Anyone who’s dug into the 2008 financial crisis knows the role that bundling and selling subprime housing loans played in bringing the world to the brink of economic collapse – out-of-control behaviors well-depicted in the movie “The Big Short.”

But one thing I hope “The Big Short” doesn’t do is further tarnish the image of subprime lending.

Despite their poor reputation, such loans remain a key tool in easing the housing affordability crisis and expanding the availability of mortgages to low-income Americans seeking to realize the dream of homeownership. They also can help policymakers cope with the growing ranks of the homeless.

I’ve been studying the world of subprime in recent years, and these are some of the lessons from my current and past research. First, we need to fix the subprime mortgage market, so that the ways in which it contributed to the financial crisis aren’t repeated.

Shocking levels of homelessness

Los Angeles, New York and other cities in America are struggling to cope with the problem of homelessness and the lack of affordable housing.

On a single night in January 2015, more than 560,000 people nationwide were homeless – meaning they slept outside, in an emergency shelter or in a transitional housing program. Almost a quarter were children. Meanwhile, homeownership is hovering at 20-year lows, while about half of renters struggle to pay their landlords.

Last fall, Los Angeles Mayor Eric Carcetti asked the City Council to declare “a state of emergency” on homelessness and committed US$100 million to solving the problem, suggesting that subsidies would play a role.

But a focus on rental subsidies to solve homelessness and other affordable housing issues has adverse consequences, as evidenced by New York’s experience.

Its cluster-site housing program, in which privately owned apartment buildings are used to house homeless families when the city’s shelters are full, relies on such subsidies. But because the city typically pays market rents (or more), many landlords responded by pushing out regular (and low-income) tenants in favor of this steady stream from the government.

Such programs reduce the overall supply of affordable units, crowding out other groups in need. As more affordable housing units are allotted to the homeless, there are fewer available for low-income residents who don’t qualify for those programs and are at risk of becoming homeless themselves.

Fortunately, Mayor Bill de Blasio aims to phase out the costly program over the next three years.

While there are many other approaches to tackling homelessness, they rely on addressing an important underlying problem: the housing affordability crisis. It may seem improbable, but subprime lending could help ease the housing affordability crisis.

The role of subprime lending

The relationship between homelessness and the strains in the housing rental market is well-known: when there are more rental vacancies available, homelessness decreases (I survey the academic findings on the topic here).

This suggests that if we reduce home affordability problems, we can effectively reduce homelessness.

A powerful tool to help ease the housing affordability crisis is subprime mortgage lending – defined as loans made to borrowers with credit scores below 640.

The idea is simple: by helping more low-income tenants qualified to take out a subprime mortgage become homeowners, there’ll be more affordable rental housing available for everyone else. More supply on the market helps reduce average rents, which in turns helps more of those pushed to the streets afford a roof over their heads with less government aid. Thus this makes the policies still based on rental subsidies more effective.

However, this idea cannot be implemented until we fix the subprime mortgage market. As you can see from the graph below, the market has not yet recovered from its collapse in 2008.

The subprime market has yet to recover from its collapse.Inside Mortgage Finance, Author provided

One of the reasons the market collapsed was that investors lost confidence in the ability of loan originators and regulators to use credit scoring models to accurately assess a borrower’s creditworthiness – remember the NINJA loans (no income, no job, no assets)?

This market won’t be back up and running at full strength – and able to help address the affordability crisis – until these credit-scoring models improve and mechanisms are put in place to ensure loan quality remains adequate.

The FHFA sets new goals

There has been some movement to get the subprime market moving again.

The Federal Housing Finance Agency (FHFA), an independent federal agency that regulates Fannie Mae, Freddie Mac and the 12 Federal Home Loan Banks, recently set goals for the next two years meant to expand the availability of mortgages to low-income buyers.

This policy will keep its focus on helping a small segment of borrowers with incomes no greater than 50 percent of their area’s median income to purchase or refinance a single-family home.

But many affordable housing advocates expressed concern that these targets do not go far enough. The Woodstock Institute – a leading research and policy nonprofit organization focused on fair lending, wealth creation and financial systems reform – for example, argued that the policy won’t do enough to promote affordable and sustainable home ownership for low-income families.

How to bring back subprime

Even with the FHFA embracing the idea of expanding the availability of subprime mortgages to low-income buyers, their perceived role in the 2008 crisis and bringing down the housing market may cause justifiable resistance from the general public as a means of tackling the affordability crisis.

And one cannot blame this reaction, as it was the average American taxpayer who bailed out the reckless financial system, brought down by greedy bankers and weak politicians and regulators.

So how we can encourage more subprime lending while avoiding a repeat of 2008? In my recent research, I suggest a few ways to do this.

One of the reasons subprime loans became such a problem in the run-up to the crisis is just the sheer volume (see the boom in subprime lending from 2001 to 2005 in the above graph). This expansion was fueled by the generous homeownership subsidies given to low-income households.

One way to help prevent this is to vary the size of the homeownership subsidy countercyclically to control the amount of credit flowing into the economy and prevent overborrowing during expansionary periods. It would be higher at times when the housing market contracts, and lower when it’s booming.

Another problem was that lenders had an incentive to originate mortgages to borrowers who couldn’t afford them because all the risk was passed along to banks and other investors through collateralized mortgage obligations (CMO) and other sophisticated financial instruments.

The Federal Reserve in conjunction with other regulators could reduce this risk by carefully monitoring how many mortgages lenders keep in their own portfolios. When the share lenders hold increases, they have more incentives to better screen borrowers and thus originate better mortgages.

Lastly, the so-called adverse selection problem on the part of the mortgage originator in the secondary market should also be taken into account. This problem occurs when the mortgage originator has more information about the quality of mortgages that are securitized than the secondary market investors who snap up the CMO. That allows the originator to keep the low-risk mortgages in its own portfolio while distributing the high-risk mortgages to investors.

Improving existing credit scoring models is crucial to ameliorating this problem. Also, the Fed should more carefully monitor the quality of mortgages that are sold to investors and share its information with them. At the very least, that would reduce the investors’ information disadvantage with respect to originators.

