Abolishing trailing commissions for mortgage brokers would reduce competition, drive up home loan rates and make banks the “unintended beneficiaries”, the Australian Finance Group has warned.

Speaking after the release of the Productivity Commission’s final report on competition in the Australian financial system, which recommended that the government remove trail commissions, the aggregator warned that such a move could be counterproductive and potentially lead to reduced competition in the financial system.

AFG CEO David Bailey cautioned that any move to ban trailing commissions for mortgage brokers would have the impact of consolidating the lending base of the banks, stating: “This is ironic given the tone of the majority of the final report. Consumers have been voting with their feet in greater numbers for over 20 years and increasingly use brokers for better service and less costly, better-suited home loans.

“Mortgage brokers are encouraged through trailing commission to stay with customers for the life of their loan, to review products and add value. It is in the business interest of brokers to work for their clients through the years to help them continue to gain better finance outcomes as circumstances change.

“Banning the incentive to work with customers for longer durations would have a detrimental impact on the very services that brokers help provide — greater competition.”

“Since the ASIC broker remuneration review, our industry has come together to address the recommendations from the data-driven ASIC report.

“Excellent progress has been made and a good consumer outcome has been defined. All members of the Combined Industry Forum are actively engaged in addressing the proposals raised by the regulator.

“In light of this progress, momentum-based decisions which ignore the full ramifications of such a move need to be carefully considered.”

The head of AFG went on to say that brokers are filling vital roles in areas that the banks had vacated, and particularly help vulnerable customers, first home buyers and those with complex borrowing needs.

“Providing assistance in these areas takes a lot of time — time that the bigger lenders are often not prepared to give.”

Mr Bailey highlighted that AFG had provided the Productivity Commission with evidence of the savings brokers make for their customers through ongoing contact over the life of a loan, stating that it was “disappointing” the commission “did not give sufficient weight to this evidence”.

“We invite them again to spend time with some AFG brokers to understand the value a demonstrated level of contact with a customer can deliver,” Mr Bailey said.

He concluded: “The last thing Australian consumers deserve is higher prices for lending products and less competition where banks can drive up costs for existing customers.

“We can’t afford to jettison 20 years of competitive experience without giving regard to the findings of other reviews and ensuring a stable, dynamic, customer-focused lending environment remains.”

