AFG Mortgage Index figures released today show the country’s lending in a holding pattern with first home buyers the only category of buyer to record an increase for the first quarter of the 2019 financial year. Of course the AFG data only shows their own channels, but its a good indicator nevertheless.

The volume of mortgages processed by AFG declined 2% on the prior quarter. AFG brokers lodged 27,900 mortgages during Q1 19, totalling $14.2 billion, compared with 28,883 mortgages and $14.5 billion in the final quarter of the 2018 financial year.

AFG CEO David Bailey explained the results: “As the Financial Services Royal Commission continues to rattle the market Australian homebuyers are feeling the pinch as lenders tighten their borrowing criteria. Compared to the same quarter last year, lending volumes are down by just under 5% – a sure sign of a tightening market. The availability of credit has impacted investors most of all, with that category dropping by 1% to 27% of loans processed.

Refinancers were steady at 23% and Upgraders were also static at 43%.

New South Wales and Victoria are both down on the prior quarter, 2.5% and 6% respectively. Queensland also recorded a drop across the quarter, down 2%. Gains were recorded in SA – 2% up on last quarter, NT – up 22% and WA with an increase of 6% for the quarter.

Loan to Value Ratios (LVR) have increased in SA, NSW and WA.

The national average loan size has increased to a record $509,736, led by increases in average loan sizes in NSW, SA and Victoria.

“NSW has recorded an increase in average loan size of 3%, which we suspect is the result of a drop in apartment sales and lenders tightening criteria to investors – which are usually a lower average loan size. Both factors are driving up the average overall loan size in that state.

During the quarter many lenders moved to increase interest rates independent of the RBA, causing many borrowers to rethink their arrangements. “With the recent round of rate rises flowing through, many consumers have been speaking with their brokers to discuss the value of fixing all or part of their loans,” he said.

“Fixed rates have risen to 18.9% of loans by product category, whilst standard variable loans dropped to 64.3%. Basic variable products are also back in favour, increasing to 11.2% of all loans.

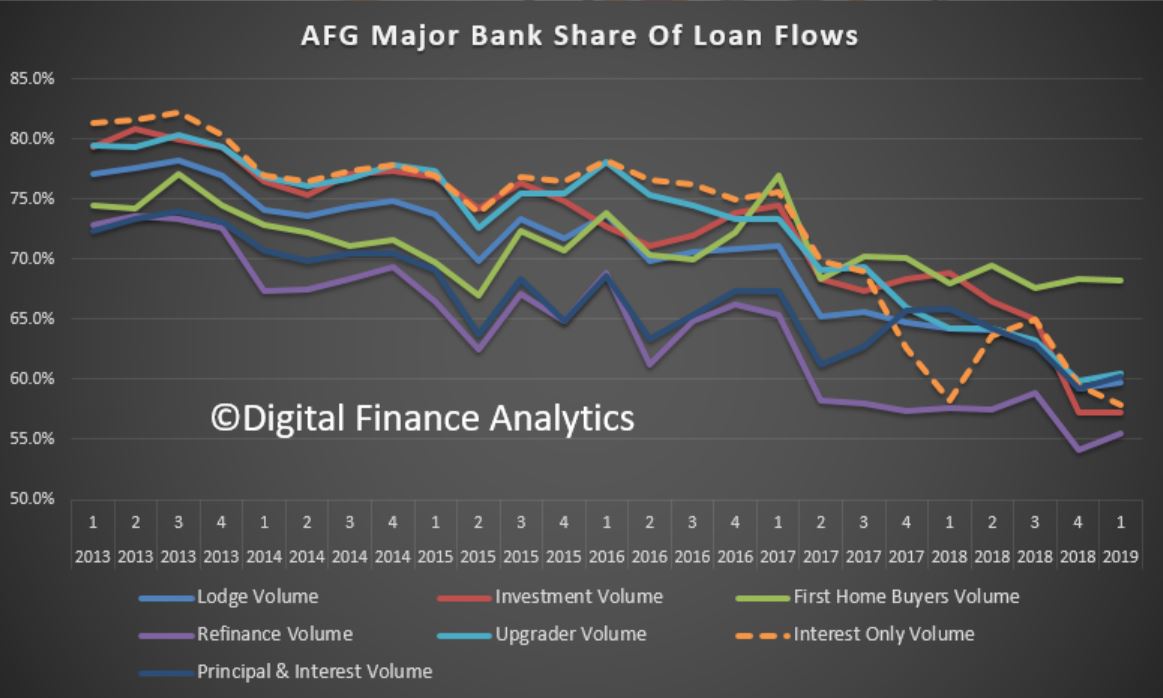

The major lenders clawed back some market share during the first quarter of the new financial year to now be sitting at 59.8%. This figure is still well below the high 70’s they had back in 2013, and much lower than they record outside of the third-party channel.

