series talking with those in the front line of finance and property, I caught up again with Tony Locantro from Alto Capital in Perth for his take on next year, the property markets and his experience in getting a mortgage. Tony is also active on Twitter.

The Australian Prudential Regulation Authority’s (APRA) macro-prudential easing on interest-only residential mortgages is unlikely to meaningfully affect loan growth, as tighter underwriting standards have become the most effective constraint on riskier types of lending, says Fitch Ratings.

The restriction that interest-only loans cannot exceed 30% of new mortgages, which APRA will remove from 1 January 2019 for most banks, was put in place in March 2017 as part of the regulator’s efforts to contain banking-sector risk amid rising house prices and high and increasing household debt. The cap initially had a strong impact, but banks have collectively been operating well below the limit over the previous year due to stronger underwriting standards. This partly reflects the regulatory focus on risk control and mortgage underwriting – with APRA strengthening serviceability testing, for example – while banks have also become more cautious as market conditions have toughened.

The benchmark will be removed for banks that have provided assurances on

maintaining the strength of their underwriting standards, which was

also a requirement for the removal of a cap on investor loan growth in

April 2018. Most banks have provided these assurances.

Some

banks could take advantage of the cap removal to gain market share in a

slow credit-growth environment, but we expect no more than a small

uptick in overall interest-only lending. Lending standards should

continue to curb the pace at which interest-only loans are made

available by banks. The weak housing market, especially in Sydney and

Melbourne, is also a headwind to interest-only lending, as it will

dampen investor demand and speculative buying. We forecast nationwide

house prices to drop by 5% yoy in 2019.

Fitch expects Australian

banks to continue tightening control frameworks and underwriting

standards, especially around expense testing and income verification,

which should support the quality of new mortgages. APRA plans to review

banks’ risk controls and interest-only lending as part of a broader

assessment of lending standards next year.

The interest-only

lending cap is the last macro-prudential measure outstanding. Fitch

maintains a negative outlook on Australia’s banking sector, as bank

returns are likely to fall further in the near term on slowing mortgage

credit growth – especially in the residential mortgage segment – further

remediation and compliance costs associated with inquiries into the

financial sector, higher wholesale funding costs and rising

loan-impairment charges.

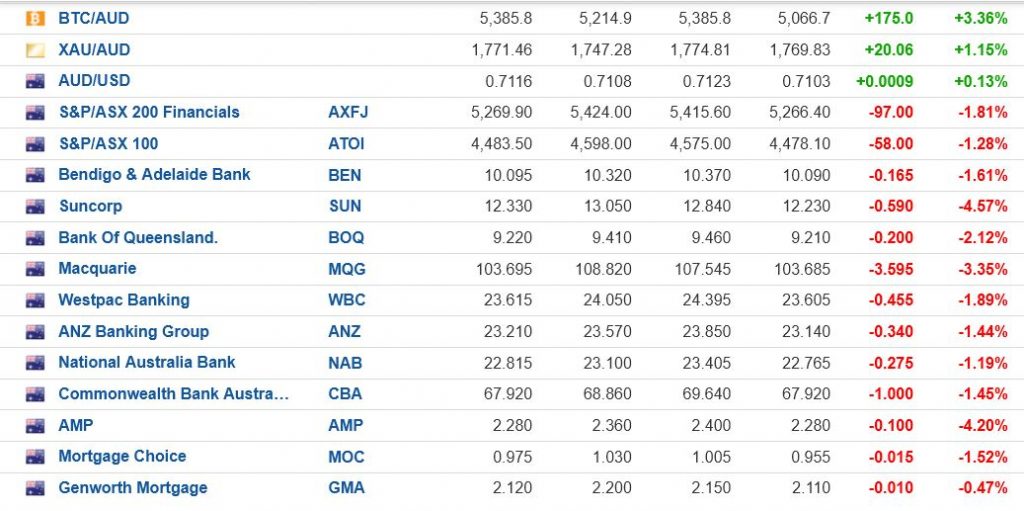

The US markets fell on Thursday, and the local market is following, with Financial Stocks under pressure. Here is the view at 1:00 PM. Macquarie is 3.36% lower, AMP down 4.2%, Mortgage Choice down 1.62% and Westpac down 1.89%. These moves are taking the financial sector firmly into negative territory.

The Financials index is down 1.81% at the moment, having started the day in positive territory.

Here is our summary of the US market action, recorded earlier today.