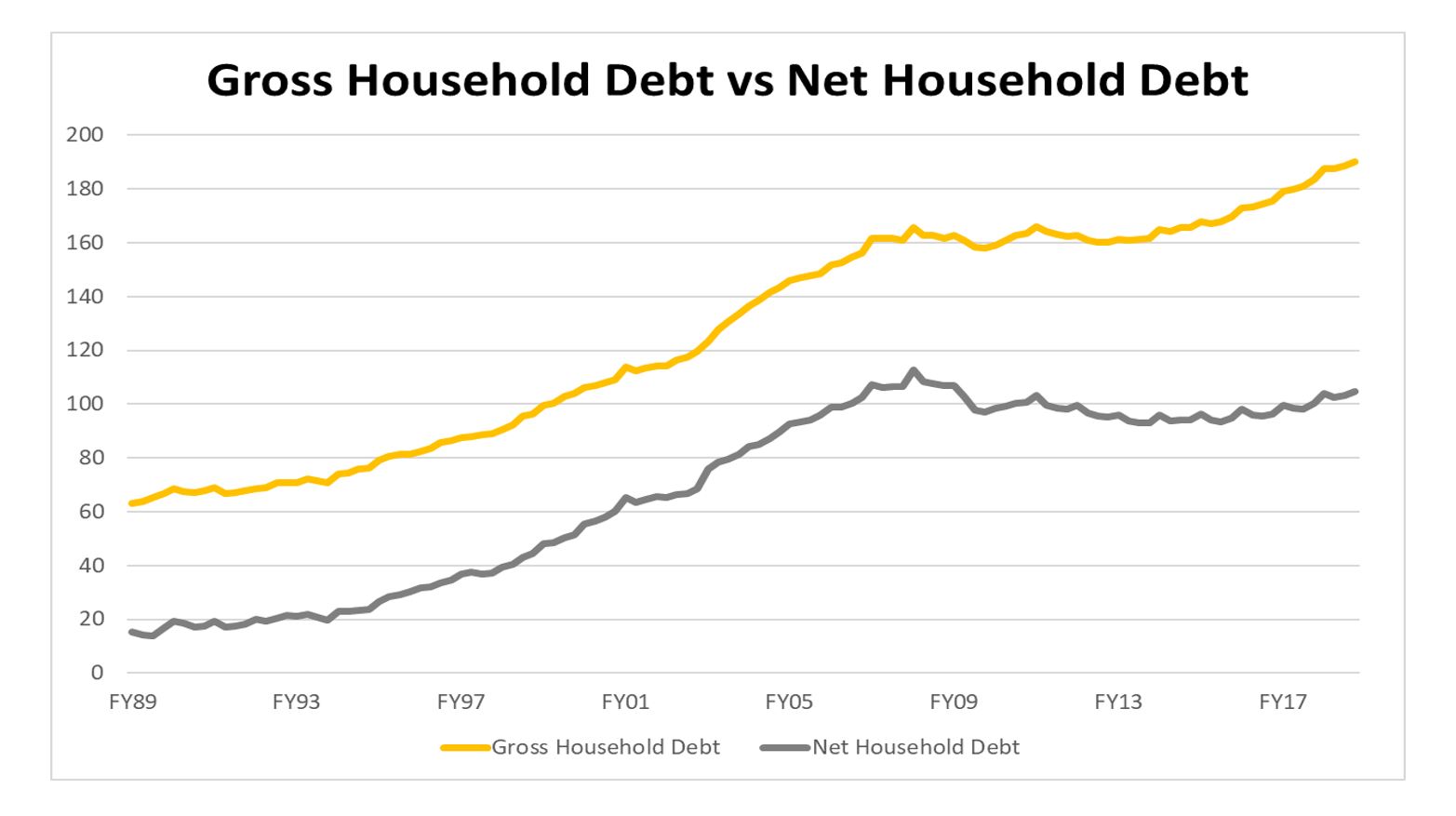

In the latest edition, John Adams, the Economist, and I discuss the recent data on household debt, and look at some commentators view that the current accepted high debt is not a problem at all. Fake news or fact?Watch the video, or read John’s original article.

Welcome to the Property Imperative weekly to 4th August 2018, our digest of the latest finance and property news with a distinctively Australian flavour.

By the way if you value the content we produce please do consider joining our Patreon programme, where you can support our ability to continue to make great content.

Watch the video, listen to the podcast, or read the transcript.

A big week of news to cover, so let’s get straight in at the deep end with the Productivity Commission report on Competition in Financial Services which was released on Friday. The final report, which was released earlier than expected really highlights the never-mind-the customer attitude of the industry and its regulators. They call out regulatory failure and conflicts of interest across the sector, referring to opaque pricing, unsuitable products, no reward for customer loyalty as well as product complexity and faux competition. Major players have too much market power, and have fingers in multiple segments of the market. Customers lose out as a result. They made a wide range of recommendations, including the introduction of a best interest obligation for all providers in the home loans market, mortgage Brokers trail commissions should be phased out, ASIC to ensure that the interests of borrowers are adequately safeguarded in the LMI market, APRA is singled out for myopic regulation. ACCC should focus on encouraging competition across the industry and safeguarding the interests of consumers in the regulatory system, the new payments system needs a proper access regime and the Payments System Board of the RBA should ban all card interchange fees. We discussed the implications in our recent video, and the link to that is above. In summary a number of critical reforms which if implemented could certainly change the landscape for financial customers in Australia for the better, whilst clipping the wings of the major incumbents. We discussed this on ABC Radio. Good Job, Productivity Commission. Let’s now see if the Government is up to the challenge.

There was a bit of good news on the retail front, with turnover for June, the month of the end of year sales, where deep discounting was the hallmark. The ABS says retail turnover rose 0.4 per cent seasonally adjusted, which follows a 0.4 per cent rise in May. The trend estimate, which I prefer, reported a 0.3 per cent in June following a rise of 0.4 per cent in May 2018. Compared to June 2017, the trend estimate rose 3.1 per cent. In trend terms, clothing and footwear rose 0.7%, department stores rose 0.5% and household goods 0.3%. Across the states, New South Wales and Victoria rose 0.5%, ACT 0.8% and Tasmania 0.9%. Queensland was flat and WA rose just 0.1%, so again the variations are significant. Online retail turnover contributed 5.7 per cent of total retail turnover in original terms in June 2018, a rise from 5.6 per cent in May 2018. In June 2017 online retail turnover contributed 4.1 per cent to total retail.

This means households are spending more than their income growth, by continuing to tap into their savings. So it will be interesting to see if the retail momentum continues, or sags in July after the end of season sales.

Continuing the “cat among the pigeons” theme, ANZ parted company from its competitors by cutting its variable home loan rate for new customers. While banks including the CBA have cut fixed loan rates and offered “honeymoon deals” in recent weeks, the ANZ is the first to move on variable rates. The ANZ told mortgage brokers it was bringing down its basic principal and interest home rate for owner-occupiers by 0.34 percentage points to 3.65 per cent. The ANZ offer only applies to new customers looking for a loan valued at 80 per cent or less than the value of their property. Loan-to-value ratios above 80 per cent remain unchanged at 3.99 per cent. As we discussed in our separate post “ANZ Ups The Ante In The Mortgage Wars” – the industry is homing in on lower risk customers in an attempt to maintain loan book growth. We also discussed this significant event on 2GB’s Money Show with Ross Greenwood. As Ross said, picture the lions around a shrinking watering hole trying to protect their territory!

Also this week ASIC released their review of exchange traded products (ETP’s) in Australia. These are open-ended investment products that are traded on a securities exchange market. ETPs trade and settle like shares and give investors exposure to underlying assets without owning those assets directly. They differ from listed funds because they are open-ended. This means that the number of units on issue may increase or decrease daily depending on investor demand. ETPs, especially exchange traded funds (ETFs), are increasingly popular with retail investors and self-managed superannuation funds (SMSFs). This is because of their accessibility, perceived low cost, transparency, intraday liquidity, diversification benefits and ability to provide exposure to new asset classes. There has been steady growth in both funds under management and the number of ETP products available on the market in Australia. ASIC called out a number of concerns, including the question of spreads and liquidity, the concentration of market makers, and the lack of good disclosure. More of the same-ol’ same -ol’. Potential investors should be wary.