“The major lenders took some share from the non-majors after treading cautiously for the prior two quarters. The non-majors are still sitting at near historical highs with 40.2% market share after peaking at 40.8% last quarter.

“This is further evidence of the value brokers deliver to competition in the Australian lending market. Refinancers (55.5%) and Upgraders (60.5%) are favouring the competitive offers available from the non-major lenders.

Economist John Adams and I discuss the $250,000 limited bank deposit guarantee which applies to Australian banks under the Financial Claims Scheme. It is more complex than it looks!

The US market fell last night with tech stocks hit very hard, and the negative sentiment haunted our markets today. The NASDAQ fell 4.43% to 7,108, and has now moved more than 10% off its highs – so officially a correction.

The fear index was up to its recent highs again, at 25.23

And the Dow Jones fell 2.41% to 24,583. Actually most of the news was old news, with the expectations of a higher US interest rate and fall out from the Trade wars. But sentiment went negative again.

So no surprise the local market was hard hit in choppy trading today. The banks felt the pain. For example, Bendigo and Adelaide Bank fell 2.57% to 9.85,

Suncorp dropped 1.95% to 13.61

and Bank of Queensland dropped 5.32% to 9.43.

Falls were seen across the sector, with CBA down 1.97% to 65.54.

National Australia Bank down 2.21% to 24.61

ANZ down 2.24% to 24.88

And Westpac down 2.06% to 25.96.

Macquarie, with its international exposure fell 2.84% to 110.46

And the ASX Financials fell 3.02% to 5,534.

The Aussie ended at 70.74 against the US dollar, at the low end of the range and

The ASX 100 ended down 2.82% at 4,661.

The local fear index was up again to recent highs

But AMP was hit hard, thanks to their announcement today of further divestments. Timing is everything! “AMP announced the successful completion of its portfolio review including an agreement to divest its Australian and New Zealand wealth protection and mature businesses (AMP Life) and reinsure New Zealand retail wealth protection for total proceeds of A$3.45 billion”.

Tomorrow will be another day, will prices bounce or fall further?

Westpac Group has announced that it will introduce new changes to the way brokers are remunerated as part of a move to “enhance transparency and customer outcomes”, via The Adviser.

Effective 1 January 2019, Westpac and its subsidiaries, St.George, Bank of Melbourne, and BankSA, will link upfront commission payments for standard home loans to net debt utilisation and inclusive of loan offset arrangements, rather than the approved loan limit.

The group noted that the amount of upfront commission paid for most home loans will now be calculated as a percentage of the amount drawn down and used by the customer at settlement, excluding any amount which remains in an offset account.

Westpac general manager, home ownership, Will Ranken, said: “We know many of our customers value the independent service and advice mortgage brokers provide.

“Westpac Group continues to be an active participant in the Combined Industry Forum and supportive of its work to ensure better customer outcomes.

“We believe the changes we are introducing will be the start of delivering a more transparent commission model that better meets the needs of consumers and industry.

“We remain committed to supporting mortgage brokers to ensure we are providing the right home loan solutions for our customers.”

Westpac also stated that the new commission structure for standard home loans will also allow for a subsequent upfront commission for when brokers arrange loans for customers with funds held in offset accounts for a short term future purpose like renovations.

The bank said that the changes will mean if a customer takes out a $400,000 home loan and purchases a property for $350,000 and puts $50,000 of that loan into an offset account, the broker will be paid an upfront commission based on the $350,000 amount. Westpac added that if the customer then draws down the $50,000 in the offset account in the twelve months following settlement, the broker will receive a subsequent upfront commission calculated on the $50,000.

In addition, Westpac Group noted that it will implement improvements to increase the transparency of customer disclosure of the commissions mortgage brokers receive, including providing details of how the commission paid to mortgage brokers will be calculated.

According to Westpac, the new changes will also provide brokers with access to priority service arrangements for their clients if they “consistently meet quality loan application measures”.