Accompanied by the right means to regulate the housing market, we can support subprime while avoiding the disastrous outcomes highlighted in “The Big Short.“ And we can create an environment in which making low-cost mortgages available to people helps resolve the problem of unaffordable housing and homelessness.

Author: Jaime Luque, Assistant Professor, Real Estate & Urban Land Economics, University of Wisconsin-Madison

Governor Lael Brainard, spoke at the 2016 U.S. Monetary Policy Forum, New York, New York. The speech highlighted that whilst there was a phase when different economic centres were diverging, now there are more common elements, including low growth, low interest rates and low inflation. Global shocks are being transmitted via the financial system, creating volatility and spillover effects.

To the extent that we are observing limited divergence in inflation outcomes and less divergence in realized policy paths than many anticipated, this could be attributable to common shocks or trends that cause economic conditions to be synchronized across economies. The sharp repeated declines in the price of oil have been a major common factor depressing headline inflation and are also likely feeding into low core inflation, although to a lesser extent. As noted previously, these price declines have led headline inflation across the globe to behave quite similarly over this time period. Even so, most observers expect this source of convergence in inflationary outcomes to eventually fade and thereafter not affect monetary policy paths over the medium term.

In contrast, a more persistent source of convergence may be found in an apparent decline in the neutral rate of interest. The neutral rate of interest–or the rate of interest consistent with the economy remaining at its potential rate of output and inflation remaining at target level–appears to have declined over the past 30 years in the United States and is now at historically low levels. Similarly, longer-run interest rates appear also to have fallen across a broad group of advanced and emerging market economies, suggesting that neutral rates are at historically low levels in many countries around the world and near or below zero in the major advanced foreign economies. Although the reasons for the declines in neutral rates are not perfectly understood and may differ across countries, there are some common drivers, such as slower productivity and labor force growth and a heightened sensitivity to risk.

The very low levels of the shorter run neutral rate reflect in part headwinds from the crisis that are likely to dissipate over time. However, if many of the common forces holding down neutral rates prove persistent, then neutral rates may remain low through the medium term, implying a shallower path for policy trajectories.

The global economy is also experiencing a downshift in emerging market growth momentum led by China, which may prove somewhat persistent. Whereas earlier in the recovery there was a striking divergence between the relatively buoyant growth in major emerging economies and depressed growth in advanced economies, lately the extent of divergence has diminished noticeably. China is undergoing a challenging set of economic transitions. Trend growth has slowed substantially and is expected to slow further, and the composition of growth is shifting away from resource-intensive manufacturing and exports toward a greater share for consumption and services. China’s investment has slowed sharply recently after accounting for nearly one-third of global investment over the past three years and about one-half of global consumption in certain metals such as iron ore, aluminum, copper, and nickel. Commodity exporters and close trading partners in Asia will be most affected, but the changes in the composition and rate of growth in a country that has accounted for about one-third of the growth in world output and trade will likely ripple through the global economy much more generally.

Amplified Spillovers

Of course, policy divergence among major economies could be limited by rapid and strong transmission of foreign shocks across borders. In particular, although the U.S. real economy has traditionally been seen as more insulated from foreign trade shocks than many smaller economies, the combination of the highly global role of the dollar and U.S. financial markets and the proximity to the zero lower bound may be amplifying spillovers from foreign financial conditions. By one rough estimate, accounting for the net effect of exchange rate appreciation and changes in equity valuations and long term yields, over the past year and a half, the United States has experienced a tightening of financial conditions that is the equivalent of an additional increase of over 75 basis points in the federal funds rate.10

The transmission of divergent economic conditions across borders typically occurs though a couple of different channels. First, a decline in demand in one country reduces its demand for imports from other countries. Second, the fall in economic activity would be expected to trigger a more accommodative monetary policy, which helps offset the effect of the shock by both supporting domestic demand and weakening the exchange rate. The weaker exchange rate in turn leads domestic consumers to switch their expenditures away from more expensive foreign imports to cheaper domestic products while increasing the competitiveness of exports. The extent to which monetary policy offsets the shock by dispersing it to trade partners as opposed to strengthening domestic demand depends on the responsiveness of domestic demand relative to the exchange rate. The exchange rate channel, by raising the price of imports in domestic currency, also pushes up domestic inflation and exerts downward pressure on foreign inflation.

The strength of spillovers across countries and the extent to which that affects policy divergence across countries depend on a foreign economy’s openness to these different channels. The recent experience of Sweden suggests that for highly open economies, the effect of foreign shocks can be extremely powerful. Sweden’s economic growth has been relatively rapid recently, reaching nearly 4 percent over the most recent four quarters. Moreover, the employment gap is estimated to be nearly closed, and there are signs of financial excess in the housing market. In ordinary times, these conditions would be consistent with relatively tight monetary policy. However, inflation has run persistently well below the central bank’s 2 percent inflation target. Given the relative openness of Sweden’s economy, moving the inflation rate back up to target has been greatly complicated by the sensitivity of Sweden’s exchange rate and financial conditions to developments in the euro area, where domestic economic conditions are consistent with much more accommodative policy. As a result, the Riksbank has been pursuing extremely accommodative monetary policy, most recently lowering the interest rate on deposits to minus 0.5 percent and authorizing the Governor and Deputy Governor to intervene in foreign currency markets.

Even in the much larger United States economy, with imports accounting for a little over 15 percent of gross domestic product (GDP), spillovers can be quite strong, in part reflecting the international role of U.S. financial markets and the dollar. Since the middle of 2014, with a reassessment of demand growth in the euro area and subsequently in emerging markets and other commodity exporters, the real trade-weighted value of the dollar has increased nearly 20 percent. As a result, in 2014 and 2015, net exports subtracted a little over 1/2 percentage point from GDP growth each year, and econometric models point to a subtraction of a further 1 percentage point this year.12 In addition, the dollar’s appreciation is estimated to have put significant downward pressure on inflation: Non-oil import prices fell 3-1/2 percent in 2015, subtracting an estimated 1/2 percentage point from core PCE inflation.