Data from the Household, Income and Labour Dynamics in AustraliaHILDA survey came out this week and showed again the rise in the proportion of the household population who is renting, with the number of Australian renters eventually becoming homeowners plummeting over the last 15 years – particularly for those between the ages of 18 and 24. The survey found the overall proportion of people living in rental accommodation has increased by 23 per cent since 2001 to 31.3 per cent in 2016. They called out “The growing evidence of ‘intergenerational inequality’”. The data also chimes with our surveys, that more households are under financial pressure thanks to flat incomes and rising costs. It’s worth highlighting their data only runs to 2016, so it’s already a couple of years old. We think the trends continue to grow, based on our latest Mortgage Stress data which will be out next week.

And another survey from mortgage lender State Custodians found that as many as 15% of surveyed homeowners have faced challenges when trying to refinance, due to falling property prices. The figures published by State Custodians also revealed that young people were the most affected, with around 34% of those under the age of 34 saying they’ve been unsuccessful in re-financing because of declining property values. This highlights the rise of “mortgage prisoner’s” who cannot refinance to get the better deals because of little or no equity, or other financial pressures.

And talking of households in financial pressure, the number of Australians falling behind on their mortgages will rise in the next two years as interest-only loans end and repayments get more expensive, ratings agency Moody’s warned this week. Delinquencies on loans that have converted from interest-only to principal and interest are running at double the rate of those still on interest-only, they said. About 40 per cent of loans by Australian banks in 2014 and 2015 were interest-only for five years, meaning a large portion are set to come under pressure with higher repayments in 2019 and 2020, said Moody’s. This backs up our findings, which estimates that more than 970,000 Australian households are now believed to be suffering housing stress. We discussed this in our video Wither Interest Only Loans.

Genworth, the Lender’s Mortgage Insurer related their 1H18 results this week and their profit remains under pressure, as claim rates rise. The Delinquency Rate increased from 0.51% in 1H17 to 0.54% in 1H18, and they pointed and increase in the number of delinquencies in Western Australia, New South Wales and to a lesser extent South Australia. This was partially offset by a decrease in delinquencies in Victoria and Queensland. New delinquencies were down in the half (1H18: 5,565 versus 1H17: 5,997). Delinquencies in mining areas are showing signs of improving. In non-mining regions there are indications of a softening in cure rates.

Turning now to property, the home price slides continue, as we discussed in our post “Home Price Falls Are Just Starting (…more to come!). We discussed the importance of looking at the local, micro property markets as the averages mean nothing. For example, over the past year prices are down more than 20% in some suburbs, and not necessarily where you might expect.

And talking of videos, do check out the latest in our series of Adams/North discussions, “The Great Airbrush Scandal – Policy Failure of the Year!”, where we dissect APRA’s Bank Stress Tests and conclude they were not fit for purpose. This one has already generated a large number of comments and observations. John suggests our regulators are asleep at the wheel! You can also read his original article.

Corelogic says Auction volumes are lower across each individual capital city this week with 1,224 homes scheduled to go under the hammer, down from 1,536 last week. A further sign of weakness in the property sector. Melbourne is particular is slowing fast.

Last week the homes taken to auction across the combined capital cities, returning a final auction clearance rate of 55.6 per cent, down from 57.0 per cent across 1,257 auctions the previous week. Over the same week last year, 1,987 homes went to auction and a clearance rate of 68.7 per cent was recorded. Melbourne’s final clearance rate was recorded at 58.5 per cent across 802 auctions last week, compared to 59.9 per cent across 613 auctions over the previous week. This time last year 956 homes were taken to auction across the city and a much stronger clearance rate was recorded (75.6 per cent). Sydney’s final auction clearance rate came in at 52.4 per cent across 469 auctions last week, down from 55.2 per cent across 407 auctions over the previous week. Over the same week last year, 714 homes went to auction returning a clearance rate of 65.4 per cent. Across the smaller auction markets, clearance rates improved across Canberra and Perth, while Brisbane and Adelaide saw clearance rates fall week-on-week. There were no auctions recorded in Tasmania last week. Of the non-capital city auction markets, the Hunter region was the best performing in terms of clearance rate, with 10 of the 14 reported auctions selling (71.4 per cent), followed by Geelong with a 65.0 per cent clearance rate across 20 results. The busiest region for auctions was the Gold Coast where 39 homes were taken to auction, returning a clearance rate of just 32.3 per cent.

Building approvals in June were slightly stronger in trend terms, rising by just 0.1% as reported by the ABS. The Mainstream media fixated on the stronger, but less reliable seasonally adjusted figures. Among the states and territories, dwelling approvals rose in June in the Australian Capital Territory (5.8 per cent), South Australia (5.6 per cent), Northern Territory (4.8 per cent), Tasmania (2.2 per cent), Western Australia (1.7 per cent) and New South Wales (0.2 per cent) in trend terms. Dwelling approvals fell in trend terms in Queensland (1.6 per cent) and Victoria (1.2 per cent). Overall momentum is slowing in our view, as demand for high-rise investment apartments ease.

And overall lending for housing is still tracking higher despite investor lending sliding, according to the latest RBA and APRA figures for June. Owner occupied housing lending rose 0.6% or $6.6 billion to $1.18 trillion, while investment lending fell $800 million, down 0.1% in seasonally adjusted terms, or rose $1 billion, up 0.2% in original terms. (I have no idea what adjustments the RBA makes, it’s not disclosed!). Investment lending fell to 33.5% of the portfolio. Total lending for housing is a new record $1.77 trillion, and remember this is at a time when housing debt to income is knocking on the 200 door, and we are one of the most in debt nations on the planet. Lest we forget, loans need to be repaid, eventually! We discussed both the credit data and the building approvals in our video “Another Housing Record Set”. We have not fundamentally addressed the credit elephant in the room. Despite all the noise. Perhaps the regulators would like to tell us, how much debt is too much? We clearly have not hit their pain threshold yet, despite the rising financial stress in many households.