The group added that there will be no requirement for brokers to meet any dollar volume business threshold to access these new arrangements.

Westpac Group said that the measures are part of its commitment to implement reforms recommended by the Combined Industry Forum (CIF) to “ensure better consumer outcomes”, which it said includes preserving and promoting competition and consumer choice, and improving standards of conduct and culture in mortgage broking.

Westpac also stated that The changes to commission calculations do not apply to Construction Loans, Equity Access Loans or Portfolio Loans as the commissions for these products remain unchanged in-line with the Combined Industry Forum recommendations, and said that changes to the commission model and service model will take effect by 1 January 2019.

Changes to make commission payments more transparent to Westpac Group customers will start being made in February 2019.

Westpac’s move follows similar broker remuneration changes announced by NAB in September.

AMP Limited has announced the successful completion of its portfolio review including an agreement to divest its Australian and New Zealand wealth protection and mature businesses (AMP Life) and reinsure New Zealand retail wealth protection for total proceeds of A$3.45 billion.

The stock dropped (in a down day) to a new low.

AMP will exit its Australian and New Zealand wealth protection and mature businesses via a sale to Resolution Life1 for total cash and non-cash consideration of A$3.3 billion; transaction expected to complete in 2H 2019; subject to regulatory approvals.

Binding agreement with Swiss Re2 to reinsure New Zealand retail wealth protection, releasing additional capital of up to A$150 million to AMP prior to completion of sale; subject to regulatory approvals.

Intention to seek divestment of New Zealand wealth management and advice businesses via initial public offering (IPO) in 2019 subject to market conditions and regulatory approvals, unlocking further value.

Significant capital release will strengthen AMP’s balance sheet and provide strategic flexibility; all options for use of proceeds to be evaluated and update to be provided following transaction completion.

Wealth protection and mature – Resolution Life transaction summary

Under the terms of today’s agreement, AMP will sell its Australian and New Zealand wealth protection and mature businesses (AMP Life) to Resolution Life for a total consideration of A$3.3 billion, which comprises:

A$1.9 billion in cash.

A$300 million in AT1 preference shares in AMP Life (issued on transaction completion).

A$1.1 billion in non-cash consideration:

o Economic interest in future earnings from the mature business, equivalent to A$600 million; expected to provide steady ongoing earnings to AMP of approximately A$50 million after tax per annum, assuming an annual run-off at 5 per cent.

o A$515 million interest in Resolution Life, focused on the acquisition and management of in-force life insurance books globally.

AMP expects to monetise all non-cash consideration over time.

Together with the New Zealand reinsurance agreement, the total value equates to approximately 0.82x pro forma embedded value of the sold businesses at 30 June 2018, excluding franking credits.

Resolution Life assumes risk and profits of the wealth protection and mature businesses from 1 July 20183, subject to Australian wealth protection risk-sharing arrangements.

A new relationship Agreement has been established with Resolution Life and AMP Capital will continue to manage wealth protection and mature assets under management. AMP Capital will also join Resolution Life’s global panel of preferred asset managers.

The transaction is subject to regulatory approvals and other conditions precedent and is expected to complete in 2H 2019.

Partnering to ensure smooth transition for customers

Resolution Life is an international insurance and reinsurance group whose management has a 15-year track record in providing quality service to in-force insurance customers.

The transaction has been designed to ensure all existing terms and conditions will be retained. The teams supporting existing AMP customers will largely transfer on completion to maintain continuity of service.

AMP and Resolution Life will work closely together to ensure a smooth transition for customers.

New Zealand wealth protection reinsurance

AMP has entered into a binding reinsurance agreement with Swiss Re for the New Zealand retail wealth protection portfolio which is expected to release up to A$150 million of capital to AMP, subject to regulatory approval. The agreement is expected to be effective from 31 December 2018, and will cover approximately 65 per cent of the New Zealand retail wealth protection portfolio for new claims incurred from that date.

The reinsurance agreement is expected to reduce New Zealand profit margins by A$20 million on a full-year basis. The reinsurance outcomes are factored into the Resolution Life transaction.

New Zealand wealth management and advice businesses

AMP is today also announcing its intention to seek divestment of its New Zealand wealth management and advice businesses via an IPO in 2019. The decision to proceed with an IPO and its timing remain subject to market conditions and regulatory approvals.