Financial channels can powerfully propagate negative shocks in one market by catalyzing a broader reassessment of risks and increases in risk spreads across many financial markets. Since the beginning of the year, U.S. financial markets have reacted strongly to adverse news on emerging market growth, even though the news on the U.S. labor market has remained positive. In this regard, although China’s direct imports from the United States are modest, uncertainty about changes to its exchange rate system and financial imbalances, together with changes in the composition of its growth, have had broader global spillovers that may pose risks to the U.S. outlook.

Recent events suggest the transmission of foreign shocks can take place extremely quickly such that financial markets anticipate and indeed may thereby front-run the expected monetary policy reactions to these developments. It also appears that the exchange rate channel may have played a particularly important role recently in transmitting economic and financial developments across national borders. Indeed, recent research suggests that financial transmission is likely to be amplified in economies with near-zero interest rates, such that anticipated monetary policy adjustments in one economy may contribute more to a shifting of demand across borders than a boost to overall demand. This finding could explain why the sensitivity of exchange rate movements to economic news and to changes in foreign monetary policy appear to have been relatively elevated recently.

Financial tightening associated with cross-border spillovers may be limiting the extent to which U.S. policy diverges from major economies. As policy adjusts to the evolution of the data, the combination of heightened spillovers from weaker foreign economies, along with a lower neutral rate, could result in a lower policy path in the United States relative to what many had predicted.

Policy

In circumstances where many economies face common negative shocks or where negative shocks in one country are quickly transmitted across borders, it is natural to consider whether coordination can improve outcomes. Under certain conditions–such as flexible exchange rates, deep and well-regulated financial markets, and flexible product and labor markets–policies designed for the domestic economy can readily offset any spillovers from economic conditions abroad, and policies designed to address domestic conditions can achieve desirable outcomes both within the national economy and more broadly.

In some circumstances, however, cooperation can be quite helpful. If, for example, economies face a common challenge, coordination can communicate to markets that policymakers recognize the challenge and will work to address it. Reducing uncertainty about the direction of policy and addressing concerns about policies working at cross-purposes can boost the confidence of businesses and households. With intensified transmission effects in the vicinity of the zero lower bound, there is a risk that uncoordinated policy on its own could have the effect of shifting demand across borders rather than addressing the underlying weakness in global demand. The difficult start to the year should be a prompt for greater policy coherence and clarity. This might be a good time for policymakers to reaffirm their commitment to work toward the common goal of strengthening global demand.

Similarly, with anemic global demand and interest rates near zero, in some economies there is scope for monetary policy to be more effective with fiscal policy working in the same direction. With potential growth and nominal borrowing rates both low, public investment that increases potential in the longer run and demand in the shorter run could make an important contribution. A joint determination by policymakers across major economies to better deploy policy tools to provide support for global demand could be beneficial.

The Mortgage and Finance Association of Australia (MFAA) has branded a report in the Australian Financial Review (AFR) – which questions the ethics of mortgage brokers and likened some to a Ponzi scheme – as a “serious allegation”.

The AFR report, titled ‘Uncovering the big Aussie short’ claims mortgage brokers in the western suburbs of Sydney encouraged the undercover hedge-fund manager and economist posing as a low income couple to lie on loan application documents about the deposit for a house and about income.

Jonathan Tepper, economist and founder of Variant Perception, wrote in a report, “we asked if the bank would call our employer, and both reputable and disreputable brokers said banks rarely verified payslips”.

John Hempton, Bronte Capital’s chief investment officer added that they were also told the checking of documents was sometimes done by Indian call centres.

Tepper and Hempton also claimed they encountered many investors who were able to get revaluations on their properties to increase their equity for speculative purposes.

According to Hempton, in north-western Sydney they met one mortgage broker who told them which of the big four banks would revalue properties quickly.

“They wanted to put you in 10 to 15 apartments. The only way they could do that was getting the bank to revalue the property so you could borrow more money. They were acute about which banks had bad practices,” the AFR report quotes Hempton.

Siobhan Hayden, the chief executive of the MFAA, says this sort of behaviour has no place in the mortgage broking industry and she is calling on the AFR to provide the names of the offending brokers.

“The practices of brokers are well documented and require the provision of supporting upfront documents such as payslips, group certificates, tax returns and identification check as part of the upfront application. Lying has no place in this industry and we take swift action if members are acting unethically. It should also be noted that brokers who act outside of the law represent an incredibly small portion of the industry,” Hayden said.

“We call on the AFR or the research firm provides the names of these mortgage brokers, as the MFAA has a strict code of practice and ethics attached to its membership. If these are MFAA members we would initiate a full investigation and work in partnership with the industry regulator, ASIC.”

She is also condemning the authors of the report, Tepper and Hempton, as well as the AFR for not seeking out either industry body for comment.

“We would have hoped that with any story of this nature the industry body would have been contacted to seek commentary and supporting data for validation. The article is based on invalid research samples sizes and infers that overseas outsourcing of administration is somehow inferior. Both sides of the story should be told.”

Hayden also pointed to the ‘Observations on the value of mortgage broking’ report, commissioned by the MFAA and prepared by Ernst & Young, which showed that 92% of consumers who had used a broker were satisfied with the experience, stating that the convenience and access to a range of suitable deals were the best qualities.

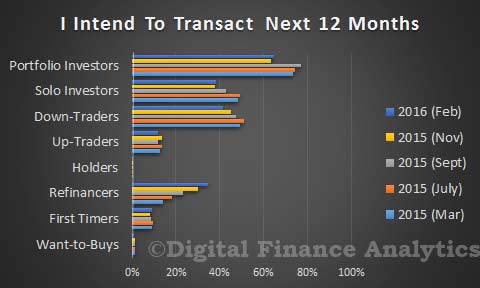

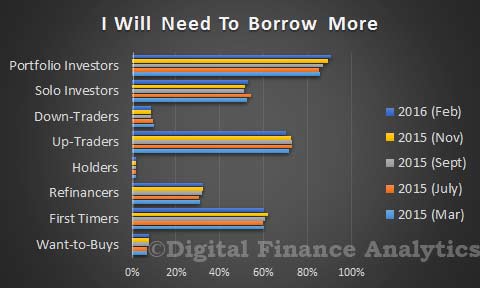

The latest results from the Digital Finance Analytic Household Surveys are in, and demand has recovered somewhat after the wobble late last year. Worth also remembering that Sirens were dangerous yet beautiful creatures, who lured nearby sailors with their enchanting music and voices to shipwreck on the rocky coast of their island! Over the next few days we will present the summary results, using our household segmentation, and examine why property remains so alluring despite being in bubble territory.

