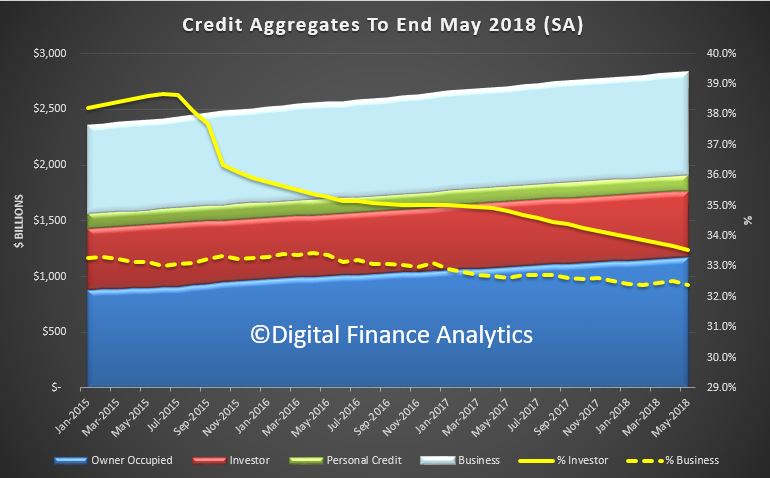

The RBA data shows that total housing lending rose 0.37% from last month, up $6.6 billion to $1.76 trillion. Within that, owner occupied housing rose 0.55% or $6.5 billion, and investment lending rose just 0.02% or $220 million. Personal credit fell again, and business lending fell 0.3% down $2.5 billion to $917 billion, all seasonally adjusted.

Investment lending made up 33.5% of all housing loans, down from 33.7% the previous month, and continues to slide, as expected. However the drop in business credit meant the proportion of commercial lending fell to 32.4% of all lending.

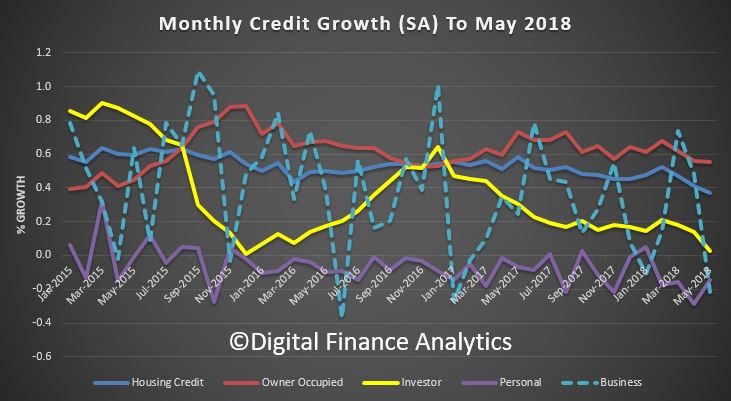

The monthly growth trends show the fall in business lending, and the fall-off in investor lending, all seasonally adjusted, which in the current environment may well be writing the volumes down too far.

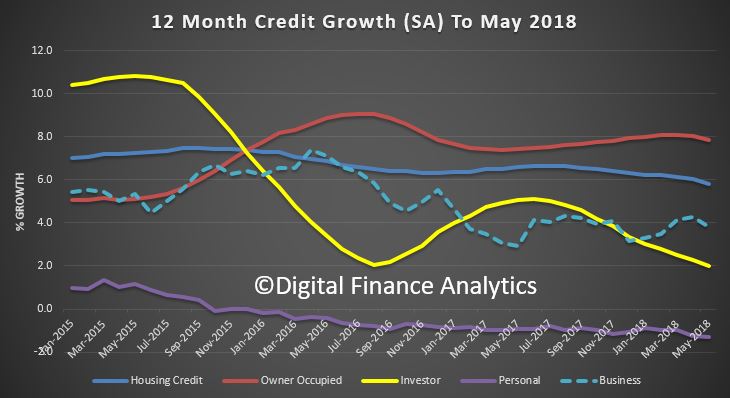

The 12 month rolling trend shows owner occupied housing still running at 7.9%, well above inflation and wage growth, while investor lending has a read of 2%, which is the lowest see since the RBA series started to be published in 1991. Have no doubt, investor lending is fading.

Personal credit dropped an annualised 1.3%, the largest fall since the fall out from GFC in 2009. Business lending was around 3.8% annualised and slid a little.