These businesses have FY18 pro forma operating earnings of approximately A$40 million on a standalone basis. The IPO would release capital to AMP and create a standalone New Zealand wealth management and advice business.4

Portfolio review outcomes will release capital, simplify portfolio and create strategic flexibility

The completion of the portfolio review will strengthen AMP’s balance sheet and provide strategic flexibility. All options for use of proceeds will be considered including growth investments and/or capital management activity.

The exit from Australian and New Zealand wealth protection and mature will also significantly simplify AMP and its earnings profile, enabling it to focus on its higher growth businesses of Australian wealth management, AMP Capital and AMP Bank.

The simplification and separation costs related to the Resolution Life sale transaction are expected to be in the order of A$320 million post-tax.

Additional capital from the transaction with Resolution Life will facilitate a reduction in AMP’s corporate debt of up to A$800 million.

The financial impacts of the transaction on AMP post-separation are outlined in the investor presentation.

AMP will exclude the 2H 18 earnings from the discontinued businesses in determining the FY 18 dividend. AMP continues to target a total FY 18 dividend payout within, but towards the lower end of its dividend guidance range of between 70 – 90 per cent of underlying profit.

Further guidance on use of proceeds will be provided following the completion of the transaction in 2H 2019.

The global economic outlook remains solid. The US economy is especially robust and is expected to moderate over the projection horizon, as forecast in the Bank’s July Monetary Policy Report (MPR). The new US-Mexico-Canada Agreement (USMCA) will reduce trade policy uncertainty in North America, which has been an important curb on business confidence and investment. However, trade conflict, particularly between the United States and China, is weighing on global growth and commodity prices. Financial market volatility has resurfaced and some emerging markets are under stress but, overall, global financial conditions remain accommodative.

The Canadian economy continues to operate close to its potential and the composition of growth is more balanced. Despite some quarterly fluctuations, growth is expected to average about 2 per cent over the second half of 2018. Real GDP is projected to grow by 2.1 per cent this year and next before slowing to 1.9 per cent in 2020.

The projections for business investment and exports have been revised up, reflecting the USMCA and the recently-approved liquid natural gas project in British Columbia. Still, investment and exports will be dampened by the recent decline in commodity prices, as well as ongoing competitiveness challenges and limited transportation capacity. The Bank will be monitoring the extent to which the USMCA leads to more confidence and business investment in Canada.

Household spending is expected to continue growing at a healthy pace, underpinned by solid employment income growth. Households are adjusting their spending as expected in response to higher interest rates and housing market policies. In this context, household credit growth continues to moderate and housing activity across Canada is stabilizing. As a result, household vulnerabilities are edging lower in a number of respects, although they remain elevated.

CPI inflation dropped to 2.2 per cent in September, in large part because the summer spike in airfares was reversed. Other temporary factors pushing up inflation, such as past increases in gasoline prices and minimum wages, should fade in early 2019. Inflation is then expected to remain close to the 2 per cent target through the end of 2020. The Bank’s core measures of inflation all remain around 2 per cent, consistent with an economy that is operating at capacity. Wage growth remains moderate, although it is projected to pick up in the coming quarters, consistent with the Bank’s latest Business Outlook Survey.

Given all of these factors, Governing Council agrees that the policy interest rate will need to rise to a neutral stance to achieve the inflation target. In determining the appropriate pace of rate increases, Governing Council will continue to take into account how the economy is adjusting to higher interest rates, given the elevated level of household debt. In addition, we will pay close attention to global trade policy developments and their implications for the inflation outlook.

On Friday submission to the Royal Commission into Financial Service Misconduct relating the the draft report closes. You can still make a Public Submission – a quick and painless process, and it is a once in a generation chance to shape the future of finance in Australia.

This is what DFA did today, and here is a copy of what I said.

Summary

We welcome the findings from the draft report and recommend the following policy options.

The culture in the finance sector needs to change, to put the customer first. Mortgage brokers for example should have a best interest duty and commissions should be banned.

The current focus on “financial stability” is myopic, favouring large players, over small, and building structural risks into the system; the regulators have failed.

The large players are too big to fail and too complex to manage, and need to be broken apart. A modern Glass Steagall separation would achieve this, and is proven to reduce risk, and drive better customer outcomes and right size our finance sector.

The existing regulatory structure, operating in the Council of Financial Regulators needs to be changed, as its narrow focus on financial stability, and a massive “bet” on inflating the housing sector now at risk. None of the regulatory actors are without blame.