By way of background, we are using data from our rolling 26,000 household data set, the most recent data is up to 20th February 2016, so this captures the state of play after the recent stock market and resource sector ructions. Today we will overview some of the main cross-segment data, and in later posts dive into more detailed analysis of specific segment behaviour. These results will then flow into the next edition of the Property Imperative – the last edition is still available from September 2015, and the new edition will be out in March.

We start with transaction intentions. The most significant move is the rise in those expecting to refinance their existing mortgage, from 29% last time to 34% now. This despite record refinance volumes which have already been written. We found that many households were reacting to the strong discounts available for existing borrowers, especially with loan-to-value ratios below 80%. Three quarters of these households will use a broker, so no surprise we see brokers volumes on the rise. First time buyers are still in the market, from 8.2% to 8.9% this time. Property investors, whether holding a portfolio of properties, or just one, are still in the market, despite the rise in interest rates for investment loans, and tighter lending criteria. Portfolio investors moved form 63% to 64% this time, whilst solo investors moved from 37% to 38%. Up traders and down traders are a little less inclined to transact, whilst those wanting to buy, but who cannot, remain on the sidelines.

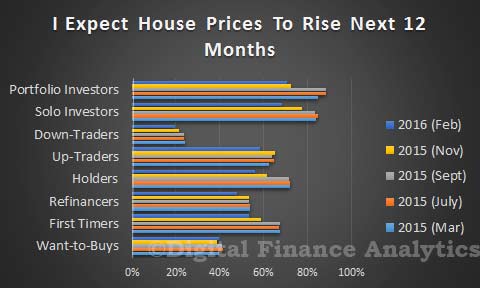

House price rise expectations are still quite strong, though lower than at their peak last year. More than half of property investors still think the market will go higher in the next 12 months. Down traders are the least optimistic with only 20% expecting further price hikes. First time buyers are still bullish, with 53% expecting a rise, though a fall from 67% last year.

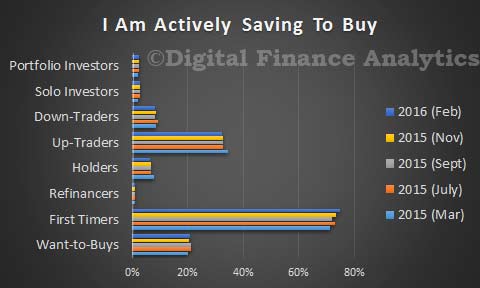

Savings behaviour has not changed that much, with first time buyers still saving the hardest. Some of those wanting to buy are also saving, but it continues to sit at around 20%.

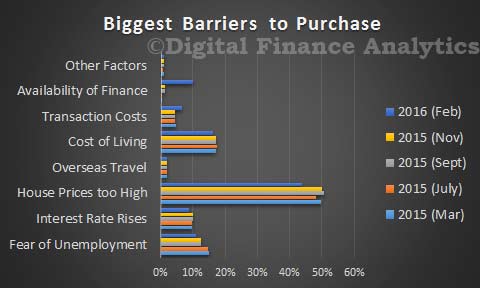

Of note is the significant rise in households who say that availability of finance is now a barrier to transacting, with nearly 10% saying finding a loan is now a problem compared with just 1.5% last year. Of course house prices remains high, so 43% say this is a barrier to transacting, down from 49% last year. On the other hand, unemployment fears are down compared with last year, down from 15% to 11%.

Prospective purchasers are still looking for finance, with investors and first time buyers seeking to borrow more. Around 15% of those refinancing will look to increase the size of their loan, which explains some of the ongoing loan portfolio growth noted in recent statistics.

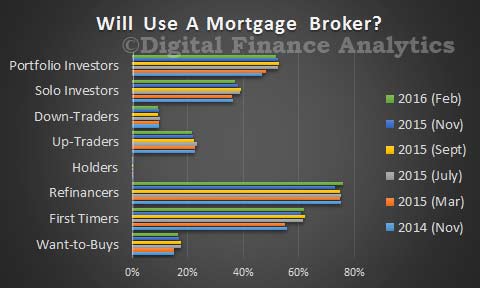

Finally, in this over view, we note the importance of mortgage brokers as noted in the recent APRA data, with first time buyers and those seeking to refinance the most likely to consult a broker. Investors are also still broker aligned, especially portfolio investors.

So, the expectations are for ongoing demand for property still to be strong, and refinance volumes will remain elevated. Banks are competing hard to offer deep discounts for owner occupied loans. Next time we will look in more detail at first time buyers, and then those seeking to refinance.

Research from the USA highlights the fact that when house prices fall, and household debt is high, the rise in defaults is more correlated to the number of households falling behind in their mortgage payments that the debts of those already in default.

The large decrease in US house prices between 2006 and 2011 led to a dramatic increase in mortgage debt defaults. Since then, the share of mortgage debt in default has decreased significantly and is now close to the pre-2006 level. In this essay, we argue that these fluctuations are predominantly the consequence of changes in the number of households falling behind in their mortgage payments (the extensive margin) and not changes in the amount of debt of those in default (the intensive margin). On average, the extensive margin accounts for 78 percent of the increase in the 2006-09 period and 93 percent of the decrease in the 2011-15 period. This information may be useful in designing prudential policies to mitigate mortgage default.

The analysis is performed using data from the Federal Reserve Bank of New York Consumer Credit Panel/Equifax. In our measure of default, we consider all households with mortgage payments 120 or more days late. Figure 1 shows the share of mortgage debt in default, which fluctuated between 0.7 percent and 1 percent in the 1999-2006 period and then jumped to 7.5 percent in 2009. The figure also shows the evolution of house prices, whose collapse coincided with increasing mortgage defaults. In a recent article, Hatchondo, Martinez, and Sánchez (2015) show how these two series are related: A rapid decrease in house prices causes a sharp increase in mortgage defaults because more households find themselves with negative home equity (“under water”), and some of these households find it beneficial to default after a negative shock to income (i.e., unemployment).