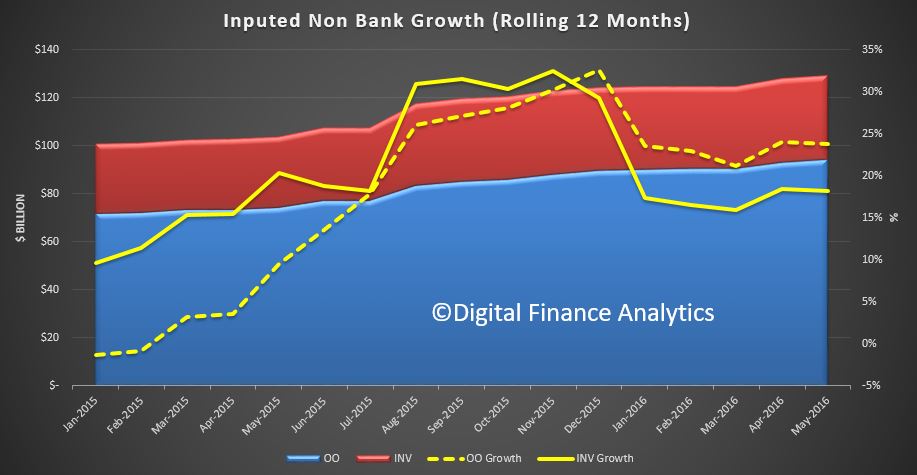

Finally, the non-bank contribution to lending growth can be imputed by subtracting the APRA ADI data from the RBA market data. This is an inexact science because of timing and coverage issues across the data. But it tells an interesting story, with non-bank growth rates sitting at around 20% for owner occupied loans and around 18% for investor loans, on a twelve month rolling basis. So we can see where some of the slack in the system is being taken up as non-banks flex their muscles. Regulation of this sector is a concern, as Moody’s highlighted recently. APRA has this responsibility, but how actively they are looking at this segment of the market, when data is so hard to acquire is a moot point. My guess is they are light on.

The rapid growth of non-bank lenders reflects the positive quality of their loan books and residential mortgage-backed securities (RMBS) – but growth should happen in a sustainable way, according to Moody’s Investors Service; via MPA.

Moody’s vice president and senior analyst John Paul Truijens said in a statement that although “investment and interest-only mortgages have historically been riskier than owner-occupier principal and interest mortgages, they are less risky than the non-conforming or alternative documentation loans that most non-bank lenders have traditionally focused on”.

The conclusions are found in Moody’s recently released study, “Financial institutions and RMBS – Australia: Growth opportunities not without risks as non-bank lenders push into investment and interest-only mortgages”. The report was written by Truijens and another Moody’s vice president and senior analyst, Daniel Yu.

The report stressed that the push into investment and interest-only lending has further captured the interest of private equity investors. And this has led to three acquisitions of non-bank lenders in the last nine months.

“If the current rapid growth rate were to be sustained over a prolonged period or even rise, or if non-bank lenders were to push into the riskier segments of the investment and interest-only mortgage markets to maintain growth, this would pose risks,” Truijens and Yu said.

According to them, non-bank lenders may need to rapidly expand their underwriting teams, and this could compromise the quality of their staff experience and risk controls.

If the banks return to pursue strong investments and interest-only lending, increased competition would make it difficult for non-bank lenders to sustain their rapid growth and this could push them to the riskier segments of the mortgage market.

Moody’s still believes non-bank lenders are generally suited to underwrite and risk-price investment and interest-only loans. But borrowers’ financial situations need to be scrutinised even more for these mortgages than for owner-occupier principal and interest loans. The experience of non-bank lenders in underwriting non-conforming loans enables them to demonstrate such scrutiny.

Risks are further lessened by the legislative amendments made in February 2018 that now allow APRA to regulate non-bank lenders.

Funding of non-bank lenders is not guaranteed, according to Moody’s. These lenders depend on “bank funding via warehouse facilities for the initial organisation of loans and RMBS investors for RMBS issuance”. Both funding sources depend on market confidence and economic conditions.

Non-bank lenders are increasingly getting into the investment and interest-only loan market after APRA released a series of measures in 2014 that limit banks from offering such loans. Non-banks accounted for almost 35% of investment loans originated in 2017, up from around 15% in 2014. Their share of interest-only mortgages was around 25%. However, the report said the non-bank mortgage sector still remains relatively small in Australia despite massive growth, accounting for just under 4% of the $1.7trn mortgage market.

The ABA says Australia’s four major banks have reached an agreement to protect vulnerable customers from being unfairly treated in the new mandatory Comprehensive Credit Regime.

The four major banks, who will be required to report the credit history of 50% of customers by the end of September, will not include customers who have reached agreement on hardship arrangements with their bank. This will continue for the first 12 months of the regime while the Attorney-General is conducting a review into this issue.

CEO of the Australian Banking Association Anna Bligh said this was a critical issue for Australia’s major banks who were united behind this arrangement to ensure all customers are treated fairly in what will be an important change in credit history reporting.