Introduction.

Digital Finance Analytics (DFA) is an Australian boutique research, consulting and advisory firm which combines primary consumer and small business research, analysis of both private and public datasets and economic modelling to analyse the dynamics of the finance and property sector. We have been operating since 2005.

Our analysis is based on a rolling 52,000 household survey, with more than 4,000 new data points added each month. From this we are able to assess the state of household finances, their future property transaction intentions, and their level of debt; and ability to service it.

Households Are Overextended

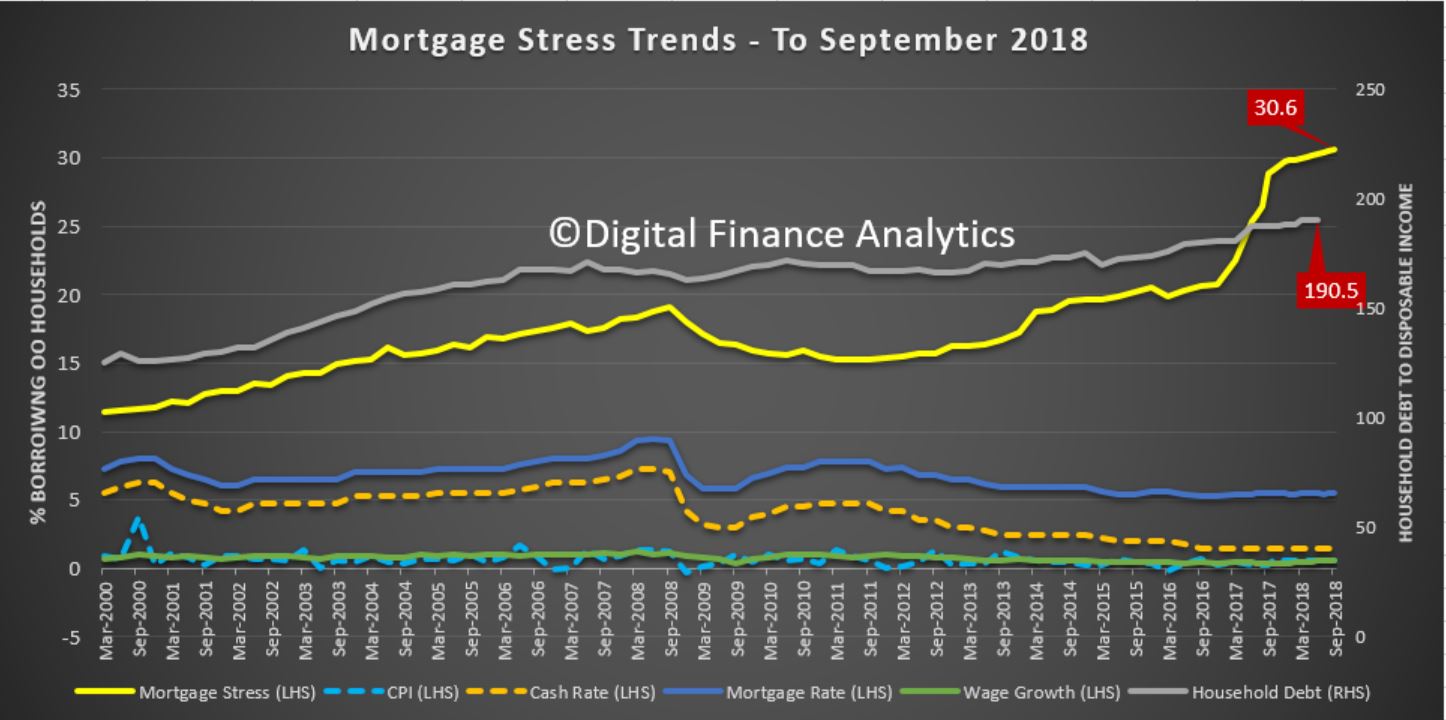

We have observed a considerable expansion of household debt in recent years, driven by low interest rates, more generous lending standards, and some degree of “not suitable” lending and fraud. The RBA reports that the household debt to income ratio is now around 190 and the debt to GDP ratio is one of the highest in the world.

As a result, more households are in financial stress, as tracked in our mortgage stress trends (defined in cash flow terms, not a set percentage), and last month more than one million households with owner occupied mortgages were in difficulty, despite the ultra-low interest rates. This equates to 30.6% of all borrowing households.