So to the markets. Locally, the ASX100 finished down a little on Friday to 5,126, still significantly higher than earlier in the year. The banks were down, for example, CBA fell 1.15% on Friday, to end the week at 72.83, in reaction to the Productivity Commission report. Westpac fell 0.96% to end at 28.91. AMP also fell, down 0.85% on Friday, to 3.50, despite a broker’s report suggesting there may be long term value in the stock, after a restructure. The market was perhaps not convinced.

The Aussie was below 74 cents against the US dollar, despite a small rise on Friday, to 73.97, but higher, up 0.29% to 5.05 against the Chinese Yuan. It appears China is flexing its currency muscles in response to the US trade tariffs.

The Bank of England lifted their cash benchmark rate 0.25% to 0.75% as inflation is above the lower bounds target, despite the uncertainty surrounding Brexit (be it hard or soft). The Aussie was up 0.62% on Friday against to UK Pound to 0.56 cents in reaction to the news.

Across the pond in the US market, Apple took market attention for a host of reasons this week, including reaching a historic Wall Street milestone by becoming the first U.S. company to hit $1 trillion in market capitalization. Apple Inc stock hit the target number of $207.05 (based on the numbers of shares outstanding reported in its 10Q) just before noon on Thursday. Shares closed solidly above that Friday at 207.99. Shares moved into trillion-dollar territory following a strong earnings report earlier this week. On Tuesday, Apple’s fiscal third-quarter results beat on the top and bottom lines, driven by sales of the pricier iPhone X and subscription revenue to services such as Apple Music and its App Store. Apple also lifted the cloud that was hovering over the tech sector following weak reports from Facebook and Twitter. The NASDAQ ended the week at 7,812, a strong finish, but not a record, despite the Apple price. The S&P Information Technology sector index finished at 1,277.05 Friday, compared with 1,262.27 a week ago.

The July US employment report gave the market more evidence that the economy is humming along at a pace that won’t alarm the Federal Reserve. Although the rise in nonfarm payrolls was less than expected for July, jobs gains for the two previous months were revised up by 59,000, making the overall rise about in line with forecasts. And average hourly earnings showed wage inflation at the same year-on-year pace as before. That leaves the Fed set up to continue its plan of gradually rising rates. “The economy is growing really strongly and headline inflation set to hit 3% next week, so the case for September and December Fed rate hikes remains strong,” ING Chief International Economist James Knightley said.

Fed fund futures are still pricing in the next rate hike to be at the next September 25-26 meeting. Odds for an additional increase in December remained little changed after the release at around 65%.

The Fed had its say this week as well. The Federal Open Market Committee kept rates unchanged as expected, and also kept the language in its statement substantially the same. The FOMC said it continues to expect that further gradual increases in the target range for the federal funds rate will be consistent with “sustained expansion of economic activity, strong labor market conditions and inflation near the Committee’s symmetric 2% objective over the medium term.” That reaffirmed investor expectations that the central bank remained on track to hike rates twice more this year. “The stance of monetary policy remains accommodative, thereby supporting strong labor market conditions and a sustained return to 2 percent inflation,” the Fed said in its statement.

A report on Tuesday showed that the Fed’s preferred measure of inflation, the core personal consumption expenditures price index, which excludes food and energy prices, was up 0.1% and 1.9% on a year-over-year basis. The Fed targets inflation of 2%.

Oil settled lower for the day and week Friday, as concerns about a trade war stifling demand hurt sentiment. On the New York Mercantile Exchange crude futures for September delivery fell 47 cents to settle at $68.65 a barrel. Oilfield services firm Baker Hughes reported on Friday that the number of U.S. oil drilling rigs in operation fell by 2 to 861, pointing to tightening U.S. output. And the weekly oil inventories numbers showed an unexpected rise in U.S. stockpiles, further weighing on prices. Concerns also remained about escalating output from the OPEC and Russia. On June 22-23, OPEC, Russia and other non-members agreed to return to 100% compliance with oil output cuts that began in January 2017, after months of underproduction elsewhere had pushed adherence above 160%. Even though output continued to decline in Iran, Libya and Venezuela, the survey suggested that compliance had only fallen to 111% in July, suggesting more room for increasing production from the likes of Saudi Arabia or OPEC’s non-member ally Russia.

Trade worries whipsawed this week, keeping the market on edge, amid conflicting reports of U.S. action and proposed retaliation from China. Tensions on Wall Street eased significantly on Tuesday on a report from Bloomberg that both sides were trying to restart trade talks. But that was quickly countered by another report that the U.S. was considering raising tariffs on $200 billion in Chinese goods to 25% from 10%, which the White House later confirmed was under consideration. On Friday, China shot back with a potential plan for tariffs on $60 billion of U.S. goods. “The U.S. side has repeatedly escalated the situation against the interests of both enterprises and consumers,” China said, according to Reuters. “China has to take necessary countermeasures to defend its dignity and the interests of its people, free trade and the multilateral system.” White House Economic adviser Larry Kudlow warned China not to underestimate President Donald Trump.