“Australia’s banks have been working closely with the Federal Government and other stakeholders to ensure we get this major reform right, without unfairly treating some customers, and implemented without delay,” Ms Bligh.

“Australia’s banks are fully behind this new regime and see the great benefit it can bring in helping customers quickly and easily get a great deal on their personal loans, home loans and credits cards. The four major banks are committed to meeting the start date of 30 September in accordance with the CCR regime.

“Currently if you have a great credit history, the only organisation who knows this is your bank.

“This new regime takes that powerful information and places it into the hands of customers who can ensure they get the best deal possible from a financial institution.

“As with all major reforms in banking it’s important we don’t leave people behind.

Those who have experienced hardship through no fault of their own such as losing a job, sickness, natural disasters or relationship breakdown need to be protected in this new regime.

“Unexpected events happen in life, which banks understand, therefore it’s important that we can discreetly show this on credit histories to make sure customers don’t have further difficulty in the future,” she said.

As the spot light turns to the emerging trade wars with the USA, the impact may be to push bond rates lower, according to Moody’s. As a result, this may also mean the FED will not raise interest rates in the US as fast as expected. This might therefore in turn act to dampen rate rises in other countries.

A still-positive outlook for operating profits is now marred by considerable uncertainty. What may degenerate into an extended trade war of attrition could preserve financial market volatility indefinitely.

Given the global complexities of modern supply-chain management, a surprisingly large number of U.S.-based businesses may delay capital spending and staffing plans until trade-related uncertainties are sufficiently resolved. As it now stands, tariff-driven increases in material costs have compelled some companies to rein in employee compensation for the purpose of protecting profit margins. In addition, higher materials costs have been weighing on the credit quality of some manufacturers that use steel intensively.

Tariffs explain why year-to-date advances of 40% for the spot price of steel and 21% for the most actively traded lumber futures contract are so much greater than the accompanying 0.5% dip by Moody’s industrial metals price index (which excludes steel’s price). To the degree tariffs increase the costs of materials and inventories, businesses will tighten their control of other costs, the most prominent being employee compensation.

Relaxation of China’s Monetary Policy May Limit Upside for Fed Funds

Any trade war will require the use of all policy weapons. Recently, the Peoples Bank of China adopted a more accommodative monetary policy ostensibly in response to slower than expected domestic spending and a need to enhance systemic liquidity. The latter brings attention to difficulties arising from troubled loans. Though not specifically mentioned, one of the intentions of the latest relaxation of China’s monetary policy is to allow China to better withstand any loss of economic activity to a trade war.

Not to be overlooked is how the $521 billion of U.S. merchandise imports from China during the 12-months-ended April 2018 far exceeded the comparably measured $133 billion of U.S. merchandise exports to China.

Worth mentioning is how that imbalance includes billions of dollars of goods that are manufactured in China for U.S.-domiciled businesses. China is unrivaled as far as being a manufacturing platform for companies based in advanced economies. Thus, many American businesses and shareholders are vulnerable to tariffs imposed on imports from China.

In quick response to the relaxation of China’s monetary policy, the U.S. dollar rose to 6.604 yuan. Though the latter was the highest yuan price of the dollar since mid-December 2017, it was still -4.7% under December 2016’s average of 6.929 yuan. Of course, Chinese officials worry that expectations of a weaker yuan might prompt unwanted capital outflows from China.

Nevertheless, a wider interest rate gap between the U.S. and China would favor a cheaper Chinese currency versus the dollar. In turn, a depreciation by China’s currency vis-a-vis the dollar would offset part of any tariff-induced increase in the dollar price of U.S. imports from China.

All else the same, a costlier dollar exchange rate diminishes prospects for U.S. corporate earnings. The recent strengthening of the dollar against a broad array of currencies from both advanced economies and emerging market countries will reduce (i) the global price competitiveness of goods and services produced in the U.S. and (ii) the dollar value of foreign-currency denominated earnings from abroad.

On the positive side, a stronger dollar will lessen the risk of faster consumer price inflation. As a result, a stronger dollar can substitute for Fed rate hikes.

Ten-year Treasury Yield Is Less Likely to Have an Extended Stay Above 3%

In view of how recent rate hikes and a nearly 3% 10-year Treasury yield disrupted financial markets outside the U.S., the Federal Open Market Committee’s latest median projection of a 2.375% midpoint for fed funds by the end of 2018 may prove to be too high.

Recognizing the risks implicit to a possible trade war and the disinflationary effect of further dollar exchange rate appreciation, the futures market disputes the FOMC’s median projection for fed funds and recently assigned only a 44.2% probability to a year-end midpoint for fed funds that exceeds 2.125%. If other central banks pursue policies that facilitate dollar appreciation, the Fed may have no choice but to stretch out its planned normalization of U.S. monetary policy.