This has been exacerbated by flat incomes, and rising costs, but poor lending practice is the underlying cause. We also believe that as interest rates rise, and property prices fall further, the financial state of households will decline further. This is because many are enjoying the “wealth effect” of property gains in recent years, but this is only a paper gain, and now prices are falling. The expectation is prices will fall further and faster.

The Cause of Property Price Falls

Following many years of over-free lending, the regulators have now intervened to an extent and as a result lending standards are tightening, with up to a 40% fall in borrowing power for many compared with a year ago. In the main though this is a result of the existing regulations now being applied as originally intended, rather than new laws, as incomes and expenses are being tested, as opposed to using a formula based on HEM (Household Expenditure Measures).

This resetting of lending standards marks a significant change in the market, and as a result according to our surveys, demand for property is easing, at the time when foreign buyers are receding, and property investors are getting twitchy. According to Bank of England research, property investors are significantly more likely to exit the market in a down turn compared with owner occupied borrowers.

Property investors, who have driven the market higher in recent years are choosing to exit, sometimes forced by the switch from interest only loans to principal and interest loans (estimated at around ~$120 billion per annum), of the $1.7 trillion total mortgage lending pools.

Our modelling shows that it is credit availability which pumped up property prices (and which allowed the Banks and other Lenders to growth their balance sheets, and profits) and the reverse is also true. The normalising of lending standards will rightly reduce credit, thus driving home prices and banks profitability lower. The catch here is that for more than a decade, Australia’s economic performance has been built on the back of ever greater mortgage and consumer debt, home price growth, and construction. Thus from a policy perspective Government, and the RBA will defend high levels of credit and home prices, despite the risks.

The other factor to consider is that as banks were so reliant on home lending to drive profitability, the incentives were there to over lend, bend the rules, and reward poor behaviour. They have not followed regulatory guidelines nor have they met community expectations. In a word, GREED, as your draft report shows.

The Policy Challenge

Our view is that whilst the restatement of the current lending standards will assist, there are more significant structural questions to be considered. Regulation and changes to the law alone cannot address the issues you call out.

The culture within the finance sector needs to be changed, to put customers at the centre of their business. Whilst talk is cheap however, there is little evidence of substantial change as yet. The removal of commissions should be a corner stone, as conflicted remuneration remains a significant problem. Mortgage brokers, for example, should have a responsibility to act in the best interest of their customers. The industry will resist this, but it is essential.

Currently, the capital adequacy rules favour mortgage lending relative to productive lending to business and as a result according to our Small and Medium Enterprise surveys, many businesses are unable to obtain finance (or can only do so by securing their property). We believe the various risk weights reflect a myopic view of the financial system and they need to be changed. Too much of the bank’s portfolio of loans – up to 65% – is against residential property – this is extraordinarily high by international standards, and presents a significant risk, to say nothing of the lack of business investment which has resulted.

However, we hold the view that the major financial sector players are too complex to be managed effectively, scale is now a disadvantage. Thus we believe there is a case to break up the banks into smaller units. This would involve both vertical disaggregation (separation of advice, sales and product manufacture) and horizontal disaggregation (separate of wealth, insurance, retail banking and investment banking). In addition, there are significant risks from their operations in derivatives, and in an integrated environment, costs, risks and profits are cross linked. Given the size of the derivatives sector (significantly larger than before the GFC), the systemic risks are significant. To counter this, we advocate the implementation of a modern Glass Steagall separation, where the high-risk speculative activities are separated from the normal lending, payment and deposit functions within banking. This would have the added benefit of reducing the potential risks of a bank deposit bail-in in a time of crisis. Evidence suggests that the existence of a modern Glass Steagall separation would reduce risk and limit systemic risk. In a post Glass Steagall world, bank lending would be more aligned with the deposits available, so their ability to make loans “from thin air” as in the current system would be curtailed. They would also be more inclined to make loans for truly productive purposes.

We also need to consider the role of the regulators and the RBA. Murray’s Financial System Inquiry recommended that the effectiveness of the current regulatory system be monitored. The Council of Financial Regulators is the peak body, chaired by the RBA, where key policy is set, with the Treasury, ASIC, APRA and others. However, none of their deliberations are made public, and it appears that all entities have been sharing the same view that growing housing credit was the chosen growth lever of choice following the mining boom. It appears that the weak supervisory approach from ASIC and APRA stemmed from this policy, and was supported by policy rates being set too low. As a result, the systemic risks have been underestimated, and the economic platform for the country narrowed.