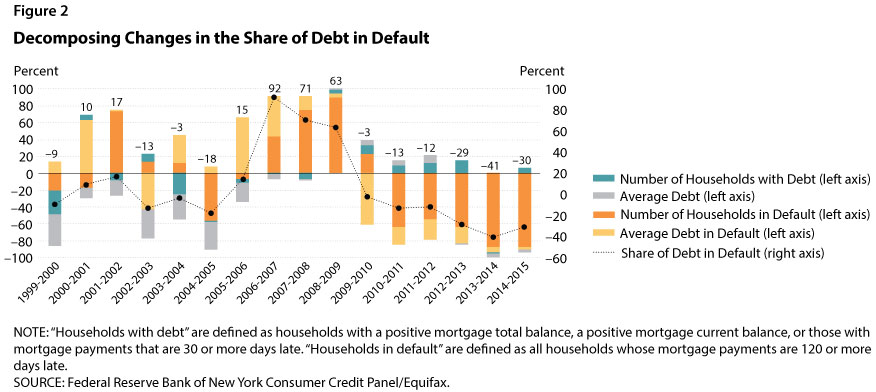

We decompose the changes in the share of debt in default into changes in four different components: average debt in default, number of households in default, average debt, and number of households with debt. Basically, since

we can compute the percentage change (%∆) in the share of debt in default as follows:

Figure 2 shows the results of the decomposition by year; the four colors in each column represent the changes in the four components. The percentage value (shown on the left vertical axis) illustrates the change in the share of debt in default generated by the changes in a particular component. According to the previous equations, the summation of changes in the four components equals the changes in the share of debt in default (represented by the values for the black dots as shown on the right axis). For example, the black dot for 2006-07 has a value of 92, which indicates that the share of debt in default increased by 92 percent in that time period.

There are three interesting findings. First, and most importantly, we find that fluctuations in the number of households in default accounted for most of the fluctuations in the share of debt in default (shown by the size of the orange part of the bars in Figure 2). The share of households in default was very large not only for the years when defaults were increasing (2006 to 2009), but also for the subsequent years when the share of debt in default decreased slowly but steadily. The changes in the number of households in default confirm our earlier claim that the drastic decline in house prices between 2006 and 2009 caused negative home equity for more households. For some of these households a negative income shock triggered default, thus leading to the sharp increase in mortgage debt default. Another reason for this pattern is the delay in foreclosure proceedings that started during the Great Recession. Chan et al. (2015) show that borrowers’ knowledge of a possible long delay between the formal notice of foreclosure and the actual foreclosure sale date affects the likelihood of default: Borrowers who anticipate a longer period of “free rent” have a greater incentive to default on their mortgages.

Second, our results indicate that from 2003 to 2007 the average amount of debt (the gray part of the bars in Figure 2) exerted downward pressure on the share of debt in default. That is, since the average amount of debt was increasing, if the other three components had not increased, the share of debt in default would have decreased.

Finally, we find that the average amount of debt in default (the yellow part of the bars in Figure 2) was important in the 2006-08 period. This finding indicates that part of the increase in the share of debt in default during that period was actually due to an increase in the amount of the debt of households in default. This increase is in line with the fact that the decline in house prices affected households with larger debt (not necessarily subprime loans) that were not falling into default before 2006. When house prices plummeted in 2006, more households from this group defaulted. Later in the recession, the importance of the average amount of debt was overtaken by the number of households in default as more and more households with similar characteristics chose to default.

To summarize, the rapid increases in mortgage debt in default between 2006 and 2011 captured the attention of the public, policymakers, and researchers. It is important to understand the main forces driving the default increase, especially in designing prudential policies that minimize mortgage default such as those analyzed by Hatchondo, Martinez, and Sánchez (2015). The decomposition exercise in this essay suggests that the evolution of the share of mortgage debt in default can be accounted for mostly by changes in the number of households in default rather than changes in the overall amount of mortgage debt and the number of households with mortgages. Changes in the amount of debt in default also played a nonnegligible role, especially during the pre-crisis to early crisis periods.

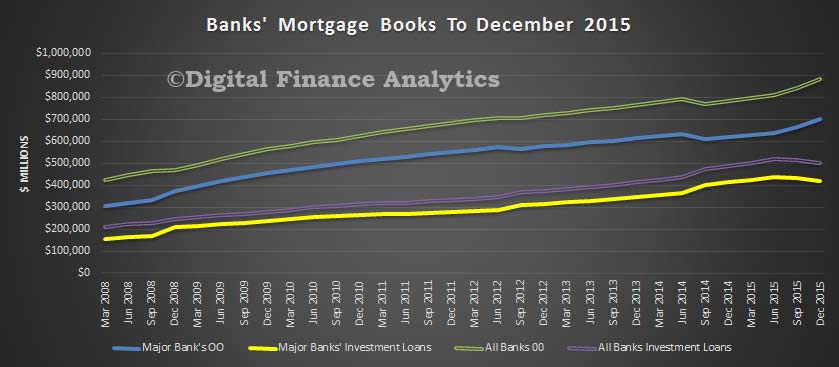

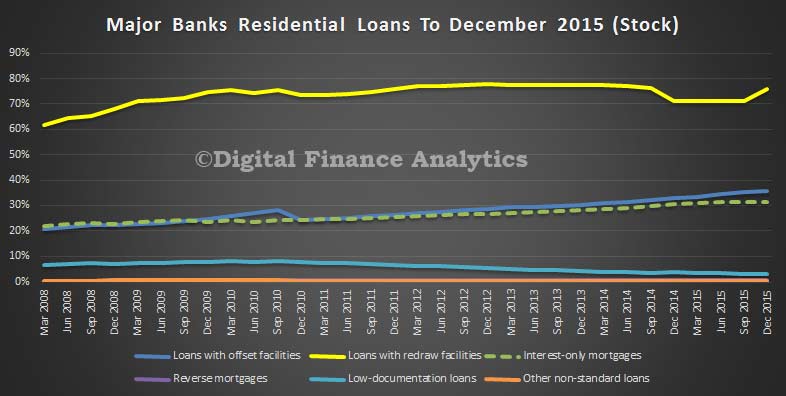

APRA has released the quarterly real estate data for the banks in Australia to December 2015. There are some strong signs that the regulatory intervention has changed the profile of loans being written, despite overall significant growth in loan balances on book.