Just prior to the latest outbreak of trade-related stress, the 10-year Treasury yield closed at June 14’s 2.94%. Since then, the benchmark Treasury yield eased to a recent 2.83%. From the perspective of the accompanying 3.0% drop by the market value of U.S. common stock since June 14, the decline by the 10-year Treasury yield has not been especially deep.Nevertheless, a downwardly revised outlook for Treasury yields has prompted a 5.8% advance by the Dow Jones Utility index since June 14.

However, despite the possibility of lower than earlier expected mortgage yields, an index of housing-sector share prices has sunk by 5.1% since June 14. The latter brings attention to how trade related uncertainties and financial market volatility may force businesses to show restraint when it comes to staffing and employee compensation.

In turn, the upside for home sales may continue to be limited by the subpar financial condition of many lower- and middle-income households. The pitifully low 3.1% personal savings rate of the 12-monthsended April 2018 highlights the well below-average financial flexibility of many Americans. Implicit to such a very low average for the personal savings rate is the likelihood that 33% to 40% of U.S. households save an imperceptible, if any, amount of their after-tax income.

When a financially stronger middle class provided a hospitable breeding ground for the persistently rapid consumer price inflation of 1972-1981, the personal savings rate averaged a much higher 11.4%. Yes, consumer price inflation may spurt higher every now and then, but today’s average American consumer may lack the financial wherewithal necessary for the establishment of stubbornly rapid price inflation.

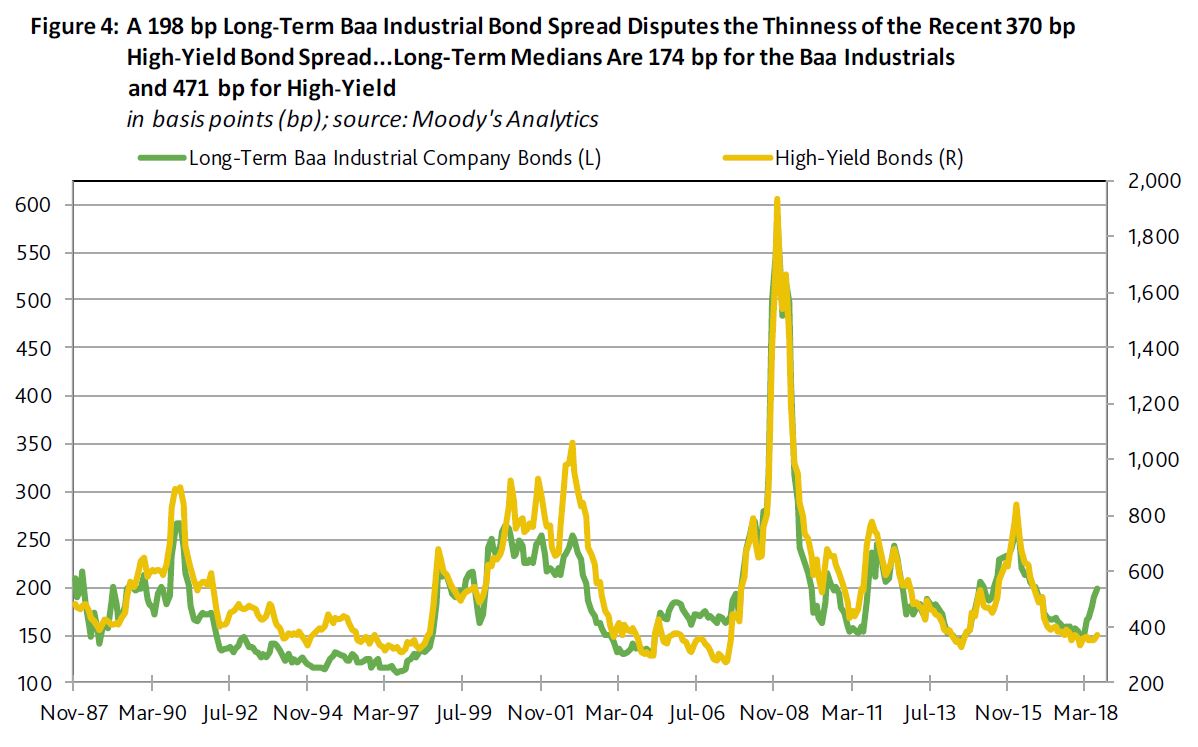

VIX and Baa Yield Spread Imply High-Yield Bond Spread Is Unsustainably Thin

Though a composite high-yield bond spread has widened from June 14’s 345 basis points to the 370 bp of June 27, the latter still remains well under the spread’s post September 2003 median of 460 bp. However, a recent VIX of 18.0 points was noticeably above its accompanying median of 15.9 points. In the event the VIX remains above 16.5 points, the high-yield spread is likely to widen to at least 425 bp.