The Dow Jones ended at 25,462, up 0.54%, high, but not at a peak, while, the US Dollar Chinese Yuan sat at 6.83, right at the top of its range, and China exerts pressure on the rate.

Bond rates were down a little, with the 10 Year benchmark sitting at 2.95, well down from its 3.12 in May. At the short end, the 3-month bond rate is 2.00, still at the top of its range. Libor is still sitting at 2.34, at the top of its range, signalling higher funding costs in the system.

Gold continues lower, at 1,222, as many risk investors are favouring the US Dollar at the moment. Bitcoin ended the week at 7,443 up 0.65% on Friday, but below its recent highs.

So back once more to cats and pigeons. Next week we will be hearing the latest from the Royal Commission in sessions covering wealth management. NAB and MLC are up first, but I will be especially interested in the evidence from the Industry superfunds. We suspect more revelations as the Commission works its magic. And the results from CBA will be a highlight, it will be interesting to see what they report in terms of net interest margin. I am expecting more loan repricing, both up and down.

It’s never a dull moment in the finance and property sector, so expect more turbulence ahead. The bumpy ride continues….

The final report [674 pages !] has been released earlier than expect, and contains a series of recommendations which will have significant impact on the industry. It also passes the weight test… A best interests test is recommended in the home loan market (a change from not unsuitable).

They call out regulatory failure and conflicts of interest across the sector, referring to opaque pricing, unsuitable products, no reward for customer loyalty as well as product complexity and faux competition. Major players have too much market power, and have fingers in multiple segments of the market. Customers lose out as a result.

“It is a fundamentally important fact that no Australian financial system regulator has the responsibility of putting competition first. Indeed, ASIC does not yet even have competition in its objectives. Nor, until this Inquiry, did other members of the Council of Financial Regulators emphasise that interest in a discernible fashion”.

Some of the key recommendations:

The Commission recommends the introduction of a best interest obligation for all providers in the home loans market — whether as a lender or mortgage broker — who interact directly with consumers seeking a home loan.

Mortgage Brokers trail commissions should be phased out (but not replaced by a fee for service). “At its simplest, brokers have a strong incentive — regardless of what may be in their customer’s best interest — to give preference in their loan recommendations to lenders that pay higher commissions. This may be uncommon, but there is no obligation for transparency of the payment to prove it.”

ASIC to ensure that the interests of borrowers are adequately safeguarded in the LMI market.

use of the term ‘advice’ should be limited to effort that is undertaken on a client’s behalf by a professional adviser.

APRA is singled out for myopic regulation. “Interest rates increased on both new and existing investment loans, boosting lenders’ profit on home loans. Up to half of the increase in lenders’ profit was in effect paid for by taxpayers, as interest on investment loans is tax deductible. We estimated that the cost borne by taxpayers as a result of changes in home loan investor rates following APRA’s intervention on interest-only loans in 2017, was up to $500 million per year (which may be partly offset by increased tax paid by the lending institutions on their profits)”.

ACCC should focus on encouraging competition across the industry and safeguarding the interests of consumers.

The new payments system needs a proper access regime.

The Payments System Board of the RBA should ban, by end-2019, all card interchange fees as a way to reduce distortions in payment choices and the flow-on costs of these distortions to merchants.

Here is their release:

The Australian economy has generally benefited from having a financial system that is strong, innovative and profitable.

There have been past periods of strong price competition, for example when the advent of mortgage brokers upset industry pricing cohesion. And technological innovation has given consumers speed and convenience in many financial services, and a range of other non-price benefits.

But the larger financial institutions, particularly but not only in banking, have the ability to exercise market power over their competitors and consumers.

Many of the highly profitable financial institutions have achieved that state with persistently opaque pricing; conflicted advice and remuneration arrangements; layers of public policy and regulatory requirements that support larger incumbents; and a lack of easily accessible information, inducing unaware customers to maintain loyalty to unsuitable products.

Poor advice and complex information supports persistent attachment to high margin products that boost institutional profits, with product features that may well be of no benefit.

What often is passed off as competition is more accurately described as persistent marketing and brand activity designed to promote a blizzard of barely differentiated products and ‘white labels’.

For this situation to persist as it has over a decade, channels for the provision of information and advice (including regulator information flow, adviser effort and broker activity) must be failing.

In home loan markets, the mortgage brokers who once revitalised price competition and revolutionised product delivery have become part of the banking establishment. Fees and trail commissions have no evident link to customer best interests. Conflicts of interest created by ownership are obvious but unaddressed.

Trail commissions should be banned and clawback of commissions from brokers restricted. All brokers, advisers and lender employees who deliver home loans to customers should have a clear legally-backed best interest obligation to their clients.

Complementing this obligation, and recognising that reward structures may still at times conflict with customer best interest, all banks should appoint a Principal Integrity Officer (PIO) obliged by law to report directly to their board on the alignment of any payments made by the institution with the new customer best interest duty. The PIO would also have an obligation to report independently to ASIC in instances in which its board is not responsive.

In general insurance, there is a proliferation of brands but far fewer actual insurers, poor quality information provided to consumers, and sharp practices adopted by some sellers of add-on insurance products. A Treasury working group should examine the introduction of a deferred sales model to all sales of add-on insurance.

Australia’s payment system is at a crucial turning point. Merchants should be given the capacity to select the default route that is to be used for payments by dual network cards — as is already possible in a number of other countries. The New Payments Platform requires a formal access regime. This is an opportunity — before incumbency becomes cemented — to set up regulatory arrangements that will support substantial competition in services that all Australians use every day.