Total loans on book to December were a record $1.38 trillion, of which $1.12 trillion – or 80% are with the big four. Within that, 36% of loans were for investment purposes, the remainder owner occupied loans. The trend shows the significant rise in owner occupied loans being written (explained by a rise in refinances), whilst investment loans have fallen. This is a direct response to the regulators intervention. But note, total loans on book are still rising.

Because the big four have the lions share of the market, the rest of the analysis will look at their portfolio in more detail. For example, looking at loan stock, we see a rise in the proportion of loans with a re-draw facility (75.7%), Loan with offsets continue to rise, reaching 35.8% and interest only loans have slipped slightly to 31.4%, another demonstration of regulator intervention (they have asked banks to tighten their lending criteria and ensure consideration of repayment options for interest only loans). Reverse mortgages remain static as a percentage of book (0.6%), and low-doc loans continue to fall (2.9%).

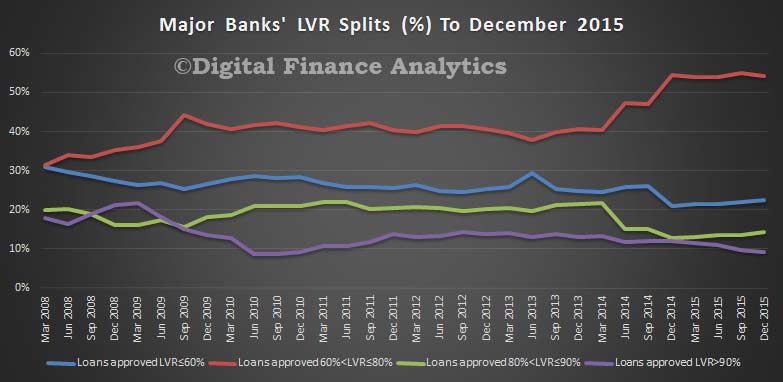

The loan to value mix has changed, again thanks to regulatory guidance, with the proportion of new loans above 90% LVR falling to 9.1%, from a high of 21.6% in 2009. Loans with an LVR of between 80% and 90% have fallen to 14.2%, from a high of 22% in 2011. Once again, we see a change in the mix thanks to regulatory guidance, and also thanks to a lift in refinance of existing loans, which tend to have a lower LVR. The portfolios are being de-risked.

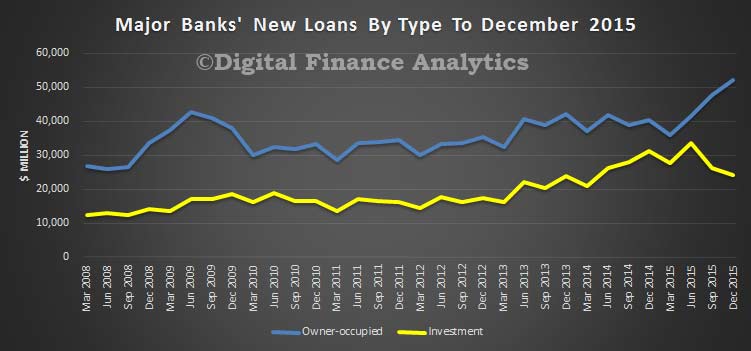

Another demonstration of de-risking is the lift in new owner occupied loans, and a fall in investment loans to 31.7% of new loans written.

If we look at interest only loans, we see a fall to 39.5% of new loans written (the high was 47.8% just 6 months before), so we see the hand of the regulator in play. However 3.7% of loans were outside normal serviceability guidelines, just off its peak in June 2015. Finally, 47.4% of new loans have been originated from the broker channel, another record. This is also true for all banks, and it shows that brokers are doing well in the new owner-occupied and refinance ridden environment.

So, overall, make no mistake home lending is still growing, despite regulatory guidance, thanks to the rise in owner occupied loans. This means that the banks will be able to continue to grow their books, and maintain their profitability. No surprise then that the big four are all fighting hard for new OO loans, and are discounting heavily to write business. It is too soon to judge whether the portfolios have really been de-risked, given the sky high household debt this represents, and a potential funding crunch the banks are facing.

In a Speech “The Evolving Risk Environment”, Malcolm Edey RBA Assistant Governor (Financial System) discussed some of the risks to financial stability, both globally and locally.

Much of the story has been told before, the economic uncertainties surrounding oil, China, Europe, high debt levels and locally the risks (and how they have been controlled) in the housing market, and potential risks in the commercial property sector.

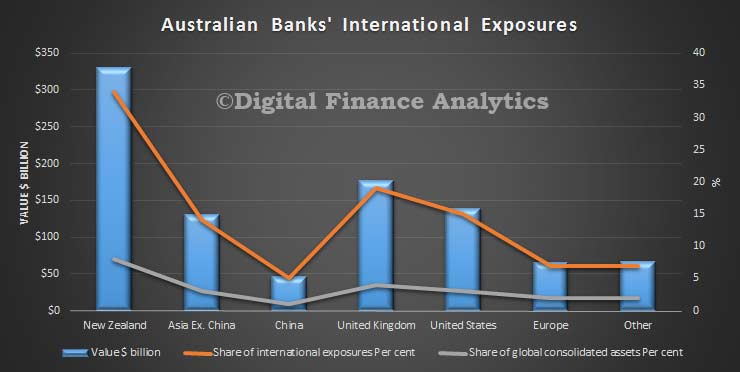

One specific issue he covered was the potential international exposures Australian banks may face. He focussed specifically on the assets Australian banks hold overseas.

Direct exposures of Australian banking institutions to the risk factors I have been describing are quite limited Exposures to the euro area have been scaled back in the wake of the crisis and now represent only around 1 to 2 per cent of Australian banks’ consolidated global assets. Although exposures to the Asian region have been growing quite rapidly over recent years, they are still a relatively small share of consolidated assets – around 4 per cent. Many of these exposures are shorter-term and trade-related, factors that should lessen credit and funding risks. That said, operational and legal risks around these exposures could be relatively high, particularly given the rapid expansion of these activities in recent times.