We believe that there should be a stronger advocate for the consumer within the regulatory system, perhaps the ACCC should take this role. But more broadly the role of individual regulators and how they connect needs clarity. The Royal Commission highlighted the lack of coherence, and alignment. We also would argue (perhaps beyond the scope the current inquiry) that APRA has myopically focussed on financial stability, at the cost of good consumer outcomes and competition, that the regulations favour large players over small players, that the RBA policy rates are too low, and the ASIC so far is still perceived as a weak and ineffective regulator. Thus the area of appropriate and effective regulation is critical.

Professor Samuel has told the COBA 2018 Convention in Melbourne today that the customer owned banking sector is “in a pretty good place.”

“The major banks have a major repair job ahead of them to restore trust in their approach to their customers,” Professor Samuel said.

“They all are now loudly proclaiming that they have been remiss in not putting their customers first. They are all promising to do so henceforth. But will they walk the walk? Will their institutional shareholders permit them to deviate from their perception of their primary remit – to increase the wealth of shareholders? How long will the shocking revelations of the Royal Commission remain at the forefront of their strategies for governance and cultural change?

“The customer owned banking sector has different drivers – and thus a different foundation on which to base their culture. And if they take advantage of the opprobrium currently attached to the major banks, and structure their conduct around the ‘should we do it’ culture, they have a lot to gain from current events.

“For they have the flexibility and motivation to not just talk about placing the customer first, but to actually walk the walk,” Professor Samuel said.

COBA CEO Michael Lawrence welcomed Professor Samuel’s comments.

“We strongly support Professor Samuel’s observation that it is the power of competition that will ultimately be the most powerful tool to bring about the changes in culture that the Hayne Commission is clearly demonstrating as an urgent priority,” Lawrence said.

The customer owned banking sector has four million customers and total assets of $113 billion.

The Reserve Bank of Australia has echoed Westpac’s warning that the impact of the royal commission could see further reductions in the availability of credit, sparking broader fears for the economy.

But of course they were the architect of the credit boom, with too low interest rates and inappropriate monetary settings. Rich then they now flick the blame to the Commission, which is simply underscoring the need to get back to a more normal regime….

In the minutes of its October meeting on monetary policy, the Reserve Bank notes that members discussed the release of the interim report of the Royal Commission into Misconduct in the Banking, Superannuation and Financial Services Industry.

“The report contains many questions covering a broad range of issues, but at this stage provides relatively little indication of the recommendations that are likely to be made in the final report,” the minutes said

“Members observed that while the regulators had already overseen a tightening of lending standards, and a degree of tightening of lending standards had been implemented by banks in anticipation of the commission’s findings, it was possible that banks could tighten lending conditions further given the issues raised in the report.

“Members noted that it would be important to monitor the future supply of credit to ensure that economic activity continued to be appropriately supported.”

The RBA’s comments come after Westpac chief executive Brian Hartzer used his opening statement at a parliamentary inquiry this month to warn against further regulation of lenders in response to the Hayne royal commission.

Appearing before the House of Representatives standing committee on economics, Westpac CEO Brian Hartzer urged legislators to consider the “second-order effects” of further regulation that may be introduced to reduce misconduct off the back of the commission.

“New regulations and tougher sanctions alone are not going to solve the risk of poor conduct,” Mr Hartzer said.

Mr Hartzer expressed support for an observation noted by commissioner Kenneth Hayne in his interim report, which suggested that simplifying regulation could reduce poor consumer outcomes.

The major bank CEO warned that further regulation could exacerbate the slowdown in credit and housing market conditions and impede economic growth.

“[In] striving to address the issues that have led to misconduct, it’s important that policymakers remain live to the potential second-order effects of new legislation and regulation,” the CEO continued.

“While overall economic growth remains sound, we are seeing increasing uncertainty, especially among the consumer and small business sectors.

“House prices are falling, income growth has been low, and consumer spending is likely to be affected by people’s confidence in the value of their home.

“Therefore, regulatory changes that impact how much individuals can borrow, the cost and availability of credit for business, or the availability and affordability of suitable financial advice, should be considered carefully.”