More nuance in the design of APRA’s prudential measures — both in risk weightings and in directions to authorised deposit-taking institutions — is essential to lessen market power and address an imbalance that has emerged in lending between businesses and housing.

Given the size and importance of Australia’s financial system, and the increasing emphasis on stability since the global financial crisis, the lack of an advocate for competition when financial system regulatory interventions are being determined is a mistake that should now be corrected. The ACCC should be tasked with promoting competition inside regulator forums, to ensure the interests of consumers and costs imposed on them are being considered.

Prohibiting the payment of trailing commission could ensure that it no longer contributes to “consumer detriment with higher prices”, according to a new consultation paper from NSW Fair Trading.

In a consultation paper entitled Easy and Transparent Trading – Empowering Consumers and Small Business, released by NSW Minister for Innovation and Better Regulation Matthew Kean, the fair trading body considered reforms to help deliver the Productivity Commission’s agenda for the Innovation and Better Regulation portfolio and weighed in on recent scrutiny of trailing commissions.

The report comes ahead of the release of the Productivity Commission’s final report into Competition in the Australian Financial System, which is expected imminently and – if its draft report is anything to go by – is expected to make several recommendations regarding changes to broker commissions.

Despite the broking industry repeatedly outlining the benefits of trail and suggesting there is no evidence to prove negative impacts of it, the NSW government claimed that the payment of trail increases consumer costs and provides “little incentive” for “sellers” such as brokers to improve consumer outcomes.

The report reads: “In some cases, advisers may be earning these payments by providing the consumer with ongoing advice, regular appraisals of investments and strategy, and other services. In other cases, they are not. The commission is not based on the additional advice. Australia is one of the last markets in the world–along with some lenders in New Zealand–to pay trailing commissions to mortgage brokers.”

It continues: “The problem of trailing commissions is that they result in sellers of products continuing to receive income, irrespective of the level of service they are providing to consumers. This increases costs for consumers,” the report noted.

“Indeed, sellers have little incentive to apply their skills to improve the situation of people to whom they have already sold products.

“Additionally, where the fees are paid by consumers, it can be unclear for consumers what the total cost of the commission will be for the life of the product.”

The NSW government also predicted that the Royal Commission into Misconduct in the Banking, Superannuation and Financial Services Industry would “most likely make recommendations on conflicted payments in the financial and insurance sector”.

The government added: “This highlights the need to ensure that all consumers, regardless of the service to which they are referred, have the benefit of consumer protections available in other sectors.

“These commissions contribute to consumer detriment through higher prices. In addition, non-disclosure of such commissions means that consumers cannot make a fully informed choice to proceed with the referred service.”

The state government also proposed the following reforms that it claimed could help address such “issues”:

Amending the Fair Trading Act to prohibit providers of services, products or advice from paying trail commissions to intermediaries who recommend or refer customers to their business.

Requiring all intermediaries who refer consumers to third parties to fully disclose the benefit the intermediary will receive if a trailing commission will be paid on a successful referral, over the life of the product.

Prescribing that a trailing fee or commission is a “key term” which must be fully and clearly disclosed by the service or advisory business when entering into the service contract with the customer. Public comment is sought on the appropriateness of these commissions.

It should be noted, that the latter suggestion regarding a transparent disclosure of trail commissions received by mortgage brokers is already common practice in this sector.

The state government is therefore asking the public to put forward a “workable solution to balance the needs of industry and consumers where trailing commissions impact negatively on the market”.

The proposed reforms in the paper and policy ideas are reportedly “the result of a ‘sweep’ of legislation and regulations in the Better Regulation portfolio, a review of reports by think-tanks and government agencies on the Australian, NSW and other advanced economies and the Minister’s call for ideas from more than 100 think-tanks, industry groups, academics and other stakeholders”.

The public is being invited to provide comments to the consultation paper by 27 August 2018.

The number of Australians falling behind on their mortgages will rise in the next two years as interest-only loans end and repayments get more expensive, ratings agency Moody’s has warned, via MSN.

Delinquencies on loans that have converted from interest-only to principal and interest are running at double the rate of those still on interest-only, Moody’s said in a report released on Thursday.

“When IO (interest-only) loans convert to P&I (principal and interest), borrowers have to make higher monthly repayments, and this ‘payment shock’ can lead to mortgage delinquencies and makes IO loans riskier than P&I loans,” Moody’s said.

Repayments jump by around 30 percent when mortgages convert to principal and interest, the agency said.

Currently, the delinquency rate for mortgages converted to principal and interest is 0.94 per cent – a rate also above the arrears rate for all mortgages.

“Refinancing interest-only mortgages is also becoming more difficult, which will in itself contribute to an increase in mortgage delinquencies,” the ratings agency said.

About 40 per cent of loans by Australian banks in 2014 and 2015 were interest-only for five years, meaning a large portion are set to come under pressure with higher repayments in 2019 and 2020, said Moody’s.

Moody’s report backs up findings from Digital Finance Analytics (DFA), which estimates that more than 970,000 Australian households are now believed to be suffering housing stress.

That equates to 30.3 percent of homeowners currently paying off a mortgage.

Of the 970,000 households, DFA estimates more than 57,100 families risk 30-day default on their loans in the next 12 months.