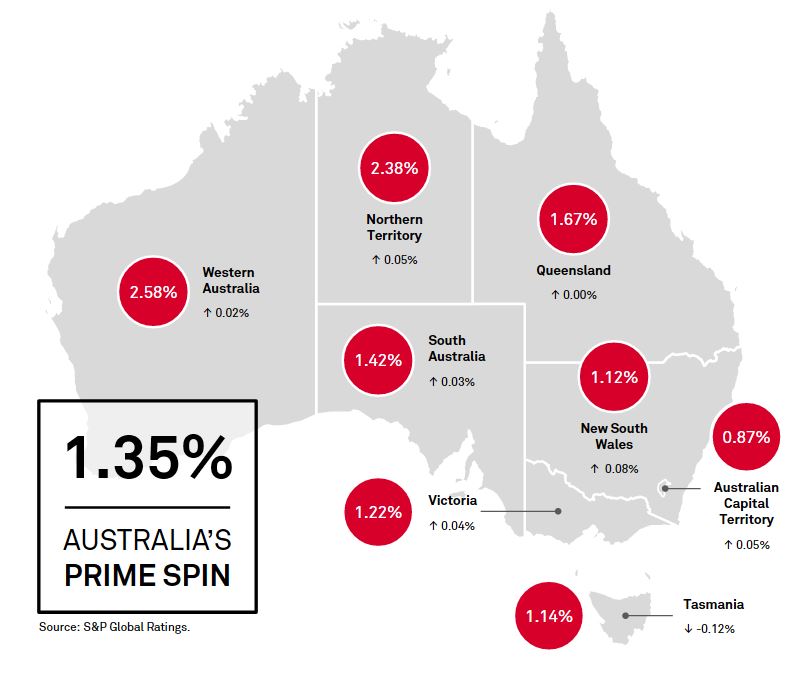

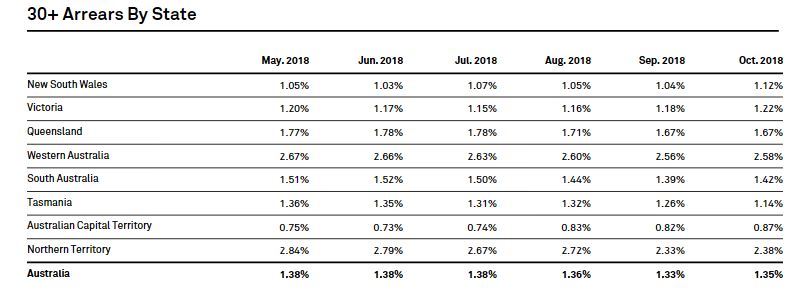

According to data from S&P Global Ratings relating to mortgage backed securities, the arrears rate rose in October 2018 (which is against normal trend).

Total SPIN index rose to 1.35%. The trend was consistent in all states and territories except Tasmania, where arrears fell to 1.14% in October from 1.26% the previous month. New South Wales recorded the largest increase in arrears in October, rising to 1.12% from 1.04% a month earlier. Arrears in New South Wales have been gradually rising throughout 2018, but remain the second lowest in the country, behind Australian Capital Territory.

WA stands out as the highest risk state, no surprise given the flat economy and many years of sliding home prices.

Investor and owner-occupier arrears increased in October. Investor

arrears increased to 1.25% in October from 1.19% in September and

owner-occupier arrears rose to 1.54% from 1.52% a month earlier. In our

opinion, the larger increase in investor arrears during the month partly

reflects the repricing of investor loans and interest-only loans, which

are more common among investors. This is also reflected in the

narrowing of the differential between investor and owner-occupier

arrears, which peaked at 0.61% in January 2017. The differential had

decreased to around 0.30% by October 2018, thanks to the ongoing

repricing of investor loans.

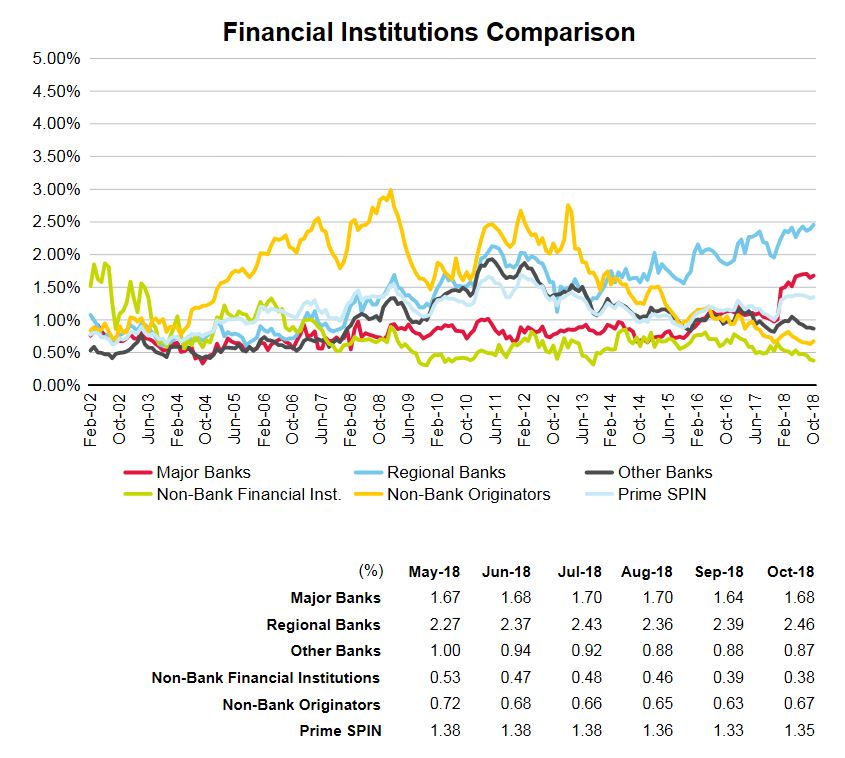

Arrears rose at the major and regional banks, offset by a small fall in the non-bank financial institutions. Defaults with non-bank originators rose.