Fair point. However, there are two other exposures to also consider. First banks here are funding their lending partly via capital markets overseas, because there is a gap between the value of deposits held and loans made. Different banks have different footprints. But this means if the international capital markets froze for any reason this would be a significant risk locally. This was demonstrated during the GFC. In any case, in the current environment, spreads are rising, and funding is becoming more expensive. To an extent, given limited competition here, they can just raise rates to customers. But there will be some limits. Recently we have seen a number of lifts in some mortgage rates and to the SME sector.

The other exposure is from international investors and fund managers who invest in the shares of the banks here, and who are also thinking about risk profiles, local economic performance and other factors. We often get asked to provide a picture of things here by such investors. They will consider levels of returns and risks implicit in these returns. Given that going forwards, it is likely banks will find it harder to maintain current dividends than in the past, we may see a change in the wind here too. If international investors were to jump ship, expect market prices to fall.

So, my simple point is that banks are exposed to global forces, well beyond those risks of default on loans, and these additional should be factored into discussions of financial stability.

I would also highlight that not all banks are equally exposed, as underscored by the batch of results declared in the past couple of weeks.

The first few months of a new year can be a stressful time financially. The Christmas holidays typically lead to depleted savings and higher credit card balances, while tax season is right around the corner.

Unfortunately for most us, this isn’t a seasonal dilemma but a chronic problem that brings anxiety throughout the year.

Indeed, as many as 44 percent of American households don’t have enough savings to cover basic expenses for even three months. Without a savings cushion, even regular seasonal expenses like holiday celebrations may end up feeling “unexpected” and lead households to turn to credit to cover costs.

U.S. consumers currently hold US$880 billion in revolving debt, with an average credit card balance of almost $6,000. The picture is even more dire for lower-income households.

So how can we turn this around? Many tacks have been tried but fallen short for one reason or another. Fortunately, behavioral science offers some useful insights, as our research shows.

What’s wrong with current approaches

Typical approaches to solving problematic finances are either to “educate” people about the need to save more or to “incentivize” savings with monetary rewards.

But when we look at traditional financial education and counseling programs, they have had virtually no long-term impact on behavior. Similarly, matched savings programs are expensive and have shown mixed results on savings rates. Furthermore, these approaches often prioritize the need for savings while treating debt repayment as a secondary concern.

Education and incentives haven’t worked because they are based on problematic assumptions about lower-income consumers that turn out to be false.

They also don’t need to be convinced of the value of saving. Many want to save but face additional obstacles to financial health.

For example, these households often face uncertainty about their cash flows, making planning for expenses even more difficult. More generally, they have little room for error in their budgets and the costs of small mistakes can compound rapidly.

Brain barriers

In this volatile context, psychological barriers common to all people exacerbate the problem.

People have difficulty thinking about the future. We treat our future, older selves as if they are strangers, decreasing motivation to make tradeoffs in the present. Additionally, we underpredict future expenses, leading us to spend more than precise budgeting can account for.

When we do focus on the future, people have a hard time figuring out which financial goals to tackle.

In research that we conducted with Rourke O’Brien of the University of Wisconsin, we found that consumers often focus either on saving money or on repaying debt. In reality, both actions simultaneously interact, contributing to overall financial health.

This can be problematic when people misguidedly take on high-interest debt while holding money in low-interest saving accounts at the same time. And, once people have identified building savings or repaying debt as an important goal, they have difficulty identifying how much should be put toward it each month. As a result, they rely on information in the environment to help determine this amount (like getting “anchored” on specific numbers that are presented as suggestions on credit card payment statements).

Unfortunately, the way current banking products are designed often makes these psychological realities worse.

For example, the information on many credit card payment systems nudges consumers toward paying the minimum balance rather than a higher amount. Budgeting tools assume income and expenses stay the same from month to month (not true for most lower-wage workers) and expect us to monitor spending against a long list of separate, complicated budget categories.

On a deeper level, the fact that banks offer credit and savings products separately exacerbates the psychological distance between paying down debt and building savings, even though these are linked behaviors.

Behavioral banking

The good news is that a range of simple, behaviorally informed solutions can easily be deployed to tackle these problems, from policy innovations to product redesign.

For instance, changing the “suggested payoff” in credit card statements for targeted segments (i.e., those who were already paying in full) could help consumers more effectively pay down debt, as could allowing tax refunds to be directly applied toward debt repayment. Well-designed budgeting tools that leverage financial technology could be integrated into government programs. The state of California, for example, is currently exploring ways to implement such technologies across a variety of platforms.

But the public and private sectors both need to play a role for these tools to be effective. Creating an integrated credit-and-saving product, for example, would require buy-in from regulators along with financial providers.

While these banking solutions may not close the economic inequality gap on their own, behaviorally informed design shifts can be the missing piece of the puzzle in these efforts to fix major problems.

Our research indicates that people already want to be doing a better job with their finances; we just need to make it a little less difficult for them. And making small changes to banking products can go a long way in helping people stabilize their finances so they can focus on other aspects of their lives.

Authors: Hal Hershfiel, Assistant Professor of Marketing, University of California, Los Angeles; Abigail Sussma, Assistant Professor of Marketing, University of Chicago.

In a speech to the Institute of Chartered Accountants of Scotland on 11 February, Dame Clara examines the UK’s position as host to a global financial centre through the lens of the Financial Policy Committee’s two main objectives: its primary objective to maintain financial stability, and its secondary objective to support the Government’s economic policy, including its objectives for growth and employment; productive investment, innovation, competition and the lead role of the City of London in international financial markets.

In the context of financial “de-globalisation” and sharply falling cross-border capital flows, Dame Clara believes that now is a good time to consider the benefits of global markets and financial centres. Historically, Dame Clara notes, the development of global financial centres went hand-in-hand with the integration of international capital markets, because a more complete market can allocate capital with much greater efficiency.

According to an IMF staff discussion note, financial development increases a country’s resilience; mobilises savings, promotes information sharing, improves resource allocation and facilitates diversification and management of risk. It also promotes financial stability to the extent that deep and liquid financial systems with diverse instruments help dampen the impact of shocks.