A recent long-term Baa-grade industrial company bond yield spread of 198 bp that well exceeds its post September 2003 median of 178 bp reinforces the negative outlook for high-yield bonds. As inferred from the historical record, a 198 bp spread for the long-term Baa industrials has typically been associated with a 544 bp midpoint for the high-yield spread, which is much wider than the recent 370 bp. It was in 2007 that a well below trend high-yield spread was joined by a significantly above average Baa yield spread.

Since late 1987, the high-yield bond spread shows a very strong correlation of 0.92 with the long-term Baa industrial company bond yield spread.

The Bank for International Settlements, Banker’s Bank has released their latest annual report. We looked at the section on how banks are fudging their ratios in our earlier post “Are Some Banks Cooking the Books?” But within its 114 pages, the BIS report also painted a worrying picture of where the global economy stands.

They say, economies are trapped in a series of boom-bust boom-bust cycles which are driving neutral interest rates ever lower and driving debt higher. The bigger the debt the worse the potential impact will be should rates rise (as they are thanks to the FED). Yet in each cycle “natural” interest rates are driven lower Implicitly the current settings are wrong.

It is as clear an articulation of the underlying issues which are driving us towards the rocks, and at quite a clip. I still hold 2019 as the critical year, my four scenarios still seem about right, with risks biased towards more concerning outcomes.

Claudio Borio, the BIS’s chief economist said “The end may come to resemble more closely a financial boom gone wrong, just as the latest recession showed, with a vengeance”.

This is a dark warning, coming as it does from the organisation which is effectively the peak body for central bankers around the world. This is no fringe movement. This is the brain of the banking system speaking!

In fact, the risks in the global monetary system remain from the Lehman crisis in 2008 and aggregate debt ratios are almost 40 percentage points of GDP higher than a decade ago.

The BIS report said: “Global US dollar funding markets are likely to be a key pressure point during any future market stress episode. There are significant roll-over risks, as sizeable parts of banks’ US dollar funding rely on short-term instruments (repos, and currency swaps).”

The BIS says central banks are on the horns of a dilemma. Do you lift rates sharply as the FED has done, or go slowly, both are fraught with difficulty. They call this the ‘great unwinding’ of the debt laden stimulus, and again it seems we are in uncertain and uncharted territory. As the report says, “A strategy of gradualism is no panacea, as it may encourage further risk-taking”. The gloom was overdone early last year but now exuberant investors may be making the opposite error, with the world 12 months further into a stretched financial cycle. Has sentiment has swung too far?

The truth is, those hoping to time global asset markets by waiting for the usual signs that the cycle has peaked risk being caught off guard. The deflationary forces of technology and a globalised labour force mean that trouble can creep up on them before inflation emits the usual warning signals.

The bank says under the precious “Phillips Curve” model, wage growth would pick up late in the cycle as the economy reached full employment. Wages would rise and inflation would pick up. So then the Fed and other central banks would lift rates – boom-bust, and it would usually lead to a recession. But, now globalisation has killed the inflation warning signals. Then you have more than 2 billion people coming on stream into the global economy from China and Eastern Europe has dampened wage growth and as a result a substantial and lasting flare-up of inflation does not seem likely.

Instead the excess stimulus driven by low rates has simply gone into asset bubbles instead. It may look benign if inflation is low but the BIS argues that it is extremely damaging. The cycle ends with a financial crisis. Again.

In fact, my read is that the BIS are saying (in bankers speak perhaps) that the big central banks misread the globalisation era with too much stimulus letting assets booms run, but stepping in with maximum stimulus in busts.

The Fed and others have in effect drawn forward prosperity from the future. It takes ever lower real interest rates with each cycle to hold the system together. At some point interest rates will hit the limit.

So now the way ahead is fraught with danger, as rates are lifted, the risks of a financial crisis follow, and the prospect of a benign set of outcomes is now fading. The BIS says the only way for the world to dig itself out of this hole is to raise productivity from its current anaemic levels. Countries must reform and shift fiscal policy from consumption to investment.

And in a parting shot, the report says, the most destructive course is to undermine free trade itself and impose trade tariffs and other forms of protectionism. “Rolling back globalisation would be as foolhardy as rolling back technological change,” Mr Borio said.

A non-bank lender has revealed how it stress-tests new residential projects amid fears of oversupply, rising defaults, falling property prices and a significant reduction in foreign buyers; via the Adviser.

Growing fears surrounding the sustainability of Australia’s new apartment market have been growing since China tightened its capital controls, the Australian government introduced new regulations and taxes on foreign buyers and the majors stopped lending to overseas investors.