“We continue to see households having to cope with rising living costs – notably childcare, school fees and fuel – whilst real incomes continue to fall and underemployment remains high,” wrote DFA principal Martin North.

“Households have larger mortgages, thanks to the strong rise in home prices, especially in the main eastern state centres, and now prices are slipping.

“While mortgage interest rates remain quite low for owner-occupied borrowers, those with interest-only loans or investment loans have seen significant rises.”

At its meeting ending on 1 August 2018, the MPC voted unanimously to increase Bank Rate by 0.25 percentage points, to 0.75%. The Committee voted unanimously to maintain the stock of sterling non-financial investment-grade corporate bond purchases, financed by the issuance of central bank reserves, at £10 billion. The Committee also voted unanimously to maintain the stock of UK government bond purchases, financed by the issuance of central bank reserves, at £435 billion.

Since the May Inflation Report, the near-term outlook has evolved broadly in line with the MPC’s expectations. Recent data appear to confirm that the dip in output in the first quarter was temporary, with momentum recovering in the second quarter. The labour market has continued to tighten and unit labour cost growth has firmed.

The MPC’s updated projections for inflation and activity are set out in the August Inflation Report and are broadly similar to its projections in May.

In the MPC’s central forecast, conditioned on the gently rising path of Bank Rate implied by current market yields, GDP is expected to grow by around 1¾% per year on average over the forecast period. Global demand grows above its estimated potential rate and financial conditions remain accommodative, although both are somewhat less supportive of UK activity over the forecast period. Net trade and business investment continue to support UK activity, while consumption grows in line with the subdued pace of real incomes.

Although modest by historical standards, the projected pace of GDP growth over the forecast is slightly faster than the diminished rate of supply growth, which averages around 1½% per year. The MPC continues to judge that the UK economy currently has a very limited degree of slack. Unemployment is low and is projected to fall a little further. In the MPC’s central projection, therefore, a small margin of excess demand emerges by late 2019 and builds thereafter, feeding through into higher growth in domestic costs than has been seen over recent years.

CPI inflation was 2.4% in June, pushed above the 2% target by external cost pressures resulting from the effects of sterling’s past depreciation and higher energy prices. The contribution of external pressures is projected to ease over the forecast period while the contribution of domestic cost pressures is expected to rise. Taking these influences together, and conditioned on the gently rising path of Bank Rate implied by current market yields, CPI inflation remains slightly above 2% through most of the forecast period, reaching the target in the third year.

The MPC continues to recognise that the economic outlook could be influenced significantly by the response of households, businesses and financial markets to developments related to the process of EU withdrawal.

The Committee judges that an increase in Bank Rate of 0.25 percentage points is warranted at this meeting.

The Committee also judges that, were the economy to continue to develop broadly in line with its Inflation Report projections, an ongoing tightening of monetary policy over the forecast period would be appropriate to return inflation sustainably to the 2% target at a conventional horizon. Any future increases in Bank Rate are likely to be at a gradual pace and to a limited extent.

ANZ has become the first big lender to cut its variable home loan rate for new customers, as the banks slug it out for business in a tightening market.

While banks including the CBA have cut fixed loan rates and offered “honeymoon deals” in recent weeks, the ANZ is the first to move on variable rates.

It comes at a time when there is upward pressure on interest rates as funding costs, particularly for smaller lenders, are rising.

The ANZ told mortgage brokers it was bringing down its basic principal and interest home rate for owner-occupiers by 0.34 percentage points to 3.65 per cent.

The ANZ offer only applies to new customers looking for a loan valued at 80 per cent or less than the value of their property.

Loan-to-value ratios above 80 per cent remain unchanged at 3.99 per cent.

Non-bank lenders growing market share rapidly

It comes at a time when small lenders have been eroding the market share of the Big Four banks.

While non-bank lenders hold less than 8 per cent of the mortgage market, their loan books have grown by about 14 per cent over the year, while growth at the Big Four is at a historically low level, a little over 1 per cent.

Ratecity research director Sally Tindall said it was a surprising move from ANZ to buck the rate-hike trend.

“It shows that the bank is competing hard to get new customers as non-banks threaten their market share,” Ms Tindall said.

“This comes at a time when the market was expecting ANZ to hike rates and not cut them and the [banking] royal commission has turned the playing field on its head.”

There are lower rates offered by the big banks in the market but they are generally so-called honeymoon deals that step up markedly after two or so years, or four years in the case of most fixed loan products.

Ms Tindall said the other three big banks were likely to come under pressure to follow ANZ’s lead or risk a further erosion of their market share.

Carefully targeted cut

Shaw and Partners bank analyst Brett Le Mesurier said ANZ’s move was carefully targeted.

“I was surprised by the extent of the reduction but ANZ has been courting the owner-occupier market for some time, and shunning the investment market relatively — most of their loan growth has been coming from Australian owner-occupier loans,” Mr Le Mesurier said.

He said there was little doubt that the differential between high-quality owner-occupier rates and investor loan rates was likely to increase.

“The banks are focusing on the below 80 per cent LVR [loan-to-value ratio] owner-occupier loans and that may well be because they expect the capital charges associated with those loans to reduce.

The bank is also cutting some of it fixed rate loans by up to 0.24 percentage points, following CBA’s move to cut fixed rates on various two and three-year fixed rate loans by 0.1 percentage points earlier this week.

As many as 15% of surveyed homeowners have faced challenges when trying to refinance, due to falling property prices.