But at the same time, financial deepening and connected markets can transmit shocks as well as dispersing and absorbing risk and driving growth. “Overall, however, with the right policy framework, choices and institutions, it seems clear that the benefits of financial globalisation are compelling,” Dame Clara observes.

Next, Dame Clara considers why global centres are needed, when advances in technology have made it feasible for the financial system to become decentralised.

On reason why it is good to be global is that a specialised financial centre can yield “agglomeration benefits” – the economies of scale arising from having an industry cluster in a particular location – and which can also improve access to finance for households and businesses.

Another benefit of centralisation is that it allows the authorities to see more. “The more that activity clusters in a small number of centres, the more that regulators and policymakers can take a holistic, systemic view of threats to financial stability,” Dame Clara says.

In the UK context, there are also economic benefits in being a global financial centre. “While the primary objective of financial stability is paramount for the FPC, the UK clearly has an interest in maintaining its strong position as a provider of these services. Provided the financial sector remains resilient – and our new regulatory framework seeks to ensure that it does – this is central to the FPC’s secondary objective.”

Following on from this, Dame Clara considers the conditions for the success or failure of financial centres. Looking back over time, she observes that while financial centres have tended to cluster around centres of economic power, they can remain in place and prosper even after economic power has shifted elsewhere.

“The UK has maintained its position right into this century, even though the days in which Britain was the dominant superpower are long gone.”

That said, the decline of a financial centre can be precipitated by an adverse event, such as war or a policy error that makes the continued provision of financial services impossible, uneconomic or simply destroys confidence in it. As such, one lesson to be drawn from history is that policy choices and institutions matter.

Looking forward, proximity to power may be less important for financial centres such as the UK, thanks to advances in communications technology. However, because moving is easier than it was in centuries past, the same factors that mean the UK can serve the world, allow for a wide range of alternative centres to become established, possibly leading to a decentralisation and fragmentation of the financial system. This would undermine the efficiency of global capital markets and harm global growth.

“To avoid this, authorities need to remain alert to shocks, including those arising from the geopolitical and wider macrofinancial environment, as well as the more ‘bread and butter’ risks that are visible on banks’ balance sheets. This is where the FPC can play an important role,” according to Dame Clara.

An environment where geography and sheer economic scale matter less, means that institutions may matter even more. “We need a clear, prudent, proportionate system of regulation, which is sensitive to the different risks and opportunities posed by different kinds of activity,” Dame Clara says.

Dame Clara concludes that: “International and global financial centres have historically played a crucial role in promoting both growth and stability. But policymakers cannot take their existence for granted. In a world where institutions and policy choices matter more than ever, a prudent and proportionate regulatory framework is essential to sustainable growth. That is what we on the FPC are seeking to achieve.

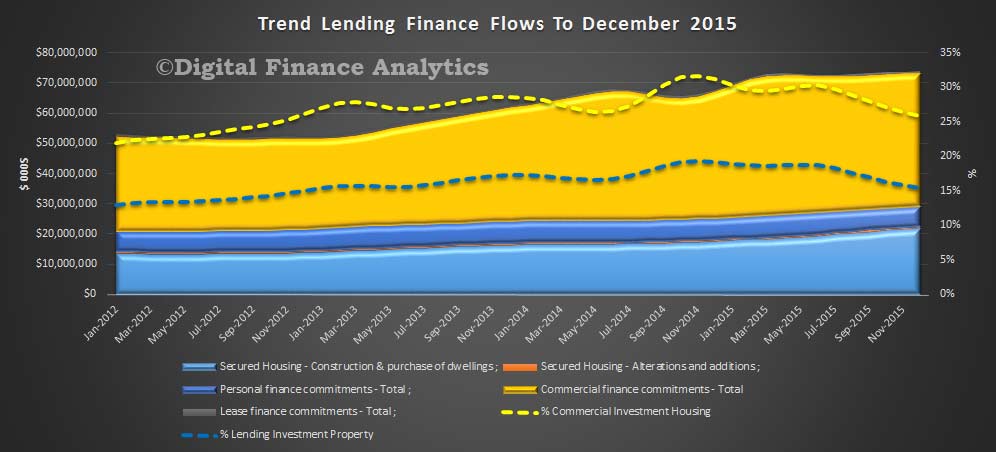

The ABS data to December 2015 of total lending by category shows that the total flow value of owner occupied housing commitments excluding alterations and additions rose 1.3% in trend terms (to $21.9 bn), and the seasonally adjusted series rose 0.9%.

The trend series for the value of total personal finance commitments fell 0.7% (to $6.9 bn). Fixed lending commitments fell 1.0% and revolving credit commitments fell 0.3%. The seasonally adjusted series for the value of total personal finance commitments rose 2.1%. Fixed lending commitments rose 2.6% and revolving credit commitments rose 1.5%.

The trend series for the value of total commercial finance commitments fell 0.3% (to $44.1 bn). Revolving credit commitments rose 2.4%, while Fixed lending commitments fell 1.2%. The seasonally adjusted series for the value of total commercial finance commitments fell 7.3%. Revolving credit commitments fell 18.3% and fixed lending commitments fell 3.3%.

The trend series for the value of total lease finance commitments rose 0.1% in December 2015 (to $602m) and the seasonally adjusted series rose 1.7%, after a fall of 3.8% in November 2015.

Commercial finance includes lending to individuals and other for investment property purchase. We see that lending for investment property purchase slid to 15% of all lending in December, having reached a high of nearly 20% in late 2014. In addition, the proportion of commercial lending which related to investment property purchase fell to 25% of all commercial lending, having reached a peak of 31.4% in late 2014.

However, bearing in mind total commercial lending fell in the month, we see that owner occupied lending is now growing considerably faster (1.3%), compared with investment lending (down 2.4% and $11.4 bn) and commercial lending in aggregate is down 0.34%, but the non-investment housing segment rose 0.38% (to $32.7 bn).

If investment lending continues to slow, this will put more pressure on commercial lending growth, or create space for other lending to business, depending on your point of view. Or will the banks simply continue to chase owner occupied refinancing, the easy option? That said, lending to business ex. investment housing did grow, if but a little in the month. We need much stronger movement here to drive productive growth.