The latest Foreign Investment Review Board (FIRB) figures show that overseas property investment fell by 65 per cent in FY17.

A BIS Oxford Economics report released this week forecasts that, given the extent of new apartment construction relative to houses, there are likely to be pockets of oversupply of apartments across Melbourne. The city’s median unit price is forecast to fall by a total 2 per cent in three years, or 9 per cent in real terms, according to BIS.

Meanwhile, in Brisbane, the forecast for unit prices in 2018 will be 25 per cent lower than their real peak in 2010.

Late last year, UBS warned that poor-quality projects are “under significant pressure” and that one in five, or 20 per cent, of foreign buyers are failing to settle.

Non-bank lender Qualitas, which funds residential real estate projects on the east coast of Australia, has said that it is “very conservative” about funding new developments.

“The default rates are not substantial,” Qualitas managing director Andrew Schwartz said.

“To the extent that a developer is left with some residual stock, it is generally their profit in the development. Or it is an amount that allows them to take out a residual stock loan. That is why you are not reading stories about buildings being sold by receivers.”

Qualitas calculates a decent fall over rate when funding property developers and is well aware of some of the fears surrounding the Australian apartment market.

“We already assume defaults. We assume the property market comes down in value,” Mr Schwartz said.

“What you generally find in the developments that we do is, if you start with one times pre-sale, that means if you give someone a $100 loan, they have at least got $100 of sales in their development. So long as you start on one times, what you will find is you can withstand about a 20 per cent decline in property value and a 20 per cent default on those that committed to you and you will still earn your full rate of return of interest.”

To date, the group has funded 109 projects and earned full returns on all of them.

Non-bank lenders like Qualitas have grown in recent years after the majors reduced their appetite for apartment funding, foreign buyers and mezzanine debt.

YBR announced that Yellow Brick Road Investment Services has entered into a book sale and purchase agreement with INPRO Australia.

The transaction will see INPRO senior financial adviser Alex Kean acquire YBRIS’ advice service relationships, records and recurring revenues – impacting about 150 private clients.

YBR said the decision to sell is based solely on the YBR Wealth division focusing on the scale provided by the YBR branch franchisee and Vow adviser and broker network, and other platforms.

INPRO will pay $425,000 for the client book; about 80% of which is payable upfront. The remainder is to be paid 12 months post-completion, adjusted depending on revenues.

YBR executive chairman Mark Bouris said it is important that clients are provided with the best financial service possible, saying INPRO is in a better position to offer this than YBR.

“YBRIS is a stand-alone legacy business within the broader YBR Wealth division of the YBR Group and its portfolio did not fit within the operational structure required for a branch and broker focused network,” Bouris said.

INPRO is delighted with this announcement and is looking forward to working with YBR’s wealth clients, Kean said.

“INPRO has a long and proud history of working closely with clients to deliver tailored advice solutions in a professional, yet highly personalised manner. Our clients value our integrity, transparency and dependability which we’re confident the YBR clients will also embrace,” he added.

YBR will work with INPRO to ensure a seamless transition, he added. The transaction is expected to be complete within two months.

He described the basics of Crypto, with reference in particular to Bitcoin, compares it with money, and concludes that many of these shortcomings of cryptocurrencies stem from their design around trustless distributed ledgers and the costly proof-of-work verification method that is required in the absence of a trusted central entity. In contrast, in situations where there are trusted central entities in well-functioning payment systems, there may be little need for cryptocurrencies.

He then goes on to explore the implications for central banks.

The Bank has been watching developments in these areas for about five years. Currently, however, cryptocurrencies do not appear to raise any major concerns for the Bank given their very low usage in Australia. For example, it is hard to make a case that they raise any significant concerns for the Bank’s mandate to promote competition and efficiency and to control systemic risk in the payments system.

Nor do they currently raise any major issues for the Bank’s monetary policy and financial stability mandates. There are only very limited links from cryptocurrencies to the traditional financial sector. Indeed, many financial institutions have actively sought to avoid dealing with cryptocurrencies or cryptocurrency intermediaries. So, it is unlikely that there would be significant spillovers to the broader financial system if cryptocurrency holders were to suffer valuation losses or if a cryptocurrency system or intermediary was compromised.

But given all the interest in cryptocurrencies or private digital currencies, people have inevitably asked whether central banks should consider issuing digital versions of their existing currencies. I can give you an indication of the Bank’s preliminary thinking on this issue, as outlined in December by the Governor in a speech entitled ‘An eAUD?’.

Currently if households wish to hold money, they have two choices. They can hold physical cash, which is a liability of the Reserve Bank, or they can hold deposits in a bank (or credit union or building society), which is an electronic form of money and is a liability of a commercial bank that is covered (up to $250,000) by the Financial Claims Scheme. Both forms of money serve as a store of value and a means of payment (assuming the bank deposit is in a transaction account).