Research conducted by mortgage lender State Custodians, quizzed 1,022 home owners on their ability to refinance in the current climate, as national average home values continues to fall.

According to CoreLogic market data for the month of July, capital city home prices declined by 0.6% and now stand 2.4% lower over the year; it is the largest monthly decline in six and a half years. The national home price index also declined by 0.6% to average a 1.6% decline over the year.

The figures published by State Custodians also revealed that young people were the most affected, with around 34% of those under the age of 34 saying they’ve been unsuccessful in re-financing because of declining property values.

“Property prices have been stagnating and falling across much of Australia for some time now – especially in the major capital markets of Sydney and Melbourne – which has made refinancing tougher for some,” State Custodian general manager Joanna Pretty said in a statement.

“Anyone who has not yet built up a substantial amount of equity in property or whose property has fallen in value is more likely to be unsuccessful in seeking refinancing,” she added.

However, there is some good news as 29% of respondents said they are confident their property’s value has improved since purchase. Further, 41% of people with mortgages have successfully refinanced their home and experienced no problem getting a better rate as their property’s value increased.

Pretty said that when refinancing, homeowners and investors are often overly confident that their property increased in value.

“Declines in property value are influenced by what is happening in the market and the land value of the area,” she said. She explained that valuation of homes even in good areas can still come back below expectation due to poor property maintenance and upkeep.

Pretty suggested that “it may also be helpful to be present when a valuer visits to point out improvements that may not be immediately apparent, such as solar panels.”

Elsewhere, AB says brokers can help the thousands of people labelled ‘mortgage prisoners’ by directing them to non-bank lenders, is the call from an industry association.

Mortgage prisoners are borrowers unable to refinance to a lower interest rate due to changed lending criteria by the banks.

FBAA executive director Peter White said the government should also step in and push banks to be realistic with their modelling.

He revealed he personally brought up the issue with federal treasurer Scott Morrison when the two caught up at a recent lunch.

White said banks have recently increased the interest rate ‘buffer’ they add onto a loan to ensure the borrower has capacity to pay if rates rise, but the extent of the increase has led to a situation where borrowers who are already paying a mortgage are being rejected for loans that actually reduce their repayments.

He said, “It’s madness. Someone wants to refinance to pay a lower rate yet the bank adds an extra 4% to the interest rate and decides the borrower can’t afford to pay less.”

He said while he understands the need for a lender to add a safety net to the prevailing interest rate, they are now effectively doubling the rate to a level where the borrower can’t meet the new lending criteria.

He added, “This doesn’t affect the wealthy, it affects those who can least afford it and it has almost stalled the home loan refinance market.”

The assessment change is a knee-jerk reaction by the banks to recent inquiries and the royal commission, according to White, who predicts the banks may start to set an even higher rate.

He said the situation only reinforces the value of the expert advice that finance brokers provide and has urged brokers to be proactive in the space.

He said, “Many Australians are not even aware of non-bank lenders, let alone the difference or that they are not under some of the same regulatory oversight, so we must educate and help them. We know the banks won’t!”

Digital banking platform start-up, Trade Ledger, has been named the “Ashurst Fintech Start-up of the Year” after expanding into the UK market and signing up a series of major deals in just one year.

Trade Ledger is the world’s first open digital banking platform that gives banks and other business lenders the ability to assess business lending risk in real time. This will enable these lenders to address the £1.2 trillion of undersupply in trade finance lending globally, while providing high-growth companies with the working capital needed to sustain growth.

The award goes each year to a fintech start-up “that has disrupted the financial services sector with new and innovative services, creating competition and transforming the way we experience financial services”.

Trade Ledger has done this by being the first corporate lending platform in the world to automate the entire credit assessment process, assess SME supply chain data in real-time, and calculate risk down to the individual invoice.

This allows banks and other business lenders to tap into the AU$90 billion of unmet business credit demand in Australia, and US$2.1 trillion globally.

“As the global economy transitions towards smaller, high-growth businesses – our all-important start-up and innovation ecosystem – business lenders have an obligation to learn how to supply working capital desperately needed by these businesses of the future,” said Martin McCann, CEO and Co-Founder of Trade Ledger.

“Australian banks and business lenders also face risks on several fronts. On the one hand, they need to improve both their cost/income ratio and their capital efficiencies within this segment that is traditionally considered as high risk. On the other, they are facing increased competition from technology behemoths such as Amazon, Tencent, and eBay, who are all threatening to use their hordes of data to enter financial services.

“The Trade Ledger platform equips these lenders with the same degree of technological proficiency as these massive tech firms, while arming them with the tools needed to meet our booming innovation ecosystem’s need for credit,” concluded Martin McCann.

This is the third year the FinTech Awards have been running, and the FinTech Awards owner, Glen Frost, was particularly impressed with both the quality and quantity of this year’s applications.

Speaking on the night, Glen Frost said: “The 3rd Annual FinTech Awards recognise and reward the innovators and the risk takers. To be recognised by your peers for your innovation and entrepreneurial spirit will sustain you through the tough times, it will motivate you, and it will show your customers, investors and staff, that you’ve got what it takes.

“I congratulate Martin McCann, and his team at Trade Ledger, on winning the Ashurst FinTech Startup of the Year.”

The keynote guest speaker for the evening was the Hon Scott Morrison, MP, Treasurer, who told the crowd that he was relying on the fintech community to ensure the success of his policy on comprehensive credit reporting.