Most money is already ‘digital’ or electronic in form. Currency now accounts for only about 3½ per cent of what we call broad money. The remaining 96½ per cent is bank deposits, which we might call commercial bank digital money.

Furthermore, the use of cash by households in their transactions has been falling in recent years. This next graph shows there has been strong growth over an extended period in the use of cards and other forms of electronic payments. In contrast, the dots, which are from the Bank’s Consumer Payments Survey, show a significant fall in the use of cash. In 2007, cash accounted for nearly 70 per cent of the number of household transactions. Nine years later, this had fallen to 37 per cent.

Clearly, some households are moving away from cash and finding that electronic payments provided by banks better meet their needs. And this trend is likely to continue as the New Payments Platform (NPP), which launched recently, allows banks to offer better services to households – namely real-time electronic payments that give immediate value to the recipient, are easily addressed, are available 24/7 and carry lots more data than currently.

So the question is: ‘should the Reserve Bank introduce a new form of cash – an eAUD as the Governor called it – to give households an electronic payment instrument issued by the central bank for their everyday payments?’

Our current thinking is that there would not necessarily be all that much demand for an additional form of money in normal times, though this would presumably depend partly on design decisions such as the interest rate (if any) that would be paid on this money.

But to the extent that there was significant demand, particularly if this occurred at times of financial uncertainty with households switching out of the banking sector, there could be significant implications for the Bank’s financial stability mandate. There would also be implications for the structure of the financial sector – for example, it could result in reduced financial intermediation. We would need to think through these implications carefully.

So for the time being at least, consideration of a possible new electronic form of money provided by the Reserve Bank to households is not something that we are actively pursuing. Based on our interactions with our counterparts in other countries, it is also not front of mind for most other advanced economy central banks. An exception is Sweden, where the shift away from the use of cash is significantly more advanced than in Australia and elsewhere. Sweden’s Riksbank is studying the issues regarding the possible issuance of an e-krona and expects to report by late 2019.

However, as the Governor indicated in December, there might be a stronger case for considering a new form of central bank liability for use by businesses and financial institutions.

Here it is important to remember that the Reserve Bank already offers electronic balances to financial institutions in the form of Exchange Settlement Accounts (ESAs) at the Reserve Bank. These balances can be passed between financial institutions during the banking day, with the Bank keeping the official record (or the ledger) of account balances.[10] A key function of ESAs is that they provide banks with a risk-free liquid asset for settling payment obligations through the day, to prevent the build-up of large exposures that could threaten financial stability.

However, some stakeholders in the payments area – including some fintechs – have expressed the view that the introduction of another form of central bank balances could be quite transformative. They have suggested the issuance of a new form of digital money that would be accessible to businesses and could be passed around on a distributed ledger. They argue that the availability of another form of central bank settlement instrument could reduce risk and increase efficiency in business transactions. For example, it could allow the simultaneous exchange of money and other assets on blockchains. A central bank digital currency on a blockchain could potentially also enable ‘programmable money’, involving smart contracts and the simultaneous execution of complex, linked transactions.

Moving in this direction would involve two major changes to current arrangements: it would involve the introduction of a new form of settlement asset and it would presumably involve broader access to central bank money for non-bank institutions. Consideration of the first aspect will require an assessment of issues relating to the technology. Consideration of the second aspect would get into some of the issues that are relevant to thinking about giving households access to electronic central bank money, namely the implications for financial stability and the structure of the financial sector.

As we think more about a model along these lines we will be considering whether the benefits could be equally well facilitated by other means. For example, could there be commercial bank money on blockchains – say Bank X tokens, Bank Y tokens, and the like, rather than RBA digital settlement tokens? Indeed, some models have been sketched out whereby commercial banks would put aside ESA balances at the central bank or would put risk-free assets into special-purpose vehicles, and then issue credit-risk-free settlement tokens for use by their customers. We will also need to think about whether the possible use-cases that have been proposed really need central bank money on a blockchain, or if they might also be possible using other real-time payment rails – perhaps the NPP. At the moment, it does not appear that a strong case has emerged for us to provide this new form of central bank money, but we have an open mind.

CBA’s decision to distance itself from Aussie Home Loans via the bundled spin-off of its wealth management business has been labelled a “clean and timely exit” by CEO Matt Comyn.

Any conflicts of interest to be found in the ownership of Australia’s biggest mortgage brokerage by Australia’s biggest bank will soon be a thing of the past.

On Monday morning, CBA announced that it will demerge Aussie, along with several wealth management businesses such as Colonial First State, into a separate company known as CFS Group. That group will list on the ASX.

“Ultimately, we believe that they will perform better outside the Commonwealth Bank Group,” CBA chief executive Matt Comyn said.

“Aussie Home Loans [is] the leading mortgage broking franchise, and we have decided to put that inside the demerged group. It is a very successful business, over nearly 20 years, and we believe again that the best opportunities for growth and performance from Aussie Home Loans is inside the CFS Group, rather than inside the Commonwealth Bank Group.”

Mr Comyn said that a demerger, rather than a sale, offers a couple of important benefits.

“Firstly, it is a clean and timely exit of all of these businesses,” he said. “I think each of them are good businesses in their own right. We think the best chance for these businesses to perform at their potential, is outside the Commonwealth Bank Group. And CBA shareholders will receive a proportionate interest in the demerged entity, relative to their CBA shareholding. And that enables them to either participate in the growth of the CFS Group over time, or if should they prefer, they can also exit and sell on market.”

While there has been no mention of conflicts of interest or vertical integration in Mr Comyn’s statements about cutting ties with Aussie, there has been plenty of criticism over the bank’s ownership of the brokerage that no doubt weighed on an already heavily saddled CBA.

Representatives from both Aussie and CBA appeared as witnesses during the first round of the Hayne royal commission. Bank ownership of brokerages was also brought up by the Productivity Commission in its draft report on competition in financial services. The PC report concluded that the mortgage broking revolution, which disrupted the major banks in the 1990s, has failed and many brokers now act in the best interest of the banks that own them and not consumers.

“The early 2000s was the last time Australia’s financial system saw a period of fierce competition,” PC chairman Peter Harris said. “If we are to see its like again, we will need a series of policy shift, and a champion to own them.”

CBA’s decision this week may foreshadow some of the policy shifts the PC chairman has suggested, which could see changes to bank ownership of broking businesses. The PC will deliver its final report on Monday.

Meanwhile, it’s business as usual at Aussie Home Loans, according to CEO James Symond.

“Aussie Home Loans confirms CBA Group’s announcement about the planned demerger of its mortgage broking businesses along with its wealth management operations into a new, independent and separately ASX-listed company to be known as [the] CFS Group,” Mr Symond told The Adviser.

“As has been the case since we started, Aussie is committed to providing the best, independent service to our customers, ensuring they get the most suitable home loan tailored to their needs.

“While important in terms of our ultimate ownership, CBA’s announcement will not change this commitment to our customers or have any impact on the service we provide them. As a larger part of a smaller group, this opens greater opportunity for Aussie.”

This week’s announcement is the end of an era for Aussie, which sold its first 20 per cent stake to CBA back in 2008. In August last year, founder John Symond received 2.1 million of CBA shares — worth nearly $164 million — for his remaining 20 per cent stake in the brokerage.

Investment lending made up 33.5% of all housing loans, down from 33.7% the previous month, and continues to slide, as expected. However the drop in business credit meant the proportion of commercial lending fell to 32.4% of all lending.

Investment lending made up 33.5% of all housing loans, down from 33.7% the previous month, and continues to slide, as expected. However the drop in business credit meant the proportion of commercial lending fell to 32.4% of all lending. The 12 month rolling trend shows owner occupied housing still running at 7.9%, well above inflation and wage growth, while investor lending has a read of 2%, which is the lowest see since the RBA series started to be published in 1991. Have no doubt, investor lending is fading.

The 12 month rolling trend shows owner occupied housing still running at 7.9%, well above inflation and wage growth, while investor lending has a read of 2%, which is the lowest see since the RBA series started to be published in 1991. Have no doubt, investor lending is fading. Finally, the non-bank contribution to lending growth can be imputed by subtracting the APRA ADI data from the RBA market data. This is an inexact science because of timing and coverage issues across the data. But it tells an interesting story, with non-bank growth rates sitting at around 20% for owner occupied loans and around 18% for investor loans, on a twelve month rolling basis. So we can see where some of the slack in the system is being taken up as non-banks flex their muscles. Regulation of this sector is a concern, as Moody’s highlighted recently. APRA has this responsibility, but how actively they are looking at this segment of the market, when data is so hard to acquire is a moot point. My guess is they are light on.

Finally, the non-bank contribution to lending growth can be imputed by subtracting the APRA ADI data from the RBA market data. This is an inexact science because of timing and coverage issues across the data. But it tells an interesting story, with non-bank growth rates sitting at around 20% for owner occupied loans and around 18% for investor loans, on a twelve month rolling basis. So we can see where some of the slack in the system is being taken up as non-banks flex their muscles. Regulation of this sector is a concern, as Moody’s highlighted recently. APRA has this responsibility, but how actively they are looking at this segment of the market, when data is so hard to acquire is a moot point. My guess is they are light on.